Ethylene Vinyl Acetate (EVA) Market Size

| Study Period | 2019 - 2029 |

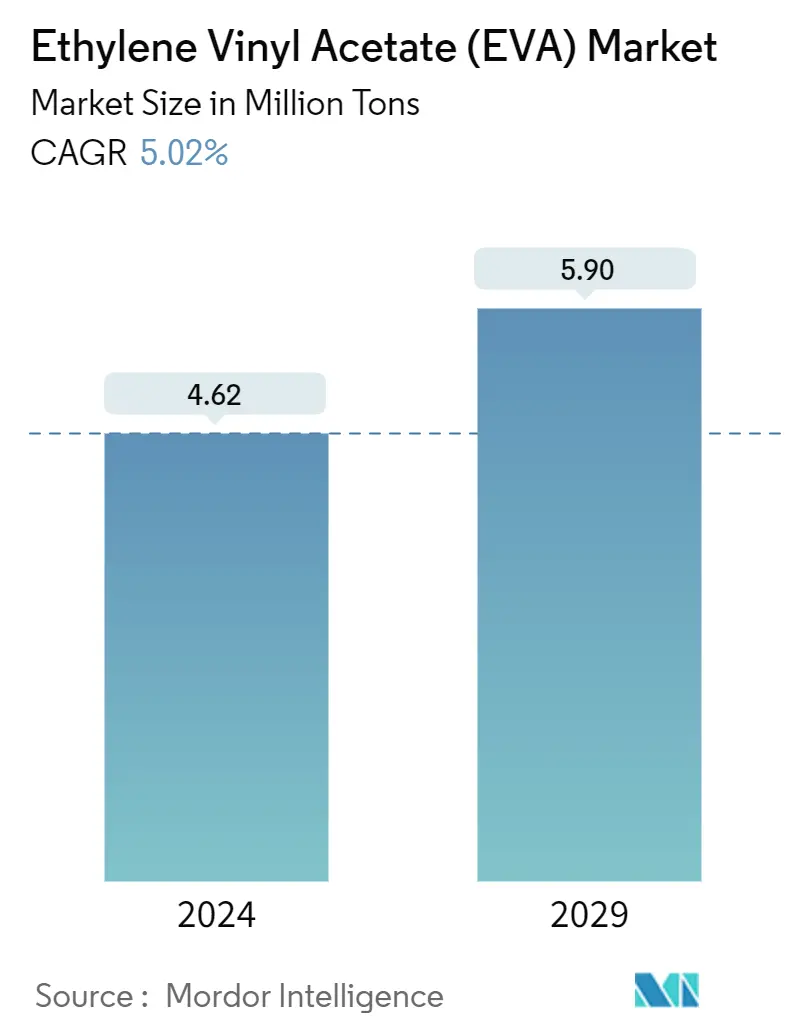

| Market Volume (2024) | 4.62 Million tons |

| Market Volume (2029) | 5.90 Million tons |

| CAGR (2024 - 2029) | 5.02 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Ethylene Vinyl Acetate (EVA) Market Analysis

The Ethylene Vinyl Acetate Market size is estimated at 4.62 Million tons in 2024, and is expected to reach 5.90 Million tons by 2029, growing at a CAGR of 5.02% during the forecast period (2024-2029).

- The COVID-19 pandemic severely impacted market growth in various sectors. Stoppage or slowdown of projects, movement restrictions, production halts, and labor shortages to contain the pandemic have led to a decline in the ethylene vinyl acetate market growth. However, it recovered significantly in 2021, owing to rising consumption from various applications, including films, adhesives, and foams.

- In the short term, the increasing demand for ethylene-vinyl acetate (EVA) from the packaging industry and agricultural applications is expected to drive the market.

- The increasing threat of substitutes is expected to hinder the market's growth.

- The increasing demand for photovoltaic (PV) solar cell encapsulants is expected to offer growth opportunities for the market between 2024 and 2029.

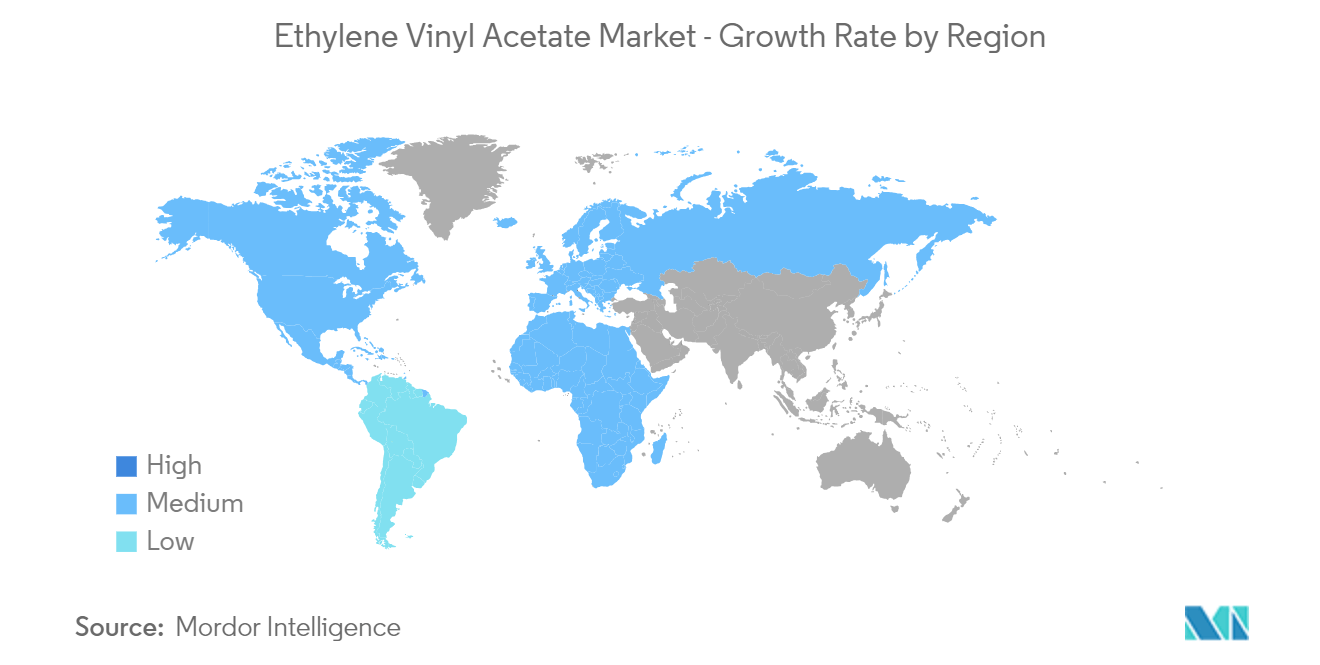

- Asia-Pacific is expected to dominate the market and is likely to witness the highest CAGR from 2024 to 2029, as the economies in the region are growing, driving the consumption of films, adhesives, and foams.

Ethylene Vinyl Acetate (EVA) Market Trends

The Films Segment is Expected to Dominate the Market

- Ethylene vinyl acetate (EVA) is a copolymer resin that, when heated and mixed thoroughly before being extruded through a flat die, forms EVA films. These films are available in white, clear, and other colors, providing a non-sticky and smooth surface finish. EVA films are generally sandwiched between two plastic or glass sheet pieces as an interlayer.

- During the manufacturing of EVA films, the thermoplastic resin is typically copolymerized with LLDPE, LDPE, or other resins, or it is manufactured as a part of a multi-layer film. Generally, the percentage of ethylene vinyl acetate ranges between 2 and 25 in the case of copolymers and blends.

- Adding EVA helps to enhance the sealability and clarity of olefins, improve the low-temperature performance, and reduce the melting point. Further, a higher percentage of vinyl acetate content can significantly impact the mechanical properties and lower the barrier to moisture and gas while improving the clarity.

- Some of the advantages of EVA films are relatively higher tensile strength, sound barrier properties, excellent transparency, superior adhesion, waterproofing in nature, and UV protection. It also exhibits good resistance and durability at high temperatures, strong winds, and humid environments.

- In lower percentages, EVA films have been used for frozen food packaging (at 6% EVA), bread bags (at 2% EVA), and ice bags (at 4% EVA), as they help provide enhanced sealability for such applications. Further, in higher percentages, with up to 20% EVA, these films are used in applications involving low melt/total batch inclusion bags. Similarly, in solar panels, films with up to 33% EVA are used as a bonding layer for these panels.

- However, recently, food packaging applications have seen increased consumption of metallocene PE as an alternative to EVA films, as it offers superior down-gauging properties and faster hot tack. The use of mPE allows for thinner films and overall packaging while providing a relatively better barrier to moisture and gases.

- EVA is still extensively used across several film applications. Usually, EVA resin is combined with other film resins to obtain the desired properties. Some of the other key applications include using EVA films as sealants in dairy and meat packaging applications, photovoltaic encapsulation, wire and cable insulation, and glass lamination to help improve its impact resistance.

- Some of the key manufacturers of EVA films have been increasingly investing in production expansion projects, given the growing demand for EVA films in critical applications. For instance, in February 2023, SVECK, one of the largest suppliers of EVA films for PV modules in China, announced its decision to invest around CNY 1.36 billion (~USD 203 million) into its production expansion project. The new factory will be built in two phases, in Yancheng, China’s Jiangsu, at a planned annual capacity of 420 million sq. m. The first phase is expected to begin commercial operations by Q3 2023, with an annual capacity of 120 million sq. m spread across 16 production lines.

- The increasing demand for EVA films in non-food applications, photovoltaic encapsulations, and solar panels is anticipated to strengthen the EVA films market between 2024 and 2029.

Asia-Pacific is Expected to Dominate the Market

- The Asia-Pacific market is the largest ethylene vinyl acetate (EVA) market. It is also expected to remain the largest market between 2024 and 2029, owing to the major demand from China and India, mainly for the adhesive and packaging industry applications.

- Ethylene vinyl acetate copolymers (EVA) are commonly used in packaging applications, replacing polyvinyl chloride as the most used resin. EVA copolymers require no curing or plasticizer and have no odor. The use of EVA in the packaging sector is increasing significantly, owing to its advantages over the conventional packaging plastics used.

- The Chinese packaging industry is expected to grow. As projected by the government, the industry is expected to achieve a growth rate of nearly 6.8%. The report published by the Chinese government foresees the industry achieving a valuation of CNY 2 trillion (approximately USD 290 billion) by 2025. The growing Chinese food industry, which ranks among the largest globally, is expected to affect the EVA market.

- Moreover, India has a huge packaging industry. The country is expected to witness consistent growth between 2024 and 2029, owing to the rise of customized packaging in the food segment, like microwave, snack, and frozen foods, along with increasing exports.

- According to the Packaging Industry Association of India (PIAI), the Indian packaging industry is expected to grow by 22% between 2024 and 2029. The Indian packaging market is expected to reach USD 204.81 billion by 2025, registering a CAGR of 26.7% till 2025. Therefore, the EVA market is expected to grow in the region.

- EVA is also increasingly used in footwear, hockey pads, martial arts gloves, and other sports goods due to its shock absorber properties.

- The Chinese footwear industry consists of over 14,400 businesses. China is the largest footwear producer in the world. China accounts for over 50% of footwear exports. The country exported more than 9,000 million pairs of shoes in 2022.

- Furthermore, according to the Union Minister for Trade Industries, Consumer Affairs, Food, and Public Distribution and Textiles, India has the potential to become a world leader in the footwear and leather sector due to government and industry efforts. For instance, the leather industry is expected to grow, owing to a free trade agreement (FTA) with the United Arab Emirates, which saw exports increase by 64% in November 2022.

- India is the second largest producer of footwear and leather garments, boasting nearly 3 billion sq. ft of tanneries worldwide. In addition, in 2021, the Center passed an expenditure of INR 1,700 crore (USD 205.8 million) to the Indian Footwear and Leather Development Program (IFLDP) for implementation from 2021 to 2026.

- All the aforementioned factors are expected to boost the demand for the market studied between 2024 and 2029.

Ethylene Vinyl Acetate (EVA) Industry Overview

The global ethylene vinyl acetate market is partially consolidated, with top-level players accounting for a sizeable global market share. The major manufacturers of ethylene vinyl acetate (EVA) are Exxon Mobil Corporation, Hanwha Solutions, Dow, Formosa Plastics Corporation, and Celanese Corporation.

Ethylene Vinyl Acetate (EVA) Market Leaders

Exxon Mobil Corporation

Hanwha Solutions

Dow

Formosa Plastics Corporation

Celanese Corporation

*Disclaimer: Major Players sorted in no particular order

Ethylene Vinyl Acetate (EVA) Market News

- June 2023: PetroChina Guangxi Petrochemical Company announced the license of the LyondellBasell polyethylene technology at its facility in Qinzhou City, Guangxi, China. The Lupotech process technology would produce mainly low-density polyethylene (LDPE) with ethylene vinyl acetate copolymers (EVA).

- February 2023: Celanese Corporation announced the completion of an ultra-low capital project to repurpose existing manufacturing and infrastructure assets to unlock additional ethylene vinyl acetate (EVA) capacity at its facility in Edmonton, Alberta. This expansion resulted in a 35% growth in the EVA capacity of the plant.

Ethylene Vinyl Acetate Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Demand from the Packaging Industry

4.1.2 Increasing Demand from Agricultural Applications

4.2 Restraints

4.2.1 Increasing Threat of Substitutes

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Volume)

5.1 Grade

5.1.1 Low Density

5.1.2 Medium Density

5.1.3 High Density

5.2 Application

5.2.1 Films

5.2.2 Adhesives

5.2.3 Foams

5.2.4 Solar Cell Encapsulation

5.2.5 Other Applications

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of the Middle East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Asia Polymer Corporation

6.4.2 BASF-YPC Company Limited

6.4.3 Benson Polymers

6.4.4 Braskem

6.4.5 Celanese Corporation

6.4.6 China Petrochemical Corporation

6.4.7 Clariant

6.4.8 Dow

6.4.9 Exxonmobil Corporation

6.4.10 Formosa Plastics Corporation

6.4.11 Hanwha Solutions

6.4.12 HD Hyundai

6.4.13 Innospec

6.4.14 Jiangsu Sailboat Petrochemical Co. Ltd

6.4.15 Levima Advanced Materials Corporation

6.4.16 Lotte Chemical Corporation

6.4.17 LG Chem

6.4.18 Lyondellbasell Industries Holdings BV

6.4.19 Repsol

6.4.20 Saudi Arabian Oil Co. (Arlanxeo)

6.4.21 Sinochem Holdings Corporation Ltd

6.4.22 Sipchem Company

6.4.23 Sumitomo Chemical Co. Ltd

6.4.24 Zhejiang Petroleum & Chemical Co. Ltd

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Increasing Demand for Photovoltaic (PV) Solar Cell Encapsulants

Ethylene Vinyl Acetate (EVA) Industry Segmentation

Ethylene-vinyl acetate is the thermoplastic resin produced by vinyl acetate monomer and ethylene co-polymerization process in a high-pressure reactor. The major applications of EVA include packaging, plastic goods industries, footwear, pipes, wire and cable insulation, toys, photovoltaic encapsulation, corks, medical packaging, hot melt adhesives, and glass lamination.

The ethylene-vinyl acetate (EVA) market is segmented by grade, application, and geography. By grade, the market is segmented into low density, medium density, and high density. By application, the market is segmented into films, adhesives, foams, solar cell encapsulation, and other applications. The report covers the market sizes and forecasts for the global ethylene vinyl acetate (EVA) market in 15 countries across major regions. The report offers the market size in terms of volume (tons) for all the abovementioned segments.

| Grade | |

| Low Density | |

| Medium Density | |

| High Density |

| Application | |

| Films | |

| Adhesives | |

| Foams | |

| Solar Cell Encapsulation | |

| Other Applications |

| Geography | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

Ethylene Vinyl Acetate Market Research FAQs

How big is the Ethylene Vinyl Acetate Market?

The Ethylene Vinyl Acetate Market size is expected to reach 4.62 million tons in 2024 and grow at a CAGR of 5.02% to reach 5.90 million tons by 2029.

What is the current Ethylene Vinyl Acetate Market size?

In 2024, the Ethylene Vinyl Acetate Market size is expected to reach 4.62 million tons.

Who are the key players in Ethylene Vinyl Acetate Market?

Exxon Mobil Corporation, Hanwha Solutions, Dow, Formosa Plastics Corporation and Celanese Corporation are the major companies operating in the Ethylene Vinyl Acetate Market.

Which is the fastest growing region in Ethylene Vinyl Acetate Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Ethylene Vinyl Acetate Market?

In 2024, the Asia Pacific accounts for the largest market share in Ethylene Vinyl Acetate Market.

What years does this Ethylene Vinyl Acetate Market cover, and what was the market size in 2023?

In 2023, the Ethylene Vinyl Acetate Market size was estimated at 4.39 million tons. The report covers the Ethylene Vinyl Acetate Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Ethylene Vinyl Acetate Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Ethylene Vinyl Acetate Industry Report

Statistics for the 2024 Ethylene Vinyl Acetate (EVA) market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Ethylene Vinyl Acetate (EVA) analysis includes a market forecast outlook to for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.