Control Valve Market Size

| Study Period | 2019 - 2029 |

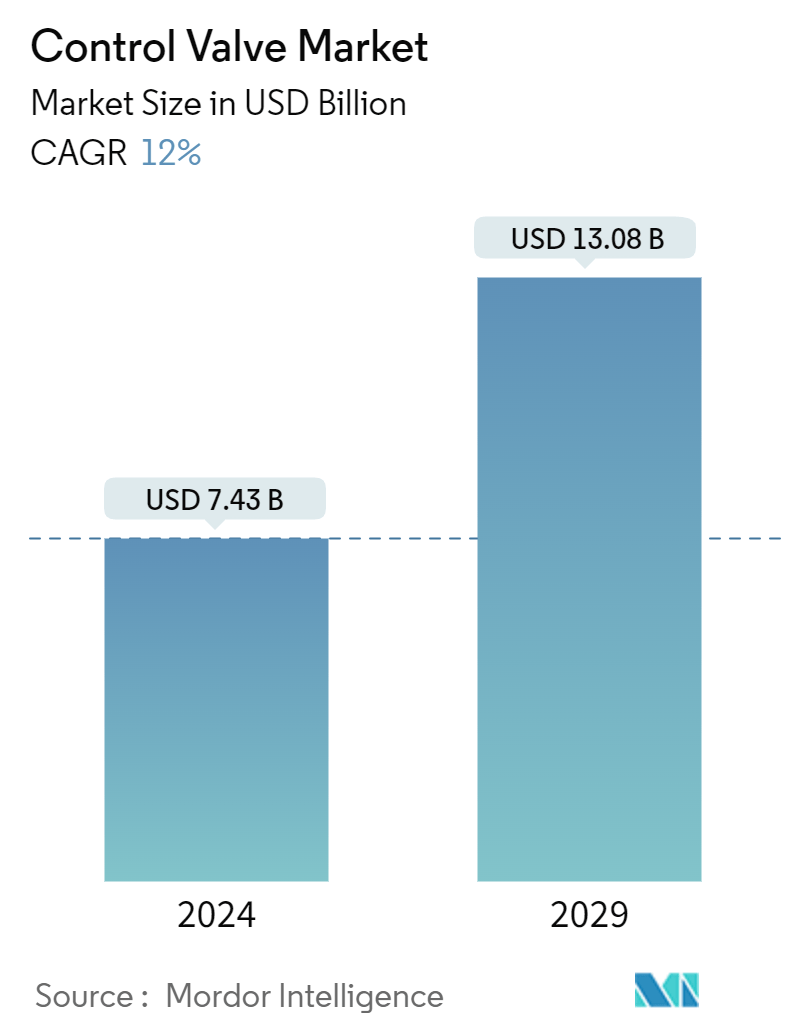

| Market Size (2024) | USD 7.43 Billion |

| Market Size (2029) | USD 13.08 Billion |

| CAGR (2024 - 2029) | 12.00 % |

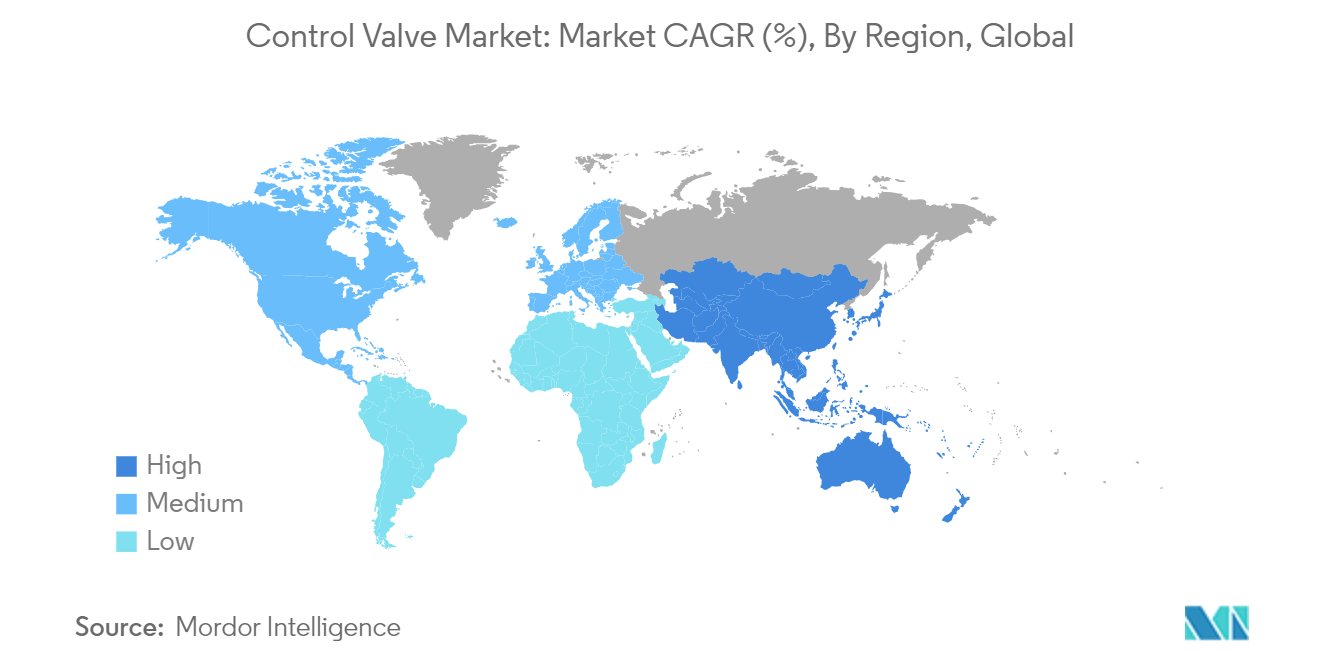

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Control Valve Market Analysis

The Control Valve Market size is estimated at USD 7.43 billion in 2024, and is expected to reach USD 13.08 billion by 2029, growing at a CAGR of 12% during the forecast period (2024-2029).

Over the forecast period, increasing investments in pipeline and infrastructure expansion and the increasing adoption of automation across several industries are expected to boost the demand for control valves.

- A control valve is a device utilized to regulate fluid flow by adjusting the size of the flow passage in response to a signal from a controller. This facilitates the precise flow rate management and subsequent regulation of process variables such as pressure, temperature, and liquid level, which are crucial in industries such as oil and gas, water management, power generation, food and beverages, and automotive. Typically, two control valves, linear and rotary, are employed in various industries, offering superior efficiency and safety.

- A control valve can be operated through electrical, pneumatic, or hydraulic means. It receives a signal from a controller, such as a Programmable Logic Controller (PLC), to initiate movement and consequently alter the flow. Whether a PLC or a Distributed Control System (DCS), the controller compares the current flow rate with the desired setpoint value. Subsequently, the controller generates an output to adjust the valve and achieve the desired flow rate.

- Technological advancements have played a key role in shaping innovative solutions that enhance the efficiency of process plants by streamlining their operations. As industry requirements continue to evolve, suppliers of control valves and valve automation solutions are expected to develop products and processes that address these new challenges. The control valves market is anticipated to grow in the coming years, driven by increasing automation in various process industries, rising investment in the oil and gas sector, and high-power requirements.

- The growth of the control valve market is being propelled by several factors, including the escalating requirement for wireless infrastructure to monitor equipment in diverse plants, an increased emphasis on automation, and a rising number of process industry establishments. In response to market demand, control valves with many cycles and the ability to withstand high temperatures have been developed. Additionally, the growing emphasis on investing in alternative energy sources, particularly renewable energy, has created new opportunities and potential uses for control valves. For example, the IEA forecasts that 70% of all global energy investment will be directed toward renewable energy.

- Market growth is expected to be further boosted over the forecast period due to the increasing adoption of industrial automation, which will drive the use of smart control valves. The demand for control valves is driven by the growing number of power generation plants worldwide and the increasing need for energy and power from developing economies. These valves are also utilized in nuclear power plants, particularly in chemical treatment, feed water, cooling water, and steam turbine control systems.

- Fluctuations significantly hinder the control valve market’s growth in terms of raw material prices. The costs of raw materials play a crucial role in determining the prices of control valves, and an increase in raw material prices poses a significant challenge for vendors as it can diminish their profit margin. Copper, stainless steel, cast iron, aluminum, brass, and bronze are the primary raw materials used to produce control valves. The absence of standardized certifications and government policies is anticipated to serve as restraints to market growth.

- The COVID-19 pandemic caused a widespread economic crisis across multiple industries. Notably, the oil and gas sector was severely impacted, leading to a significant decline in oil prices. Consequently, investments in the sector have dwindled, impeding market innovations. Nevertheless, amidst the pandemic, there was a notable proliferation of manufacturing automation, prompting control valve suppliers to seek market consolidation through mergers and acquisitions.

Control Valve Market Trends

The Oil and Gas Segment is Expected to Drive the Market

- Valves play a crucial role in the oil and gas sector as they are vital to any piping system. Their primary functions include equipment isolation and protection, flow rate control, and guidance and direction of the crude oil refining process. These valves are designed to regulate flow rate, temperature, and pressure through a controller's electrical, hydraulic, or pneumatic signals. Their automatic operation allows for remote operation, eliminating an operator's need for constant monitoring and adjustment.

- Control valves are gaining popularity in the oil and gas sector owing to their ability to regulate flow rate, pressure, and temperature. These valves adjust the flow passage size based on signals from a hydraulic, pneumatic, or electrical controller, enabling remote operation. Furthermore, increased investments in fluid handling technology, particularly in the oil and gas sector, are significantly contributing to the growth of the control valve market.

- The increasing inclination toward digitalization and automation within the oil and gas sector is increasing the need for control valves. Consequently, manufacturers of control valves are consistently involved in research and development endeavors to create and enhance their offerings in accordance with the demands of end-user industries. The escalating number of oil and gas exploration ventures in regions like the Middle East, Africa, China, and North America is projected to bolster the market’s growth significantly.

- In June 2023, Norway declared its endorsement of 19 oil and gas ventures on the Norwegian continental shelf, with a total investment value exceeding USD 19 billion. These projects encompass novel developments, expanding existing fields, and investing in projects to augment extraction at existing areas. The Ukraine conflict augmented Norway's revenues as European nations previously dependent on Russia sought alternative energy sources. Consequently, significant investments in the European Union to enhance self-reliance in the oil and gas sector will amplify opportunities for control valves.

- The oil and gas sector relies on control valves, making it a pivotal sector for their utilization. Control valves are in high demand globally due to new oil and gas exploration projects, transportation pipeline initiatives, and maintenance operations.

- As per the International Energy Agency (IEA), the global demand for fossil fuels such as oil, gas, and coal is projected to reach an unprecedented peak by 2030. This surge can be attributed to evolving energy policies worldwide, the rapid advancement of clean technologies like solar panels and electric vehicles, the growing adoption of heat pumps, and the compelled transition from gas in Europe following Russia's invasion of Ukraine. Furthermore, the sector’s escalating automation technologies are anticipated to propel the market growth significantly.

