Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

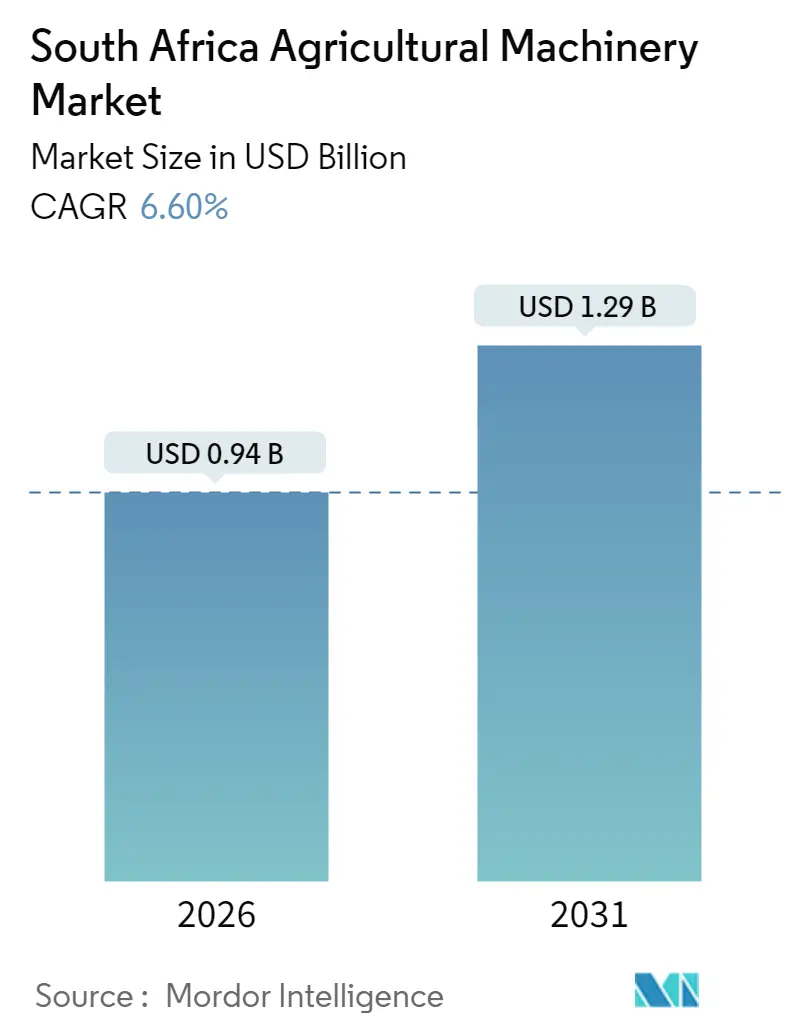

| Market Size (2026) | USD 0.94 Billion |

| Market Size (2031) | USD 1.29 Billion |

| Growth Rate (2026 - 2031) | 6.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Agricultural Machinery Market Analysis by Mordor Intelligence

South Africa agricultural machinery market size in 2026 is estimated at USD 0.94 billion, growing from 2025 value of USD 0.88 billion with 2031 projections showing USD 1.29 billion, growing at 6.6% CAGR over 2026-2031. This resilience reflects the sector’s rapid shift toward mechanization, an evolution that has helped farmers offset labor shortages, comply with tightening water-use regulations, and sustain yields despite frequent power disruptions. Record tractor sales in 2022 set new adoption benchmarks, while drought‐induced water quotas have triggered accelerated investment in drip and pivot systems that maximize every liter pumped. Government blended-finance schemes are lowering entry barriers for emerging growers, and original-equipment manufacturers (OEMs) have layered on low-rate financing and embedded telematics to reinforce lifetime value [1]Source: Industrial Development Corporation, “Agri-Industrial Fund Factsheet,” idc.co.za. At the same time, a widening preference for high-horsepower platforms and four-wheel or track drive configurations signals a maturing customer base that prioritizes field efficiency and precision capability over initial purchase price. These intertwined drivers position the South Africa agricultural machinery market for solid mid-single-digit expansion through 2030.

