Optical Spectrum Analyzer (OSA) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

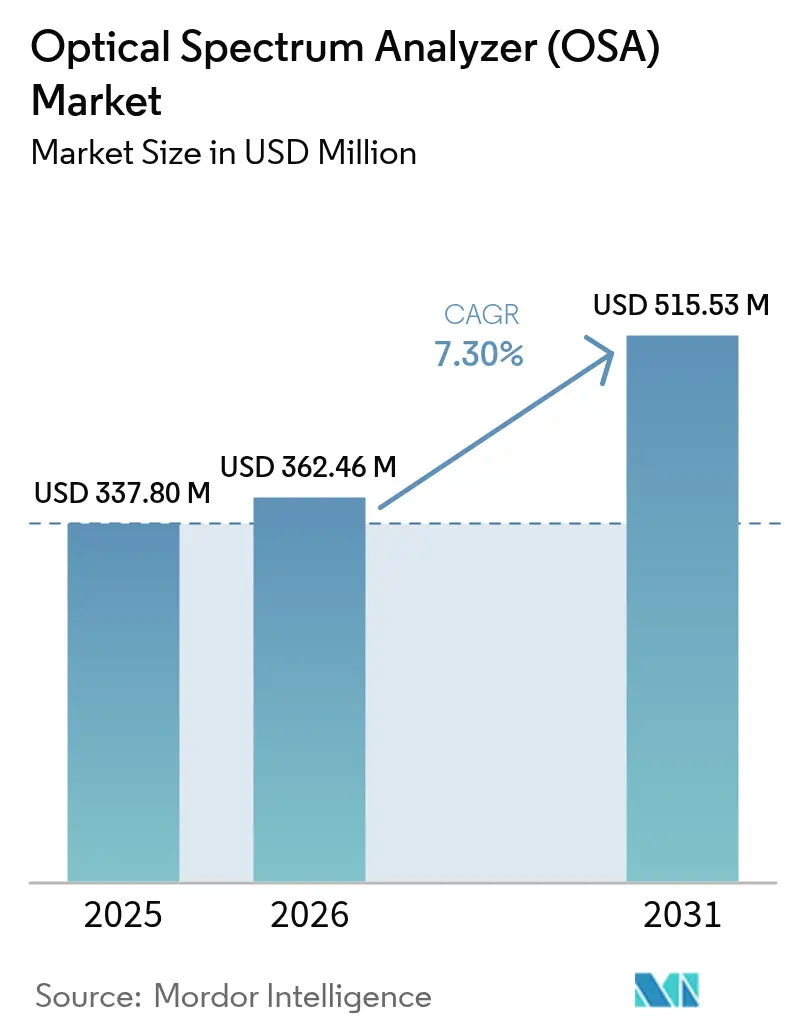

| Market Size (2026) | USD 362.46 Million |

| Market Size (2031) | USD 515.53 Million |

| Growth Rate (2026 - 2031) | 7.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

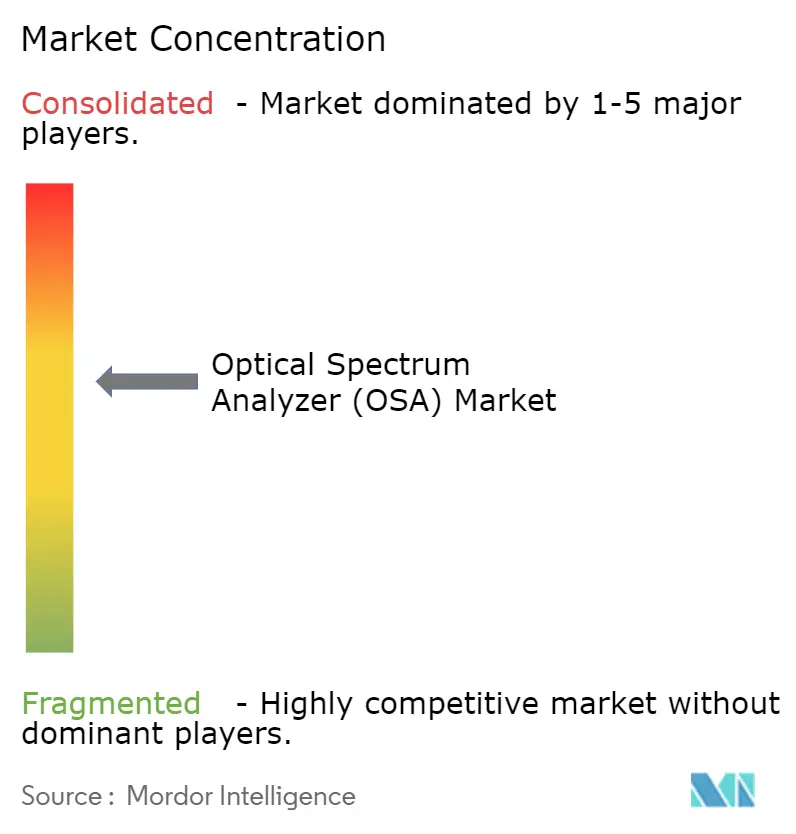

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Optical Spectrum Analyzer (OSA) Market Analysis by Mordor Intelligence

The optical spectrum analyzer market size is expected to grow from USD 337.8 million in 2025 to USD 362.46 million in 2026 and is forecast to reach USD 515.53 million by 2031 at 7.30% CAGR over 2026-2031. Uptake is accelerating as operators roll out 400 G and 800 G coherent links, data-center owners push toward tighter spectral margins, and 5G backhaul shifts to dense wavelength division multiplexing (DWDM). Field engineers now expect laboratory-grade resolution in the field, which is spurring rapid advances in miniaturization. Supply-chain volatility around gallium and germanium continues to squeeze component lead times, yet stricter optical-layer compliance rules in the United States and the European Union are compelling fresh test-equipment investment. Research funding in quantum optics and silicon photonics is widening the application base, encouraging vendors to blend high precision with AI-assisted analytics.

Key Report Takeaways

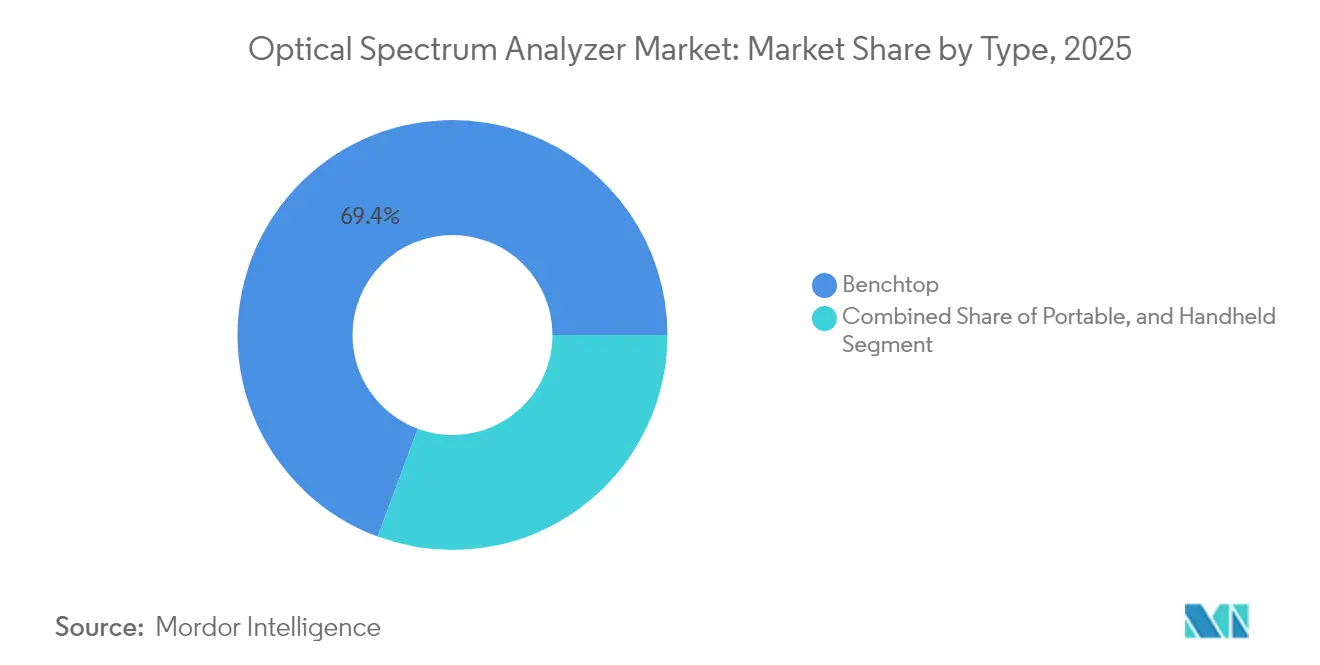

- By type, benchtop instruments led with 69.35% of the optical spectrum analyzer market share in 2025; the handheld segment is projected to expand at a 10.05% CAGR to 2031.

- By mode, spectrometer units held 64.40% revenue in 2025, while wavelength-meter units show the fastest growth at a 8.95% CAGR through 2031.

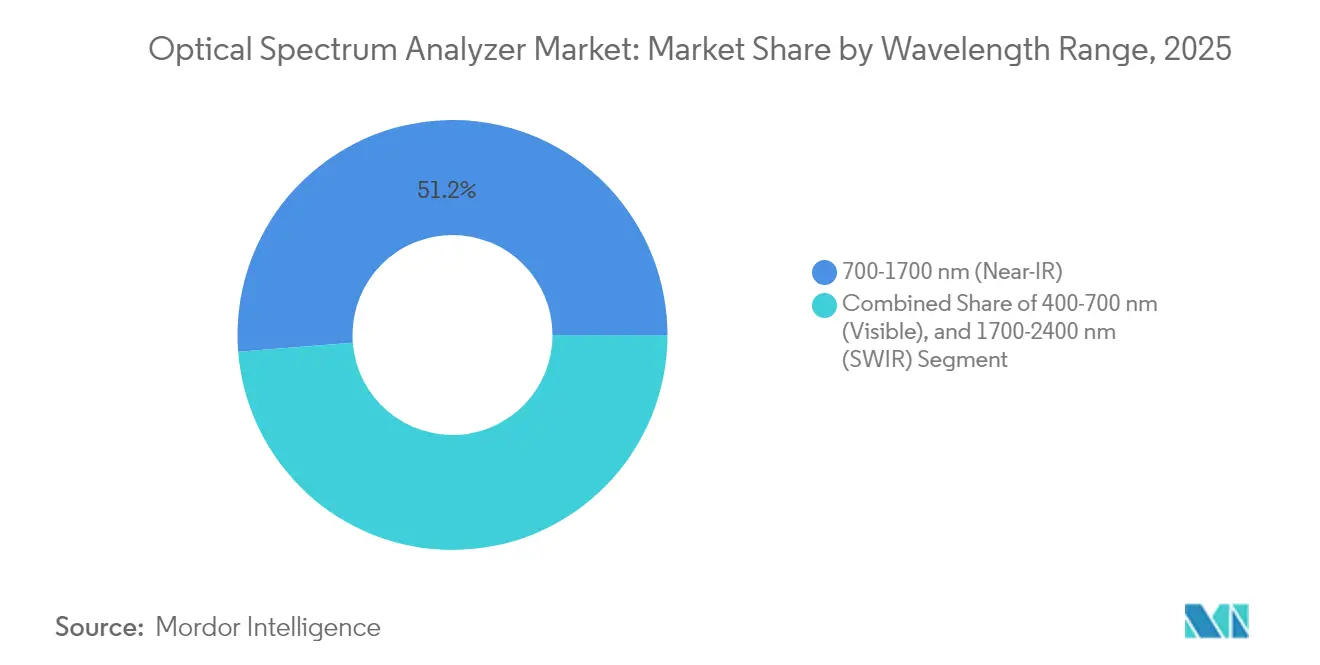

- By wavelength range, Near-IR (700-1700 nm) captured 51.25% of the optical spectrum analyzer market size in 2025; the SWIR range is forecast to grow at 9.15% annually to 2031.

- By end-user, telecommunications operators and OEMs held 45.30% share of the optical spectrum analyzer market size in 2025, whereas healthcare instrumentation is advancing at an 8.58% CAGR.

- By geography, North America led with 32.70% of the optical spectrum analyzer market share in 2025; Asia Pacific records the quickest regional CAGR at 8.78% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Optical Spectrum Analyzer (OSA) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of 400/800 G Coherent Optical Networks | +1.5% | North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Roll-out of 5G/6G Fronthaul & Backhaul DWDM Links | +1.8% | Global, with early gains in Asia Pacific | Short term (≤ 2 years) |

| Miniaturisation Enabling Field-Deployable OSAs | +1.1% | Global | Medium term (2-4 years) |

| Silicon Photonics & Quantum Optics R&D Funding Upsurge | +0.7% | North America, Europe | Long term (≥ 4 years) |

| Mandatory Optical-Layer Compliance in Data-Centre Transceivers (US and EU) | +1.1% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of 400/800 G Coherent Optical Networks

Installations of 400 G and 800 G coherent ports are rising sharply as cloud operators extend datacenter-interconnect footprints. Cignal AI expects 400 G pluggable port deployments to peak in 2026, followed by 800 G adoption.[1]Lightwave Staff, “RETN Conducts Large-Scale 400GbE Coherent Pluggable Optics Build,” Lightwave, lightwaveonline.comThese higher-order modulation formats require sub-picometer resolution and low polarization-dependent loss, driving renewed demand for high-accuracy OSAs. Vendors are embedding faster coherent receivers, automated dispersion-compensation analytics, and broader sweep bandwidths to keep pace. As networks migrate toward 1.6 T interfaces, continuous-sweep instruments with real-time digital signal processing (DSP) become indispensable for validating optical signal-to-noise ratio (OSNR) under tighter channel spacing.

Roll-out of 5G/6G Fronthaul & Backhaul DWDM Links

DWDM now underpins 5G fronthaul in dense urban clusters, and early 6G field trials already demand channel granularity below 50 GHz. Research predicts mobile backhaul and fronthaul revenue to reach USD 56.34 billion by 2030, implying unprecedented optical-testing volume.[2].Fayad, Abdulhalim, Tibor Cinkler, and Jacek Rak."Toward 6G Optical Fronthaul: A Survey on Enabling Technologies and Research Perspectives."arxiv.orgOSAs calibrated for 1550 nm C-band channels are being supplemented with extended-range units that cover 1310 nm P2P fiber and free-space optics feeds. Operators favor handheld designs that integrate remote cloud dashboards, enabling immediate spectral snapshots during tower turn-ups. The optical spectrum analyzer market is seeing increased bundling with passive optical network (PON) power meters, creating one-stop diagnostic kits.

Miniaturisation Enabling Field-Deployable OSAs

Microelectromechanical systems (MEMS) gratings, compact diode-laser arrays, and computational spectrometry algorithms are shrinking instrument footprints without sacrificing fidelity. Solid-state devices that once filled half a rack now slip into a technician’s vest pocket, maintaining 0.05 nm resolution in harsh outdoor conditions onlinelibrary.wiley.com. Battery-operated units with multi-hour runtime enable continuous monitoring of long-haul links, reducing truck rolls. Portable analyzers are increasingly coupled with AI-based anomaly detection, automatically flagging out-of-spec power ripple or filter drift. These enhancements support the optical spectrum analyzer market as fiber build-outs penetrate rural zones where bench instruments are impractical.

Silicon Photonics and Quantum Optics R&D Funding Upsurge

Government programs, led by a USD 998 million allocation under the National Quantum Initiative for FY 2025, are accelerating work on integrated photonics and quantum key distribution.[3]National Quantum Initiative. "NQI-Annual-Report-FY2025.pdf." quantum.govResearchers need OSAs that measure faint entangled-photon signatures and broad-bandwidth photonic-integrated circuits (PICs). Innovations such as wideband vector spectrum analyzers deliver 55.1 THz windows with 471 kHz frequency resolution, enabling complete characterization of on-chip modulators. This fusion of quantum-grade sensitivity and telecom-grade robustness is extending the optical spectrum analyzer market into defense sensing, secure communications, and ultrafast computing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Calibration Cost of Sub-pm Resolution OSAs | -0.7% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Performance Limits of Handheld Units for Coherent Systems | -0.4% | Global | Medium term (2-4 years) |

| Alternative Real-time Spectrum Monitoring (SWI-based) Solutions | -1.1% | North America, Europe | Medium term (2-4 years) |

| Tariff-Driven Photonic Component Supply-Chain Volatility | -0.7% | Global, with higher impact in Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High capital and calibration cost of sub-pm resolution OSAs

Sub-picometer instruments often exceed USD 100,000 per unit and demand periodic factory calibration to maintain ±0.03 nm absolute accuracy. These recurring expenses deter smaller labs and network operators in price-sensitive regions. EXFO notes that maintaining ±0.5 dB power accuracy typically requires specialist recalibration services. Vendors are experimenting with subscription-based calibration programs and modular optics cartridges to lower ownership cost, yet adoption remains constrained among cost-conscious buyers, tempering growth in segments below 100 GHz channel spacing.

Alternative real-time spectrum monitoring (software-defined) solutions

DSP-based optical channel monitors (OCMs) and in-band telemetry embedded in modern coherent transceivers provide continuous OSNR feedback without discrete test gear. Lightwave reports that OCM firmware upgrades can now resolve ±0.1 nm drift within line cards. While these embedded tools lack the full dynamic range of an OSA, they satisfy many in-service monitoring tasks. As operators strive for lower opex, software-only telemetry could squeeze the optical spectrum analyzer market on routine maintenance tasks, restricting demand to complex troubleshooting and R&D.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Handheld Instruments Move from Niche to Mainstream

Benchtop units contributed to 69.35% of total revenue, in 2025, thanks to unmatched dynamic range and sweep resolution. High-end coherent network rollouts continue to rely on these laboratory-grade platforms for pre-deployment characterization and manufacturing QC. Yet the handheld segment is expanding at a 10.05% CAGR, nearly three percentage points above the overall optical spectrum analyzer market. The optical spectrum analyzer market size for handheld models is forecast to register a CAGR of 10,05%, propelled by MEMS-based gratings and GPU-accelerated signal reconstruction.

Portable designs integrate cloud-native dashboards, Wi-Fi backhaul, and AI-powered event annotation, letting field technicians upload traces directly into trouble-ticket systems. Computational spectrometers using pattern-encoded apertures now achieve 0.1 nm resolution in chassis weighing under 1 kg.Vendors also push hybrid “portable-bench” instruments delivering benchtop-level accuracy in a rugged case, widening mid-tier adoption. These shifts indicate a long-run balancing act between resolution, budget, and mobility across the optical spectrum analyzer market.

By Mode Type: Wavelength Accuracy Gains Priority

Spectrometer mode generated 64.40% of revenue, because it delivers a full view of power spectral density across C- and L-bands. As DWDM channel counts rise, engineers increasingly pair spectrometer sweeps with real-time wavelength-meter snapshots to catch drift under load. Wavelength-meter products, now growing at 8.95% annually, combine stabilized Fabry-Pérot references with fast photodiode arrays, producing ±0.01 nm accuracy within 200 ms.

Optical channel turn-up often begins with a wavelength-meter check before deeper spectrometer analysis, a workflow that is fostering dual-mode instruments. Keysight’s recent tester embeds both measurement paths, adding AI-driven pass-fail analytics that trim certification time. The optical spectrum analyzer industry is likely to see further convergence, as algorithmic techniques compensate for missing detector elements, compressing cost while maintaining precision.

By Wavelength Range: SWIR and Mid-IR Applications Expand

The 700-1700 nm Near-IR band, core to telecom C-band operation, held 51.25% of revenue. Growth stays healthy as carriers migrate to 400 G ZR optics and data-center operators refresh transceiver fleets. Nevertheless, emerging environmental, medical, and industrial use cases are lifting demand in the 1700-2400 nm SWIR band. Yokogawa’s AQ6377E extends coverage to 3200 nm, meeting gas-sensing requirements. The optical spectrum analyzer market size for SWIR-capable units is predicted to register a 9.15% CAGR.

Advances in silicon-nitride waveguide amplifiers now provide 330 nm continuous-wave gain, enabling broadband sources that straddle NIR and SWIR regions. Instruments must therefore calibrate both InGaAs and extended-InGaAs detectors, supporting wider sweep ranges in a single enclosure. Cross-band flexibility improves laboratory ROI and shortens prototype cycles for next-generation sensors. The visible band remains niche but vital for display metrology and fluorescence studies, keeping tri-band modularity on vendor roadmaps.

By End-user Industry: Healthcare Tests Extend Beyond Ophthalmology

Telecommunications operators and optical OEMs retained 45.30% of revenue in 2025, as OSAs remain indispensable for line qualification, chromatic-dispersion mapping, and filter validation. Yet healthcare and life-science laboratories register the highest expansion, growing 8.58% yearly. Optical coherence tomography (OCT), Raman spectroscopy, and photodynamic therapy all require precise spectral control, drawing upon compact, high-sensitivity OSAs. A recent OCT design using an NVIDIA Jetson Nano achieved fivefold processing gains while cutting system size by two-thirds, highlighting the crossover between medical devices and edge computing.

Industrial quality-control lines adopt OSAs for in-process monitoring of fiber-laser welding and additive manufacturing, whereas aerospace programs deploy them for LIDAR calibration under vibration stress. Academic laboratories remain a cradle of innovation, evidenced by PIC-testing breakthroughs in quantum transceivers backed by the National Quantum Initiative. Collectively these forces diversify the optical spectrum analyzer market, cushioning it against single-sector downturns.

Geography Analysis

North America contributed 32.70% of revenue in 2025, anchored by dense hyperscale datacenter clusters and federally backed quantum-research hubs. Regulatory mandates that embed optical-layer compliance in 800 G transceivers reinforce procurement momentum, while Ciena’s 8192 coherent router launch further stimulates demand for inline spectral verification. Regional manufacturers also benefit from reshoring incentives designed to de-risk component supply.

Asia Pacific shows the fastest trajectory, advancing at an 8.78% CAGR to 2031. Massive 5G rollouts, rising photonic-chip foundry capacity, and national programs such as “Made in China 2025” are propelling local spending on high-precision test gear. The optical spectrum analyzer market size for Asia Pacific is projected to grow rapidly by 2031 as carriers densify backhaul networks and universities escalate PIC research.

Europe maintains strong standing through concerted R&D funding, eco-design regulations, and integrated photonics clusters in the Netherlands and Germany. Strict carbon-reduction goals push operators to adopt energy-efficient coherent optics, a move that requires meticulous spectral balancing during deployment. Momentum also builds in the Middle East, Africa, and South America, where greenfield fiber projects leapfrog older copper infrastructure. While spending is smaller, high initial equipment orders accompany each network phase, expanding the global optical spectrum analyzer market footprint.

Regulatory Landscape

Compliance requirements for optical test and measurement are anchored in international standards that support calibration and repeatable optical-layer measurements, with the IEC framework commonly referenced in procurement and qualification workflows (for example, IEC 62129-1 for calibration and IEC 61290-1-1 for OSA-based test methods). A key 2026 update is the publication of IEC 61290-1-2:2026 (Edition 3.0) on optical amplifier test methods, reinforcing demand for standards-aligned instrumentation when validating OSNR and other amplifier parameters in DWDM systems.

National certification regimes are also tightening procedures that affect both test-equipment vendors and users, particularly where authorization depends on accredited labs and recognized certification bodies. In the United States, the FCC adopted a final rule (FCC 26-28, ET Docket No. 24-136) effective June 15, 2026, adding a fast-track priority review path for devices tested in Trusted Test Labs and updating post-market surveillance processes, which raises the value of traceable test data and lab credentials. In Asia, India DoT/TEC issued an April 2026 notification under the Telecommunications Act 2023 revising standards for SIM and IP security equipment with a 90-day transition window, and Cambodia regulator opened an April 2026 consultation on draft technical standards and type approval rules, highlighting how fragmented compliance can trigger re-testing and additional documentation across markets.

Value Chain Analysis

The OSA value chain begins with photonic and electronic inputs (diffraction gratings or tunable filters, detector arrays such as InGaAs and extended-InGaAs, precision optics, high-stability references, ADC/DSP and embedded compute) and then moves into instrument design, calibration, and manufacturing/assembly, followed by channel partners and direct sales into telecom operators, optical OEMs, datacenter interconnect teams, and research labs. Calibration traceability and alignment to IEC measurement methods act as acceptance gatekeepers alongside hardware differentiation, and the bill of materials is exposed to specialty-material volatility (including gallium and germanium) highlighted in the report context as a contributor to lead-time pressure.

Downstream, OSAs increasingly function as a control point within the optical networking and co-packaged optics reliability stack, supporting characterization, qualification, and production validation of photonic integrated circuits and optical engines. A practical bottleneck is production test throughput, where optical probing and sub-micron alignment to PIC couplers can take over 100 seconds per PIC, shifting competition toward automation and parallelization rather than only higher resolution. The chain is also adjusting to geopolitical and cost pressures, including early-2025 US tariff measures on imported optical components and assemblies, and a broader trend of vendors diversifying sourcing and using Southeast Asia for parts of assembly to de-risk supply while meeting demand tied to 800G and 1.6T optical transitions.

Competitive Landscape

Five suppliers-Yokogawa, Keysight, VIAVI, EXFO, and Anritsu-account for roughly 65% of worldwide revenue, confirming a moderately concentrated field. Barriers stem from patented diffraction-grating designs, proprietary detector arrays, and long-validated calibration chains. Benchtop units in the sub-picometer class remain dominated by Japanese and U.S. incumbents, while Chinese and European challengers target handheld niches with aggressive pricing.

Strategic focus centers on layered differentiation. Yokogawa advances coherence-tracking algorithms, VIAVI tunes OSAs to pair with its optical channel monitors, and Keysight blends AI to automate pass-fail logic. Teradyne’s 2025 purchase of Quantifi Photonics adds grating-based technology that stretches to 5.5 µm, widening access to mid-IR measurement. Meanwhile, Anritsu co-develops 5G testing suites with Tier-1 operators, embedding OSA options into transport analyzers.

Emerging technologies threaten to realign positioning. Vector spectrum analyzers covering 55 THz with sub-MHz resolution present a leap in bandwidth, potentially unseating legacy scanning techniques. Also, modular plug-ins that snap into cloud-linked handheld frames promise recurring subscription revenue. Alliance building between instrument makers and PIC fabs is intensifying, aiming to deliver factory-calibrated wafers bundled with test micro-APIs. As a result, the optical spectrum analyzer market shows fertile ground for both incremental refinements and disruptive form factors.

Optical Spectrum Analyzer (OSA) Industry Leaders

-

Yokogawa Test & Measurement Corporation

-

Thorlabs Inc.

-

VIAVI Solutions

-

EXFO Inc.

-

Anritsu Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary whitespace is production-grade spectral test for high-volume optical component manufacturing, where faster sweep architectures and compact footprints broaden the case for 100% inspection for lasers, transceiver sub-assemblies, and passive devices. This is supported by vendor moves aimed at factory workflows rather than lab-only use, including Yokogawa AQ6361 (introduced in 2025 as a compact production OSA with markedly higher measurement speed versus prior models) and Shimadzu March 2026 announcement of the Laser Spectrum Analyzer SPG-V500 (InGaAs type) for 950 to 1700 nm, positioned for high-speed laser characterization and manufacturing inspection with planned availability across China, India, and the EU.

Another opportunity area is component and module characterization for 1.6T class optical interconnect development, where broader electrical bandwidth and tighter spectral margins increase the need for correlated optical and electro-optic measurements during validation. Keysight March 2026 introduction of a 220 GHz Lightwave Component Analyzer for next-generation optical transceiver components signals investment in test capability aligned with AI datacenter infrastructure development. At the same time, optical-network standardization work around ITU-T Study Group 15, alongside bodies such as IEEE and OIF, keeps focus on spectrum management and measurement consistency, reinforcing demand for standards-referenced OSAs and adjacent platforms that shorten qualification cycles for new coherent and photonics designs.

Recent Industry Developments

- January 2026: VIAVI introduced a medium and long-range bidirectional testing and certification solution for hollow core fiber on its OneAdvisor 800 Fiber platform using advanced OTDR modules. The release targets field certification of splice quality and connector losses, complementing optical-layer troubleshooting needs that often drive demand for portable spectral and fiber test instrumentation.

- September 2025: VIAVI expanded its ONE LabPro test and validation platform with the ONE-1600ER module to support 1.6Tb optical component testing aligned with emerging IEEE 802.3dj requirements. This extends lab validation capacity for next-generation optical components, which increases pull-through for higher-performance optical measurement workflows across development and pre-production.

- February 2025: Yokogawa Test and Measurement released the AQ6361 optical spectrum analyzer for production testing of datacom and telecom components such as laser diodes, optical transceivers, and optical amplifiers, with substantially higher measurement speed than the prior AQ6370E. The focus on manufacturing throughput supports broader adoption of OSAs on factory lines, where test time and repeatability directly affect yield and time-to-ship.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from optical spectrum analyzers used to measure and display optical power distribution across wavelengths in fiber optic and photonics test setups. The sizing reflects shipments of dedicated OSA instruments sold as benchtop, portable, handheld, or as integrated test modules.

Scope exclusions: We exclude software-only analysis tools, service and calibration contracts, and broader RF test platforms where optical analysis is not a dedicated OSA function.

Segmentation Overview

-

By Type

- Portable

- Handheld

- Benchtop

-

By Mode Type

- Spectrometer Mode

- Wavelength Meter Mode

-

By Wavelength Range

- 400-700 nm (Visible)

- 700-1700 nm (Near-IR)

- 1700-2400 nm (SWIR)

-

By End-user Industry

- Telecommunication Operators and OEMs

- Healthcare and Life-Sciences Instrumentation

- Consumer Electronics and Photonics Devices

- Industrial and Manufacturing QA/QC

- Aerospace and Defence Optoelectronics

- Academic and Government Research Labs

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- South Korea

- India

- South East Asia

- Rest of Asia-Pacific

-

South America

- Brazil

- Rest of South America

-

Middle East and Africa

-

Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

-

Africa

- South Africa

- Rest of Africa

-

Middle East

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building the demand context around fiber optics and photonics testing, then mapping it to where OSAs are specified and purchased. Public references used for grounding included sources such as the International Telecommunication Union (ITU) for telecom direction, IEEE and Optica Publishing Group for standards-linked technical adoption, NIST material on measurement practices, and the US International Trade Commission (USITC) trade statistics for optical instrument flows.

On the supply side, we used company annual reports, investor presentations, product documentation, and reputable press coverage to list active offerings and typical performance claims by form factor. Where the public trail was thin, a paid subscription for company financials and news helped verify corporate structure changes, geographic exposure, and product line emphasis over time. The desk sources mentioned here are illustrative only, and we also referred to many other public sources for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on confirming how OSAs are bought and used across telecom network testing, datacenter optics, component manufacturing, and research labs. We spoke with a mix of instrument OEM teams, channel partners, and end users across APAC, EMEA, and the Americas, then used that input to adjust adoption assumptions, replacement cycles, and realistic pricing bands, including cases where an integrated module is counted as an OSA sale.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 13% | APAC: 46% |

| Mid tier: 53% | Functional/Unit leaders: 31% | EMEA: 32% |

| Smaller Players: 15% | Managers: 56% | Americas: 22% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where telecom and photonics test activity was reconstructed through deployment signals and testing intensity, then translated into OSA demand using penetration and refresh logic. To keep the totals realistic, we corroborated them with selective bottom-up checks such as sampled average selling price (ASP) bands by form factor, channel markups, and a roll-up of supplier positioning in key application areas.

Key model inputs included the pace of fiber network upgrades and coherent optics rollout, datacenter interconnect growth, optical component production trends, typical replacement cycles for lab and field instruments, and the split between benchtop versus portable and handheld purchasing. Wavelength coverage needs (for example, visible versus 700 to 1700 nm and extended bands) were also used as a practical indicator for which customers tend to buy higher priced systems. Forecasts were produced using scenario analysis supported by expert expectations on capex cycles, lead times, and ASP movement, then stress-tested with a light exponential smoothing pass to reduce year-to-year noise.

Where bottom-up evidence was incomplete, gaps were handled by applying conservative adoption rates to the addressable test points, then re-checking the implied unit volumes against typical purchasing behavior shared by practitioners.

Data Validation & Update Cycle

Outputs were checked in several steps so the model stayed aligned with real market signals. We compared the implied unit demand and ASP levels against independent indicators such as procurement patterns, trade direction for optical instruments, and public product mix shifts, then investigated any sharp variances before internal sign-off.

If a major mismatch appeared, assumptions were revisited and relevant experts were re-contacted to confirm whether the change was temporary or structural. The report is refreshed annually, and interim updates are made when material events occur such as large product launches, pricing resets, or demand shocks in telecom spending. Before delivery, the latest data is re-reviewed so clients receive an up-to-date view.

Mordor Intelligence's Optical Spectrum Analyzer Osa Market Sizing Compared With Other Published Estimates

Published market values for optical spectrum analyzers can differ even when they appear to cover the same product, because the scope and counting rules are not always the same. Differences can also come from the chosen base year, how currency conversion timing is handled, and whether pricing is kept flat or allowed to move with mix changes.

The main gap comes from whether integrated test modules and extended wavelength configurations are counted as full OSA revenue or treated as adjacent optical test equipment, and Mordor Intelligence counts them only when the shipped unit is a dedicated OSA instrument or a clearly priced OSA module. Another common driver is refresh cadence, where some sources keep older ASPs for too long or apply one growth rate across end uses, even though telecom, datacenter optics, and lab demand can move on different cycles.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 362.46 M (2026) | |

| Regional Consultancy A | USD 412.30 M (2024) | Uses an earlier base year and appears to include a wider set of optical test equipment categories around OSAs, which can lift the stated size if modules and related instruments are bundled. |

| Industry Publisher B | USD 352.69 M (2025) | Applies a longer forecast horizon with smoother growth, and likely relies on blended ASP assumptions that underplay mix shifts between benchtop and portable systems. |

Taken together, the spread is mostly explained by what gets counted as an OSA sale, plus the year chosen for the starting point. By keeping the scope tied to dedicated OSA revenue and checking the implied unit and price logic against real purchase behavior, the final number stays traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

What is driving the current growth of the optical spectrum analyzer market?

Strong deployment of 400 G / 800 G coherent links, 5G backhaul densification, and stricter optical-layer compliance standards are pushing up demand for precise spectral measurement tools.

How large will the optical spectrum analyzer market be in 2031?

The optical spectrum analyzer market size is projected to hit USD 515.53 million by 2031, up from USD 362.46 million in 2026.

Which product type is expanding the fastest?

Handheld analyzers, aided by MEMS gratings and computational spectrometry, are forecast to grow at a 10.05% CAGR between 2026 and 2031.

Why are healthcare applications gaining traction?

Optical coherence tomography, advanced imaging, and spectroscopic diagnostics require compact, high-sensitivity OSAs, propelling an 8.58% CAGR in healthcare demand.

What regional market is growing the quickest?

Asia Pacific leads with an 8.78% CAGR through 2031, fueled by large-scale 5G rollouts and rising photonic-chip manufacturing capacity.

Are software-based monitors replacing traditional OSAs?

Embedded optical channel monitors handle routine in-service checks, yet high-resolution OSAs remain essential for coherent-system troubleshooting, R&D, and regulatory compliance.

Page last updated on: