Tackifier Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

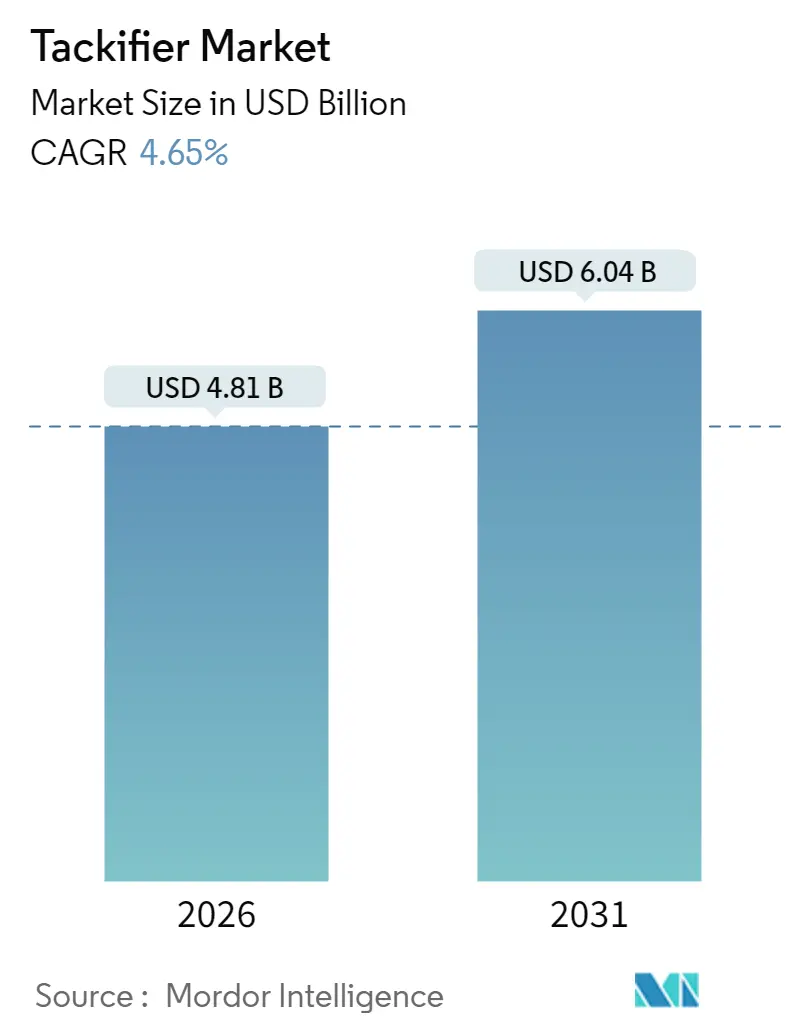

| Market Size (2026) | USD 4.81 Billion |

| Market Size (2031) | USD 6.04 Billion |

| Growth Rate (2026 - 2031) | 4.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

