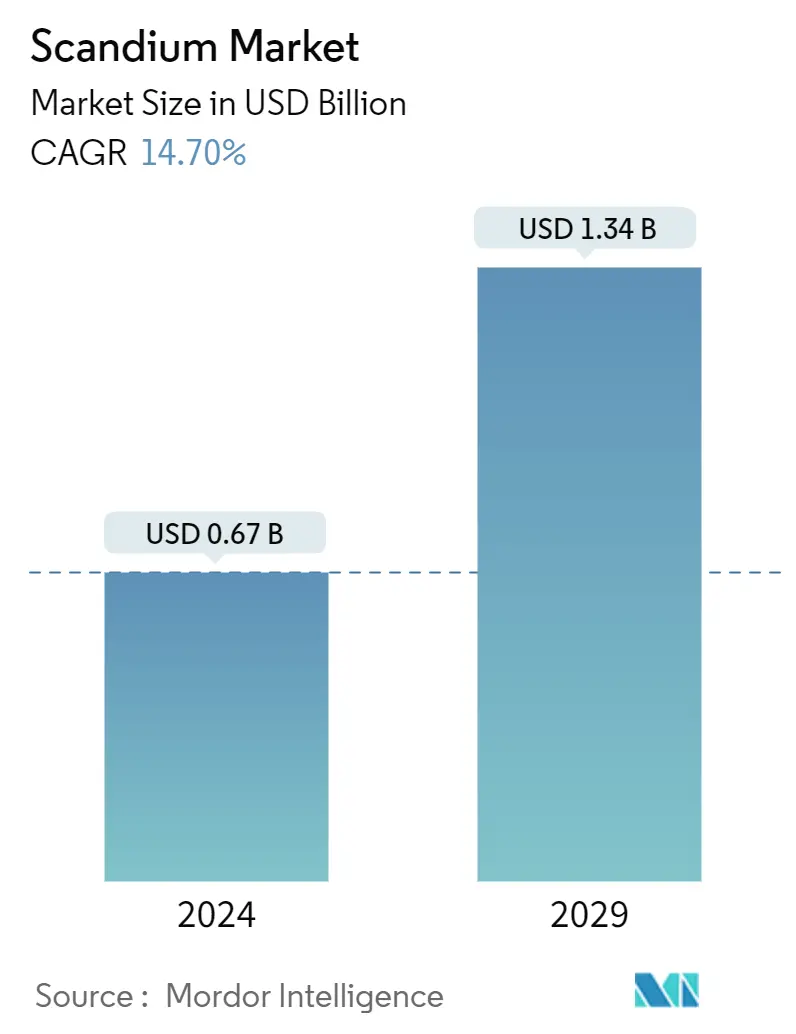

Scandium Market Size

| Study Period | 2024 - 2029 |

| Base Year For Estimation | 2023 |

| Market Size (2024) | USD 0.67 Billion |

| Market Size (2029) | USD 1.34 Billion |

| CAGR (2024 - 2029) | 14.70 % |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Scandium Market Analysis

The Scandium Market size is estimated at USD 0.67 billion in 2024, and is expected to reach USD 1.34 billion by 2029, growing at a CAGR of 14.70% during the forecast period (2024-2029).

- The COVID-19 pandemic negatively impacted the scandium market. Due to the lockdown, major end-user segments such as aerospace and defense, ceramics, and electronics were suspended, reducing the usage of scandium. However, post-pandemic, the market expanded steadily because of the continued activities in major end-user segments.

- In the short term, increasing usage in solid oxide fuel cells (SOFCS) and increasing demand for aluminum-scandium alloys in the aerospace and defense industry are the factors driving the studied market.

- However, the high price of scandium may hinder the growth of the studied market between 2024 and 2029.

- Potential applications in the automotive industry and growing technology for storing energy are likely to give the market opportunities in the coming years.

- China is expected to dominate the market, and the European Union is expected to see the highest CAGR between 2024 and 2029.

Scandium Market Trends

The Solid Oxide Fuel Cells (SOFCs) Segment is Expected to Dominate the Market

- SOFCs use a solid oxide material called an electrolyte, which helps move negative oxygen ions from the cathode to the anode. In these cells, anodes and cathodes are made from special inks that cover the electrolyte. Therefore, SOFCs do not require any precious metal, corrosive acids, or molten material.

- Electrolyte materials are subjected to high temperatures to catalyze natural gas conversion to energy. However, the high temperature for the catalyzing conversion process can lead to the quick degradation of ceramic electrolytes, adding to the capital and maintenance costs.

- Using scandium in solid electrolytes helps the system work at much lower temperatures than traditional SOFCs. So, the use of scandium helped lower the cost of SOFCs, which made them easier to use for power generation in many places.

- As electricity prices go up, people will need to use more environmentally friendly ways to make power, which is likely to create many market opportunities for SOFCs and make scandium even more important.

- Due to growing environmental concerns regarding traditional energy sources like coal and natural gas, solid oxide fuel cells are likely to see increased demand in the future.

- The increasing demand for clean energy over environmental concerns of energy generation from conventional sources, such as coal and natural gas, is expected to drive the demand for solid oxide fuel cells in the future. Solid oxide fuel cells offer high efficiency and deliver environmental and financial benefits. The electrical efficiency of solid oxide fuel cells reaches up to 60%. This means 60% of the energy stored in the fuel is converted to useful electrical energy. This is much higher than the efficiency of coal power plants.

- Furthermore, according to the Energy Information Administration, around USD 2.8 trillion was invested in energy in 2023, out of which USD 1.7 trillion was used for clean energy, including renewable power, nuclear, grids, storage, low-emission fuels, efficiency improvements, and end-use renewables and electrification.

- In addition, according to the US Department of Energy, the share of electricity from clean sources in 2030 could grow to 80%, nearly twice the expected amount before the Inflation Reduction Act passed.

- Furthermore, various expansions in the SOFC market are fueling the demand for scandium. For instance:

- In October 2023, HD Hyundai announced an investment of EUR 45 million (USD 47.6 million) in Estonian solid oxide fuel cell firm Elcogen. With the new investment, the two companies intend to focus on marine propulsion systems and stationary power generation based on Elcogen’s proprietary solid oxide fuel cell (SOFC) and green hydrogen production based around Elcogen’s solid oxide electrolyzer cell (SOEC) technology.

- In August 2023, Bloom Energy, a manufacturer of solid oxide fuel cells, successfully installed the initial phase of a groundbreaking 10-megawatt (MW) solid oxide fuel cell contract with Unimicron Technology Corp., a prominent chip substrate and printed circuit board (PCB) manufacturer in Taiwan.

- The solid oxide fuel cell market is likely to witness a big increase in demand for scandium in the near future.

China is Expected to Dominate the Market

- Scandium in China is produced as a by-product of other materials such as titanium, iron ore, and zirconium. Nowadays, more than 60-70 % of the scandium production in China is as titanium by-products. The sizeable chuck of scandium in the country is also produced by exploiting the residue from titanium dioxide (TiO2) leach streams in pigment plants such as titanium ore like magnetovana–ilmenite located in Panzhihua, China, at a concentration as high as 0.04%.

- Globally, the principal source of scandium is niobium-rare earth element-iron (Nb–REE–Fe), the world's largest REE resource and second largest resource of scandium. It is located in Inner Mongolia, China, and accounts for approximately 90% of global scandium production. In Bayan Obo, scandium is regenerated as a by-product of the mining of the other REEs and iron.

- China has great potential in the fuel cell market as the government increasingly focuses on utilizing clean energy technology to switch to a low-carbon economy. For the past 2–3 years, the Chinese government put great emphasis on the roll-out of fuel cell mobility in the country, shifting the public support focus slightly away from BEV to FCEV. The national government offers CNY 500,000 (USD 73 thousand) as a subsidy for each vehicle.

- Furthermore, the Chinese government announced plans to support around 50,000 zero-emissions fuel cell vehicles by 2025, with plans to rapidly expand to 1 million FCEVs in service by 2030, providing opportunities to SOFCs and the scandium market in the country.

- China is one of the largest aircraft manufacturers and one of the largest markets for domestic air passengers. Moreover, the country’s aircraft parts and assembly manufacturing sector has been growing rapidly, with the presence of over 200 small aircraft parts manufacturers. Also, the Chinese government is investing heavily in increasing its domestic manufacturing capacities.

- China is the largest base for electronics production in the world. China is actively engaged in manufacturing electronic products, such as smartphones, TVs, wires, cables, portable computing devices, gaming systems, and other personal electronic devices. Economic development in China and improving living standards among the population drive consumer electronics demand. Electronic products, such as smartphones, OLED TVs, and tablets, have the highest growth rates in the consumer electronics segment of the market in terms of demand. The revenue is expected to show an annual growth rate of 2.04% by 2025.

- Therefore, the above-mentioned factors are expected to impact the demand for the studied market.

Scandium Industry Overview

The scandium market is consolidated in nature. Some of the major players in the market are Hunan Institute of Rare Earth Metal Materials, MCC Group, Sunrise Energy Metals Limited, Hunan Oriental Scandium Co. Ltd, and Henan Rongjia Scandium Vanadium Technology Co. Ltd.

Scandium Market Leaders

Hunan Institute of Rare Earth Metal Materials

MCC Grop

Sunrise Energy Metals

Hunan Oriental Scandium Co., Ltd.

Henan Rongjia scandium vanadium Technology Co., Ltd

*Disclaimer: Major Players sorted in no particular order

Scandium Market News

- January 2024: NioCorp Developments Ltd agreed with London-based Brunel University London, a leading research university focused on the global application of cast aluminum alloys, to develop innovative aluminum-scandium alloys and applications for use in the automotive sector.

- April 2023: Rio Tinto entered a binding agreement to acquire the Platina Scandium Project, a high-grade scandium resource in New South Wales, from Platina Resources Limited for USD 14 million. The project, near Condobolin in central New South Wales, comprises a long-life, high-grade scalable resource that could produce up to 40 tons per annum of scandium oxide for an estimated period of 30 years.

Scandium Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Usage in Solid Oxide Fuel Cells (SOFCS)

4.1.2 Increasing Demand for Aluminum-Scandium Alloys in the Aerospace and Defense Industry

4.2 Restraints

4.2.1 High Cost of Scandium

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

4.5 Price Analysis

4.6 Environmental Impact Analysis

5. MARKET SEGMENTATION

5.1 Product Type

5.1.1 Oxide

5.1.2 Fluoride

5.1.3 Chloride

5.1.4 Nitrate

5.1.5 Iodide

5.1.6 Alloy

5.1.7 Carbonate and Other Product Types

5.2 End-user Industry

5.2.1 Aerospace and Defense

5.2.2 Solid Oxide Fuel Cells

5.2.3 Ceramics

5.2.4 Lighting

5.2.5 Electronics

5.2.6 3D Printing

5.2.7 Sporting Goods

5.2.8 Other End-user Industries

5.3 Geography

5.3.1 Production Analysis

5.3.1.1 China

5.3.1.2 Russia

5.3.1.3 Philippines

5.3.1.4 Rest of the World

5.3.2 Consumption Analysis

5.3.2.1 United States

5.3.2.2 China

5.3.2.3 Russia

5.3.2.4 Japan

5.3.2.5 Brazil

5.3.2.6 European Union

5.3.2.7 Rest of the World

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%) **/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Guangxi Maoxin Technology Co. Ltd

6.4.2 Henan Rongjia Scandium Vanadium Technology Co. Ltd

6.4.3 Huizhou Top Metal Materials Co. Ltd

6.4.4 Hunan Rare Earth Metal Materials Research Institute Co. Ltd

6.4.5 Hunan Oriental Scandium Co. Ltd

6.4.6 JSC Dalur

6.4.7 MCC Group

6.4.8 NioCorp Development Ltd

6.4.9 Rio Tinto

6.4.10 Rusal

6.4.11 Scandium International Mining Corporation

6.4.12 Stanford Advanced Materials

6.4.13 Sumitomo Metal Mining Co. Ltd (Taganito HPAL nickel Corp.)

6.4.14 Sunrise Energy Metals Limited

6.4.15 Treibacher Industrie AG

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Potential Applications in the Automotive industry

7.2 Growing Technology for Storing Energy

Scandium Industry Segmentation

Scandium, with the chemical symbol Sc and atomic number 21, is a silver-white transitional metal categorized as a rare-earth element. It possesses distinctive traits such as lightness, a high melting point, and a small ionic radius. Due to its small ion size, it seldom forms concentrations exceeding 100 ppm naturally, as it doesn't readily bond with common ore-forming anions. Notably, its main applications include solid oxide fuel cells (SOFCs) and aluminum-scandium alloys, enhancing strength and performance, particularly due to its fine grain refinement, which reduces hot cracking in welds and improves fatigue behavior.

The scandium market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into oxide, fluoride, chloride, nitrate, iodide, alloy, carbonate, and other product types. By end-user industry, the market is segmented into aerospace and defense, solid oxide fuel cells, ceramics, lighting, electronics, 3D printing, sporting goods, and other end-user industries. The report also covers the market size and forecasts for scandium in 6 countries across major regions. For each segment, market sizing and forecasts were made based on revenue (USD million).

| Product Type | |

| Oxide | |

| Fluoride | |

| Chloride | |

| Nitrate | |

| Iodide | |

| Alloy | |

| Carbonate and Other Product Types |

| End-user Industry | |

| Aerospace and Defense | |

| Solid Oxide Fuel Cells | |

| Ceramics | |

| Lighting | |

| Electronics | |

| 3D Printing | |

| Sporting Goods | |

| Other End-user Industries |

| Geography | |||||||||

| |||||||||

|

Scandium Market Research FAQs

How big is the Scandium Market?

The Scandium Market size is expected to reach USD 0.67 billion in 2024 and grow at a CAGR of 14.70% to reach USD 1.34 billion by 2029.

What is the current Scandium Market size?

In 2024, the Scandium Market size is expected to reach USD 0.67 billion.

Who are the key players in Scandium Market?

Hunan Institute of Rare Earth Metal Materials, MCC Grop, Sunrise Energy Metals, Hunan Oriental Scandium Co., Ltd. and Henan Rongjia scandium vanadium Technology Co., Ltd are the major companies operating in the Scandium Market.

What years does this Scandium Market cover, and what was the market size in 2023?

In 2023, the Scandium Market size was estimated at USD 0.57 billion. The report covers the Scandium Market historical market size for years: . The report also forecasts the Scandium Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Scandium Industry Report

Statistics for the 2024 Scandium market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Scandium analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.