Key Report Takeaways

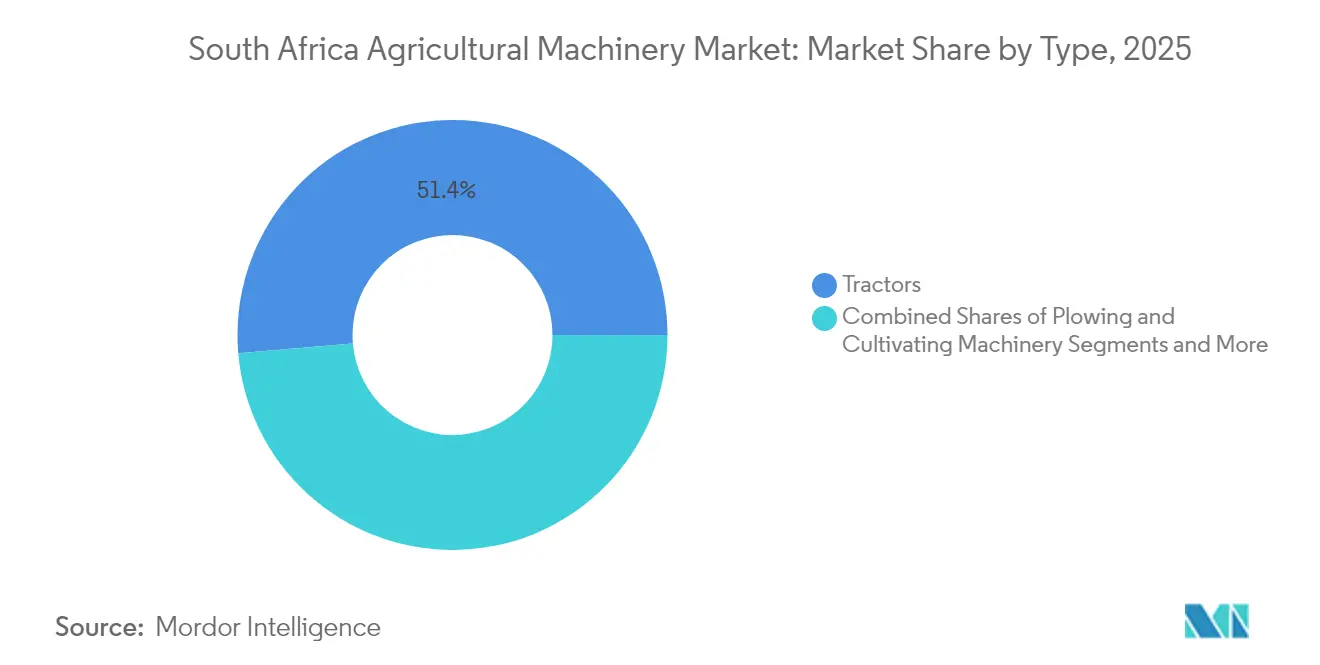

- By type, tractors held 51.35% of the South Africa agricultural machinery market share in 2025, while irrigation machinery is projected to expand at an 10.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Agricultural Machinery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Deepening mechanization demand post-pandemic | +1.6 % | National, with spillover to the Southern Africa Development Community | Medium term (2 – 4 years) |

| Water-scarcity push toward precision irrigation | +1.4 % | Western and Northern Cape provinces | Long term (≥ 4 years) |

| Government recap grants for emerging farmers | +1.1 % | Rural provinces nationwide | Medium term (2 – 4 years) |

| Rapid rise of telematics-enabled tractors | +0.8 % | Grain belts and broadacre zones | Short term (≤ 2 years) |

| OEM (Original Equipment Manufacturer) financing arms lowering entry barriers | +0.7 % | Urban-adjacent farming areas | Short term (≤ 2 years) |

| Sub-meter GPS retrofit kits for legacy fleets | +0.4 % | Commercial farming districts | Medium term (2 – 4 years) |

| Source: Mordor Intelligence | |||

Deepening Mechanization Demand Post-Pandemic

Record tractor arrivals in 2022 set new baselines for mechanization, expanding the active fleet by double digits and convincing growers at every scale that output hinges on horsepower. Emerging farmers in the Eastern Cape pushed mechanization penetration to 90%, uplifting yields and labor productivity in cereal and vegetable schemes. Import manifests skewed heavily toward 75–95 HP platforms that pair versatility with modest diesel burn, explaining the category’s enduring dominance. Seasonal cash-flow financing and duty rebates fostered adoption, showing that once credit barriers fall, mechanization climbs rapidly. As these tractors age, parts and service demand will ripple through dealers, cementing lifetime revenue streams across the South Africa agricultural machinery market.

Water-Scarcity Push Toward Precision Irrigation

Increasing drought intensity and statutory water quotas nowadays force producers to replace flood irrigation with pivots and drip sets that lift application efficiency by up to 40%. Solar-powered pump stations irrigate 364 hectares across the Western and Eastern Cape, freeing farmers from Eskom disruptions while cutting grid bills. Viticulture and citrus estates, where water rights carry boardroom-level weight, justify the capital expenditure (capex) with stronger export grades and reduced rejection rates. Government irrigation revitalization grants and the Agriculture and Agro-processing Master Plan funnel technical aid and working capital into these projects, accelerating unit shipments. OEMs (Original Equipment Manufacturers) integrate pump telemetry into dashboards, allowing growers to throttle flow by block and align with plant water-stress indices, a leap forward for the South Africa agricultural machinery market.

Government Recap Grants for Emerging Farmers

The R5 billion (USD 340 million) Agri-Industrial Fund pairs 60% concessional debt with 40% grants, underwriting sprayers, small tractors, and harvesters for new Black commercial farmers. Additional Land Redistribution grants of R20,000 to R100,000 (USD 1,360 to 6,800) kick-start entry-level purchases, while collateral-free Micro-Agricultural Financial Institutions loans cap at R100,000. These financial stacks eliminate down-payment barriers and boost dealer throughput in rural nodes. Early analysis shows 23% lower default than legacy credit programs, validating the blended model. In 2024, the South Africa government introduced an asset assistance program offering up to R250,000 (USD 17,000) for machinery acquisition, supported by nationwide roadshows [2]Source: Department of Agriculture, Land Reform and Rural Development, “Comprehensive Agricultural Support Programme: Mechanisation Support,” dalrrd.gov.za. Over time, such finance is likely to migrate beneficiaries into larger horsepower brackets, deepening the South Africa agricultural machinery market pipeline.

Rapid Rise of Telematics-Enabled Tractors

OEM (Original Equipment Manufacturers) embedded SIM modules such as JD Link stream real-time performance data to cloud dashboards, cutting unscheduled downtime by 14% on average. Fleet visibility allows farm managers to redeploy assets dynamically, saving fuel and labor over time. Case IH’s AFS Connect integrates agronomic maps with variable-rate controllers, improving seed placement accuracy from 30 centimeters to 2.5 centimeters. Because South Africa faces a shortage of diagnostic technicians, remote-support features that push fault codes directly to dealer workshops have become critical to limiting out-of-service hours. Telematics subscriptions also help lenders monitor asset utilization, reducing credit risk and enabling more competitive interest rates, which in turn fuels fresh purchases.

Restraints Impact Analysis

| Restraint | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-power instability inflating operating costs | –1.3 % | Rural provinces nationwide | Short term (≤ 2 years) |

| Rising interest rates curbing cap-ex cycles | –1.0 % | Commercial grain and horticulture hubs | Medium term (2 – 4 years) |

| Grey-market imports undermining dealer margins | –0.7 % | Peri-urban produce belts | Medium term (2 – 4 years) |

| Persistent skills gap for high-tech equipment | –0.5 % | Remote agricultural zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid-Power Instability Inflating Operating Costs

Stage-6 load-shedding drives annual producer costs of R3.95–4.08 billion (USD 268–277 million) as farmers scramble for diesel generators and backup pumps. Nearly all irrigation pivots and pack-house cold rooms rely on Eskom electricity; therefore, outages disrupt quality-critical processes. Many vegetable growers nowadays factor diesel at ZAR 3.50 per kilowatt-hour when budgeting, triple the grid tariff, directly squeezing margins. Retailers reject produce that fails cold-chain protocols, compounding losses. As solar micro-grid payback remains five-plus years for most operations, equipment outlays compete with energy investments, delaying upgrades other than essential replacements.