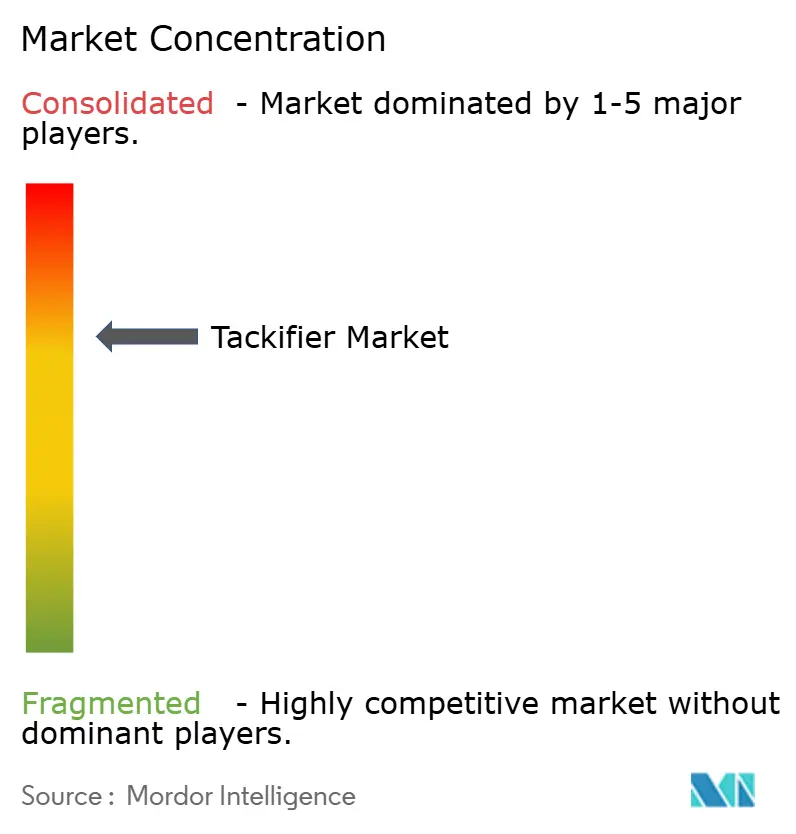

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tackifier Market Analysis by Mordor Intelligence

Tackifier market size in 2026 is estimated at USD 4.81 billion, growing from 2025 value of USD 4.60 billion with 2031 projections showing USD 6.04 billion, growing at 4.65% CAGR over 2026-2031. Rapid infrastructure spending across Asia Pacific, stringent emission norms in North America and Europe, and brand owner commitments to bio-based materials collectively reinforce market momentum. Innovation in ultra-low-VOC grades, high-heat hydrocarbon resins, and rosin-derived dispersions allows suppliers to address tightening food-contact and environmental regulations without sacrificing bond performance. Technology shifts toward tackifier-free reactive hot melts and dynamic polyurethane chemistries, alongside crude-oil price swings, remain overarching risks that could temper profitability yet also spur R&D diversification.

Key Report Takeaways

- By feedstock, petroleum resins held 64.82% of the tackifier market share in 2025, while rosin-based grades record the fastest 4.95% CAGR through 2031.

- By form, solid products captured 80.90% revenue in 2025, and resin dispersions post the highest 5.05% CAGR to 2031.

- By type, synthetic grades accounted for 65.40% of the tackifier market size in 2025; natural grades expand at 5.02% CAGR between 2026-2031.

- By application, tapes and labels led with 58.90% of the tackifier market share in 2025 and grow at a 4.96% CAGR to 2031.

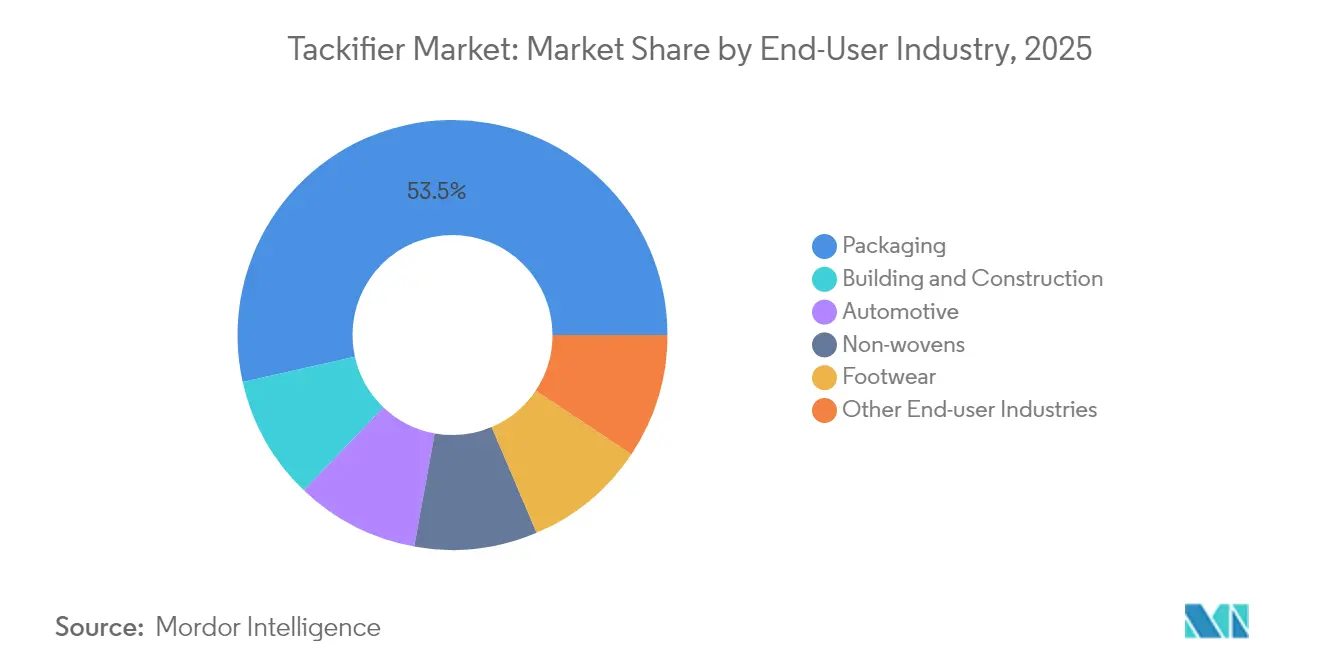

- By end-user industry, packaging commanded 53.50% share of the tackifier market size in 2025 and represents the fastest 5.45% CAGR through 2031.

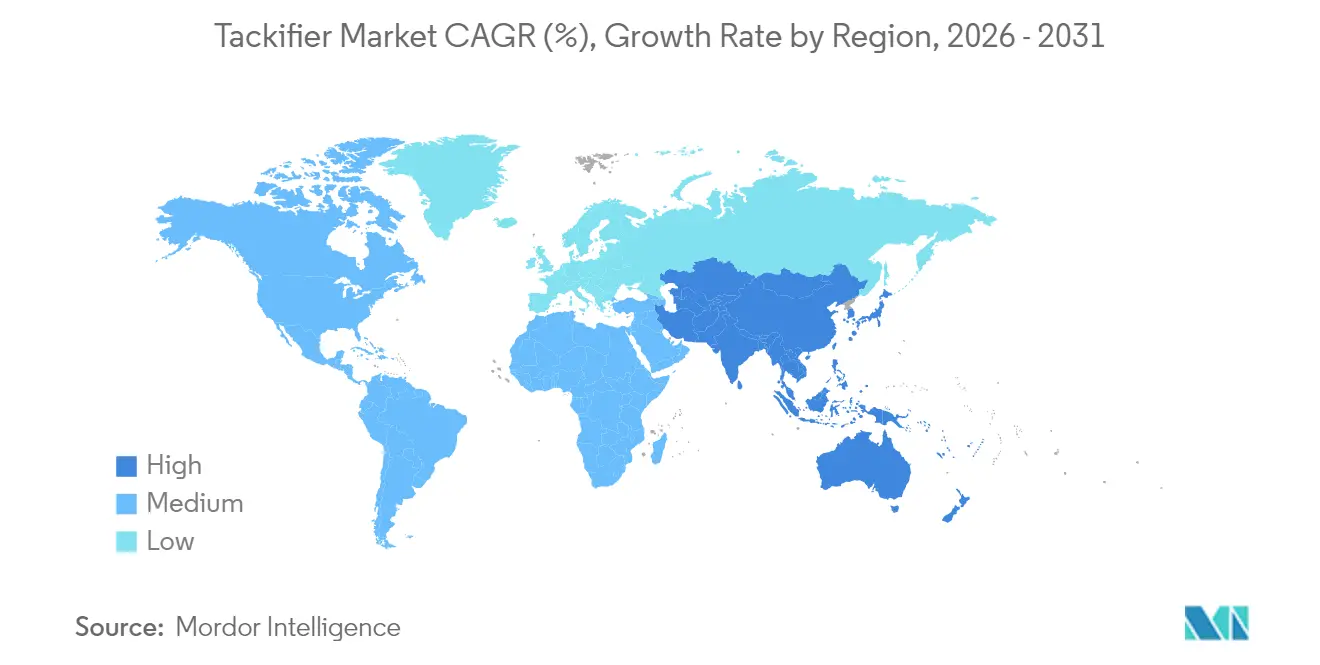

- By region, Asia Pacific contributed 35.95% of 2025 revenue and rises at a 5.25% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tackifier Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for hot-melt & PSA adhesives in packaging and hygiene | +1.20% | Global, with concentration in APAC and North America | Medium term (2-4 years) |

| Urban infrastructure boom in APAC spurring construction adhesives | +0.80% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| E-commerce growth accelerating tape & label consumption | +0.90% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Ultra-low-VOC, food-contact compliant resin grades gain preference | +0.60% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| EV battery & lightweight automotive assembly needing high-heat tackifiers | +0.40% | Global, concentrated in automotive manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Hot-Melt & PSA Adhesives in Packaging and Hygiene

E-commerce parcel volume, combined with premium hygiene products, continues to lift hot-melt and pressure-sensitive adhesive consumption. Tackifier resins provide the critical early-grab and sustained peel strength these fast-running production lines require. H.B. Fuller’s Full-Care 6217 shows how formulation tweaks can cut adhesive usage by 20% while improving peel, a direct cost-and-performance benefit to diaper makers[1]“Full-Care 6217 Technical Bulletin,” H.B. Fuller, hbfuller.com . Biodegradable rosin resins gain traction in paper-backed tapes, aligning with brand sustainability pledges. Moisture-management features in feminine care pads push suppliers toward tackifiers that tolerate high humidity yet keep odor low. ExxonMobil’s Escorez portfolio illustrates the push for light-color, thermally stable grades serving transparent packaging films where clarity is paramount[2]“Escorez Tackifiers Product Guide,” ExxonMobil Product Solutions, exxonmobilchemical.com . These combined needs ensure that the tackifier market remains firmly linked to consumer goods growth through 2030.

Urban Infrastructure Boom in APAC Spurring Construction Adhesives

Mass transit lines, airports, and affordable housing programs across China, India, and ASEAN nations underpin long-run demand for flooring, roofing, and panel bonding adhesives. Moisture-cure systems excel in tropical humidity, and their reliance on tackifier resins for initial wet-out drives incremental volumes. Master Builders Solutions targets INR 500 crore turnover in India by 2028 on the strength of such products. Building codes pushing lightweight composite façades and sandwich panels widen the performance window for synthetic hydrocarbon tackifiers that deliver thermal stability. The China Adhesive Tape Council reports volume gains in building tapes, highlighting how infrastructure and consumer durables intersect. These investments sustain APAC’s leadership in tackifier market growth.

E-commerce Growth Accelerating Tape & Label Consumption

Parcel shipments surged again in 2025, escalating the need for reliable carton sealing tapes and shipping labels. Paper-based tapes witness the highest adoption as retailers seek curbside recyclability, boosting demand for resin systems that bond to kraft and recycled liners instantly. Asia Pacific leads in sustainable tape uptake due to both industrialization and fresh environmental directives that limit plastic waste. Tackifiers must balance high tack, cold-resistance for cross-border transport, and compatibility with reclaim streams, challenging formulators to fine-tune molecular weight and softening point. H.B. Fuller’s 2025 packaging trend review underlines portion-controlled flexible pouches, a format heavily dependent on robust label adhesion over variable substrates. These factors ensure tape and label applications remain the backbone of tackifier consumption.

Ultra-Low-VOC, Food-Contact Compliant Resin Grades Gain Preference

Regulatory scrutiny on migratory substances in food packaging drives sharp growth in ultra-low-VOC tackifiers. U.S. FDA 21 CFR 175.125 delineates stringent compositional limits for pressure-sensitive adhesives in direct and incidental food contact. The U.S. EPA consumer product rule caps VOCs in adhesive categories, pushing resin producers toward high-purity, low-odor grades. South Coast AQMD’s Rule 1168 “Super Compliant” roster lists products below 25 g/L VOC, becoming a de facto benchmark for national retailers. Natural rosin and terpene tackifiers, inherently lower in VOCs, secure preference but must match synthetic alternatives for color and oxidation stability. H.B. Fuller’s migration-safe PSA range exemplifies industrial alignment with food-contact mandates.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petroleum-feedstock price volatility hurting hydrocarbon resin margins | -0.70% | Global, with acute impact in regions dependent on imports | Short term (≤ 2 years) |

| Emergence of tackifier-free reactive hot-melt systems | -0.50% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Sustainability certifications constraining tall-oil & gum-rosin supply | -0.30% | Global, with concentration in forestry-dependent regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Petroleum-Feedstock Price Volatility Hurting Hydrocarbon Resin Margins

Hydrocarbon tackifier lines mirror crude-oil price swings because C5 and C9 streams are co-products of naphtha crackers. Spikes erode margins, stall expansion CAPEX, and constrain R&D budgets. During the 2021 European logistics crunch, adhesive demand slipped 5%, underscoring vulnerability to supply disruptions. Specialty chemical planners now emphasize hedging and agile pricing tools, yet smaller independent resin houses remain exposed. With petroleum resins occupying 65.45% share, extended volatility could redirect buyers toward bio-based grades, reshaping the competitive landscape.

Emergence of Tackifier-Free Reactive Hot-Melt Systems

Reactive PUR and dynamic polyurethane hot melts bond without external tackification, leveraging post-application crosslinking for strength. Buehnen highlights customers shifting from traditional hot melts toward these one-component reactive lines. EU REACH limits on >0.1% diisocyanates catalyze R&D into isocyanate-free epoxies and acrylics, circumventing historical tackifier use. Academic work on dynamic polyurethane hot melts delivering tenfold adhesion gains over commercial benchmarks demonstrates the disruptive potential. Penetration remains nascent but threatens traditional tackifier volumes in high-performance segments.

Segment Analysis

By Feedstock: Petroleum Dominance Faces Bio-Based Challenge

Petroleum resins delivered 64.82% of 2025 revenue, anchoring the tackifier market with a reliable quality and price-performance balance. C5-C9 hybrids secure tack and heat resistance for automotive interiors and industrial tapes. Meanwhile, rosin grades expand at a 4.95% CAGR as converters pursue renewable content for eco-labels and certified compostable pouches. Tall-oil rosin supply tightens because biofuel refiners draw from the same feed pool, leading to a projected 8% deficit by 2030. Successful suppliers diversify between hydrocarbon and rosin lines, hedging price swings while meeting brand sustainability targets. Terpene resins, though niche, add polarity advantages that improve adhesion to natural rubber and elastic substrates. The tackifier market benefits from this blended feedstock approach, ensuring formulators can balance cost, performance, and green content.

Petroleum producers aim to lock in long-term contracts to preserve stability, but such commitments reduce flexibility when customers pivot to bio-content mandates. Conversely, rosin innovators exploit hydrogenated modifications to match color and odor standards demanded in transparent packaging films. The interplay between cost volatility and sustainability legislation defines feedstock strategy for the decade ahead.

Note: Segment shares of all individual segments available upon report purchase

By Form: Solid Tackifiers Maintain Processing Advantages

Solid chips and pellets held 80.90% of 2025 sales because converters prefer easy feeding, low dust, and compatibility with established hot-melt equipment. They withstand melting peaks above 150 °C without oxidative degradation, making them indispensable for carton-sealing and woodworking lines. Resin dispersions outpace with 5.05% CAGR, meeting waterborne adhesive growth in labels and flexible laminations. These dispersions reduce VOC output and simplify line cleanup, critical under tighter plant-emission audits. Liquid forms serve ribbon-coating and solvent systems where room-temperature viscosity is needed, yet their market share lags amid solvent abatement costs. For manufacturers, offering multi-form portfolios elevates switching barriers and secures share in specialty end uses that demand customized viscosity profiles.

By Type: Synthetic Leadership Challenged by Natural Growth

Synthetic grades aggregated 65.40% share in 2025, reflecting decades of process optimization that yields pale color and thermal stability. Hydrogenated C9 resins remain staples for clear hygiene films and automotive interiors requiring UV resistance. Natural tackifiers, led by gum rosin and terpene phenolics, grow fastest at 5.02% CAGR. Pinova’s pine-stump chemistry illustrates how circular forestry streams feed adhesive markets. Research showing rosin-based reactive hot melts tripling tensile strength versus petroleum references further validates natural potential. Still, variability in acid value and color index demands tighter QC, constraining uptake in critical optical applications. Hybrid blends permit formulators to raise bio-content while retaining synthetic performance, a practical bridge until natural purification scales.

By Application: Tapes & Labels Drive Market Growth

Tapes and labels comprised 58.90% of 2025 revenue and expand at 4.96% CAGR to 2031, a trajectory tied to omnichannel retail packaging and automated case-sealing lines. These applications rely on instant tack for high-speed lanes and shear stability for stacked pallets, cementing tackifier indispensability. Assembly adhesives for electronics and appliances form the second pillar, where resins enhance early bond strength for in-line testing. Bookbinding, footwear, and rubber remain steady, though technology migrations to digital reading and modern sewing may cap volumes. Medical drapes and transdermal patches add niche demand for medical-grade rosin esters cleared for skin contact. The tackifier market therefore benefits from both high-volume commodity tapes and high-margin specialty medical segments, diversifying revenue streams.

By End-User Industry: Packaging Leads Multi-Industry Demand

Packaging supplied 53.50% of 2025 demand and climbs at 5.45% CAGR through 2031, spurred by flexible pouch adoption and shift-to-paper initiatives that demand new adhesive architectures. Building and construction follow, benefiting from composite façade panels, LVT flooring, and insulation bonding that substitute mechanical fasteners. Automotive trends toward lightweight multi-material joints and battery cell fixation require tackifiers stable above 150 °C. Non-woven hygiene lines count on consistent resin tack at high speed, while footwear leverages resins for upper-sole bonding that endures flex cycles. Electronics assembly adopts high-purity terpene phenolics to mitigate ionic contamination risk. These diversified outlets allow the tackifier market to cushion downturns in any single sector.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia Pacific commanded 35.95% of 2025 revenue and rises at 5.25% CAGR, underpinned by infrastructure investment, surging e-commerce, and expanding diaper penetration. China’s adhesive tape production grew at high single digits, aligned with construction and electronics verticals that specify differentiated tackifiers. India’s construction chemicals market, sized at INR 20,000 crore in 2025, underscores regional appetite for adhesives that accelerate build cycles. Government policies favoring biodegradable packaging boost rosin-based demand, while volatile tall-oil supply challenges local formulators to secure consistent feedstock.

North America retains innovation leadership through tight VOC caps and FDA food-contact rules steering purchases toward ultra-low-odor grades. Automotive electrification in the United States and Mexico triggers demand for high-heat synthetic resins that secure battery cell stacks. Europe emphasizes circular economy targets and REACH compliance, prompting a pivot to bio-content tackifiers despite higher costs. The 2025 rebound in European construction adhesives signals that regulatory headwinds can coexist with sustainable substitution opportunities.

South America and Middle East & Africa, though smaller, offer upside tied to logistics corridors, consumer goods growth, and foreign direct investment in manufacturing. Saint-Gobain’s USD 1.025 billion purchase of FOSROC bolsters distribution of construction adhesives in GCC states and India, an example of global firms placing strategic bets on emerging demand centers. Exchange-rate swings and limited local resin capacity temper immediate growth, but gradual industrialization sets a foundation for tackifier uptake over the next decade.

Competitive Landscape

The tackifier market is moderately consolidated, with top players cultivating broad feedstock coverage and regional production bases to buffer logistics risks. Eastman Chemical, Kraton Corporation, and ExxonMobil Chemical integrate hydrocarbon cracking, hydrogenation, and downstream compounding, granting cost leverage and supply assurance. Eastman’s CASPI division ranks second worldwide in adhesive raw materials, reflecting scale advantages in both C5 and rosin families. Kraton’s 2023 acquisition of Michelman’s tackifier assets extends it into water-borne dispersions, widening exposure to paper labels and flexible laminations[3]“Kraton Announces Michelman Tackifier Acquisition,” Kraton Corporation, kraton.com .

Strategic focus rests on differentiated chemistries: hydrogenated hydrocarbon resins for optical clarity, terpene phenolics for medical devices, and bio-esterified rosins for compostable packaging. Suppliers pair these with cradle-to-gate carbon data and regulatory dossiers to aid customer compliance. Digital formulation portals and rapid-prototyping labs strengthen technical partnerships, creating switching friction. Volatile feedstock economics motivate vertical integration or offtake pacts with cracker operators and tall-oil distillers. M&A activity centers on bolt-on technologies or geographic footprints, such as Saint-Gobain’s emerging-market push via FOSROC. Simultaneously, startups developing reactive hot-melts lure venture capital, posing future substitution threats. For now, incumbents leverage scale and brand trust to hold share, yet must invest in sustainable options to pre-empt disruptive entrants.

Tackifier Industry Leaders

Kraton Corporation

Ingevity Corporation

Eastman Chemical Company

Exxon Mobil Corporation

Arkema

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2023: Lawter has launched Snowtack HS80, a high-performance water-borne resin tackifier dispersion with 66% high solids content, designed for labeling and taping applications in water-based pressure-sensitive adhesives.

- June 2023: Kraton has strengthened its portfolio by acquiring Michelman's tackifier business, enabling access to new chemistries and customer segments. This acquisition is expected to enhance competition and innovation in the tackifier market.

Global Tackifier Market Report Scope

Tackifiers are chemical compounds that are used in manufacturing adhesives to increase tack, the stickiness of the surface of the adhesive. They are low-molecular-weight compounds that have high glass transition temperatures. They find applications in several end-users such as building and construction, automotive, etc.

The tackifiers market is segmented by feedstock, form, type, application, end-user industry, and geography. By feedstock, the market is segmented into rosin resins, petroleum resins, and terpenes resins. By form, the market is segmented into solid, liquid, and resin dispersion. By type, the market is segmented into synthetic and natural. By application, the market is segmented into tapes and labels, assembly, bookbinding, footwear, leather and rubber articles, and other applications (profile wrapping, etc.). By end-user industry, the market is segmented into automotive, building and construction, non-wovens, packaging, footwear, and other end-user industries (pulp and paper, etc.). The report also covers the market size and forecasts for the market in 15 countries across the globe.

For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Rosin Resins |

| Petroleum Resins |

| Terpene Resins |

| Solid |

| Liquid |

| Resin Dispersion |

| Synthetic |

| Natural |

| Tapes and Labels |

| Assembly |

| Bookbinding |

| Footwear, Leather and Rubber |

| Other Applications |

| Packaging |

| Building and Construction |

| Automotive |

| Non-wovens |

| Footwear |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| Feedstock | Rosin Resins | |

| Petroleum Resins | ||

| Terpene Resins | ||

| Form | Solid | |

| Liquid | ||

| Resin Dispersion | ||

| Type | Synthetic | |

| Natural | ||

| Application | Tapes and Labels | |

| Assembly | ||

| Bookbinding | ||

| Footwear, Leather and Rubber | ||

| Other Applications | ||

| End-user Industry | Packaging | |

| Building and Construction | ||

| Automotive | ||

| Non-wovens | ||

| Footwear | ||

| Other End-user Industries | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the tackifier market by 2031?

The tackifier market is forecast to reach USD 6.04 billion in 2031, expanding at a 4.65% CAGR from 2026 levels.

Which segment holds the largest tackifier market share today?

Tapes and labels lead with 58.90% of 2025 revenue, supported by e-commerce packaging and automated labeling lines.

Why are rosin-based tackifiers growing faster than petroleum resins?

Rosin grades align with brand sustainability goals and offer lower VOCs, driving a 4.95% CAGR despite some supply constraints.

Which region will contribute most to future tackifier demand?

Asia Pacific, already at 35.95% share, advances at 5.25% CAGR thanks to infrastructure projects and rising consumer goods output.

How are suppliers addressing VOC regulations in food packaging?

Producers launch ultra-low-VOC and migration-safe tackifiers that meet FDA 21 CFR 175.125 and EPA consumer product limits while preserving bonding performance.