Acute Repetitive Seizures Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

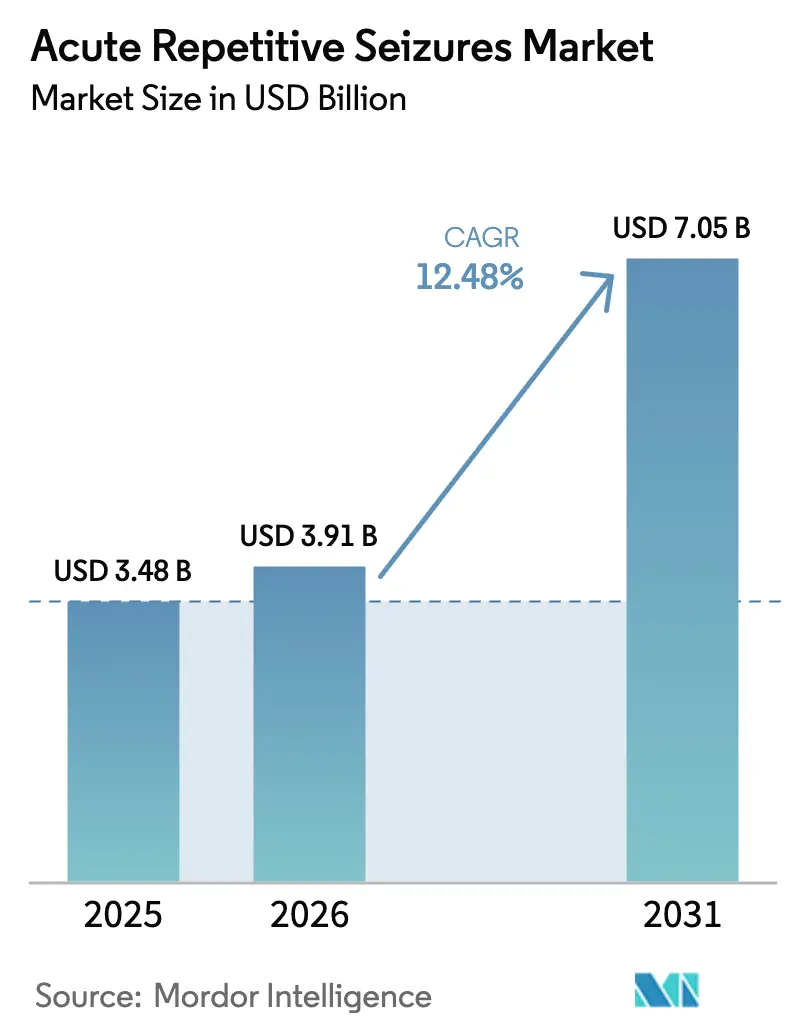

| Market Size (2026) | USD 3.91 Billion |

| Market Size (2031) | USD 7.05 Billion |

| Growth Rate (2026 - 2031) | 12.48% CAGR |

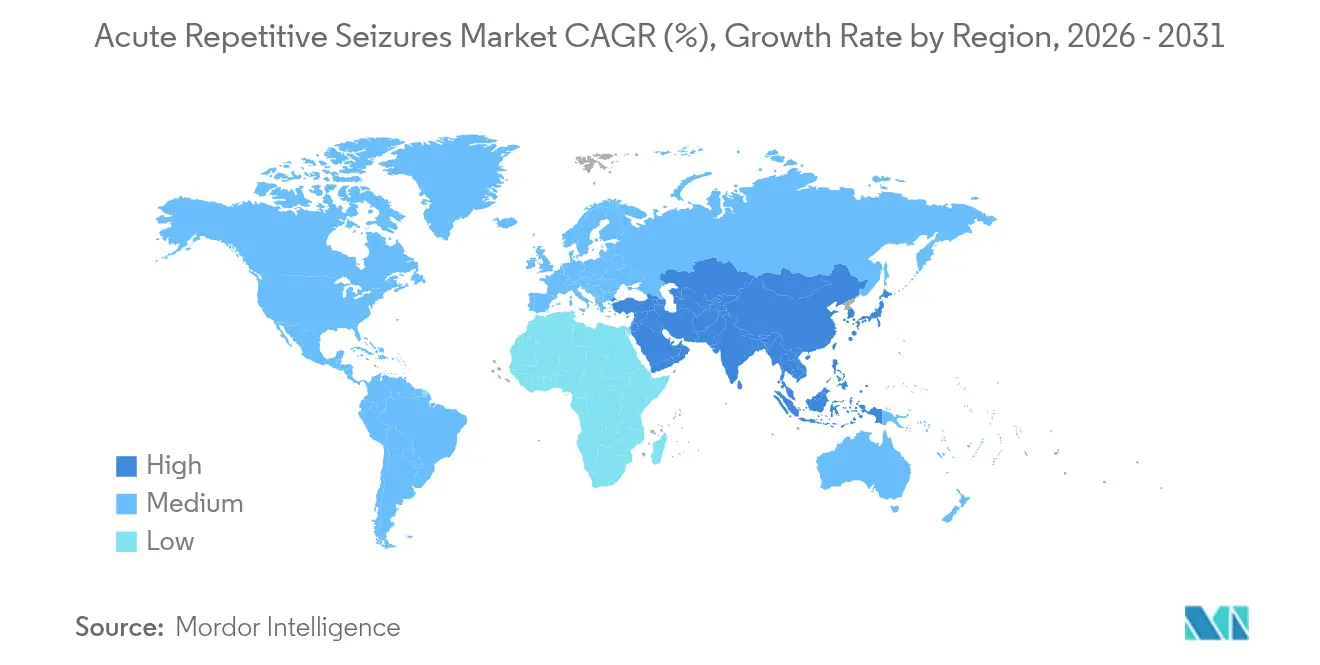

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

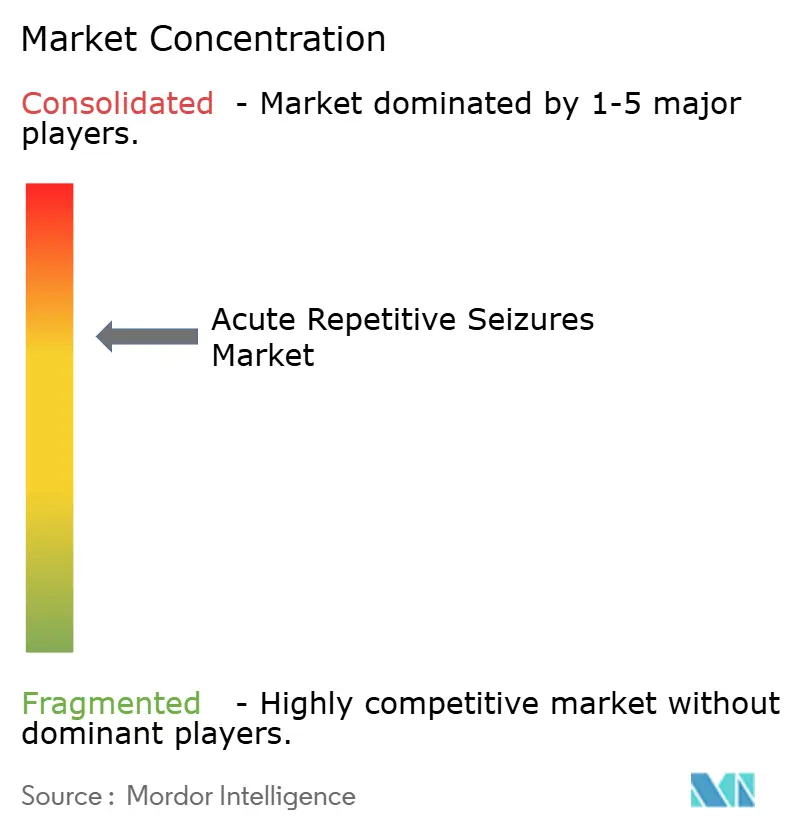

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acute Repetitive Seizures Market Analysis by Mordor Intelligence

Acute repetitive seizures market size in 2026 is estimated at USD 3.91 billion, growing from 2025 value of USD 3.48 billion with 2031 projections showing USD 7.05 billion, growing at 12.48% CAGR over 2026-2031. Adoption accelerates as intranasal and buccal rescue therapies make out-of-hospital intervention faster and more acceptable, while aging populations drive a steady influx of first-time seizure patients. Regulatory agencies now prioritize patient-centric delivery formats, illustrated by multiple United States FDA approvals for diazepam nasal sprays and buccal films in 2024-2025. Investment in novel molecules and nanocarrier technologies broadens the pipeline, addressing the 40% of patients who remain refractory to standard antiseizure medicines. At the same time, legislative mandates for seizure-action plans in schools and workplaces institutionalize demand for easy-to-administer rescue products.