Rising Interest Rates Curbing Cap-Ex Cycles

Since 2023, the South Africa Reserve Bank has lifted the repo rate by 275 basis points, pushing prime borrowing costs above 12%. Each percentage-point increase raises annual tractor repayment on a R1 million (USD 68,000) note by roughly R7,500 (USD 510), lengthening payback periods beyond five seasons for many row-crop operations. Cash-flow pressures are causing farmers to extend service-life targets and defer combine and sprayer upgrades. While OEMs subsidize rates, they cannot fully neutralize policy tightening, leading to a 9% decline in new tractor financing approvals during 2024. The restraint is most acute for growers exposed to export commodity price swings and currency volatility.

Segment Analysis

By Type: Tractors Drive Market Foundation

Tractors generated 51.35% of 2025 revenue, underpinning the South Africa agricultural machinery market size for basic tillage, planting, and haulage duties. Their versatility keeps them relevant across commercial cereals, horticulture, and mixed livestock systems. Meanwhile, irrigation machinery, although only 7.18% of 2025 turnover, is the fastest-expanding slice at an 10.3% CAGR thanks to drought resilience mandates. OEMs respond by bundling drip lines, filters, and solar pumps into tractor-financing packages, tightening cross-sell synergies. Farmers shifting to precision sprayers and planters also lift demand for power-take-off implements, which ride on tractor sales momentum.

Innovation centers on integrating ISOBUS controllers that allow seamless plug-and-play between tractor hitches and smart implements. Dealers have reported a 35% uptick in inquiries for variable-rate planters that can read prescription maps generated by drones or satellite imagery. Haying and forage machinery maintains a niche role serving the feed requirements of KwaZulu-Natal’s dairy clusters, while harvesting combines enjoy cyclical spikes aligned with maize price rallies. The equipment mix reinforces tractors as the anchor asset around which most fleets are built, underscoring why any change in tractor sentiment ripples through the broader South Africa agricultural machinery market share.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

South Africa’s Western Cape spearheads precision irrigation adoption because perennial water scarcity and premium vineyards justify high-capex systems that conserve every cubic meter. The province collaborates with Case IH under a five-year research pact, supplying experimental farms with sensor-laden tractors to field-test conservation tillage and crop-stress analytics. Combined fruit exports ensure adequate foreign exchange earnings to service machinery loans, making the Western Cape a bellwether for smart-equipment penetration.

The Eastern Cape showcases what coordinated extension and grant programs can do for smallholder productivity. Mechanization adoption has touched 90% in pilot districts, narrowing the yield gap with commercial growers and stimulating local demand for mid-horsepower tractors. Load-shedding nevertheless remains acute in rural circuits, pushing the adoption of solar-powered pumps and encouraging equipment with lower fuel burn. The Free State, as the maize capital, drives high-horsepower tractor and combine sales. A projected 11% rebound in summer-grain output for 2025 is likely to keep dealerships busy staging pre-season service clinics.

KwaZulu-Natal’s diversified base of sugarcane, beef, and dairy farms shapes demand for specialized implements such as cane loaders and forage harvesters. Coastal humidity and saline soils challenge machine longevity, prompting OEMs to tailor corrosion-resistant packages. Government master-plan funding for rural roads enhances access to dealer workshops, mitigating downtime. Northern provinces such as Limpopo remain under-mechanized but possess latent potential once irrigation infrastructure expands. Overall, geography-specific crop mixes, climate stresses, and energy reliability issues combine to create a mosaic of opportunities that collectively reinforce the South Africa agricultural machinery market.

Competitive Landscape

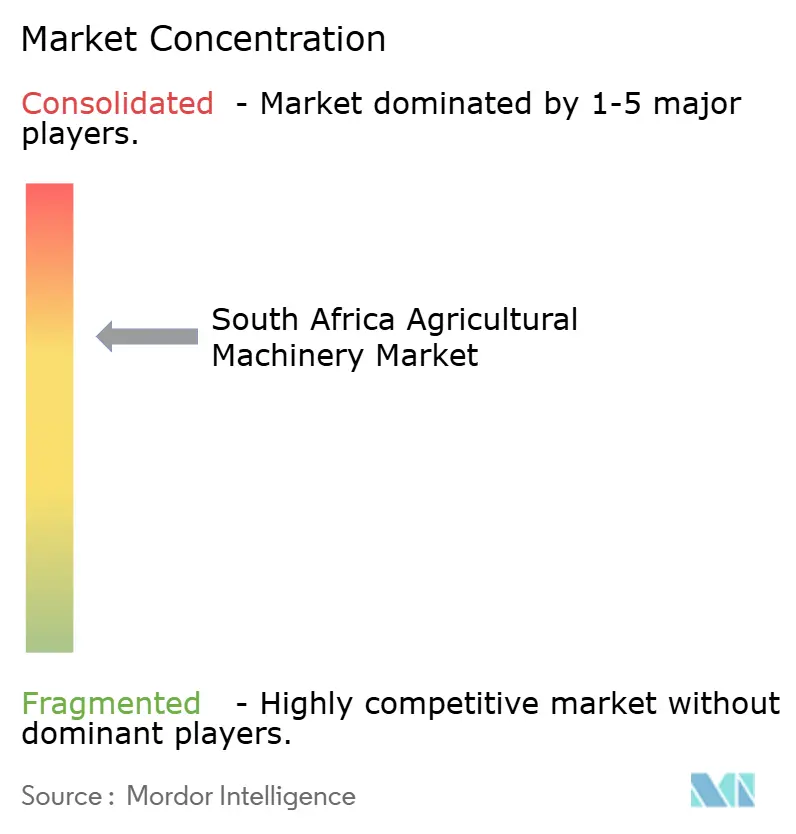

The South Africa agricultural machinery market demonstrates moderate concentration, with players including Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, and Mahindra & Mahindra Ltd. Kubota appeals to horticulture with compact high-power-to-weight tractors, reaching 9.2% share. OEMs (Original Equipment Manufacturers) increasingly package hardware with agronomic software, financing, and warranty extensions, turning equipment sales into long-term service relationships. Precision irrigation suppliers such as Valley and Netafim target white-space niches, partnering with tractor dealers to leverage existing customer pipelines.

Strategic moves include John Deere’s 22% jump in precision agriculture revenue in 2024, which was plowed into autonomous and electric prototypes [3]Source: Deere and Company, “Form 10-K 2023,” deere.com. Load-shedding risks have prompted all majors to introduce generator-compatible control units and solar-friendly irrigation lines. Competitive rivalry now centers on energy efficiency, total-cost-of-ownership analytics, and embedded service ecosystems rather than headline horsepower.

White-space opportunities exist in precision irrigation systems, retrofit technology solutions, and energy-efficient equipment designed for load-shedding resilience. The Competition Tribunal's approval of equipment sector consolidation, such as the AFGRI Equipment and Agrico merger, indicates regulatory acceptance of market concentration trends that enhance operational efficiency without compromising competition.

South Africa Agricultural Machinery Industry Leaders

Deere & Company

CNH Industrial N.V.

AGCO Corporation

Kubota Corporation

Mahindra & Mahindra Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2024: Western Cape Department of Agriculture signed a five-year agreement with Case IH to supply advanced agriculture equipment for public research farms.

- August 2023: Mahindra Tractors launched the Mahindra OJA tractor range at the Futurescape event in Cape Town, introducing seven lightweight tractor models equipped with standard 4WD. These tractors, ranging from 20HP to 40HP (14.91kW to 29.82kW), offer platform versatility to effectively manage various agricultural tasks.

- July 2023: John Deere acquired Smart Apply Inc., a precision spraying equipment company that developed the Smart Apply Intelligent Spray Control System (an upgrade kit that can improve the precision and performance of virtually any air-blast sprayer used in orchard, vineyard, and tree nursery spraying applications). Smart Apply is primarily sold through John Deere dealers in South Africa.

- November 2022: Kubota established a supply chain to sell low-cost tractors produced in India, leveraging India’s lower material and labor costs. Instead of exporting from Japan, Kubota will have an Indian subsidiary ship compact models to the small-scale farms that dominate Africa's agricultural sector, including South Africa.

South Africa Agricultural Machinery Market Report Scope

Agriculture machinery and equipment are the farm equipment, machines, and farmer tools that increase agricultural crop productivity and food output. It accomplishes regular agriculture tasks that help boost food crop production and alleviate poverty.

The South African agricultural machinery market is segmented by type (tractors (engine power (less than 40 HP, 40 HP-99 HP, and greater than 100 HP) and type (compact utility tractors, utility tractors, and row crop tractors)), plowing and cultivating machinery (plows, harrows, cultivators and tillers, and other plowing and cultivating machinery), harvesting machinery (combine, forage, and other harvesting machinery), haying and forage machinery (mowers and conditioners, balers, and other haying and forage machinery), and irrigation machinery (sprinkler, drip, and other irrigation machinery)). The report offers market size and forecasts for the market in value (USD) for all the above segments.

By Type

| Tractors | Engine Power | Less than 40 HP |

| 40 HP to 99 HP | ||

| Greater than 100 HP | ||

| Type | Compact Utility Tractors | |

| Utility Tractors | ||

| Row Crop Tractors | ||

| Plowing and Cultivating Machinery | Plows | |

| Harrows | ||

| Cultivators and Tillers | ||

| Other Plowing and Cultivating Machinery | ||

| Planting Machinery | Seed Drills | |

| Planters | ||

| Spreaders | ||

| Other Planting Machinery | ||

| Harvesting Machinery | Combine | |

| Forage | ||

| Other Harvesting Machinery | ||

| Haying and Forage Machinery | Mowers and Conditioners | |

| Balers | ||

| Other Haying and Forage Machinery | ||

| Irrigation Machinery | Sprinkler Irrigation | |

| Drip Irrigation | ||

| Other Irrigation Machinery | ||

| By Type | Tractors | Engine Power | Less than 40 HP |

| 40 HP to 99 HP | |||

| Greater than 100 HP | |||

| Type | Compact Utility Tractors | ||

| Utility Tractors | |||

| Row Crop Tractors | |||

| Plowing and Cultivating Machinery | Plows | ||

| Harrows | |||

| Cultivators and Tillers | |||

| Other Plowing and Cultivating Machinery | |||

| Planting Machinery | Seed Drills | ||

| Planters | |||

| Spreaders | |||

| Other Planting Machinery | |||

| Harvesting Machinery | Combine | ||

| Forage | |||

| Other Harvesting Machinery | |||

| Haying and Forage Machinery | Mowers and Conditioners | ||

| Balers | |||

| Other Haying and Forage Machinery | |||

| Irrigation Machinery | Sprinkler Irrigation | ||

| Drip Irrigation | |||

| Other Irrigation Machinery | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the anticipated value of the South Africa agricultural machinery market in 2031?

The market is projected to reach USD 1.29 billion by 2031.

Which equipment type currently leads sales?

Tractors account for 51.35% of 2025 revenue.

How fast is precision irrigation machinery expanding?

Sales of precision irrigation units are growing at an 10.3% CAGR through 2031.

Why are high-horsepower tractors gaining share?

Larger consolidated farms need 100 HP-plus platforms to cover more hectares efficiently within narrow planting windows.

How does load-shedding influence machinery investment?

Blackouts raise operating costs, pushing farmers toward energy-efficient equipment and solar-integrated irrigation systems.