Active Geofencing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.7 Billion |

| Market Size (2031) | USD 6.97 Billion |

| Growth Rate (2026 - 2031) | 20.94% CAGR |

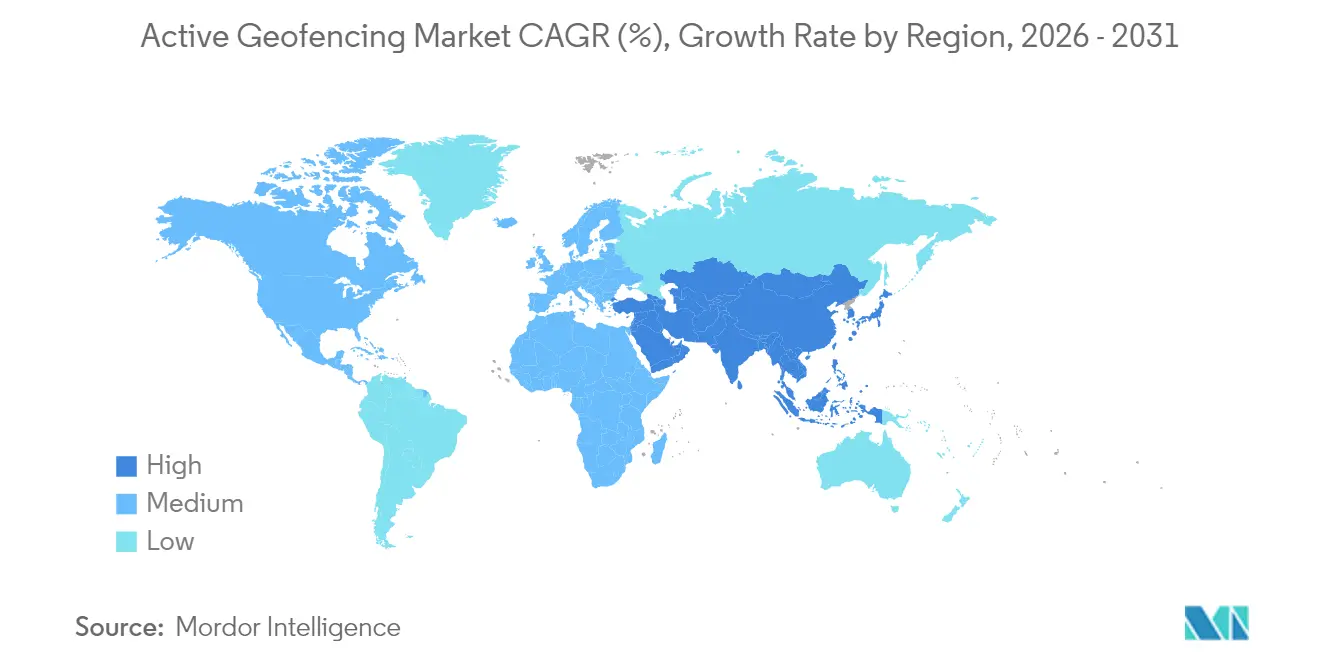

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Active Geofencing Market Analysis by Mordor Intelligence