Key Report Takeaways

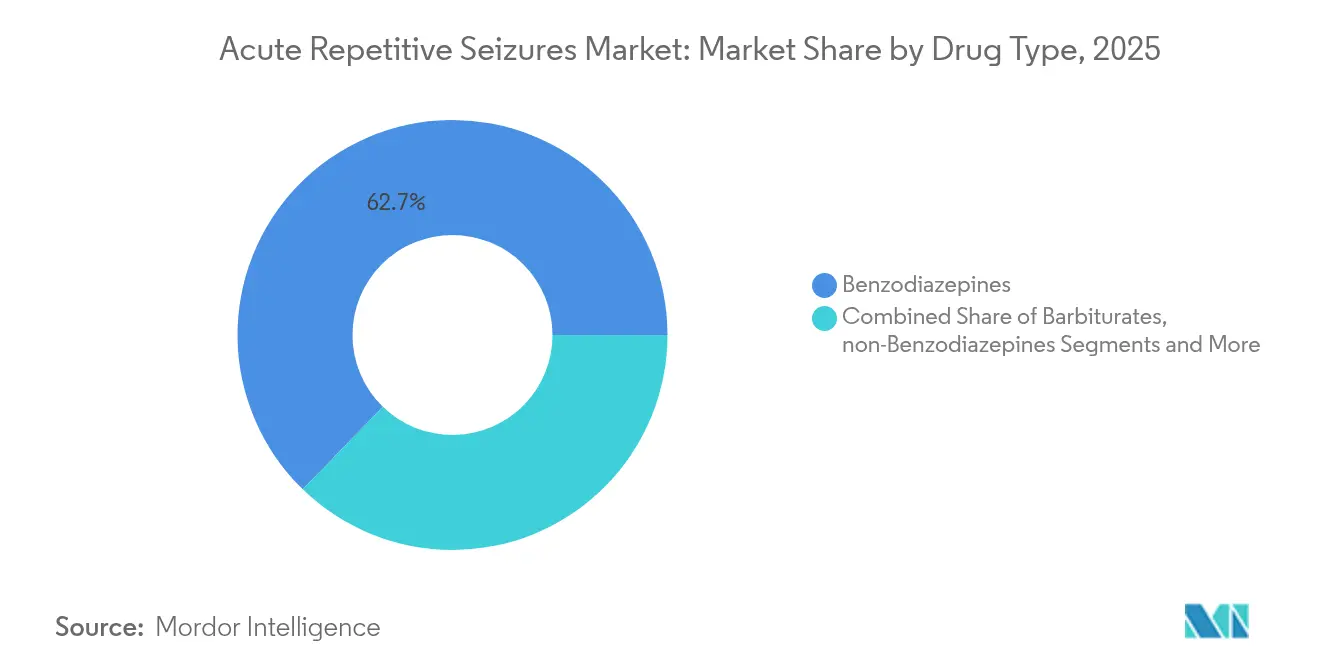

- By drug type, benzodiazepines led with 62.74% revenue share in 2025, while non-benzodiazepines are projected to expand at a 14.12% CAGR through 2031.