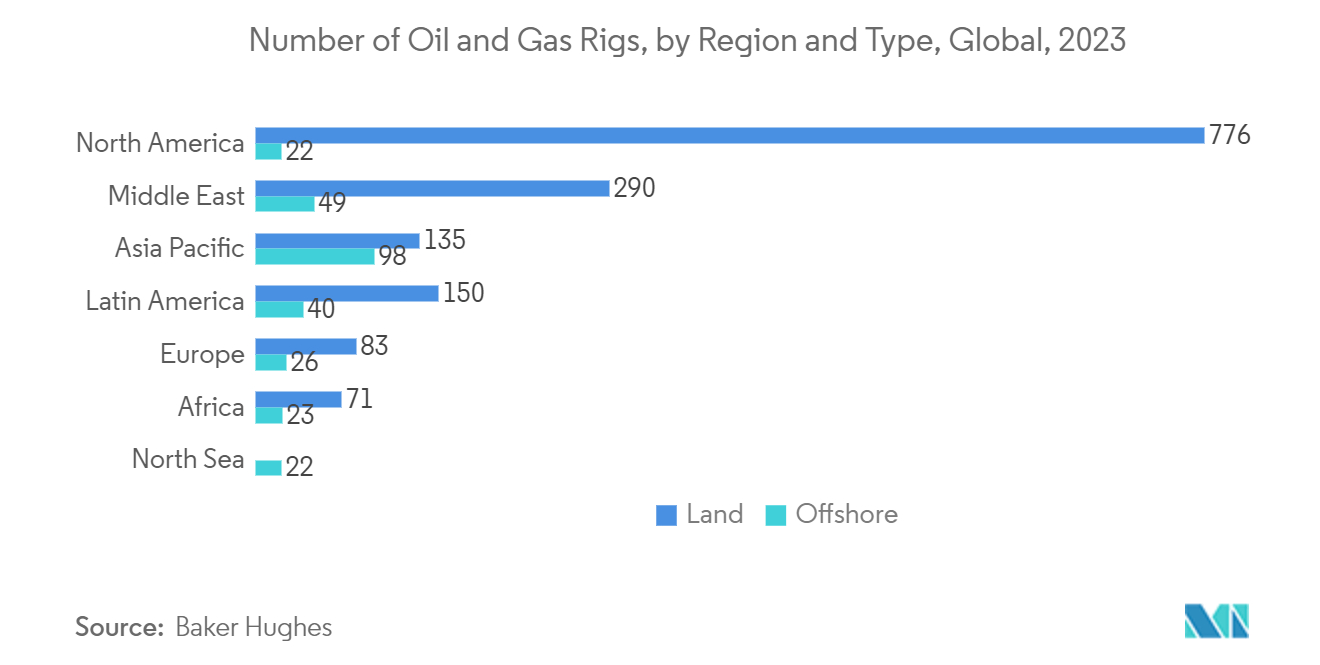

- The demand for control valves across onshore applications is expected to rise with the increasing distribution of oil and gas. For instance, according to EIA, in 2025, it is projected that 28% of the world's crude oil production will be derived from offshore sources, with the remaining 72% being extracted onshore.

- As of February 2024, there were 296 land rigs in that region, with a further 53 rigs located offshore in the Middle East and 95 land rigs in that region, with 16 rigs located offshore in Africa. These notable capabilities and the anticipated growth in the oil and gas industry will undoubtedly generate substantial prospects for the market.

North America is Expected to Hold a Significant Market Share

- North America is one of the world's most significant markets for control valves. There is immense demand from various industries in the United States and Canada, including oil and gas, electricity, food and packaging, and chemicals. With rapid industrial automation, the region is expected to spearhead the need for control valves.

- Rapid industrialization and the growing transportation sector in these nations are expected to increase the demand for oil and gas. The need to provide potable water to the ever-increasing population also leads to the setting up of desalination plants, further resulting in the demand for control valves. Waste and wastewater management is also a considerable segment that is expected to drive future demand.

- The United States plays a critical role in increasing the demand from the region compared to Canada. The demand from almost all the end-user segments is increasing, especially from the oil and gas, refining, and power generation segments. Major industries in the country, such as oil and gas, renewable energy, and water and wastewater treatment, are moving toward valve technology with embedded processors and networking capability to work alongside sophisticated monitoring technology coordinated through a central control station.

- The United States is experiencing a significant expansion in oil production. ExxonMobil, a prominent oil producer in the country, announced its intention to augment production activity in the Permian Basin of West Texas, with a target of producing over 1 million barrels per day (bpd) of oil equivalent by 2024. This represents an increase of almost 80% compared to the current production capacity. Chevron was projected to increase its net oil-equivalent production to 600,000 bpd by 2020 and 900,000 bpd by 2023.

- The shale oil boom in North America generated a significant need for fluid handling equipment and components, particularly control valves. These valves play a crucial role in regulating the shale oil exploration and production process and ensuring the smooth transportation of shale oil through pipelines. The initiation of new upstream oil and gas exploration projects is anticipated to fuel the demand for control valves in the oil and gas industry.

- In the United States, developing new shale oil projects necessitates the construction of additional pipelines for the transportation of shale oil. According to Baker Hughes, North America currently boasts the highest number of oil and gas rigs worldwide. As of May 2023, the region had a total of 776 land rigs, with an additional 22 rigs situated offshore. The number of oil and gas rigs experienced a surge in late 2022 due to the gradual impact of sanctions on Russian exports, resulting in increased exploration activities in North America.

- The region has experienced a surge in the utilization of control valves due to the heightened emphasis on renewable energy initiatives, resulting in a rapid rise in the number of solar thermal energy facilities. The region boasts an abundance of wind, solar, geothermal, hydro, and biomass resources. The demand for renewable energy projects is fueled by ample financing opportunities and a highly skilled workforce.

- The water and wastewater industry is a significant consumer of fluid handling technology due to increasingly stringent regulations regarding the treatment and cleanliness of water. The increasing investments in the region's water and wastewater industry are expected to offer significant market growth opportunities.

Control Valve Indsutry Overview

The control valve market is highly fragmented due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are Emerson Electric Co., Flowserve Corporation, Baker Hughes Company, Metso Corporation, and CIRCOR International Inc. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- February 2024: Emerson released innovative solutions that transform valves installed in industrial applications and interact with end users globally. End users need to know how their control valves are performing, address any issues, and improve valve performance in general, for instance, by reducing maintenance. The Fisher™ FIELDVUE™ DVC7K digital valve controller addresses these and other issues by creating an optimized path to action.

- October 2023: Andritz signed an agreement with Flowserve Corporation to acquire its NAF AB valve business. The production plant and equipment deliveries have been equipped with NAF control valves for many years. This acquisition further extended and strengthened Andritz's product and service portfolio in process control.

- May 2023: Emerson unveiled the ASCO Series 209 proportional flow control valves, which boast unparalleled precision, pressure ratings, flow characteristics, and energy efficiency within a specially designed, space-saving structure. These valves, with their optimal size and exceptional performance, enable users to accurately regulate fluid flow in various devices demanding meticulous performance, such as those utilized in medical equipment, food and beverage, and HVAC industries.

Control Valve Market Leaders

Emerson Electric Co.

Flowserve Corporation

Baker Hughes Company

Metso Corporation

CIRCOR International Inc.

*Disclaimer: Major Players sorted in no particular order

Control Valve Market News

- March 2024: Precision Pump & Valve ("PPV") announced a partnership with Beaumont Manufacturing & Distribution ("BMD"). The new partnership will allow PPV to further serve customers in the oil and gas surface production market, including midstream and upstream users, fabrication shops, and others. The partnership will allow PPV to provide all BMD products to oil producers across the United States.

- November 2023: Emerson announced its innovative Fisher Whisper Trim Technology for use in rotary and globe valves. It presented an extension to its existing portfolio of Whisper noise solutions. The next generation of Fisher Whisper Trim technology focuses on addressing noise issues with the help of additive manufacturing and other advanced techniques to create trim designs with increased capabilities.

Control Valve Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Consumers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Assessment of COVID-19 Impact on the Industry

5. MARKET DYNAMICS

5.1 Industry Supply Chain Analysis

5.2 Market Drivers

5.2.1 Growing emphasis on Power and Water and Wastewater in Emerging Markets

5.2.2 Focus of End Users on Environmental Issues and Refurbishment of Aging Infrastructure to Stay Competitive

5.3 Market Challenges

5.3.1 Focus of End Users on Environmental Issues and Refurbishment of Aging Infrastructure to Stay Competitive

5.3.2 Dynamic Change in Oil Prices is Expected to Influence the Overall Spending on the Projects

5.4 Market Opportunities

6. MARKET SEGMENTATION

6.1 By Type

6.1.1 Globe

6.1.2 Ball

6.1.3 Butterfly

6.1.4 Plug

6.1.5 Diaphragm

6.1.6 Other Types of Valves

6.2 By End-user Industry

6.2.1 Oil and Gas

6.2.2 Chemical, Petrochemical, and Fertilizer

6.2.3 Energy and Power

6.2.4 Water and Wastewater Treatment

6.2.5 Metal and Mining

6.2.6 Other End-user Industries (Food and Beverage, Pharmaceutical, Pulp and Paper, etc.)

6.3 By Geography***

6.3.1 North America

6.3.1.1 United States

6.3.1.2 Canada

6.3.2 Europe

6.3.2.1 United Kingdom

6.3.2.2 Germany

6.3.2.3 France

6.3.2.4 Italy

6.3.3 Asia

6.3.3.1 China

6.3.3.2 Japan

6.3.3.3 India

6.3.3.4 South Korea

6.3.4 Australia and New Zealand

6.3.5 Latin America

6.3.6 Middle East and Africa

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles*

7.1.1 Emerson Electric Co.

7.1.2 Flowserve Corporation

7.1.3 Baker Hughes Company

7.1.4 Metso Corporation

7.1.5 CIRCOR International Inc.

7.1.6 IMI PLC

7.1.7 Christian Burkert GmbH & Co. KG

7.1.8 GEA Group Aktiengesellschaft

7.1.9 Neway Valve (Suzhou) Co. Ltd

8. INVESTMENT ANALYSIS

9. FUTURE TRENDS

Control Valve Industry Overview

The control valve manipulates moving fluid, such as water, steam, gas, or chemical compounds, to compensate for the load disturbance and keeps the regulated process variable as close as possible to the desired set point. Control valves are the most important part of any process control loop, as they are critical to the overall performance of the process, especially when reliability and productivity are the primary goals.

The control valve market is segmented by type (globe, ball, butterfly, plug, diaphragm, and other types of valves), end-user industry (oil and gas, chemical, petrochemical and fertilizer, energy and power, water and wastewater treatment, metal and mining, food and beverage, pharmaceutical, pulp and paper, and other end-user industries), and geography (North America [United States and Canada], Europe [United Kingdom, Germany, France, Italy, and Rest of Europe], Asia-Pacific [China, Japan, India, South Korea, and Rest of Asia-Pacific], and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Type | |

| Globe | |

| Ball | |

| Butterfly | |

| Plug | |

| Diaphragm | |

| Other Types of Valves |

| By End-user Industry | |

| Oil and Gas | |

| Chemical, Petrochemical, and Fertilizer | |

| Energy and Power | |

| Water and Wastewater Treatment | |

| Metal and Mining | |

| Other End-user Industries (Food and Beverage, Pharmaceutical, Pulp and Paper, etc.) |

| By Geography*** | ||||||

| ||||||

| ||||||

| ||||||

| Australia and New Zealand | ||||||

| Latin America | ||||||

| Middle East and Africa |

Control Valve Market Research Faqs

How big is the Control Valve Market?

The Control Valve Market size is expected to reach USD 7.43 billion in 2024 and grow at a CAGR of 12% to reach USD 13.08 billion by 2029.

What is the current Control Valve Market size?

In 2024, the Control Valve Market size is expected to reach USD 7.43 billion.

Who are the key players in Control Valve Market?

Emerson Electric Co., Flowserve Corporation, Baker Hughes Company, Metso Corporation and CIRCOR International Inc. are the major companies operating in the Control Valve Market.

Which is the fastest growing region in Control Valve Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Control Valve Market?

In 2024, the North America accounts for the largest market share in Control Valve Market.

What years does this Control Valve Market cover, and what was the market size in 2023?

In 2023, the Control Valve Market size was estimated at USD 6.54 billion. The report covers the Control Valve Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Control Valve Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Control Valve Industry Report

Statistics for the 2024 Control Valves market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Control Valves analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.