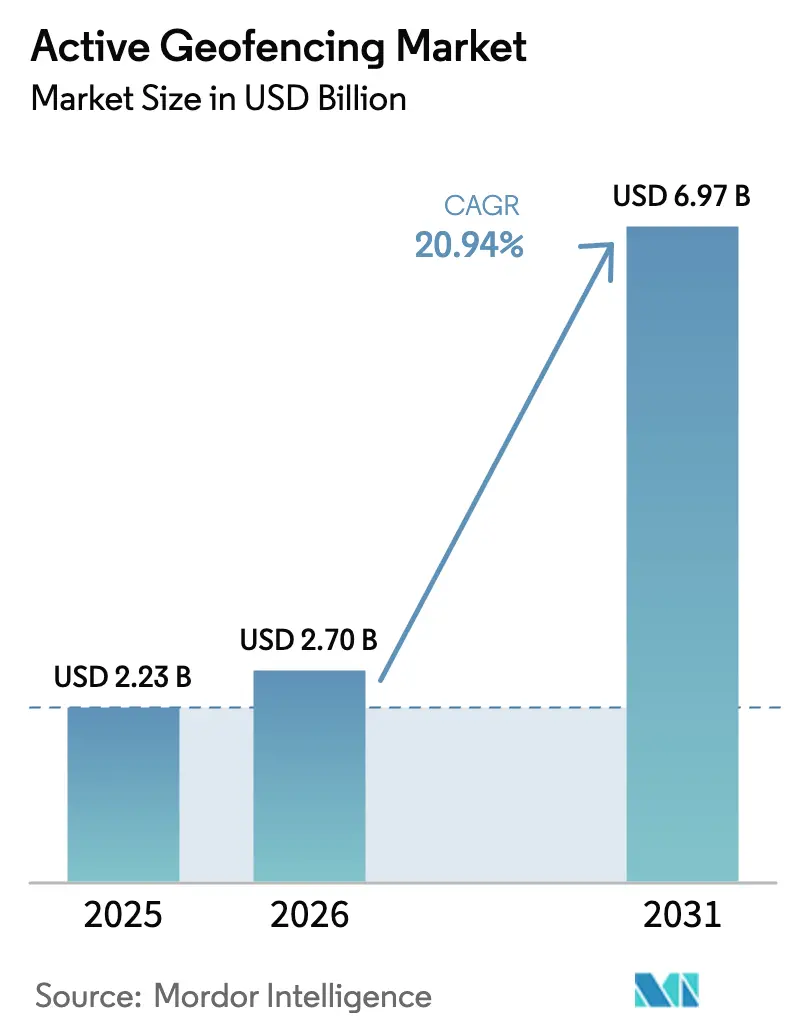

The active geofencing market size is expected to grow from USD 2.23 billion in 2025 to USD 2.7 billion in 2026 and is forecast to reach USD 6.97 billion by 2031 at 20.94% CAGR over 2026-2031. The expansion reflects how location technology has progressed from simple proximity triggers to real-time spatial intelligence layers that support decision-making in logistics, retail, healthcare, and autonomous systems. Growing smartphone penetration, 5G roll-outs, and cloud-native development tools continue to reduce deployment friction, while government smart-city programs push adoption of geo-aware public services. Enterprise strategies now emphasize monetizing first-party location data, illustrated by Google’s plan to earn USD 11 billion a year from Maps advertising, and by retailers that report three-fold lift in customer acquisition when campaigns include geofence triggers. Parallel advances in drone flight safety, indoor positioning, and fleet telematics broaden the number of industrial problems that geofencing can solve, sustaining double-digit growth through the decade.