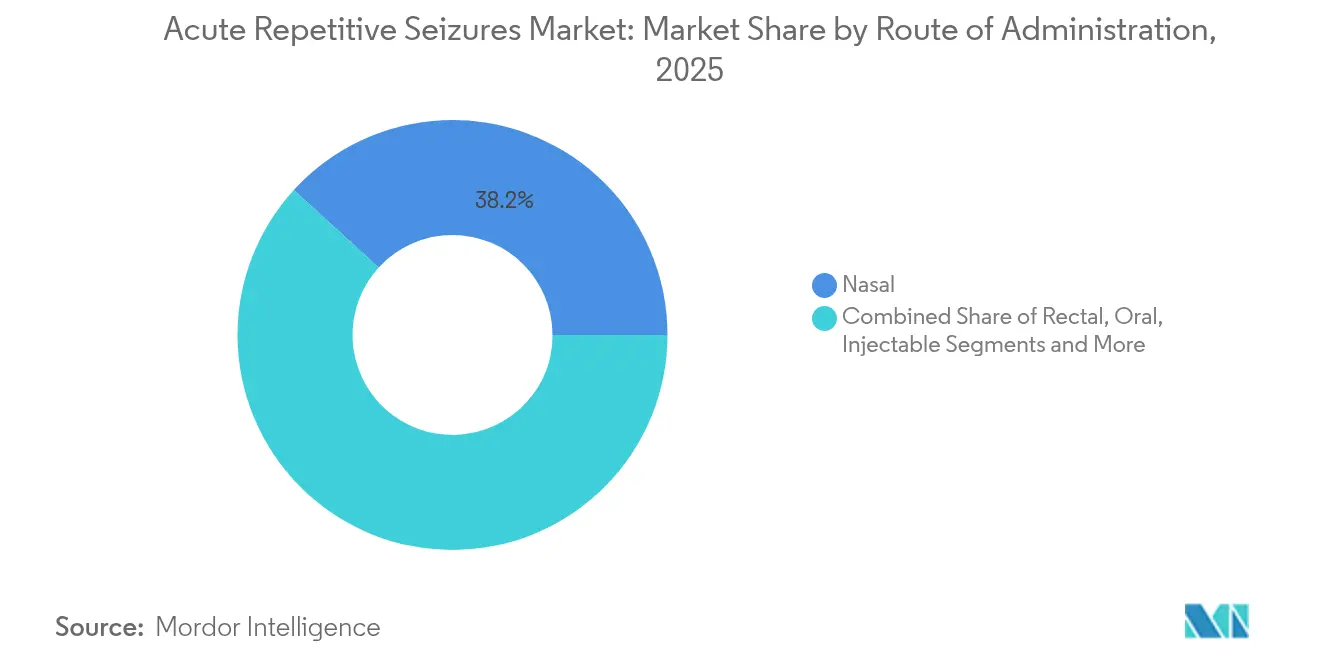

- By route of administration, the nasal segment captured 38.21% of the acute repetitive seizures market share in 2025 and is advancing at a 13.32% CAGR through 2031.

- By distribution channel, hospital pharmacies held 48.42% share of the acute repetitive seizures market size in 2025, whereas online pharmacies are forecast to expand at a 15.55% CAGR to 2031.

- By geography, North America accounted for 45.78% of the acute repetitive seizures market in 2025, and Asia-Pacific is poised to grow at a 14.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Acute Repetitive Seizures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden Of Seizure Disorders & Ageing Population | + 2.8% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Rapid FDA Approvals Of Intranasal / Buccal Rescue Benzodiazepines | + 3.2% | North America, expanding to Europe & Asia-Pacific | Medium term (2-4 years) |

| Growing R&D Investment In Novel Antiseizure Molecules & Delivery Tech | + 2.1% | Global, led by North America & Europe | Long term (≥ 4 years) |

| Patient / Caregiver Shift Toward Non-Invasive Rapid-Onset Rescue Formats | + 1.9% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Mandated Seizure-Action Plans In Schools & Workplaces | + 1.4% | North America, expanding to Europe & Australia | Medium term (2-4 years) |

| AI-Enabled Wearables Triggering Auto-Delivery Devices | + 1.3% | North America & Europe, early pilot programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising burden of seizure disorders & ageing population

Global epilepsy prevalence climbed 29.61% between 1990 and 2024, reaching 50 million people, with incidence gains most pronounced in the 75-79 age bracket.[1]Ling-zhi Yang et al., “Global Burden of Epilepsy Across All Age Groups,” Frontiers in Neurology, frontiersin.org Nearly 24% of new-onset epilepsy now arises after age 60.[2]Rani A. Sarkis and Matthew Schrettner, “Seizures and Epilepsy in the Elderly,” Practical Neurology, practicalneurology.com The demographic shift raises demand for rescue medicines formulated for seniors who often juggle polypharmacy and heightened sensitivity to sedatives. Incidence of acute symptomatic seizures among adults older than 60 sits at 0.55–1 per 1,000 person-years, reinforcing the value of community-deployable treatments. Health systems answer by creating late-onset epilepsy clinics and integrating cognitive screening into seizure pathways. Together these developments anchor long-run growth in the acute repetitive seizures market.

Rapid FDA approvals of intranasal / buccal rescue benzodiazepines

Between 2024 and 2025 the FDA approved Libervant diazepam buccal film and widened the Valtoco nasal spray indication to children aged 2-5, sharply expanding rescue options. Clinical trials show diazepam nasal spray posts the highest single-dose success rate among approved cluster-control formulations. Filing activity mirrors the US trajectory, as Japan’s Aculys Pharma submitted a diazepam nasal spray dossier in September 2024. Quicker reviews shorten launch curves and lift physician confidence, undergirding a 3.2% positive push to the forecast CAGR.

Growing R&D investment in novel antiseizure molecules & delivery tech

Biopharma allocated USD 53.23 billion to neurology and psychiatry pipelines, with USD 48.71 billion earmarked for pharmacological products. Nanocarriers such as stimulus-responsive niosomes improve blood–brain targeting, reducing systemic toxicity. Praxis Precision Medicines advances candidates like vormatrigine for focal onset seizures and relutrigine for developmental epileptic encephalopathies. AI-driven compound screening compresses discovery timelines, enabling quicker translation of academic findings into clinical candidates. These dynamics widen the pipeline and lift market expectations.

Patient / caregiver shift toward non-invasive rapid-onset rescue formats

Studies comparing intranasal diazepam with rectal gel indicate faster seizure-cluster resolution and stronger caregiver satisfaction for the former.[3]Nancy Santilli et al., “Use of Intranasal Rescue Therapy in Schools,” PubMed, pubmed.ncbi.nlm.nih.govPrivacy considerations in schools and workplaces motivate substitution away from rectal formulations. Survey data covering 49,314 US school nurses shows rectal diazepam experience at 45.7% versus 9.3% for diazepam nasal sprays, implying ample headroom for uptake. High bioavailability enhancers like Intravail® further justify the shift. Together these factors reinforce non-invasive routes as the preferred community option.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Price & Limited Reimbursement Of Branded Rescue Products | -1.8% | Global, most pronounced in North America | Short term (≤ 2 years) |

| Respiratory-Depression & Abuse-Potential Safety Constraints | -1.2% | Global, with stricter regulations in Europe | Medium term (2-4 years) |

| Low Awareness & Training Among Caregivers And School Staff | -0.9% | Global, particularly in emerging markets | Medium term (2-4 years) |

| Compounding-Pharmacy Intranasal Mixes Eroding Branded Pricing Power | -0.7% | North America, expanding to Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High price & limited reimbursement of branded rescue products

Branded antiseizure medicine prices rose from USD 8.71 to USD 15.45 between 2013 and 2023, while generic alternatives fell from USD 1.39 to USD 1.25, widening the cost gap by 3,419%. Nayzilam remains brand-only until 2028, hindering generic erosion. Insurers often require prior authorization or step therapy, delaying access. Advocacy groups lobby to cap out-of-pocket costs under Medicare Part D’s protected-classes rule, but resolution in the near term is uncertain.

Respiratory-depression & abuse-potential safety constraints

FDA alerts highlight additive respiratory risk when benzodiazepines are combined with opioids. Benzodiazepine initiators show a 101% rise in sudden cardiac arrest versus non-users. Withdrawal following abrupt discontinuation may boost mortality by 1.6 times in opioid-treated populations. These findings reinforce prescriber caution and may steer certain patients toward non-benzodiazepine alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Benzodiazepines Sustain Dominance but Innovation Gains Steam

Benzodiazepines accounted for 62.74% of the acute repetitive seizures market in 2025. Their fast onset and proven efficacy underpin hospital and community reliance. Yet, non-benzodiazepines are tracking a 14.12% CAGR to 2031, propelled by differentiated mechanisms and fewer respiratory warnings. The FDA approval of Ztalmy ganaxolone for CDKL5 deficiency delivered the first neuroactive steroid option and reinforced investor appetite. Sales jumped 125% year-on-year to USD 7.5 million in Q1 2024. As additional agents advance, the acute repetitive seizures market size for non-benzodiazepines is set to expand sharply, although benzodiazepines will retain a meaningful clinical foothold for refractory emergencies.

A sizeable hospital subset continues using barbiturates during refractory status epilepticus, preserving a niche yet stable revenue stream. Emerging classes, including selective sodium-channel blockers and neuropeptide modulators, move through Phase II pipelines. Companies dedicate companion diagnostics to match mechanisms with seizure phenotypes, illustrating the pivot toward precision treatment within the broader acute repetitive seizures industry.

By Route of Administration: Nasal Delivery Becomes the Community Standard

The nasal segment held 38.21% of the acute repetitive seizures market share in 2025. Bio-adhesive sprays leveraging permeation enhancers deliver drug to systemic circulation within minutes, a critical trait for seizure clusters. Clinical audits find intranasal diazepam achieves single-dose cluster control more consistently than rectal gel, lifting caregiver confidence. Buccal delivery is the fastest riser, thanks to Libervant’s film technology enabling absorption through oral mucosa. Rectal formulations lose ground in schools and public settings due to privacy concerns.

Injectable routes remain indispensable for inpatient escalation. Oral rescue pills are limited by swallowing difficulty during seizures but find utility in planned taper protocols. Forward-looking R&D explores nanoparticle-loaded sprays and thermosensitive gels that further enhance mucosal retention. As these formats commercialize, the acute repetitive seizures market size attributable to non-parenteral routes could overtake injections within the decade.

By Distribution Channel: Digital Platforms Accelerate Access

Hospital pharmacies dominated with 48.42% revenue in 2025 because emergency departments require 24-hour stock. Nevertheless, online pharmacies are growing at 15.55% CAGR, propelled by telehealth adoption and direct-to-patient fulfillment. Retail chains occupy the middle ground, providing counseling while handling maintenance scripts. Specialized rare-disease pharmacies manage cold-chain-sensitive products like ganaxolone, offering adherence coaching to caregivers.

COVID-19 normalized remote prescribing, and insurers now reimburse virtual neurology visits, supporting digital expansion. Secure e-prescribing platforms mitigate controlled-substance diversion risk, a historic barrier for benzodiazepines. As logistics networks mature, acute repetitive seizures market participants are building omnichannel capabilities that merge hospital procurement with at-home resupply.

Geography Analysis

North America generated 45.78% of global revenue in 2025, buoyed by comprehensive insurance coverage and structured seizure-action mandates. The United States accounted for the lion’s share, supported by rapid FDA review cycles and strong advocacy-group lobbying. Canada follows a similar path, with provincial programs funding intranasal diazepam for pediatric clusters. Academic centers collaborate with startup device firms, accelerating closed-loop therapy trials.

Europe ranks second, with Germany, France, and the United Kingdom leading adoption of novel buccal and nasal products. Harmonized labeling through the European Medicines Agency eases multi-country launches, while local reimbursement decisions shape speed to market. National epilepsy strategies emphasize school-based seizure training, reinforcing volume for community-use sprays.

Asia-Pacific posts the highest regional growth at 14.01% CAGR. China’s July 2024 approval of ganaxolone for CDKL5 deficiency marks a milestone, reflecting greater regulatory openness. Japan’s regulatory review of diazepam nasal spray targets adults outside hospital settings, potentially opening new channels. Rising middle-class income and urban hospital expansion drive formulary uptake across India and Southeast Asia, though reimbursement variability tempers near-term penetration.

The Middle East and Africa remain nascent, constrained by specialist shortages and variable medicine supply chains. Governments in the Gulf Cooperation Council introduce central tender systems for rescue sprays, offering future scale. South America grows steadily, led by Brazil, where public health programs fund diazepam nasal sprays for epileptic cluster emergencies.

Competitive Landscape

Competition blends established multinationals with agile neuroscience specialists. Lundbeck’s USD 2.6 billion purchase of Longboard Pharmaceuticals brought Phase III bexicaserin, deepening its seizure portfolio. Johnson & Johnson’s USD 14.6 billion acquisition of Intra-Cellular Therapies underscores Big Pharma’s renewed neurological focus. UCB’s acquisition of Engage Therapeutics secured Staccato Alprazolam, a breath-actuated inhalation device for rapid seizure termination.

Technology convergence differentiates challengers. Neuroelectrics’ wearable headcap achieved 41% median seizure reduction in FDA-approved trials, positioning the firm as a device-drug partner. Praxis Precision Medicines combines genetics-guided discovery with digital phenotyping. Meanwhile, Marinus defends its ganaxolone patents against rival claims, signaling high intellectual-property stakes.

Partnership models evolve. Neurelis monetized USD 208 million of Intravail royalty streams to fund commercialization, illustrating creative financing routes for mid-cap innovators. Contract manufacturers scale spray and film technologies, shortening lead times for regional launches. As players compete on molecule novelty, route convenience, and digital integration, brand equity increasingly hinges on seamless caregiver experiences within the broader acute repetitive seizures market.

Acute Repetitive Seizures Industry Leaders

Aquestive Therapeutics

Eisai Co., Ltd

H. Lundbeck A/S

Neurelis, Inc.

UCB S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Neurelis received United States FDA approval for VALTOCO diazepam nasal spray in patients aged 2 years and older.

- December 2024: Immedica Pharma agreed to acquire Marinus Pharmaceuticals, adding ZTALMY ganaxolone to its rare-disease portfolio, with deal completion expected in Q1 2025.

- April 2024: Aquestive Therapeutics gained FDA approval for Libervant diazepam buccal film for seizure clusters in children aged 2–5 years.

Global Acute Repetitive Seizures Market Report Scope

As per the scope of the report, acute repetitive seizures are characterized by multiple seizures happening within a brief timeframe, usually within 24 hours. This condition can be triggered by several factors, such as acute brain injuries, infections, metabolic imbalances, or withdrawal from specific substances. In contrast to epilepsy, where seizures are recurrent, acute repetitive seizures are often instigated by immediate medical concerns.

The acute repetitive seizures market is segmented by drug type, routes of administration, distribution channel, and geography. By drug type, the market is segmented into benzodiazepines, antiepileptic drugs, barbiturates, and other drug types. The other drug types segment includes anticonvulsants and general anesthesia drugs. By route of administration, the market is segmented into oral, injectable, and other routes of administration. The other routes of administration segment includes nasal, rectal, buccal, and parenteral. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. By geography, the market is divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market sizing and forecasts have been done based on value (USD).

| Benzodiazepines |

| non-Benzodiazepines |

| Barbiturates |

| Other Drug Types (anticonvulsants, anaesthetic drugs) |

| Oral |

| Injectable |

| Nasal |

| Rectal |

| Buccal |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Type | Benzodiazepines | |

| non-Benzodiazepines | ||

| Barbiturates | ||

| Other Drug Types (anticonvulsants, anaesthetic drugs) | ||

| By Route of Administration | Oral | |

| Injectable | ||

| Nasal | ||

| Rectal | ||

| Buccal | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the acute repetitive seizures market?

The acute repetitive seizures market was valued at USD 3.91 billion in 2026 and is projected to climb to USD 7.05 billion by 2031.

Which drug type leads the market?

Benzodiazepines held 62.74% of revenue in 2025, maintaining the leading position because of rapid onset and strong clinical familiarity.

Why is nasal delivery gaining popularity?

Intranasal sprays offer fast absorption, privacy, and ease of administration, resulting in a 38.21% market share in 2025 and the highest growth rate among delivery routes.

Which region is expanding the fastest?

Asia-Pacific is forecast to grow at a 14.01% CAGR due to expanding healthcare infrastructure and broader seizure disorder recognition.

What are the main restraints on market growth?

High branded drug prices, respiratory safety concerns, limited caregiver training, and competition from compounded intranasal formulations exert downward pressure on growth.

Page last updated on: