حجم سوق البروتين في المملكة المتحدة

| فترة الدراسة | 2017 - 2029 | |

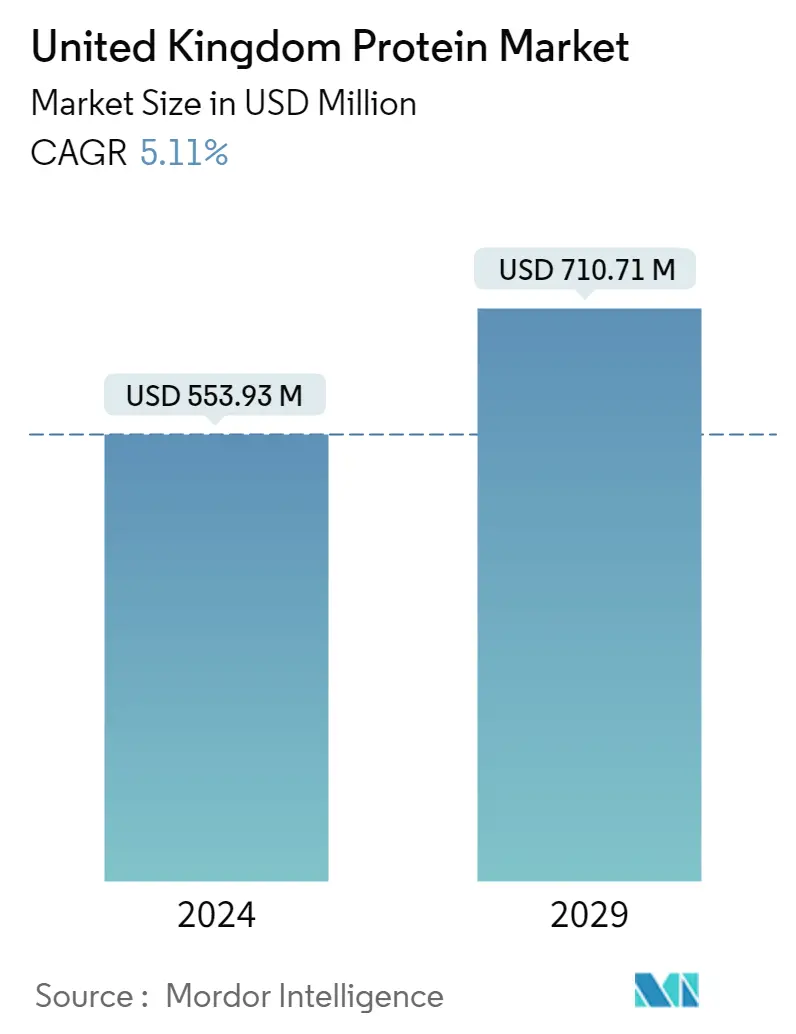

| حجم السوق (2024) | 553.93 مليون دولار أمريكي | |

| حجم السوق (2029) | 710.71 مليون دولار أمريكي | |

| أكبر حصة حسب المستخدم النهائي | طعام و مشروبات | |

| CAGR (2024 - 2029) | 5.11 % | |

| الأسرع نموًا حسب المستخدم النهائي | المكملات | |

| تركيز السوق | قليل | |

اللاعبين الرئيسيين | ||

*تنويه: لم يتم فرز اللاعبين الرئيسيين بترتيب معين |

تحليل سوق البروتين في المملكة المتحدة

يقدر حجم سوق البروتين في المملكة المتحدة بـ 553.93 مليون دولار أمريكي في عام 2024، ومن المتوقع أن يصل إلى 710.71 مليون دولار أمريكي بحلول عام 2029، بمعدل نمو سنوي مركب قدره 5.11٪ خلال الفترة المتوقعة (2024-2029).

إن التساهل الناشئ تجاه المنتجات الموجهة نحو الصحة مع الوعي العام بالبروتين يؤثر على النمو

- من حيث التطبيق، في عام 2022، كانت صناعة الأغذية والمشروبات هي قطاع التطبيقات الرائد للبروتين في المنطقة، يليها قطاع الأعلاف الحيوانية. في فئة المأكولات والمشروبات، استحوذ قطاع اللحوم وبدائل اللحوم على حصة كبيرة من الحجم تبلغ 32.40%، يليه قطاع الألبان وبدائل الألبان بحصة تبلغ 27.9% في عام 2022. وتعد المملكة المتحدة السوق الرائدة للحوم وبدائلها. منتجات الألبان البديلة. يطلق السوق باستمرار مصادر صحية للبروتين المشتق من النباتات أو الأعشاب البحرية أو زراعة الخلايا غير الحيوانية أو التخمير أو اللحوم المزروعة، والتي توفر بديلاً لمصادر البروتين التقليدية.

- احتل قطاع الأعلاف الحيوانية ثاني أكبر حصة في السوق، أي 35.5٪ من حيث الحجم في عام 2020، والذي من المتوقع أن يقود السوق بقيمة معدل نمو سنوي مركب اسمي يبلغ 2.65٪ خلال الفترة المتوقعة. أحد العوامل الرئيسية التي تغذي توسع السوق هو الوعي العام المتزايد بالفوائد الصحية لمكونات البروتين القائمة على الطحالب في الأعلاف الحيوانية. في المراحل المبكرة من تطور الأبقار، تلعب الطحالب الدقيقة دورًا حاسمًا في إضافة العناصر الغذائية إلى أعلاف الحيوانات. كما أنه يعزز النمو البدني ويضمن إنتاج البيض والحليب واللحوم عالية الجودة.

- من حيث القيمة، من بين جميع شرائح المستخدمين النهائيين، من المتوقع أن يسجل قطاع المكملات أسرع معدل نمو بنسبة 6.47٪ خلال الفترة المتوقعة. إن التساهل الناشئ تجاه المنتجات الموجهة نحو الصحة، إلى جانب الاهتمام المتزايد بقائمة المكونات، يقود نمو السوق بشكل كبير. ضمن فئة المكملات الغذائية، تحظى التغذية الرياضية والأداء بحصة بارزة في السوق، ويرجع ذلك أساسًا إلى زيادة الوعي بشأن المدخول الغذائي اليومي، وتساعد منتجات التغذية الرياضية في تعويض العناصر الغذائية المفقودة أثناء عملية الهضم والاستهلاك.

اتجاهات سوق البروتين في المملكة المتحدة

- إن نضج السوق وانخفاض معدلات المواليد هما المسؤولان عن معدل النمو البطيء

- دعم حرفي وخالي من الغلوتين لصناعة المخابز

- تلعب المشروبات الوظيفية دورًا رئيسيًا في نمو السوق المستقبلي

- نمو أقوى في تجارة التجزئة مع تناول المزيد من المستهلكين وجبة الإفطار في المنزل

- صلصات الطبخ تشهد أعلى الطلب في سوق المملكة المتحدة

- برامج خفض السكر تعيق النمو القطاعي خلال فترة التنبؤ

- بديل الألبان لتعزيز نمو السوق

- تغيير التركيبة السكانية للميل نحو المكملات الصحية

- بدائل اللحوم تشهد معدل نمو كبير

- من المتوقع أن ينمو سوق الأغذية المعبأة الجاهزة للأكل على أساس نباتي خلال الفترة المتوقعة

- ارتفاع الطلب على الوجبات الخفيفة اللذيذة في المملكة المتحدة

- برز ميل جيل الألفية نحو اللياقة البدنية باعتباره المحرك الرئيسي للسوق

- زيادة الطلب على المنتجات ذات المصدر الحيواني

- أصبح اتجاه التبسيط مطلوبًا بشكل كبير في المملكة المتحدة

- يؤدي نمو استهلاك البروتين النباتي إلى توفير الفرص للاعبين الرئيسيين في قطاع المكونات

- وتركز المملكة المتحدة على زيادة قدرات إنتاج القمح والبازلاء

نظرة عامة على صناعة البروتين في المملكة المتحدة

سوق البروتين في المملكة المتحدة مجزأ، حيث تشغل الشركات الخمس الكبرى 30.45%. اللاعبون الرئيسيون في هذا السوق هم شركة آرتشر دانييلز ميدلاند، وشركة آرلا فودز AmbA، وشركة دارلينج إنجرينتس، وشركة إنترناشيونال فلافورز آند فراغرانسيس إنك، ومجموعة كيري بي إل سي (مرتبة أبجديًا).

قادة سوق البروتين في المملكة المتحدة

Archer Daniels Midland Company

Arla Foods AmbA

Darling Ingredients Inc.

International Flavors & Fragrances Inc.

Kerry Group PLC

Other important companies include A. Costantino & C. SpA, Agrial Enterprise, Glanbia PLC, Kernel Mycofood, Roquette Frères, Volac International Limited.

*تنويه: لم يتم فرز اللاعبين الرئيسيين بترتيب معين

أخبار سوق البروتين في المملكة المتحدة

- ديسمبر 2021 جمعت شركة Kernel Mycofoods الناشئة المتخصصة في مجال البروتين القائم على الفطريات أكثر من 15 مليون دولار أمريكي في جولة تمويل مؤسسي.

- أغسطس 2021 أطلقت شركة Arla Foods المكونات MicelPure™، وهو معزول من الكازين ميسيلار، في السوق. تحتوي عزلة الكازين ميسيلار الجديدة على ما لا يقل عن 87% من البروتين الأصلي، وهي منخفضة في اللاكتوز والدهون، وهي مستقرة للحرارة، ولها طعم محايد. يتم استخدامه بشكل رئيسي في مشروبات RTD والمشروبات عالية البروتين ومخفوقات المسحوق.

- مايو 2021 أعلنت شركة Darling Ingredients Inc. أن علامتها التجارية Rousselot وسّعت مجموعتها من الجيلاتين المنقى والمعدل من الدرجة الصيدلانية مع إطلاق X-Pure® GelDAT - Gelatin Desaminotyrosine.

تقرير سوق البروتين في المملكة المتحدة – جدول المحتويات

1. الملخص التنفيذي والنتائج الرئيسية

2. مقدمة

- 2.1 افتراضات الدراسة وتعريف السوق

- 2.2 نطاق الدراسة

- 2.3 مناهج البحث العلمي

3. اتجاهات الصناعة الرئيسية

- 3.1 حجم سوق المستخدم النهائي

- 3.1.1 أغذية الأطفال وصيغة الرضع

- 3.1.2 مخبز

- 3.1.3 المشروبات

- 3.1.4 حبوب الإفطار

- 3.1.5 التوابل / الصلصات

- 3.1.6 الحلويات

- 3.1.7 الألبان ومنتجات الألبان البديلة

- 3.1.8 تغذية المسنين والتغذية الطبية

- 3.1.9 اللحوم/الدواجن/المأكولات البحرية ومنتجات اللحوم البديلة

- 3.1.10 المنتجات الغذائية RTE/RTC

- 3.1.11 وجبات خفيفة

- 3.1.12 تغذية الرياضة/الأداء

- 3.1.13 الأعلاف الحيوانية

- 3.1.14 العناية الشخصية ومستحضرات التجميل

- 3.2 اتجاهات استهلاك البروتين

- 3.2.1 حيوان

- 3.2.2 نبات

- 3.3 اتجاهات الإنتاج

- 3.3.1 حيوان

- 3.3.2 نبات

- 3.4 الإطار التنظيمي

- 3.4.1 المملكة المتحدة

- 3.5 تحليل سلسلة القيمة وقنوات التوزيع

4. تجزئة السوق (يشمل حجم السوق من حيث القيمة بالدولار الأمريكي والحجم والتوقعات حتى عام 2029 وتحليل آفاق النمو)

- 4.1 مصدر

- 4.1.1 حيوان

- 4.1.1.1 حسب نوع البروتين

- 4.1.1.1.1 الكازين والكازينات

- 4.1.1.1.2 الكولاجين

- 4.1.1.1.3 بروتين البيض

- 4.1.1.1.4 الجيلاتين

- 4.1.1.1.5 بروتين الحشرات

- 4.1.1.1.6 بروتين الحليب

- 4.1.1.1.7 بروتين مصل اللبن

- 4.1.1.1.8 بروتينات حيوانية أخرى

- 4.1.2 ميكروبية

- 4.1.2.1 حسب نوع البروتين

- 4.1.2.1.1 بروتين الطحالب

- 4.1.2.1.2 البروتين الفطري

- 4.1.3 نبات

- 4.1.3.1 حسب نوع البروتين

- 4.1.3.1.1 بروتين القنب

- 4.1.3.1.2 بروتين البازلاء

- 4.1.3.1.3 بروتين البطاطس

- 4.1.3.1.4 بروتين الأرز

- 4.1.3.1.5 أنا بروتين

- 4.1.3.1.6 بروتين القمح

- 4.1.3.1.7 بروتينات نباتية أخرى

- 4.2 المستخدم النهائي

- 4.2.1 الأعلاف الحيوانية

- 4.2.2 طعام و مشروبات

- 4.2.2.1 بواسطة المستخدم النهائي الفرعي

- 4.2.2.1.1 مخبز

- 4.2.2.1.2 المشروبات

- 4.2.2.1.3 حبوب الإفطار

- 4.2.2.1.4 التوابل / الصلصات

- 4.2.2.1.5 الحلويات

- 4.2.2.1.6 الألبان ومنتجات الألبان البديلة

- 4.2.2.1.7 اللحوم/الدواجن/المأكولات البحرية ومنتجات اللحوم البديلة

- 4.2.2.1.8 المنتجات الغذائية RTE/RTC

- 4.2.2.1.9 وجبات خفيفة

- 4.2.3 العناية الشخصية ومستحضرات التجميل

- 4.2.4 المكملات

- 4.2.4.1 بواسطة المستخدم النهائي الفرعي

- 4.2.4.1.1 أغذية الأطفال وصيغة الرضع

- 4.2.4.1.2 تغذية المسنين والتغذية الطبية

- 4.2.4.1.3 تغذية الرياضة/الأداء

5. مشهد تنافسي

- 5.1 التحركات الاستراتيجية الرئيسية

- 5.2 تحليل حصة السوق

- 5.3 المناظر الطبيعية للشركة

- 5.4 ملفات تعريف الشركة (تتضمن نظرة عامة على المستوى العالمي، ونظرة عامة على مستوى السوق، وقطاعات الأعمال الأساسية، والبيانات المالية، وعدد الموظفين، والمعلومات الأساسية، وتصنيف السوق، وحصة السوق، والمنتجات والخدمات، وتحليل التطورات الأخيرة).

- 5.4.1 A. Costantino & C. SpA

- 5.4.2 Agrial Enterprise

- 5.4.3 Archer Daniels Midland Company

- 5.4.4 Arla Foods AmbA

- 5.4.5 Darling Ingredients Inc.

- 5.4.6 Glanbia PLC

- 5.4.7 International Flavors & Fragrances Inc.

- 5.4.8 Kernel Mycofood

- 5.4.9 Kerry Group PLC

- 5.4.10 Roquette Frères

- 5.4.11 Volac International Limited

6. الأسئلة الإستراتيجية الرئيسية للرؤساء التنفيذيين لصناعة مكونات البروتين

7. زائدة

- 7.1 نظرة عامة عالمية

- 7.1.1 ملخص

- 7.1.2 إطار القوى الخمس لبورتر

- 7.1.3 تحليل سلسلة القيمة العالمية

- 7.1.4 ديناميكيات السوق (DROs)

- 7.2 المصادر والمراجع

- 7.3 قائمة الجداول والأشكال

- 7.4 رؤى أولية

- 7.5 حزمة البيانات

- 7.6 مسرد للمصطلحات

المملكة المتحدة تجزئة صناعة البروتين

تتم تغطية الحيوانات والميكروبات والنباتات كقطاعات حسب المصدر. تتم تغطية أعلاف الحيوانات والأغذية والمشروبات والعناية الشخصية ومستحضرات التجميل والمكملات الغذائية كقطاعات من قبل المستخدم النهائي.

- من حيث التطبيق، في عام 2022، كانت صناعة الأغذية والمشروبات هي قطاع التطبيقات الرائد للبروتين في المنطقة، يليها قطاع الأعلاف الحيوانية. في فئة المأكولات والمشروبات، استحوذ قطاع اللحوم وبدائل اللحوم على حصة كبيرة من الحجم تبلغ 32.40%، يليه قطاع الألبان وبدائل الألبان بحصة تبلغ 27.9% في عام 2022. وتعد المملكة المتحدة السوق الرائدة للحوم وبدائلها. منتجات الألبان البديلة. يطلق السوق باستمرار مصادر صحية للبروتين المشتق من النباتات أو الأعشاب البحرية أو زراعة الخلايا غير الحيوانية أو التخمير أو اللحوم المزروعة، والتي توفر بديلاً لمصادر البروتين التقليدية.

- احتل قطاع الأعلاف الحيوانية ثاني أكبر حصة في السوق، أي 35.5٪ من حيث الحجم في عام 2020، والذي من المتوقع أن يقود السوق بقيمة معدل نمو سنوي مركب اسمي يبلغ 2.65٪ خلال الفترة المتوقعة. أحد العوامل الرئيسية التي تغذي توسع السوق هو الوعي العام المتزايد بالفوائد الصحية لمكونات البروتين القائمة على الطحالب في الأعلاف الحيوانية. في المراحل المبكرة من تطور الأبقار، تلعب الطحالب الدقيقة دورًا حاسمًا في إضافة العناصر الغذائية إلى أعلاف الحيوانات. كما أنه يعزز النمو البدني ويضمن إنتاج البيض والحليب واللحوم عالية الجودة.

- من حيث القيمة، من بين جميع شرائح المستخدمين النهائيين، من المتوقع أن يسجل قطاع المكملات أسرع معدل نمو بنسبة 6.47٪ خلال الفترة المتوقعة. إن التساهل الناشئ تجاه المنتجات الموجهة نحو الصحة، إلى جانب الاهتمام المتزايد بقائمة المكونات، يقود نمو السوق بشكل كبير. ضمن فئة المكملات الغذائية، تحظى التغذية الرياضية والأداء بحصة بارزة في السوق، ويرجع ذلك أساسًا إلى زيادة الوعي بشأن المدخول الغذائي اليومي، وتساعد منتجات التغذية الرياضية في تعويض العناصر الغذائية المفقودة أثناء عملية الهضم والاستهلاك.

| حيوان | حسب نوع البروتين | الكازين والكازينات |

| الكولاجين | ||

| بروتين البيض | ||

| الجيلاتين | ||

| بروتين الحشرات | ||

| بروتين الحليب | ||

| بروتين مصل اللبن | ||

| بروتينات حيوانية أخرى | ||

| ميكروبية | حسب نوع البروتين | بروتين الطحالب |

| البروتين الفطري | ||

| نبات | حسب نوع البروتين | بروتين القنب |

| بروتين البازلاء | ||

| بروتين البطاطس | ||

| بروتين الأرز | ||

| أنا بروتين | ||

| بروتين القمح | ||

| بروتينات نباتية أخرى |

| الأعلاف الحيوانية | ||

| طعام و مشروبات | بواسطة المستخدم النهائي الفرعي | مخبز |

| المشروبات | ||

| حبوب الإفطار | ||

| التوابل / الصلصات | ||

| الحلويات | ||

| الألبان ومنتجات الألبان البديلة | ||

| اللحوم/الدواجن/المأكولات البحرية ومنتجات اللحوم البديلة | ||

| المنتجات الغذائية RTE/RTC | ||

| وجبات خفيفة | ||

| العناية الشخصية ومستحضرات التجميل | ||

| المكملات | بواسطة المستخدم النهائي الفرعي | أغذية الأطفال وصيغة الرضع |

| تغذية المسنين والتغذية الطبية | ||

| تغذية الرياضة/الأداء | ||

| مصدر | حيوان | حسب نوع البروتين | الكازين والكازينات |

| الكولاجين | |||

| بروتين البيض | |||

| الجيلاتين | |||

| بروتين الحشرات | |||

| بروتين الحليب | |||

| بروتين مصل اللبن | |||

| بروتينات حيوانية أخرى | |||

| ميكروبية | حسب نوع البروتين | بروتين الطحالب | |

| البروتين الفطري | |||

| نبات | حسب نوع البروتين | بروتين القنب | |

| بروتين البازلاء | |||

| بروتين البطاطس | |||

| بروتين الأرز | |||

| أنا بروتين | |||

| بروتين القمح | |||

| بروتينات نباتية أخرى | |||

| المستخدم النهائي | الأعلاف الحيوانية | ||

| طعام و مشروبات | بواسطة المستخدم النهائي الفرعي | مخبز | |

| المشروبات | |||

| حبوب الإفطار | |||

| التوابل / الصلصات | |||

| الحلويات | |||

| الألبان ومنتجات الألبان البديلة | |||

| اللحوم/الدواجن/المأكولات البحرية ومنتجات اللحوم البديلة | |||

| المنتجات الغذائية RTE/RTC | |||

| وجبات خفيفة | |||

| العناية الشخصية ومستحضرات التجميل | |||

| المكملات | بواسطة المستخدم النهائي الفرعي | أغذية الأطفال وصيغة الرضع | |

| تغذية المسنين والتغذية الطبية | |||

| تغذية الرياضة/الأداء | |||

تعريف السوق

- المستخدم النهائي - يعمل سوق مكونات البروتين على أساس B2B. يعتبر مصنعو الأغذية والمشروبات والمكملات الغذائية والأعلاف الحيوانية والعناية الشخصية ومستحضرات التجميل من المستهلكين النهائيين في السوق الذي تمت دراسته. يستثني النطاق الشركات المصنعة التي تشتري مصل اللبن السائل/الجاف لاستخدامه في التطبيق كعامل ربط أو مكثف أو تطبيقات أخرى غير بروتينية.

- معدل الاختراق - يتم تعريف معدل الاختراق على أنه النسبة المئوية لحجم سوق المستخدم النهائي المدعم بالبروتين من إجمالي حجم سوق المستخدم النهائي.

- متوسط محتوى البروتين - متوسط محتوى البروتين هو متوسط محتوى البروتين الموجود لكل 100 جرام من المنتج الذي تصنعه جميع شركات المستخدم النهائي التي تدخل ضمن نطاق هذا التقرير.

- حجم سوق المستخدم النهائي - حجم سوق المستخدم النهائي هو الحجم الموحد لجميع أنواع وأشكال منتجات المستخدم النهائي في البلد أو المنطقة.

منهجية البحث

تتبع Mordor Intelligence منهجية مكونة من أربع خطوات في جميع تقاريرنا.

- الخطوة 1: تحديد المتغيرات الرئيسية: يتم اختيار المتغيرات الرئيسية القابلة للقياس (الصناعية والخارجية) المتعلقة بقطاع المنتجات المحدد والبلد من مجموعة من المتغيرات والعوامل ذات الصلة بناءً على البحث المكتبي ومراجعة الأدب ؛ جنبًا إلى جنب مع المدخلات الأولية للخبراء. يتم تأكيد هذه المتغيرات بشكل أكبر من خلال نمذجة الانحدار (حيثما يلزم ذلك).

- الخطوة الثانية: بناء نموذج السوق: من أجل بناء منهجية تنبؤ قوية ، يتم اختبار المتغيرات والعوامل المحددة في الخطوة 1 مقابل الأرقام السوقية التاريخية المتاحة. من خلال عملية تكرارية ، يتم تعيين المتغيرات المطلوبة لتوقع السوق ويتم بناء النموذج على أساس هذه المتغيرات.

- الخطوة 3: التحقق من الصحة والانتهاء منها: في هذه الخطوة المهمة ، يتم التحقق من جميع أرقام السوق والمتغيرات ومكالمات المحللين من خلال شبكة واسعة من خبراء البحوث الأولية من السوق المدروسة. يتم اختيار المستجيبين عبر المستويات والوظائف لتوليد صورة شاملة للسوق المدروسة.

- الخطوة 4: مخرجات البحث: تقارير موحدة ، مهام استشارية مخصصة ، قواعد بيانات ومنصات اشتراك.