Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

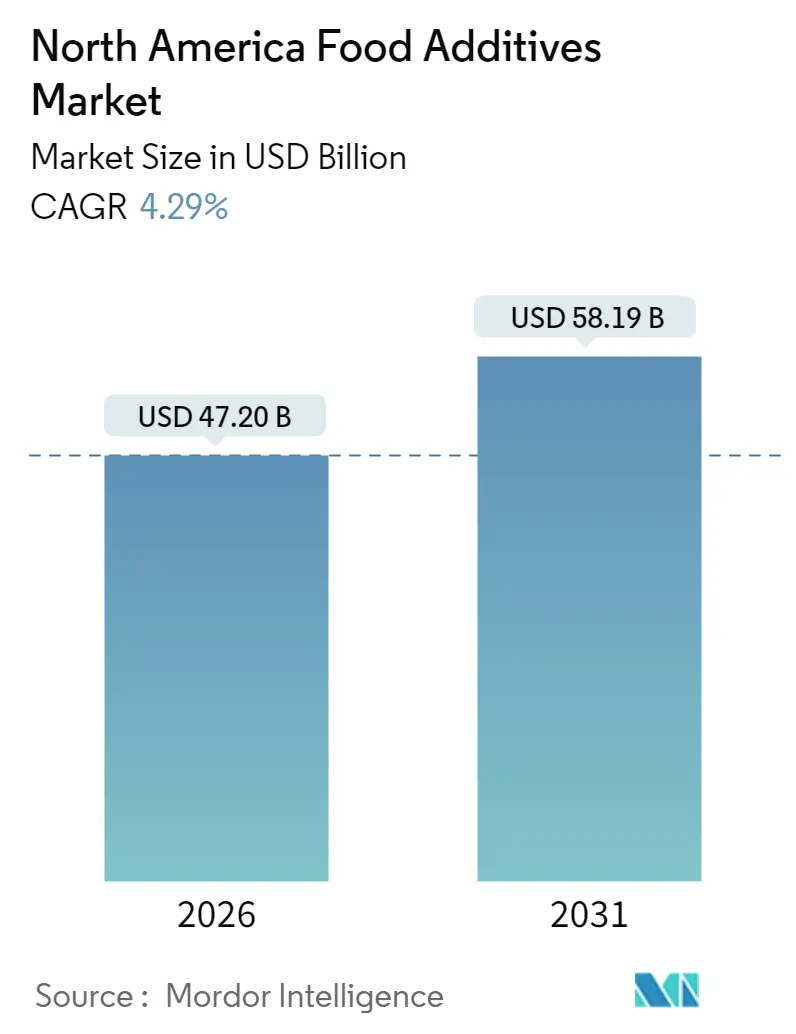

| Market Size (2026) | USD 47.2 Billion |

| Market Size (2031) | USD 58.19 Billion |

| Growth Rate (2026 - 2031) | 4.29% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Food Additives Market Analysis by Mordor Intelligence

North America food additives market size in 2026 is estimated at USD 47.2 billion, growing from 2025 value of USD 45.26 billion with 2031 projections showing USD 58.19 billion, growing at 4.29% CAGR over 2026-2031. Robust demand comes from a mature food processing base that balances regulatory change with consumer wellness goals. Reformulation toward reduced sugar, natural colors, and clean-label preservation keeps functional additives at the center of product innovation. Manufacturers also prioritize texture systems that safeguard quality in omnichannel supply chains. Strategic public funding in Canada and state-level programs in the United States improve plant capacity and stimulate new ingredient solutions. Intensifying regulatory scrutiny favors suppliers with strong compliance capabilities, creating structural barriers that shelter incumbents while still welcoming specialized entrants.

Key Report Takeaways

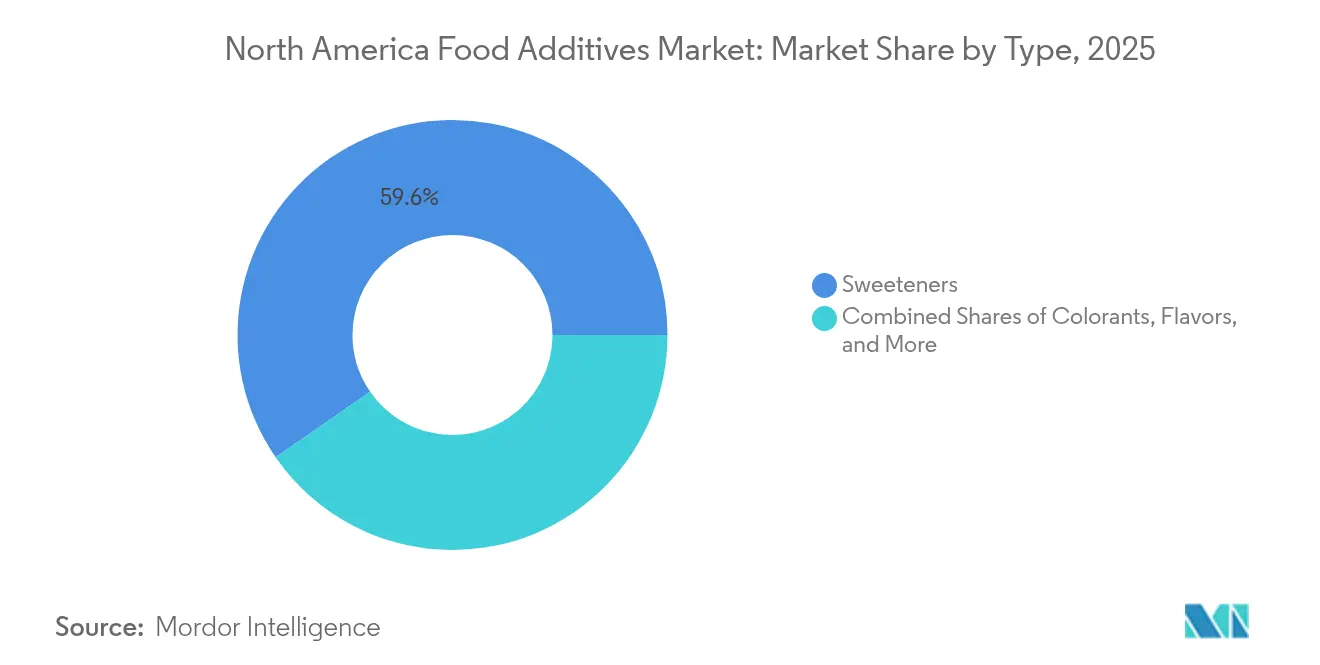

- By product type, sweeteners led with 59.62% revenue share in 2025; colorants are forecast to expand at a 5.42% CAGR through 2031.

- By source, synthetic additives held 55.83% of the North America food additives market share in 2025, while natural alternatives are growing at a 5.78% CAGR through 2031.

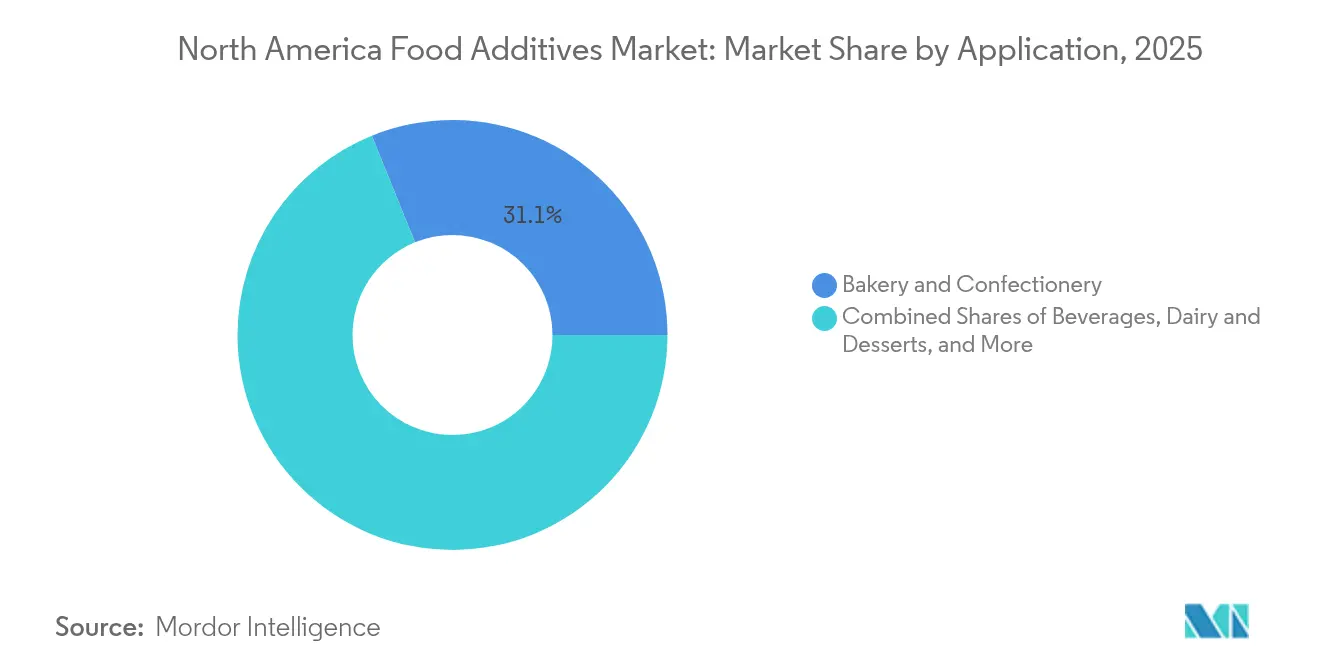

- By application, bakery and confectionery accounted for 31.12% of the North America food additives market size in 2025, and beverages are advancing at a 5.46% CAGR through 2031.

- By geography, the United States captured a 53.21% share in 2025; Canada is projected to post the fastest 5.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Food Additives Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for processed and convenience foods | +1.2% | United States & Canada, with spillover to Mexico | Medium term (2-4 years) |

| Rising demand for natural, clean-label, and organic food additives | +1.8% | North America-wide, strongest in urban centers | Long term (≥ 4 years) |

| Government initiatives supporting food processing industry growth | +0.7% | Canada-focused, with US state-level programs | Short term (≤ 2 years) |

| Technological advancements in additive formulation | +0.9% | Global, with North America as innovation hub | Medium term (2-4 years) |

| Growing popularity of functional foods and fortified products | +1.1% | United States & Canada, premium market segments | Long term (≥ 4 years) |

| Rising export opportunities | +0.6% | Canada-led, leveraging natural ingredient positioning | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Processed and Convenience Foods

With the acceleration of consumer lifestyles, the demand for shelf-stable, ready-to-consume products is on the rise. These products increasingly depend on advanced additive systems to ensure quality and safety. The segment's growth is driven by demographic changes, particularly the increase in dual-income households and urbanization trends. These changes highlight the need for convenience while maintaining nutritional standards. Food manufacturers are addressing this demand by utilizing advanced systems, including preservative systems, texture modifiers, and flavor enhancers. These innovations extend shelf life and preserve sensory appeal, even under varying temperature and storage conditions. USDA [1] U.S. Department of Agriculture, “USDA's Food Price Outlook, 2025,” USDA, usda.govprojections indicate that spending on food away from home will grow by 3.6% in 2025, significantly outpacing the 1.3% growth expected for food at home. This trend highlights a growing institutional demand for processed ingredient solutions. Consequently, there is sustained demand for emulsifiers, stabilizers, and antimicrobial systems, which are essential for maintaining quality across extended supply chains in food service operations. Additionally, as convenience foods shift toward premium positioning, there is an increasing need for additive solutions that replicate restaurant-quality sensory experiences in packaged formats. This demand is driving innovation in flavor delivery systems and texture enhancement technologies.

Rising Demand for Natural, Clean-Label, and Organic Food Additives

Regulatory momentum and growing consumer skepticism toward synthetic additives are driving a shift toward plant-derived and fermentation-based alternatives across all functional categories. For example, the FDA's plan to eliminate petroleum-based synthetic dyes by 2026 has prompted manufacturers to secure natural colorant supplies, which often require 10 to 20 times higher inclusion rates compared to synthetic options. Additionally, state-level restrictions in California, West Virginia, and Illinois have introduced additive bans, compelling manufacturers to reformulate nationwide to avoid market fragmentation. The clean-label trend extends beyond colorants to preservatives, where rosemary extract systems and fermented vinegar solutions are replacing synthetic antioxidants, despite higher costs and increased formulation complexity. Supply chain constraints for natural alternatives have caused pricing volatility, with some botanical extracts experiencing price increases of 40-60% due to demand surpassing cultivation capacity. Companies focusing on vertical integration and sustainable sourcing partnerships are gaining a competitive edge through enhanced supply security and cost stability.

Government Initiatives Supporting Food Processing Industry Growth

By February 2025, Alberta's Agri-Processing Investment Tax Credit has approved USD 1.18 billion in projects spanning 16 corporations, reflecting the Canadian federal and provincial focus on advancing food processing. These efforts aim to enhance processing capabilities by utilizing advanced additive systems to achieve product differentiation and improve export competitiveness. The USD 725.5 million National School Food Program highlights institutional demand for additive solutions that comply with nutritional standards while appealing to child-friendly sensory preferences, as noted by the Federal Economic Development Agency for Southern Ontario[2]Government of Canada, "Healthy Meals for up to 400,000 more kids", www.canada.ca. "Healthy Meals for up to 400,000 more kids," the agency stated in a news release on June 20, 2024. Additionally, Protein Industries Canada has dedicated USD 29.02 million in technology leadership funding to drive innovations in ingredient manufacturing and food processing. This funding creates opportunities for additive companies specializing in plant-protein solutions and co-product valorization technologies. While US state-level programs support federal initiatives, they lack the coordinated impact of Canada's systematic approach. These government investments significantly reduce capital barriers for food processors, expediting the adoption of advanced additive technologies.

Technological Advancements in Additive Formulation

Nanotechnology applications are transforming additive delivery systems by utilizing microencapsulation techniques for targeted release, improved bioavailability, and enhanced stability in complex food matrices. Iron-loaded microcapsules made with whey protein isolate and gum arabic achieve a 17-fold higher retention rate compared to free iron after 21 days, providing 22% of the daily iron requirement for children per serving. Fermentation-derived colorants are emerging as scalable alternatives to extraction-based natural colors. Companies are creating β-carotene and betalain analogs that offer better stability and color intensity while reducing land-use needs. Advanced flavor masking technologies, such as dsm-firmenich's ModulaSense platform, are enabling higher inclusion rates of plant proteins by addressing off-note pathways before receptor interaction, broadening formulation options for protein-fortified products. Progress in enzyme technology is driving co-product valorization, with IFF's FOODPRO® portfolio improving protein extraction yields and reducing energy consumption through optimized processing conditions. These technological innovations provide companies investing in R&D and intellectual property development with opportunities for competitive differentiation.

Restraint Impact Analysis

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent and evolving regulations governing food additive usage and safety | -0.8% | North America-wide, with state-level variations | Short term (≤ 2 years) |

| Consumer skepticism and negative health perceptions regarding synthetic additives | -0.6% | United States & Canada, urban markets primarily | Medium term (2-4 years) |

| Volatility and fluctuation in raw material prices | -0.5% | Global impact with North American supply chains | Short term (≤ 2 years) |

| Supply chain disruptions impacting ingredient availability and pricing | -0.4% | North America-wide, concentrated supplier dependencies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent and Evolving Regulations Governing Food Additive Usage and Safety

Federal agencies are conducting systematic reviews of existing additives, while states are introducing independent restrictions, creating a fragmented market landscape. The FDA's proposal to remove self-affirmed GRAS pathways requires manufacturers to submit formal notifications supported by peer-reviewed safety data. This change could extend product development timelines by 12-18 months and increase regulatory costs by USD 200,000-500,000 per submission. At the same time, Health Canada is updating its food additive regulations. Although some processes are being streamlined, new specification requirements and compliance obligations are being introduced, requiring advanced technical expertise and robust documentation systems. State-level regulatory variations further complicate compliance. For example, California's Food Safety Act, West Virginia's school nutrition restrictions, and Illinois's additive bans necessitate unique formulation strategies for each market. These growing regulatory demands disproportionately affect smaller additive suppliers, who often lack dedicated regulatory affairs teams. Consequently, the market is experiencing consolidation, with companies that have established compliance infrastructures gaining an advantage.

Consumer Skepticism and Negative Health Perceptions Regarding Synthetic Additives

Public health advocacy and social media amplification of additive concerns create sustained pressure for reformulation away from synthetic ingredients, regardless of safety assessments by regulatory authorities. The ultra-processed food debate, elevated to federal policy discussions through HHS and FDA workshops, positions additives as markers of nutritional inferiority rather than functional necessities. Consumer willingness to pay premiums for clean-label alternatives creates market bifurcation, with premium brands investing in natural additive systems while value-oriented products maintain synthetic formulations to control costs. The perception challenge extends beyond individual additives to processing methods, with consumers viewing fermentation-derived ingredients more favorably than chemically synthesized equivalents despite identical molecular structures. Educational initiatives by industry associations struggle against simplified messaging that equates synthetic with harmful, creating sustained headwinds for conventional additive categories. This skepticism drives innovation investment toward natural alternatives but constrains pricing power for synthetic additives, compressing margins across traditional product lines.

Segment Analysis

By Product Type: Sweeteners Lead While Colorants Accelerate

In 2025, sweeteners lead the market with a 59.62% share, highlighting North America's focus on reducing sugar in beverages, baked goods, and confections while maintaining taste quality. This segment's dominance is driven by regulatory mandates, increasing health awareness, and advancements in high-intensity sweeteners that replicate sugar's sensory profile at significantly lower inclusion rates. Meanwhile, colorants are the fastest-growing segment, with a projected 5.42% CAGR through 2031. This growth is attributed to the FDA's gradual elimination of petroleum-based synthetic dyes, which has created a surge in demand for natural alternatives that are more expensive and require higher inclusion rates.

Preservatives continue to see stable demand due to innovations in antimicrobial solutions and the shift toward clean-label formulations. Emulsifiers benefit from the growing popularity of plant-based products, which require advanced stabilization systems. Anti-caking agents maintain steady but modest growth in industrial applications. Enzymes are gaining traction by enhancing value through co-product utilization and processing optimization. Hydrocolloids experience strong demand for their role in texture modification, particularly in reduced-fat and plant-based formulations. Food flavors and enhancers are expanding their market presence, supported by advancements in masking technology that enable greater inclusion of functional ingredients. Lastly, acidulants maintain a stable market position by offering versatile functionality in preservation and flavor enhancement across various applications.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Source: Natural Alternatives Gain Despite Synthetic Dominance

Synthetic additives retain 55.83% market share in 2025 through established supply chains, cost advantages, and proven performance characteristics that meet industrial-scale production requirements. However, natural additives accelerate at a 5.78% CAGR through 2031, driven by regulatory restrictions, consumer preferences, and technological advances that improve natural ingredient functionality and stability. The growth differential reflects structural market transformation as manufacturers invest in natural sourcing partnerships and reformulation capabilities despite higher costs and technical complexity.

Natural additive adoption varies significantly by functional category, with colorants leading the transition due to regulatory mandates, while preservatives and antioxidants follow through clean-label positioning strategies. Supply chain constraints for natural alternatives create pricing volatility and availability challenges, particularly for botanical extracts requiring specific growing conditions and seasonal harvesting. Companies developing fermentation-based natural additives gain competitive advantages through scalable production and consistent quality profiles that bridge the gap between natural positioning and industrial requirements. The synthetic-natural divide will likely persist, with premium brands adopting natural systems while value-oriented products maintain synthetic formulations for cost control.

By Application: Beverages Drive Growth Despite Bakery Leadership

Bakery and confectionery applications dominate with 31.12% market share in 2025, leveraging North America's established snacking culture and the segment's requirement for diverse additive systems including emulsifiers, preservatives, flavors, and texture modifiers. The segment's stability reflects consistent consumption patterns and manufacturers' expertise in balancing functionality with sensory appeal across shelf-stable products. Beverages represent the fastest-growing application at 5.46% CAGR through 2031, driven by functional drink innovation, plant-based alternatives, and sophisticated flavor systems that mask off-notes while delivering health benefits.

Dairy and desserts maintain steady demand through premium positioning and clean-label reformulation, while meat and meat products benefit from natural preservation systems and plant-based analog development. Soups, sauces, and dressings leverage emulsification and flavor enhancement technologies, with growth tied to convenience food trends and restaurant-quality expectations in retail formats. The application shift toward beverages signals manufacturers' focus on higher-margin, health-positioned products that command premium pricing while requiring sophisticated additive solutions for stability, bioavailability, and sensory optimization across diverse pH and storage conditions.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The United States anchors the North American food additives market with a 53.21% share in 2025, leveraging its USD 1.8 trillion food system and sophisticated regulatory framework that enables rapid product innovation and market entry. The market's depth stems from established relationships between additive suppliers and food manufacturers, advanced R&D capabilities concentrated in major metropolitan areas, and distribution networks that efficiently serve diverse regional preferences. FDA's modernization initiatives, including the systematic phase-out of synthetic dyes and GRAS pathway reforms, create both challenges and opportunities for domestic suppliers while potentially raising barriers for international competitors lacking regulatory expertise. The US market's maturity enables premium positioning for innovative additive solutions, with companies like Innophos successfully launching clean-label alternatives such as VersaCal® Bright calcium phosphate as a titanium dioxide replacement.

Canada demonstrates the highest growth trajectory at 5.55% CAGR through 2031, supported by strategic government investments totaling over CAD 3 billion in food processing infrastructure and natural ingredient development programs. The country's positioning as a natural ingredient sourcing hub gains momentum through projects like Louis Dreyfus Company's pea protein isolate facility in Saskatchewan and Jungbunzlauer's xanthan gum manufacturing complex in Ontario, representing combined investments exceeding CAD 400 million. Health Canada's regulatory modernization streamlines additive approval processes while maintaining safety standards, creating competitive advantages for companies establishing Canadian operations. The country's trade relationships and USMCA benefits enable efficient export to US markets while avoiding potential trade tensions affecting other regions.

Mexico and Rest of North America contribute growing shares through manufacturing cost advantages and strategic positioning within USMCA trade frameworks that eliminate tariffs on qualifying food ingredients. Mexico's food processing sector benefits from proximity to US markets while maintaining lower labor costs, creating opportunities for additive manufacturing and processing operations serving regional demand. The USMCA agricultural quotas for Canadian products, including dairy and sugar-containing items totaling over 50 million kilograms annually, demonstrate the integrated nature of North American food supply chains that require consistent additive specifications across borders, according to the U.S. Customs and Border Protection. Regional harmonization efforts reduce regulatory complexity while enabling economies of scale for additive suppliers serving multiple markets within the trade bloc.

Competitive Landscape

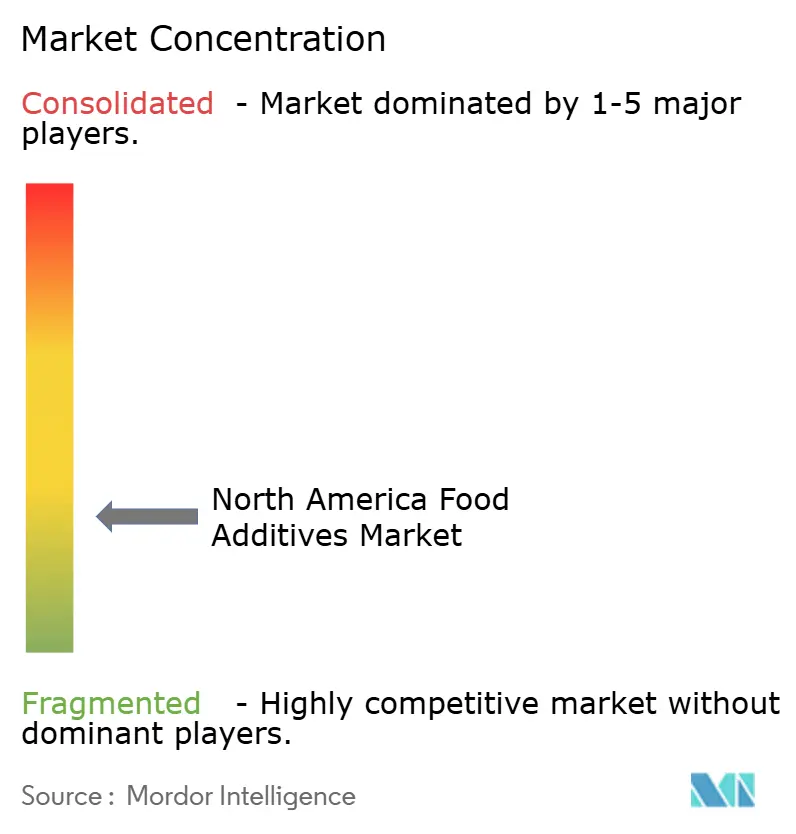

The North American food additives market is defined by a fragmented competitive landscape, with a concentration index of 3 out of 10. This fragmentation creates opportunities for specialized suppliers to target niche segments by leveraging innovation, regulatory expertise, and strategic partnerships with food manufacturers. Leading companies such as Cargill, ADM, and IFF utilize vertical integration and global supply chains to achieve cost advantages while heavily investing in clean-label alternatives and natural ingredient platforms.

The fragmented nature of the market allows smaller players to compete effectively in specialized areas like natural colorants, enzyme systems, and plant-based protein solutions, where technical expertise and regulatory compliance provide competitive advantages. Strategic consolidation is gaining momentum as companies aim to develop comprehensive additive portfolios and capitalize on synergies across functional categories. Recent acquisitions, such as Glanbia's USD 300 million purchase of Flavor Producers and Mars' USD 35.9 billion acquisition of Kellanova, highlight the industry's focus on expanding capabilities and market reach.

Technology-driven differentiation is becoming increasingly critical, with companies investing in proprietary formulation tools like Tate & Lyle's Sensation™ platform for optimizing mouthfeel and advanced delivery systems that enhance functionality while reducing inclusion rates. Patented innovations, such as Kerry's Accel plant-based curing agent, provide temporary competitive advantages and drive continued R&D investment across the industry. FDA compliance requirements favor established players with dedicated regulatory affairs teams, creating barriers for new entrants who may lack the resources to navigate complex approval processes and maintain ongoing compliance.

North America Food Additives Industry Leaders

-

Cargill Incorporated

-

Archer Daniels Midland Company

-

Novozymes AS

-

Tate and Lyle Plc

-

DuPont Numerous Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2024: Givaudan unveiled innovative fragrance solutions, aiming to elevate hair and personal wash applications. The newly introduced Bloomful Splash serves as a fragrance design aid, while Bloom Drops offers a fresh collection of accords, both crafted to enhance sensory experiences.

- June 2024: IFF, in collaboration with its in-house natural ingredients specialist LMR Naturals (LMR), introduced three new fragrance ingredients: Ylanganate, an innovative fragrance molecule, along with Grapefruit and Persian Lime Oils developed by LMR.

- December 2023: Archer Daniels Midland Company acquired Revela Foods, a Wisconsin-based developer and manufacturer of innovative dairy flavor ingredients and solutions. The purpose of this acquisition was to expand the company’s product portfolio.

- August 2023: IFF completed the expansion of its North American Creation and Design Center in New Century. The 3,700-square-foot upgrade integrated the company’s flavor and ingredient product development capabilities, strengthening its innovation capacity. The IFF Creative Center combined expertise in flavors, ingredients, and food design to better support the growth of the region’s food industry.

North America Food Additives Market Report Scope

Food additives are substances added to food to maintain or improve its safety, freshness, taste, texture, or appearance. The North American food additives market is segmented by type, application, and geography. For each segment, the market sizing and forecast have been done based on value (in USD million).

By Product Type

| Preservatives |

| Sweeteners |

| Sugar Substitutes |

| Emulsifiers |

| Anti-Caking Agents |

| Enzymes |

| Hydrocolloids |

| Food Flavors & Enhancers |

| Food Colorants |

| Acidulants |

By Source

| Natural |

| Synthetic |

By Application

| Bakery and Confectionery |

| Dairy and Desserts |

| Beverages |

| Meat and Meat Products |

| Soups, Sauces, and Dressings |

| Other Applications |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Preservatives |

| Sweeteners | |

| Sugar Substitutes | |

| Emulsifiers | |

| Anti-Caking Agents | |

| Enzymes | |

| Hydrocolloids | |

| Food Flavors & Enhancers | |

| Food Colorants | |

| Acidulants | |

| By Source | Natural |

| Synthetic | |

| By Application | Bakery and Confectionery |

| Dairy and Desserts | |

| Beverages | |

| Meat and Meat Products | |

| Soups, Sauces, and Dressings | |

| Other Applications | |

| By Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the North America food additives market in 2026?

The market is valued at USD 47.2 billion in 2026 and is forecast to reach USD 58.19 billion by 2031.

Which product type currently holds the highest share?

Sweeteners lead with 59.62% of sales thanks to sugar-reduction mandates and broad application in beverages and confectionery.

What is driving the fastest growth among applications?

Beverages post the quickest 5.46% CAGR as functional drinks and plant-based formulations demand advanced stability and flavor systems.

Which country offers the most attractive growth outlook?

Canada is projected to expand at a 5.55% CAGR through 2031 due to substantial government investment in processing capacity and natural ingredients.