Key Report Takeaways

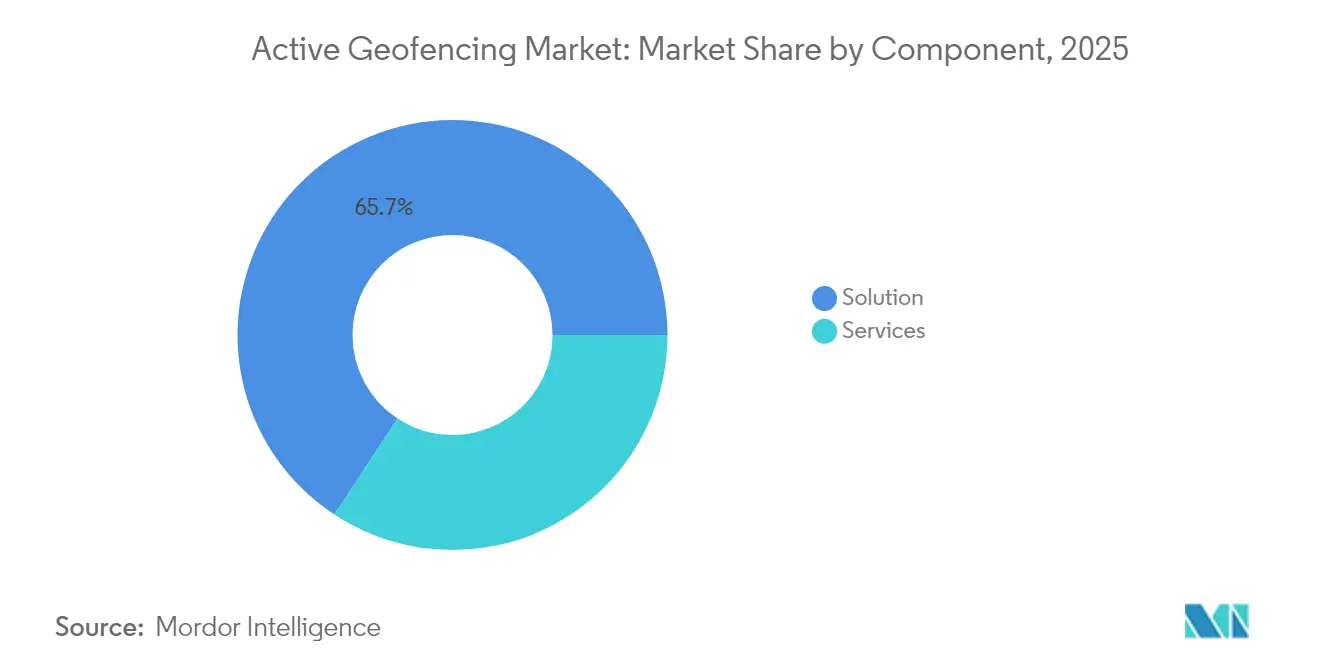

- By component, solution accounted for 65.74% of the active geofencing market share in 2025, while services is projected to grow at 17.55% CAGR over 2026-2031.

- By deployment mode, cloud infrastructure accounted for 65.95% share of the active geofencing market size in 2025; hybrid models are rising at 19.11% CAGR to 2031.

- By technology, GPS/GNSS held 41.76% of the active geofencing market share in 2025, while UAV geofencing is projected to compound at 22.95% CAGR to 2031.

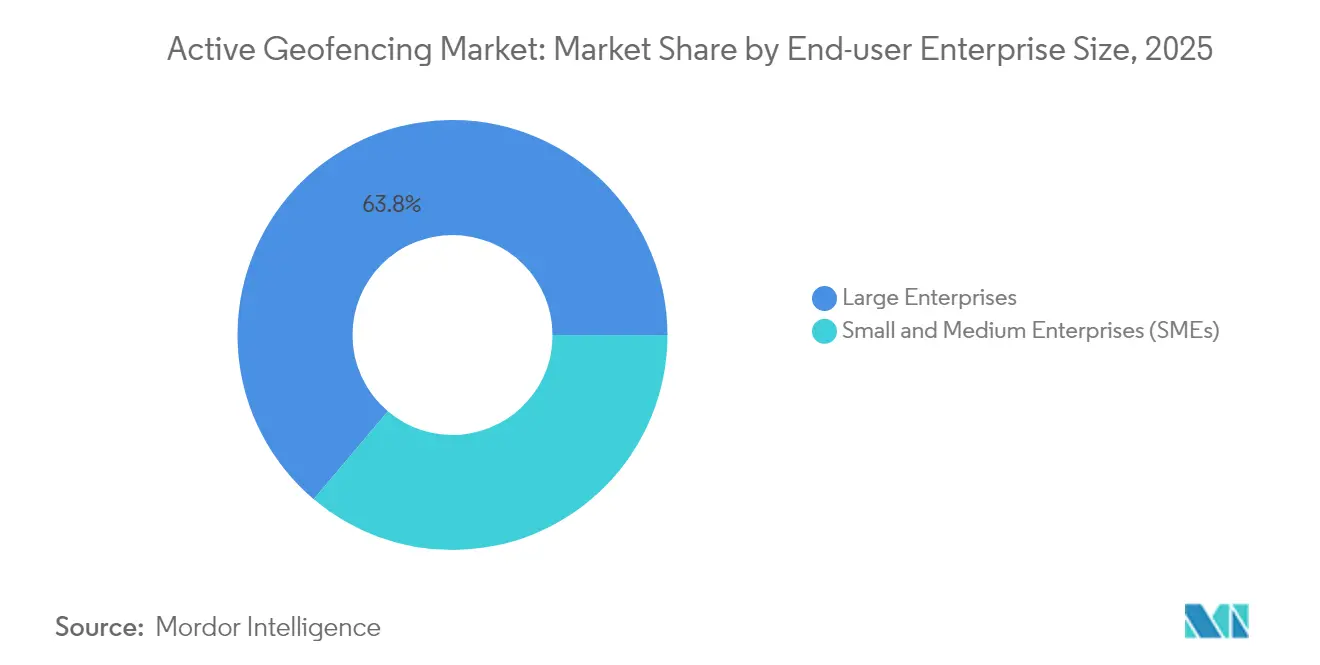

- By end-user enterprise size, large enterprises controlled 63.83% share of the active geofencing market size in 2025, whereas SMEs are advancing at 17.92% CAGR over 2026-2031.

- By end-user industry vertical, retail and e-commerce commanded 25.88% share of the active geofencing market size in 2025, while healthcare and life sciences are set to grow at 21.38% CAGR to 2031.

- By geography, North America led with 38.02% revenue share in 2025; Asia Pacific is forecast to expand at a 17.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Active Geofencing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IoT-enabled mobile devices expand precise location data | +4.2% | Global, led by Asia Pacific and North America | Medium term (2-4 years) |

| Hyper-local marketing demand from retailers and QSRs | +3.8% | North America and Europe, spreading to Asia Pacific | Short term (≤ 2 years) |

| Geofencing in fleet telematics and last-mile logistics | +3.5% | Global, strong in North America and Europe | Medium term (2-4 years) |

| Drone-based industrial inspections need dynamic safety zones | +2.9% | North America and Europe, emerging Asia Pacific | Long term (≥ 4 years) |

| Smart-city mandates for geo-aware public services | +2.7% | Europe, followed by Asia Pacific | Long term (≥ 4 years) |

| Spatial computing and AR platforms require real-time layers | +2.1% | North America and Europe first movers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of IoT-enabled Mobile Devices

Roughly 30 billion connected devices will be active worldwide by 2025, providing a dense sensor fabric that feeds high-granularity location streams into geofencing engines. Modern smartphones fuse GPS, cellular, Wi-Fi RTT, and Bluetooth Low Energy to achieve sub-meter accuracy, enabling safety-critical use cases such as hospital asset tracking and industrial automation. 5G’s ultra-low latency further tightens geofence response times, ensuring that alerts or control messages execute inside mission-critical thresholds.

Rising Demand for Hyper-local Marketing

Retailers and quick-service restaurants use geofencing to push time-sensitive offers that triple acquisition rates versus untargeted messaging. Lower CPMs than print or out-of-home media, combined with measurable foot-traffic attribution, have led major chains to embed geofencing into omnichannel playbooks. Dynamic radius sizing based on real-time travel time models also raises message relevance, sustaining high engagement while lowering ad waste[1]Esri. "New Location Services and Updated Data: Explore What's New for ArcGIS Location Services." September 5, 2025..

Integration with Fleet Telematics and Last-mile Logistics

Logistics operators overlay geofences on depots, customer sites, and congestion hot-spots so that telematics units can automate driver check-ins, trigger curbside pickup workflows, and flag unauthorized vehicle use. Amazon Location Service now offers predictive entry alerts that anticipate a truck’s arrival, letting warehouse teams stage orders more efficiently[2]AWS Community. "Enhancing Curbside Pickup with Amazon Location Service's Enhanced Location Integrity features." May 31, 2024. . Machine-learning models that mine historic route data are improving ETA accuracy, elevating customer satisfaction and reducing overtime costs.

Expansion of Drone-based Inspections

Regulators worldwide require unmanned aircraft to respect no-fly zones around airports, critical infrastructure, and temporary emergency sites. DJI’s 2025 shift from hard locks to operator-acknowledged “Enhanced Warning Zones” illustrates how policy is evolving toward operator responsibility backed by richer situational data [3]DJI ViewPoints Team. "DJI Updates GEO System in U.S. Consumer & Enterprise Drones." January 13, 2025. . Sub-centimeter GNSS corrections from networks such as Geodnet let drones perform precise corridor inspections while automatically re-routing if a new restriction is published.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tighter consumer-privacy rules on continuous tracking | -2.8% | Europe first, then North America | Short term (≤ 2 years) |

| Battery drain and performance issues in always-on apps | -1.9% | Global, acute in mobile-first Asia Pacific | Medium term (2-4 years) |

| Fragmented indoor-positioning standards | -1.4% | Global | Medium term (2-4 years) |

| Shortage of skilled spatial-analytics talent | -1.1% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened Consumer-privacy Regulations

The FTC’s prohibition on selling sensitive geolocation data, combined with multimillion-dollar penalties levied on U.S. carriers, compels vendors to invest in granular consent management and on-device anonymization. Europe’s GDPR remains the global template, requiring explicit opt-in for location tracking and rigorous data minimization. Adapting active geofencing workflows to multiple state-level rules in the United States adds compliance overhead that can slow roll-outs.

Battery-drain and Device-performance Concerns

Continuous GPS polling can cut smartphone battery life by more than one-third in weak-signal environments. Modern SDKs mitigate the issue by switching to low-power sensors when movement is unlikely and by clustering geofence edges to reduce wake-ups. Edge inference models now predict motion patterns locally so that cloud requests only occur when a boundary breach is probable, saving energy without degrading accuracy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solution Accelerate Through Integration Complexity

Solution contributed 65.74% of 2025 revenue, and the services segment is on track for 17.55% CAGR as enterprises outsource design, deployment, and optimization tasks that demand scarce spatial-analytics expertise. System integrators bundle compliance audits, low-code app development, and managed monitoring so that customers can launch campaigns in weeks instead of quarters. In regulated sectors, service providers fine-tune consent flows and encryption settings to pass HIPAA or PCI audits on the first attempt. Rising demand for outcome-based contracts is encouraging vendors to peg fees to lift in foot traffic or reduction in theft incidents, aligning incentives and deepening client stickiness.

Platform vendors also promote certification programs to enlarge the talent pool, while universities add micro-credentials in location engineering. These initiatives ease the entry barrier for small businesses and expand the overall active geofencing market. Continuous optimization services updating polygon boundaries, modifying dwell-time rules, and A/B testing creative assets ensure that campaigns remain effective as urban density, traffic patterns, or store footprints evolve

By Deployment Mode: Hybrid Models Bridge Security and Scalability

Cloud retained 65.95% share in 2025 thanks to elastic scaling and global coverage, but hybrid architectures are growing fastest at 19.11% CAGR because they let firms process sensitive coordinates on-premise while offloading analytics to the cloud. Hospitals, for example, keep patient-level location events inside a private subnet yet use cloud AI to forecast bed demand. Financial institutions follow a similar pattern: geofence checks for fraud prevention run locally, whereas aggregated heat maps go to the cloud for marketing insights.

Edge devices routers, gateways, and smartphones now host lightweight brokers that decide, in milliseconds, where to execute each location rule. This adaptive routing lowers latency for safety-critical alerts and trims egress fees. As national data-sovereignty laws proliferate, vendors bundle geo-fencing policy engines with data-residency controls, thereby future-proofing large deployments across multiple jurisdictions.

By Technology: UAV Systems Redefine Precision Requirements

GPS/GNSS contributed 41.76% revenue in 2025 and remains indispensable for outdoor use cases. Yet the rapid ascent of drone geofencing, slated for 22.95% CAGR, is reshaping engineering priorities. Autonomous flights for infrastructure surveys or emergency deliveries need centimeter-grade accuracy and dynamic no-fly zone ingestion. Vendors now blend RTK-GPS with vision-based SLAM so that drones sustain positional certainty even when satellite signals fade under bridges or in urban canyons.

Wi-Fi RTT and BLE beacons dominate indoor deployments, where hand-held scanners, wheelchairs, or forklifts must be located within rooms rather than buildings. Shipments of BLE beacons are set to surpass 530 million units annually by 2030, underscoring how indoor use cases complement traditional GPS. Hybrid engines seamlessly switch between outdoor and indoor signals, giving workers and consumers uninterrupted experiences as they move through mixed environments.

By End-user Enterprise Size: SMEs Embrace Cloud-native Solutions

Large enterprises accounted for 63.83% of 2025 revenue because they could afford bespoke integrations with ERP, CRM, and security stacks. Retail chains deploy thousands of store-level geofences that adjust marketing spend in real time, while airlines link air-side zones to staff-scheduling platforms for optimized turnaround times.

Small and medium enterprises, however, represent the most vibrant growth pocket at 17.92% CAGR, propelled by subscription-based SaaS that masks the plumbing. Food trucks can trigger curbside promotions without hiring developers, and boutique clinics can automate patient check-in when visitors enter the parking lot. Financing programs that bundle software fees into payment-processor charges reduce capital hurdles even further, unlocking long-tail expansion for the active geofencing market.

By End-user Industry Vertical: Healthcare Accelerates Through Regulatory Drivers

Retail and e-commerce dominated with 25.88% revenue share in 2025 as chains harness real-time proximity data to raise store conversions and manage inventory buffers. Cart-level loyalty IDs sync with location pings so that offers reflect both purchase history and immediate context, blending online and offline profiles seamlessly.

Healthcare and life sciences is the fastest mover, projected at 21.38% CAGR, because regulators now permit digital therapeutics that depend on verified patient location. Geofences around dementia wards alert nurses when residents approach restricted exits, while cold-chain sensors tagged to vaccine boxes raise alarms if they leave controlled-temperature corridors. Integration with electronic health records means these events auto-document, eliminating manual charting and reducing liability. The high stakes in patient safety justify premium service tiers and create a defensible niche within the broader active geofencing industry.

Geography Analysis

North America held 38.02% revenue share in 2025 owing to widespread 5G coverage, mature advertising ecosystems, and strong enterprise IT budgets. U.S. retailers report double-digit foot-traffic lift when adding geofencing to loyalty apps, and logistics providers routinely geofence fulfilment centres to shave loading-dock idle time. The FTC’s clear enforcement stance creates predictable compliance rules that let vendors innovate without guessing the regulatory direction. Canada leverages geofencing in government digital-service portals, while Mexico’s e-commerce boom fuels adoption among parcel carriers and mall operators.

Asia Pacific is the fastest-growing region at 17.01% CAGR through 2031, helped by urbanization, smartphone saturation, and megacity smart-infrastructure projects. China’s “super-apps” embed geofencing across payments, ride-hailing, and local commerce, normalizing the technology for 1 billion consumers. India’s Unified Logistics Interface Platform links carrier APIs with geofence-verified delivery milestones, streamlining regulatory filings and reducing demurrage. Advanced 5G private-network pilots in South Korea and Japan support factory automation, where micro-geofences around robotic workcells ensure worker safety and asset protection.

Europe maintains steady momentum under a privacy-first paradigm. Cities such as Stockholm and Barcelona use geofenced “green zones” to redirect polluting vehicles, cutting congestion and emissions. Manufacturers integrate geofencing into Industry 4.0 lines for predictive maintenance and accident prevention. The European Commission’s push for common urban-mobility data layers is spurring interoperable geofencing standards, enhancing cross-border logistics efficiency. Eastern European logistics hubs and Nordic renewable-energy plants add to a diverse set of regional deployments.

Regulatory Landscape

Active geofencing deployments are increasingly shaped by privacy and law-enforcement access rules that treat precise geolocation as sensitive data. In the United States, the regulatory posture is tightening through both federal enforcement and state-level statutes, which raises compliance requirements around consent, minimization, and downstream sharing of location data. On the public-safety side, U.S. courts and legislatures are also scrutinizing geofence warrants, with the U.S. Supreme Court granting certiorari in Chatrie (January 2026) on Fourth Amendment particularity questions, and model frameworks emerging to formalize judicial oversight and limit de-anonymization pathways.

In Europe, GDPR remains the anchor for location-data processing obligations, while the EU AI Act (Regulation (EU) 2024/1689) adds requirements for certain geospatial AI use cases classified as high-risk, including data governance, technical documentation, and human oversight. At the infrastructure layer, policy shifts around geospatial data access and interoperability are progressing alongside these compliance obligations, including changes to EU geospatial tooling and validation practices tied to broader data portal consolidation. Overall, these developments are pushing vendors toward purpose-limited, auditable geofencing workflows, and they continue to influence product choices such as on-device processing and hybrid deployments for data residency and governance.

Competitive Landscape

The active geofencing market is moderately fragmented, with platform giants and focused specialists coexisting. Google, Apple, and Amazon furnish SDKs that developers embed in millions of consumer apps, granting the giants scale advantages in data volume and monetization channels. Google’s goal of USD 11 billion annual Maps ad revenue underscores how geofencing has shifted from technical utility to profit center.

Mid-tier specialists such as Esri, HERE, and TomTom differentiate through high-precision cartography, offline-first runtime engines, and turnkey analytics dashboards. Esri’s tie-up with Microsoft embeds rich spatial functions into mainstream BI workflows, broadening the addressable user base without requiring GIS expertise. HERE and AWS’s USD 1 billion automotive alliance shows how cloud depth and map breadth converge to serve software-defined vehicles that rely on centimeter-grade geofencing for ADAS features.

Niche innovators tackle vertical pain points. Radar Labs offers drop-in mobile SDKs optimized for retail engagement, while Mapsted markets beacon-free indoor positioning that slashes hardware costs. In the drone realm, DJI couples air-space data with on-board obstacle sensing to maintain compliance while preserving operator flexibility. The ecosystem’s diversity supports robust innovation yet keeps average deal sizes manageable, maintaining customer leverage in price negotiations.

Active Geofencing Industry Leaders

-

Bluedot Innovation Pty Ltd

-

IBM Corporation

-

Microsoft Corporation

-

Radar Labs Inc.

-

Infillion, Inc (GIMBLE)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory tightening around the sale and sharing of precise geolocation is creating room for active geofencing solutions that rely on first-party data, explicit consent, and verifiable processing controls. Concrete signals include the FTC’s finalized enforcement resolution affecting Kochava (June 2026), which restricted the sale, licensing, or sharing of sensitive location data without affirmative express consent and required a comprehensive privacy program with board-level reporting. State actions such as Virginia’s SB338 (signed April 2026, effective July 1, 2026) banning the sale of precise geolocation data under the VCDPA are also accelerating a shift from third-party location marketplaces toward consented enterprise and platform-led implementations. That shift is directly strengthening demand for consent management, policy engines, and privacy-by-design SDKs.

At the technology and ecosystem level, opportunities are emerging around network-native geofencing and low-latency triggers aligned with telecom standards, which can reduce reliance on always-on device polling and improve reliability for logistics, mobility, and safety use cases. 3GPP specifications for 5G location services and geofencing triggers (including TS 23.437 and TS 29.515) provide an anchor for operators and API ecosystems to expose standardized capabilities, supplementing cloud-based geofencing stacks already used for fleet telematics and curbside workflows. There is also whitespace in sensitive-site compliance, since multiple U.S. states restrict geofencing around certain medical and other protected locations; vendors that operationalize exclusion zones, configurable purpose limitations, and audit-ready location event handling can differentiate in regulated verticals such as healthcare, BFSI, and government services.

Recent Industry Developments

- May 2026: Epic Charging completed the acquisition of Bluedot Technologies, adding Bluedot’s fleet-focused charging management and payment platform capabilities. The deal supports vertically integrated platforms that combine depot operations, location intelligence, and workflow automation, which can expand adjacent demand for geofencing-driven triggers in fleet and logistics environments.

- July 2025: Esri, Microsoft, and Space42 launched the Map Africa initiative to build a comprehensive basemap of Africa using Microsoft Azure cloud infrastructure and AI. The program expands access to foundational geospatial datasets and tooling, supporting more consistent boundary definition and analytics for scalable geofencing deployments across emerging markets.

- November 2024: IBM and Sustainable Energy for All launched open-source AI models focused on energy and urban development mapping through the IBM Sustainability Accelerator. By accelerating geospatial modeling and data preparation for city-scale planning, the initiative supports the data-layer maturity that underpins geo-aware services, including active geofencing for public-sector and infrastructure use cases.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the active geofencing market is defined as revenues generated from solutions and services that create virtual geographic boundaries and trigger actions when a device or asset enters or exits a defined area, across enterprise and public-sector use cases.

Scope exclusions: Excludes general location-based services that do not use geofence rules, and excludes hardware-only sales when they are not sold as part of an active geofencing solution or service.

Segmentation Overview

-

By Component

- Solution

- Services

-

By Deployment Mode

- Cloud

- On-premise

- Hybrid

-

By Technology

- GPS/GNSS

- Cellular

- Wi-Fi/BLE

- RFID/NFC

- UAV/Drone Geofencing Systems

-

By End-User Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

-

By End-User Industry Vertical

- Banking, Financial Services and Insurance (BFSI)

- Retail and E-commerce

- Transportation and Logistics

- Healthcare and Life Sciences

- Government and Defense

- Industrial Manufacturing

- Media and Entertainment

- Other End-user Industry Vertical

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

-

Asia Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- ASEAN

- Rest of Asia Pacific

-

Middle East and Africa

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

-

Middle East

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by grounding the market in observable signals and common definitions, so later assumptions do not float. We reviewed public technology standards and guidance such as FCC materials on location and wireless networks, NIST cybersecurity references that affect deployment choices, and patent databases to understand feature direction and adoption timing.

We also used sources such as the US Census Bureau and Eurostat for enterprise and workforce baselines, ITU indicators for mobile and connectivity readiness, and public procurement and tender portals to see where government demand is showing up. Company filings, product documentation, and reputable press coverage were then used to track deployment patterns like cloud preference, 5G influence, and privacy prompts that shape opt-in rates. In a few places, paid subscriptions for company financials and news intelligence, and patent coverage, were used to cross-check revenue exposure and product activity. These examples are not exhaustive, and many other public sources were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to test what the desk inputs could not fully confirm, especially pricing logic, adoption pace by vertical, and how deployments are packaged as solutions versus services. We spoke with a mix of solution providers, system integrators, telecom and cloud ecosystem participants, and end users across major regions, and then used follow-up checks when inputs like opt-in rates or subscription churn showed wide variance.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 13% | APAC: 47% |

| Mid tier: 45% | Functional/Unit leaders: 30% | EMEA: 35% |

| Smaller Players: 16% | Managers: 57% | Americas: 18% |

Market-Sizing & Forecasting

Sizing uses a top-down build where enterprise software and location intelligence spending is narrowed using adoption and usage indicators that are specific to active geofencing, and then reconciled with selective bottom-up checks. In practice, we link demand to the installed base of location-aware devices and apps, the share of enterprises running location-triggered workflows, and the split between cloud subscriptions and project-led services, and then convert that into value using observed price ranges.

A few inputs that mattered in the model include smartphone and connected device penetration, 4G and 5G coverage and quality, privacy and consent practices that affect opt-in rates, cloud migration pace, and average contract values by vertical (for example, retail and logistics often scale faster once workflows are standardized). Where vendor revenue disclosure is limited, gaps are handled by using peer benchmarks, partner channel checks, and reasonable revenue-per-customer ranges that are stress-tested in interviews.

For forecasting, scenario analysis is used so optimistic and conservative adoption paths can be mapped to clear drivers like regulation intensity, enterprise mobility budgets, and macro conditions. The final trajectory is adjusted only after the scenarios align with what primary respondents described as realistic procurement cycles and renewal behavior.

Data Validation & Update Cycle

Each key assumption is validated through triangulation across desk signals, interview feedback, and simple arithmetic checks that must reconcile to the same story. When a variable produces an outlier result, it is traced back to its driver, checked for unit or currency issues, and reviewed against independent indicators such as device growth, cloud spend direction, or public-sector tender activity.

Before sign-off, the model is reviewed in multiple steps, including internal peer review for logic and sensitivity, and re-contact is triggered when a major discrepancy remains on pricing, deployment mix, or adoption pace. Reports are refreshed annually, and interim updates are made when material events occur, such as policy changes on location consent or sharp shifts in connectivity rollouts. Right before delivery, a final pass is completed so the figures reflect the latest available information.

Mordor Intelligence's Active Geofencing Market Size Measured Against Other Published Estimates

Published market sizes for active geofencing can look far apart because sources often define what counts as geofencing in different ways, and they also pick different base years and forecasting windows. Currency timing, whether services are counted alongside solutions, and how consent-driven usage is treated can also move the totals.

Bluetooth beacons, NFC tags, and other sensor hardware sold as standalone items sit outside Mordor Intelligence's scope here, which keeps the value tied to active geofencing solutions and services rather than broad location hardware revenues.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.23 B (2025) | |

| Global Research Publisher A | USD 2.16 B (2025) | Often reported as a single topline without consistently separating solution subscriptions from implementation services, which can compress the value if service-heavy deployments are undercounted. |

| Market Data Provider B | USD 1.13 B (2024) | Uses an earlier base year and may apply narrower inclusion around vendor-defined products, which can miss enterprise spend that is bundled into broader location workflow programs. |

The table shows that the spread is mostly explained by what is included, the chosen base year, and how service revenue is treated alongside software. By keeping assumptions tied to observable adoption signals and checking them with interview-driven price and usage ranges, the final number stays transparent and repeatable.

Key Questions Answered in the Report

How large will the active geofencing market be in 2031?

The active geofencing market is projected to reach USD 6.97 billion by 2031.

Which region is expanding fastest in active geofencing?

Asia Pacific is forecast to grow at a 17.01% CAGR through 2031, driven by smart-city investments and widespread smartphone usage.

What deployment mode is gaining the most momentum?

Hybrid architecture is the fastest-growing mode at 19.11% CAGR because it balances data-sovereignty needs with cloud scalability.

Which industry vertical shows the highest future growth?

Healthcare and life sciences lead with a projected 21.38% CAGR thanks to patient monitoring and asset-tracking mandates.

What is the primary regulatory challenge for geofencing providers?

Tighter privacy laws, including the FTC’s restrictions on sensitive location data, require vendors to adopt granular consent and on-device anonymization practices.

What years does this Active Geofencing Market cover, and what was the market size in 2025?

In 2025, the Active Geofencing Market size was estimated at USD 2.23 billion. The report covers the Active Geofencing Market historical market size for years: 2019, 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Active Geofencing Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: