1,4 Butanediol Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

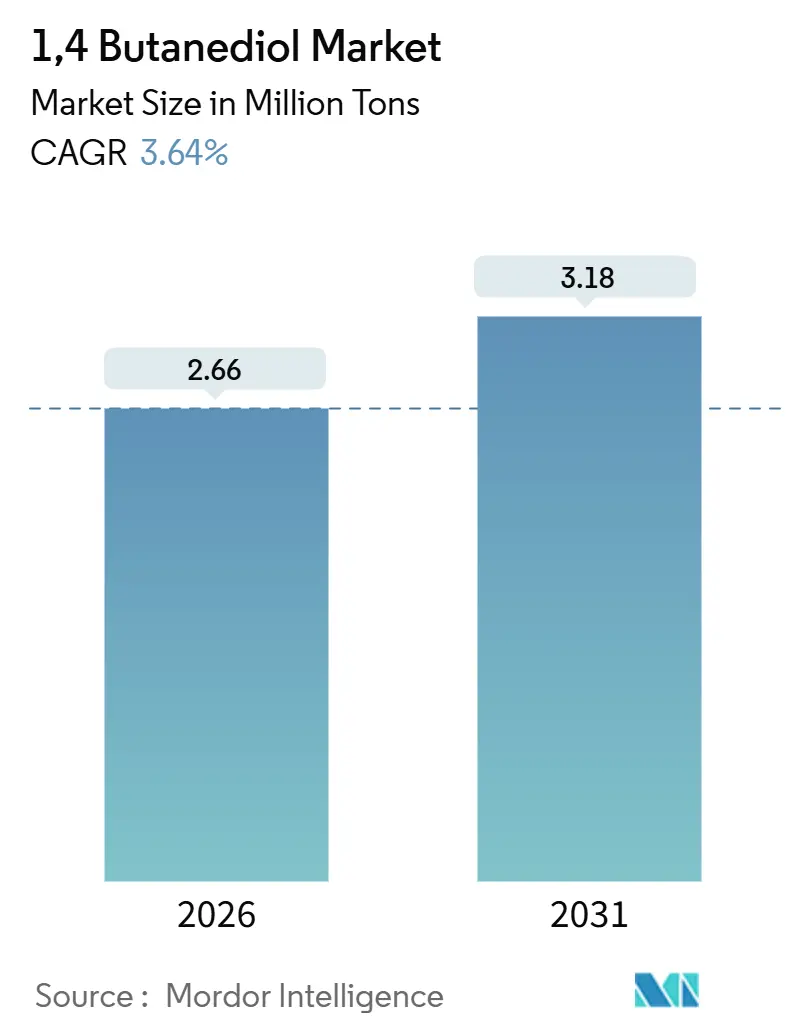

| Market Volume (2026) | 2.66 Million tons |

| Market Volume (2031) | 3.18 Million tons |

| Growth Rate (2026 - 2031) | 3.64% CAGR |

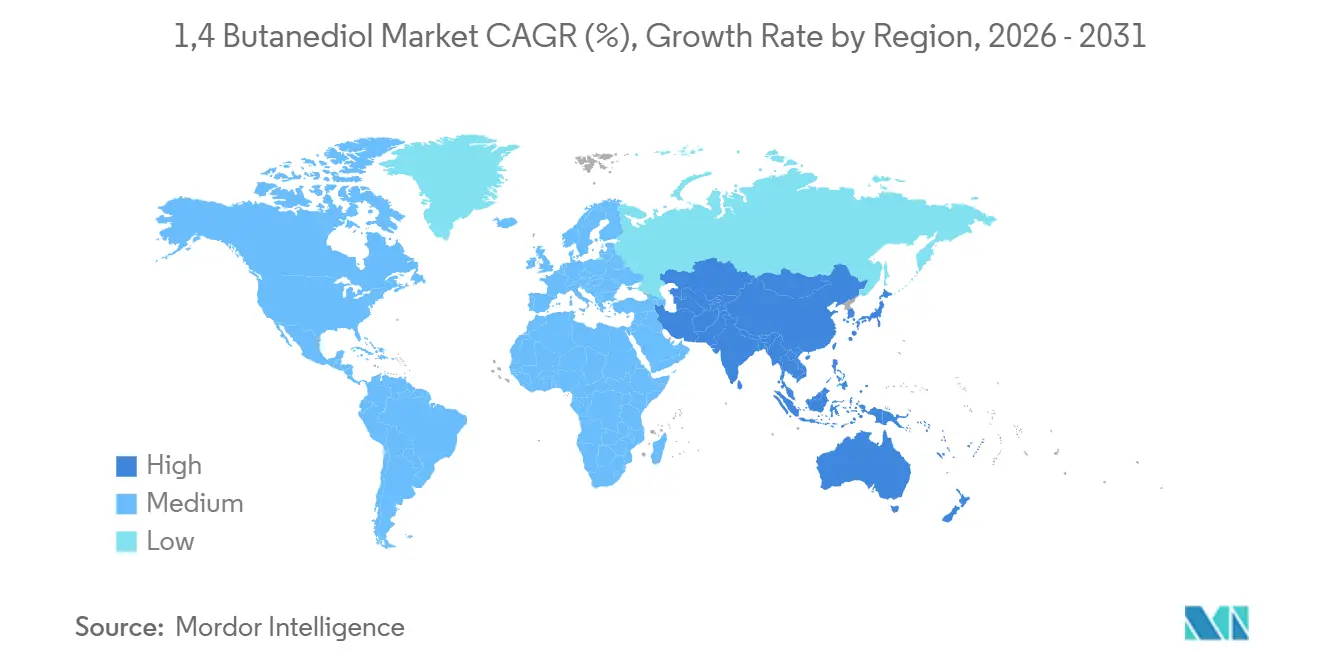

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

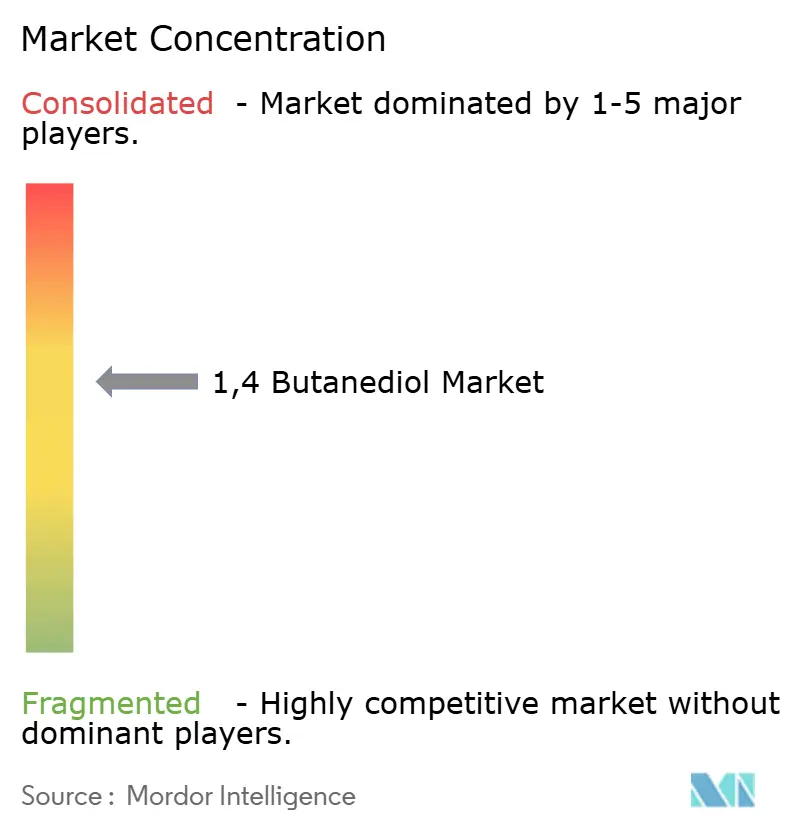

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

1,4 Butanediol Market Analysis by Mordor Intelligence

The 1,4 Butanediol Market size is estimated at 2.66 million tons in 2026, and is expected to reach 3.18 million tons by 2031, at a CAGR of 3.64% during the forecast period (2026-2031). This overall pace masks a structural pivot toward lower-carbon production routes, notably bio-fermentation, which is scaling at 7.52% per year as European and North American carbon-pricing regimes add USD 50 to USD 100 per ton to the delivered cost of coal-derived volumes. The shift is already reshaping supplier hierarchies: Hyosung brought its first 50,000-ton bio-BDO train online in Vietnam during 2026, while BASF commissioned commercial bio-BDO in Germany a year earlier. Tetrahydrofuran (THF) kept a 52.65% derivative share in 2025, anchored by spandex feedstock demand, yet polybutylene terephthalate (PBT) is expanding faster at 3.79% CAGR as electric vehicles and 5 G infrastructure require flame-retardant, high-voltage insulation. Asia-Pacific remains the production epicenter with 76.12% of volume, but the European Union’s Carbon Border Adjustment Mechanism (CBAM) penalizes carbon-intensive Chinese exports, tilting trade flows toward bio-routes.

Key Report Takeaways

- By production process, the Reppe process held 50.18% of global output in 2025; bio-fermentation is forecast to grow at a 7.52% CAGR to 2031.

- By derivative, Tetrahydrofuran (THF) led with a 52.65% share in 2025; Polybutylene Terephthalate (PBT) is advancing at a 3.79% CAGR through 2031.

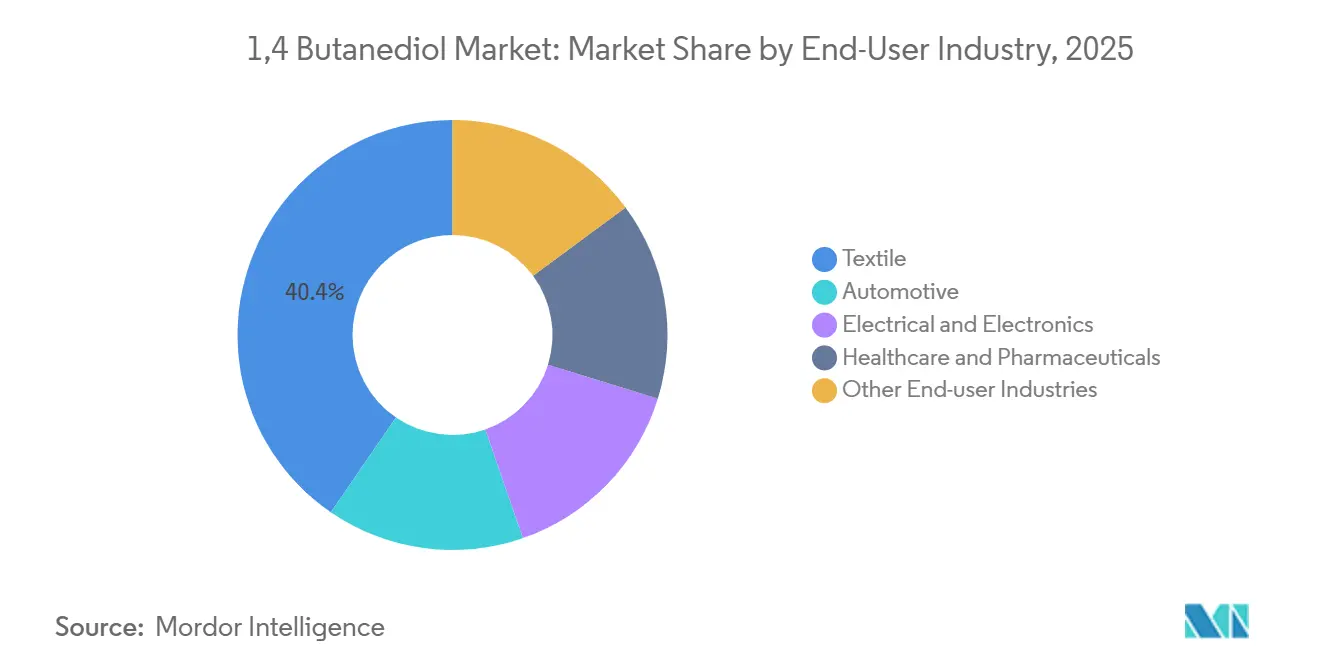

- By end-user industry, textiles accounted for 40.41% share of the 1,4 butanediol market size in 2025, while electrical and electronics is the fastest-growing segment at 4.19% CAGR.

- By geography, Asia-Pacific commanded 76.12% of the 1,4 butanediol market share in 2025, and is projected to expand at a 3.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of 1,4 Butanediol Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for THF and spandex fibers | +0.9% | Global, concentrated in Asia-Pacific textile hubs | Medium term (2–4 years) |

| Light-weighting of EV connectors spurring PBT uptake | +0.7% | North America, Europe, China EV corridors | Short term (≤ 2 years) |

| Expansion of polyurethane applications | +0.6% | Global, led by automotive and construction sectors | Medium term (2–4 years) |

| Government subsidies for bio-BDO capacity | +0.5% | North America, Europe | Long term (≥ 4 years) |

| Cost-advantaged coal-to-acetylene integrations in inland China | +0.4% | China (Xinjiang, Shanxi, Inner Mongolia) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for THF and Spandex Fibers

Tetrahydrofuran remains the gateway molecule to polytetramethylene ether glycol, the soft segment in spandex. BASF operates five PolyTHF plants worldwide and reported double-digit volume growth in Asia-Pacific technical-textile grades during 2025[1]BASF SE, “PolyTHF Market Update 2025,” basf.com. Hyosung integrated bio-BDO into its regen BIO spandex, launched in 2025, and is realizing 10-15% price premiums in European and North American apparel markets. Apparel restocking cycles normalize faster than durable-goods demand, giving THF a buffer against macro shocks. Beyond textiles, PTMEG grades flow into thermoplastic polyurethane (TPU) used in medical tubing and automotive interior films, broadening the demand base.

Light-Weighting of EV Connectors Spurring PBT Uptake

High-voltage electric-vehicle platforms require connector housings with flame-retardant, hydrolysis-resistant, and dimensional stability. PBT synthesized from BDO meets these criteria and is displacing PA 6,6 in 400-800 V architectures. BASF’s Ultradur grades passed UL 94 V-0 testing and secured design wins at several European and Chinese OEMs in 2025. Rising 5 G base-station installations and data-center construction intensify PBT demand for high-temperature circuit-breaker housings, reinforcing its 3.79% CAGR outlook.

Expansion of Polyurethane Applications

BDO-based TPU delivers superior hydrolysis resistance compared with alternative diols, making it the preferred chain extender for fuel lines, hydraulic hoses, and EV wiring insulation. Medical-device manufacturers increasingly specify BDO-TPU for catheter tubing and wound-care films due to its biocompatibility profile. Application diversification reduces reliance on a single end-market and supports steady volumetric growth.

Government Subsidies for Bio-BDO Capacity

The US Inflation Reduction Act provides a USD 1.00 per kg production tax credit for bio-based chemicals that deliver at least 25% lower life-cycle emissions[2]U.S. Department of Energy, “Bioenergy Technologies Office 2025 Funding Awards,” energy.gov. The Department of Energy allotted USD 12 million in 2025 to de-risk fermentation scale-ups. Europe’s Bioeconomy Strategic Framework, updated in 2025, coupled with European Investment Bank soft loans, channels EUR 500 million into bio-chemical projects. Qore leveraged these incentives to lock in long-term offtake with BASF, allowing bio-routes to undercut Asian imports on a delivered-cost basis.

Restraints Impact Analysis of 1,4 Butanediol Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Occupational health and safety concerns | -0.3% | Global, stringent in EU and North America | Medium term (2–4 years) |

| Volatile feedstock prices | -0.5% | Global, acute in Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Carbon-border taxes raising cost of coal-based BDO exports | -0.4% | China exports to EU, potential U.S. extension | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Occupational Health and Safety Concerns

1,4 Butanediol is an eye, skin, and respiratory irritant, and prolonged exposure depresses the central nervous system. The European Chemicals Agency and ACGIH enforce exposure thresholds, prompting investments in closed-loop transfer systems and vapor recovery. Compliance can add USD 50 to USD 100 per ton to operating costs, favoring well-capitalized producers. Several Xinjiang and Shanxi plants halted operations in 2024-2025 for ventilation retrofits, temporarily tightening regional supply.

Volatile Feedstock Prices

Acetylene tracks coal and electricity costs in inland China, fluctuating widely with seasonal supply constraints. Butadiene spot prices varied from USD 800 to USD 1,400 per ton during 2024 as crackers optimized ethylene margins. Propylene oxide used in the Davy route mirrors refinery turnaround cycles. Such volatility compresses BDO margins because derivative contracts often reset on a quarterly lag.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

1,4 Butanediol Market Segment Analysis

By Production Process:

Bio-Fermentation Gains Ground on Reppe DominanceReppe acetylene chemistry retained 50.18% of total output in 2025, reflecting decades of brownfield infrastructure. The installed base ensures that the 1,4 Butanediol market size tied to Reppe plants remains substantial through 2031. Even so, bio-fermentation grows 7.52% annually, propelled by carbon incentives that tilt project economics away from coal feedstocks. Genomatica’s GENO technology underpins BASF’s Verbund output and Hyosung’s Vietnam complex, proving that fermentation can scale to 50,000-ton trains with 90% lower life-cycle emissions. Propylene-oxide and butadiene routes stay niche because of higher variable costs and limited license holders.

Process economics now hinge on carbon accounting. Europe’s forthcoming Industrial Emissions Directive revision tightens VOC limits on acetylene plants, lifting compliance costs, while bio-routes sidestep acetylene-handling hazards. China’s 2060 carbon-neutrality pledge pressures regional authorities to curb coal-to-acetylene expansions, gradually eroding Reppe's share despite its entrenched footprint.

By Derivative:

THF Still Leads, PBT AcceleratesTetrahydrofuran (THF) commanded 52.65% derivative share in 2025, anchored by its conversion to polytetramethylene ether glycol for spandex and thermoplastic polyurethane elastomers. BASF's five global PolyTHF plants and Hyosung's integrated bio-BDO-to-PTMEG-to-spandex value chain underscore THF's entrenched position in textile supply chains. Yet polybutylene terephthalate is expanding at 3.79% CAGR through 2031, the fastest among all derivatives, as electric-vehicle connector lightweighting and 5G infrastructure rollouts drive demand for flame-retardant, high-voltage insulation materials. PBT's higher selling price, typically USD 2,500 to USD 3,500 per ton versus USD 1,800 to USD 2,200 for THF, translates to superior margins for producers who can secure automotive and electronics design wins.

Commodity THF margins compressed when BDO prices doubled from 2018-2024, whereas PBT suppliers held escalator clauses. As a result, producers increasingly direct new capacity toward PBT and TPU grades to lift overall earnings quality. Gamma-butyrolactone and pharmaceutical intermediates remain niche but offer price stability for high-purity grades.

By End-User Industry:

Textiles Remain Largest, Electronics FastestTextile applications held 40.41% end-user share in 2025, reflecting spandex's ubiquity in activewear, intimate apparel, and technical fabrics. However, electrical and electronics is the fastest-growing end-user segment at 4.19% CAGR through 2031, driven by PBT adoption in EV connectors, 5G base-station components, and semiconductor packaging. Automotive end-users, while smaller in absolute volume, are expanding rapidly as electric-vehicle architectures demand high-voltage connectors, battery enclosures, and cable insulation that meet stringent flame-retardancy and hydrolysis-resistance standards.

The textile sector's maturity and geographic concentration in Asia-Pacific create cyclical exposure: apparel restocking and inventory adjustments can swing THF demand. In contrast, automotive and electronics applications exhibit longer design-in cycles (18 to 24 months) and multi-year supply contracts, smoothing demand volatility but requiring upfront qualification investments.

Geography Analysis

APAC 1,4 Butanediol Market

Asia-Pacific accounted for 76.12% of global volume in 2025 and is set to grow at a 3.94% CAGR through 2031. China’s coal-to-acetylene clusters in Xinjiang, Shanxi, and Inner Mongolia supply most regional needs but face tightening energy-intensity and safety audits, creating intermittent outages. Hyosung’s USD 1 billion Vietnam complex marks Southeast Asia’s entry into premium low-carbon supply and will eventually relieve Chinese export dominance. India’s demand is climbing at double digits on the back of textile and automotive expansions, but lacks domestic capacity, relying on Korean and Middle-East imports.

North America and Europe 1,4 Butanediol Market

North America and Europe, both regions, advance bio-BDO capacity to hedge CBAM penalties and Scope 3 targets. BASF, Qore, and Novamont collectively added more than 100,000 tpa of fermentation output between 2024 and 2026. Local demand tilts toward high-value TPU, PBT, and pharmaceutical intermediates, giving producers a margin buffer against feedstock volatility.

MEA and South America 1,4 Butanediol Market

Saudi Arabia’s Sipchem operates a 50,000 tpa unit integrated with low-cost ethane, targeting polyurethane and solvent markets. Brazil drives South American consumption across automotive and textile channels, yet logistical and currency hurdles slow new investment. Africa’s demand is nascent, centered in South African polyurethane coatings, but infrastructure gaps remain a hurdle.

Value Chain Analysis

Upstream inputs for 1,4-butanediol (BDO) vary by route. Coal and electricity underpin acetylene generation for Reppe plants, which are highly integrated in inland China, while petrochemical pathways depend on butadiene or propylene oxide availability and pricing. Bio-fermentation routes rely on agricultural sugars and certification schemes, including Hyosung TNC's VIVE-certified sugarcane feedstock approach for its Vietnam program. Technology licensors and catalyst providers sit alongside producers as key nodes, with fermentation platforms such as Genomatica enabling commercial-scale Bio-BDO trains.

Midstream production is split between large integrated producers with captive conversion to derivatives and merchant sellers supplying external customers. BASF increased BDO production at Ludwigshafen in February 2026, reinforcing regional supply for European downstream users amid shifting trade conditions. Downstream, BDO is converted primarily into tetrahydrofuran (THF) and then PTMEG for spandex and TPU, while PBT and other derivatives serve electrical, electronics, automotive, and industrial applications. Distribution commonly runs through bulk chemical logistics and contracted offtake, and in 2026 the European Commission's definitive anti-dumping duties on BDO imports from China, Saudi Arabia, and the United States shifted sourcing economics, pushing buyers to rebalance between domestic EU supply, alternative origins, and lower-carbon routes where available.

Competitive Landscape

The 1,4 Butanediol market is moderately concentrated. Western players hedge carbon risk through technology licensing. Genomatica licenses its platform to multiple majors, compressing time-to-market but commoditizing bio-routes. White-space opportunities exist in pharmaceutical-grade BDO with sub-ppm impurity specifications, and in circular depolymerization of PBT scrap back to BDO. Ongoing EU anti-dumping cases against Chinese, US, and Saudi volumes spur plans for regional plants, raising the probability of mergers or joint ventures to secure market access.

1,4 Butanediol Industry Leaders

LyondellBasell Industries Holdings B.V.

DCC

Chang Chun Group

BASF

Markor Chemicals

- *Disclaimer: Major Players sorted in no particular order

1,4 Butanediol Market Companies Covered in this Report

- Ashland

- BASF

- Chang Chun Group

- CJ CHEILJEDANG CORP.

- DCC

- Genomatica, Inc.

- Grupa Azoty

- Henan Kaixiang Fine Chemical Co. Ltd

- Jiangsu Hailun Petrochemical Co. Ltd

- LyondellBasell Industries Holdings B.V.

- Markor Chemicals Group Co. Ltd

- Mitsubishi Chemical Group Corporation

- NAN YA PLASTICS CORPORATION

- Novamont SpA

- Shandong Yuanli Science And Technology Co. Ltd

- Shanxi Sanwei Group Co. Ltd

- Sinochem Internation Corporation

- Sipchem Company

- SK Geocentric Co., Ltd.

- Xinjiang Blue Ridge Tunhe Sci.&Tech. Co., Ltd.

- Xinjiang Tianye (Group) Co. Ltd

Market Opportunities and Future Outlook

Trade and supply-chain reconfiguration in Europe creates whitespace for regional and compliant supply, particularly after the European Commission imposed definitive anti-dumping duties on BDO imports from China, Saudi Arabia, and the United States in June 2026. BASF's February 2026 increase in output at Ludwigshafen highlights how incumbent producers are tightening local supply links to European derivative makers. This supports opportunities in long-term contracting, logistics hubs, and downstream THF/PTMEG, TPU, and PBT qualification support that emphasize continuity of supply.

Lower-carbon BDO is moving from a niche positioning to more scaled industrial use, creating room for vertically integrated offerings that carry the BDO carbon footprint through to end products, especially in textiles and engineered polymers. Hyosung TNC's Bio-BDO program in Vietnam (trial production and supply steps disclosed during 2026, using Genomatica fermentation technology) illustrates integrated sustainable textile positioning, while Qore's US bio-based BDO operations add an additional anchor point for renewable supply in North America. On the technology side, R&D around expanding fermentation feedstocks beyond conventional sugars, including lignocellulosic hydrolysates and new metabolic pathways reported in 2026 literature, is intended to support cost-down levers and new supplier entry points across pretreatment, fermentation optimization, and certification-ready mass-balance systems. Separate unmet-need space remains in higher-purity BDO grades and circular pathways that connect PBT recycling back toward monomers and intermediates, which aligns with downstream electronics and automotive qualification requirements.

Recent Industry Developments in 1,4 Butanediol Market

- June 2026: The European Commission imposed definitive anti-dumping duties on 1,4-butanediol imports from China, Saudi Arabia, and the United States, effective from 25 June 2026. The measure changed landed-cost structures for European buyers and strengthened the case for EU-based production and contracted regional supply.

- February 2026: BASF increased 1,4-butanediol production at its Ludwigshafen site in Germany to reinforce supply for European customers amid trade actions and tightening procurement requirements. The output boost supports downstream THF/PTMEG and polymer chains by improving local availability and reducing exposure to tariff-affected import flows.

- October 2025: Genomatica started operations at its Eddyville, Iowa plant to produce GENO Bio-BDO via single-step fermentation from plant-based sugars. Commercial operation at scale expands renewable BDO availability for derivatives and brand owners pursuing lower-carbon intermediates.

1,4 Butanediol Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers the global demand and supply of 1,4-butanediol (BDO) in value terms, counted at the point it is sold or consumed for downstream chemical use, across the main production routes and major consuming regions.

Scope exclusions: 1,3-butanediol and 2,3-butanediol, as well as internal transfer pricing inside fully integrated sites, are not counted.

Segments Covered in This Report

- By Production Process

- Reppe Process

- Davy Process

- Butadiene-Based Process

- Propylene Oxide-Based Process

- Bio-fermentation Route

- By Derivative

- Tetrahydrofuran (THF)

- Polybutylene Terephthalate (PBT)

- Gamma-Butyrolactone (GBL)

- Polyurethane (PU)

- Other Derivatives

- By End-user Industry

- Automotive

- Textile

- Electrical and Electronics

- Healthcare and Pharmaceuticals

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting fact base around capacity, operating rates, and where BDO demand is pulled through into finished materials like solvents, fibers, and engineering plastics. We referenced public sources such as the US International Trade Commission trade data, UN Comtrade, Eurostat, and national statistics offices for manufacturing and industrial output indicators that align with BDO derivative consumption.

To avoid over-relying on any single data stream, we also reviewed company annual reports and investor presentations for capacity additions, plant turnarounds, and integration levels, followed by press releases and association publications that track chemicals and polymers. In a few cases, paid subscriptions for company financials and intelligence, patents, and shipment-level import export records were used to confirm timelines and normalize gaps in reported volumes. The desk sources listed here are illustrative only, and many other public materials were also checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to stress-test the desk assumptions that most influence BDO sizing, especially utilization, merchant versus captive splits, and typical pricing movements by region. We spoke with producers, distributors, downstream processors, and procurement and plant teams across APAC, EMEA, and the Americas so the final model reflects what is contracted and consumed, not only what is theoretically installed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 14% | APAC: 43% |

| Mid tier: 55% | Functional/Unit leaders: 33% | EMEA: 34% |

| Smaller Players: 20% | Managers: 53% | Americas: 23% |

Market-Sizing & Forecasting

Market size is built using a top-down model where BDO demand is reconstructed from the downstream derivatives pool, and then mapped back to BDO intensity factors by application and region. We start from known and observable indicators, and then corroborate totals with selective bottom-up checks such as sampled producer and distributor volumes, channel discussions, and an ASP-times-volume sense-check for the merchant portion.

Inputs that matter in this market include announced capacity additions and shutdowns, utilization rate ranges by route, merchant versus captive consumption shares, import export flows into net importing regions, and regional price spreads tied to feedstock and energy movements. Because volume is the cleanest anchor for BDO, the value layer is added using region-specific pricing logic that is adjusted for contract timing and typical discounts for captive use where applicable.

For forecasting, scenario analysis is applied around new capacity ramp-ups, expected derivative demand growth, and trade shifts, and then the base case is selected based on what primary respondents consider most likely. When a country-level variable is not available, we bridge it using regional proxies (like polymer output and textile production indices) and then re-balance totals so they still match the global supply-demand reality.

Data Validation & Update Cycle

Outputs are checked in several steps so that the story and the math stay aligned. We compare modeled volumes and implied pricing against independent signals like trade balances, operating rate commentary, and derivative market direction, and then investigate large variances before sign-off.

If an unexpected jump appears (for example, a sudden price spike or a major plant outage), analysts re-contact relevant experts to confirm whether the change is temporary or structural. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery review is completed so clients receive the latest consistent view.

Mordor Intelligence's 1 4 Butanediol Market Size Measured Against Other Published Estimates

Published market sizes for 1,4-butanediol can vary even when the product name looks identical, because firms use different measurement units, base years, and conversion logic between tons and USD. Gaps also come from how merchant and captive volumes are treated, and whether the value layer is tied to contract pricing cycles or spot swings.

Internal transfer pricing inside fully integrated sites sits outside Mordor Intelligence's scope, which tends to keep the USD total closer to tradable economics rather than internal accounting marks. Other estimates may also mix a butanediol family view with a pure 1,4-BDO view, or apply a faster price escalation curve that is not validated against regional spreads and trade signals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.68 B (2024) | |

| Global Consultancy A | USD 7.68 B (2024) | Often presented as a value-only headline without clearly separating merchant pricing from captive transfers, which can compress the explanation for why USD and tonnage trends may diverge year to year. |

| Industry Publisher B | USD 7.80 B (2024) | Uses a different base-year setup and may rely on a more aggressive price progression into the forecast, which can lift the starting USD level slightly when averaged across regions. |

The comparison shows that even small scope and pricing-handling differences can move the headline number, especially in a market where volume anchors are steadier than price. By keeping the steps traceable to capacity, utilization, trade, and validated pricing timing, the final output remains easier to reproduce and audit across updates.

Key Questions Answered in the Report

How large is the 1,4 Butanediol market in 2026 and what is its growth rate?

How large is the 1,4 Butanediol market in 2026 and what is its growth rate?

Which derivative currently dominates consumption?

Which derivative currently dominates consumption?

Why is bio-fermentation gaining popularity in BDO production?

Why is bio-fermentation gaining popularity in BDO production?

Which end-user segment is growing fastest?

Which end-user segment is growing fastest?

How will the EU anti-dumping probe affect global trade flows?

How will the EU anti-dumping probe affect global trade flows?

Page last updated on: