North America Sugar Substitutes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

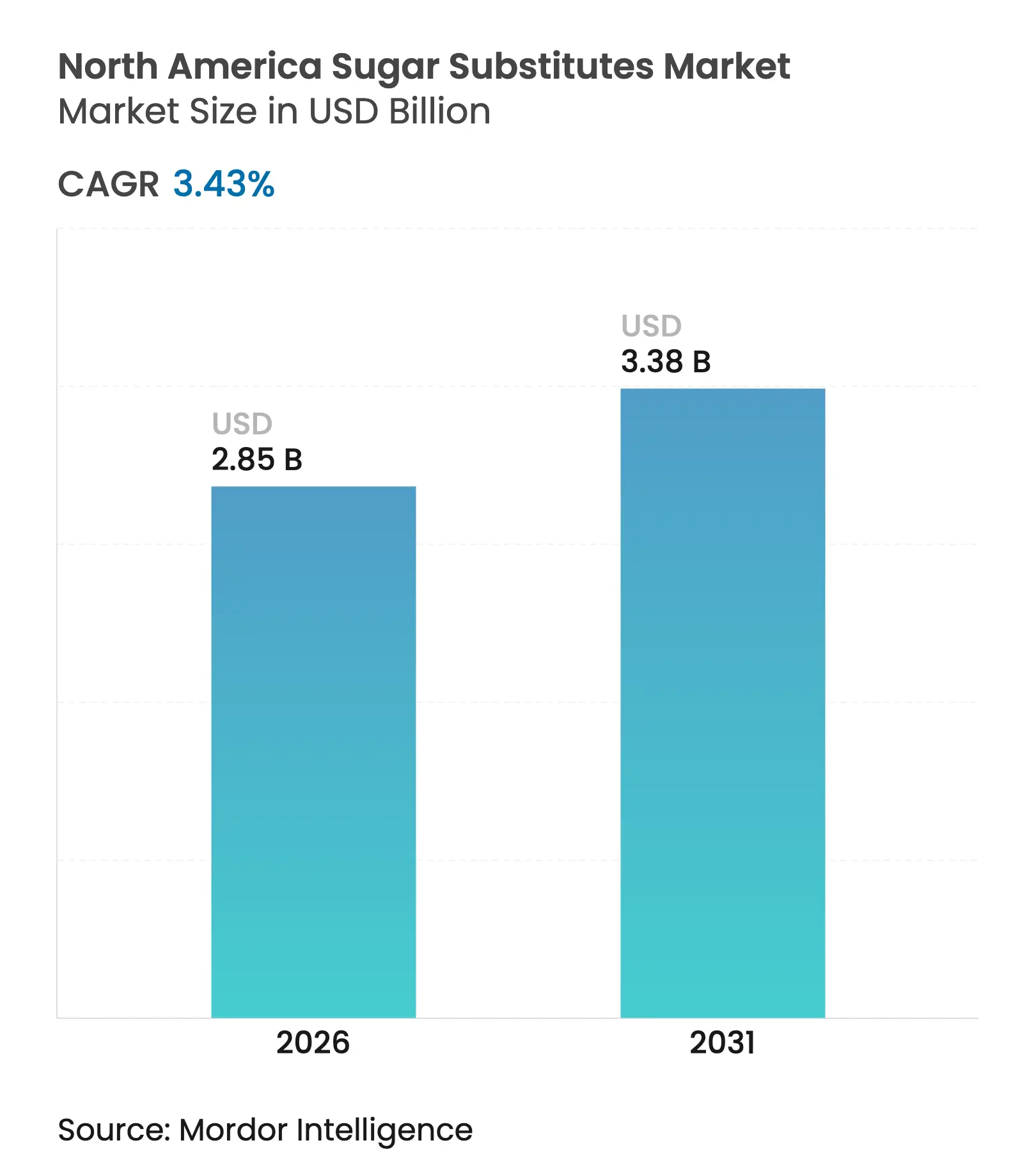

| Market Size (2026) | USD 2.85 Billion |

| Market Size (2031) | USD 3.38 Billion |

| Growth Rate (2026 - 2031) | 3.43 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

North America Sugar Substitutes Market Analysis by Mordor Intelligence

The North America sugar substitutes market size in 2026 is estimated at USD 2.85 billion, growing from 2025 value of USD 2.76 billion with 2031 projections showing USD 3.38 billion, growing at 3.43% CAGR over 2026-2031. This growth is driven by several factors, including stricter labeling regulations, an increasing number of health-conscious consumers, and efforts by major food and beverage companies to reformulate their products to include healthier alternatives. Industry consolidation, such as Tate & Lyle’s acquisition of CP Kelco, highlights a shift toward high-margin specialty ingredients while ensuring stable supply chains for essential plant-based raw materials. Market dynamics possess a clear regional concentration, with the United States leading the sugar substitutes market in North America, while Mexico is emerging as the fastest-growing area. High-intensity sweeteners hold the dominant position in the market, although sugar polyols are expanding rapidly due to their functional benefits, particularly in pharmaceutical uses. While synthetic sweeteners continue to account for the largest share, natural alternatives are gaining momentum as demand for clean-label and plant-based products strengthens. The North America sugar substitutes market is moderately fragmented, with several players competing in the space. Large companies such as Cargill, Incorporated, Ingredion, and Tate & Lyle hold significant influence due to their scale, global distribution networks, and strong research and development capabilities, the market also sees robust competition from niche, privately held firms like SweeGen, Pyure Brands.

Key Report Takeaways

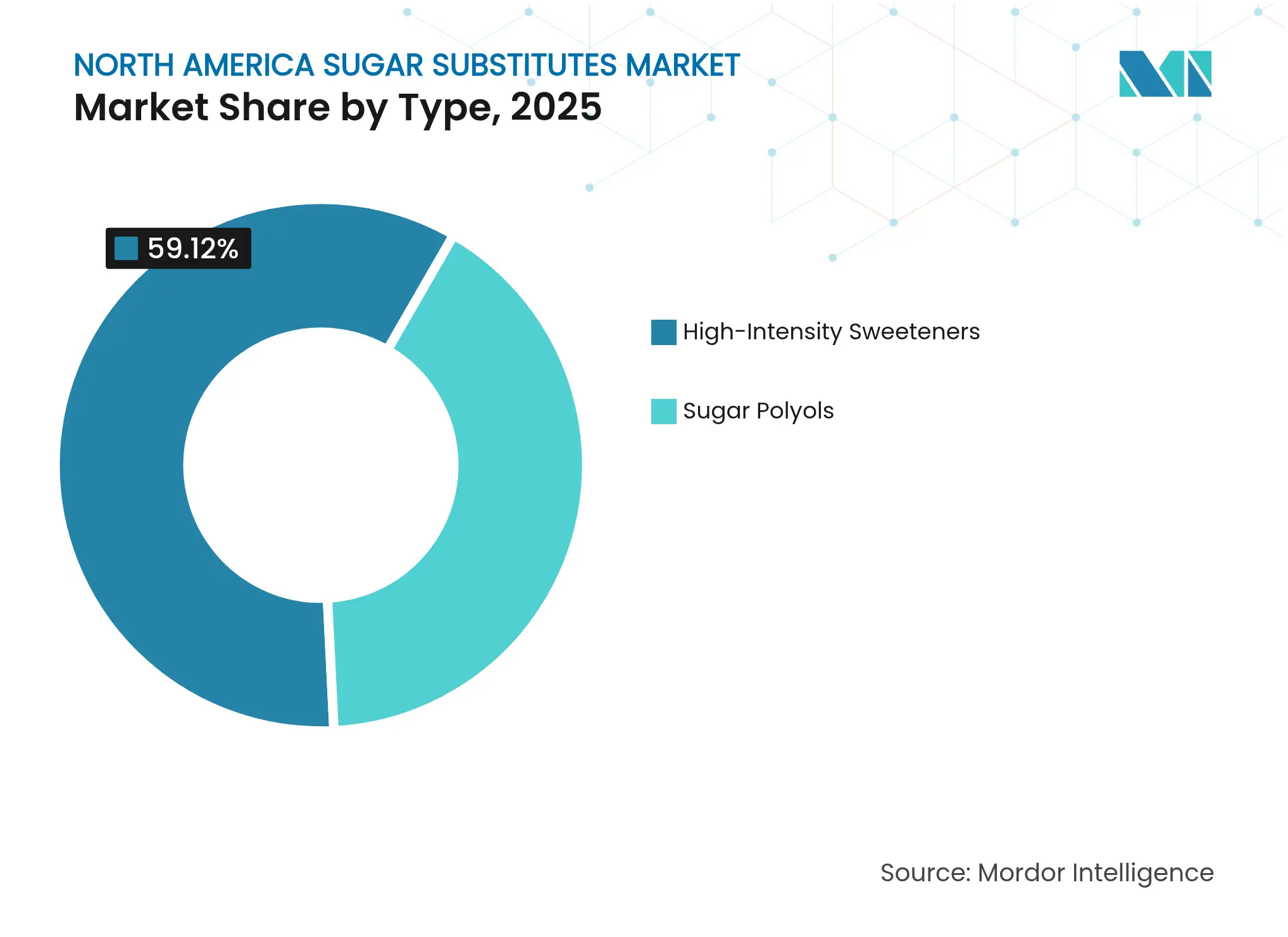

- By type, high-intensity sweeteners led with a 59.12% revenue share in 2025, while sugar polyols are forecast to grow at an 4.03% CAGR through 2031.

- By origin, synthetic alternatives captured 65.54% share of the North America sugar substitutes market size in 2025, yet plant-derived are set to advance at a 5.07% CAGR to 2031.

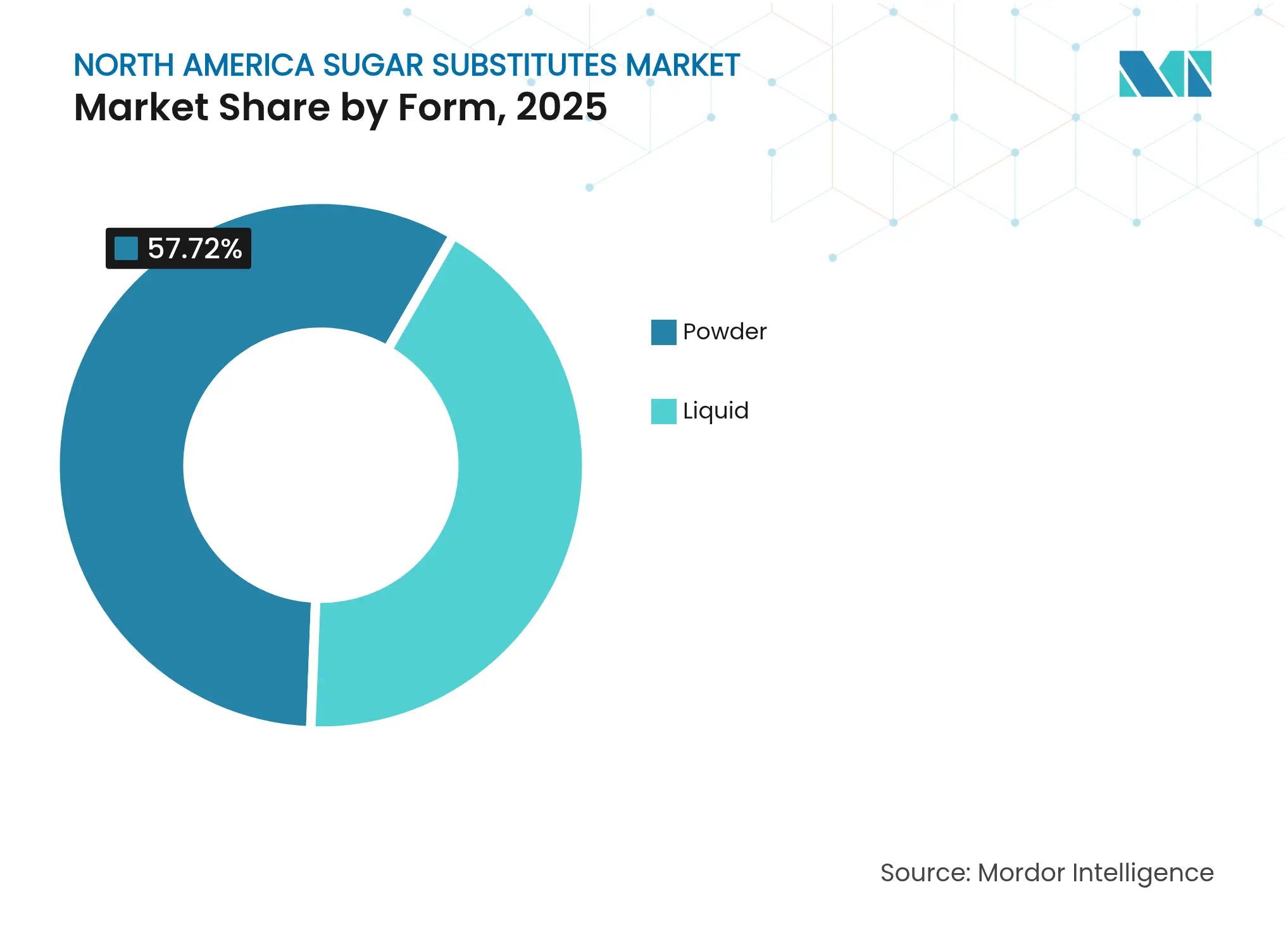

- By form, powder formats accounted for 57.72% of the North America sugar substitutes market size in 2025, and liquid formats are on track for a 5.01% CAGR through 2031.

- By application, beverages represented 28.45% revenue share in 2025, while pharmaceuticals are positioned for the highest 4.74% CAGR between 2026-2031.

- By geography, the United States held 74.01% of the North America sugar substitutes market share in 2025, whereas Mexico is projected to expand at an 4.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Sugar Substitutes Market Trends and Insights

Drivers Impact Table

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE | |||

|---|---|---|---|---|---|---|

Clean-label

movement accelerating adoption for natural sweeteners

Clean-label

movement accelerating adoption for natural sweeteners

| +0.8% | North America, with stronger influence in United States and Canada | Medium term (2-4 years) |

(~)

% IMPACT ON CAGR FORECAST

:

+0.8%

|

GEOGRAPHIC

RELEVANCE

:North

America, with stronger influence in United States and Canada |

IMPACT

TIMELINE

:

Medium

term (2-4 years)

|

Expansion

of low/no-sugar products fueling market growth Expansion

of low/no-sugar products fueling market growth | +1.2% | North America leading adoption with Mexico | Short term (≤ 2 years) | |||

Soaring

diabetes rates fueling demand for low-calorie sweeteners

Soaring

diabetes rates fueling demand for low-calorie sweeteners

| +0.9% | North America, particularly United States with highest diabetes prevalence | Long term (≥ 4 years) | |||

Rising shift to lower-carbon footprint ingredients Rising shift to lower-carbon footprint ingredients | +0.7% | United States and Canada, with Mexico following regulatory trends | Medium term (2-4 years) | |||

Advances in extraction and processing technologies reduce production costs Advances in extraction and processing technologies reduce production costs | +0.4% | North America, driven by corporate sustainability commitments | Long term (≥ 4 years) | |||

Sugar substitutes offer customizable sweetness and texture profile Sugar substitutes offer customizable sweetness and texture profile | +0.6% | North America, with focus on processed food growth | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Clean-label movement accelerating adoption for natural sweeteners

The clean-label movement is making natural sweeteners increasingly popular in North America, as consumers now prefer plant-based and easily recognizable ingredients over artificial ones. This shift has led many well-known brands to replace synthetic sweeteners like aspartame and sucralose with enzyme-modified steviol glycosides, which are derived from natural sources. Regulatory changes are also playing a key role in this transition. In January 2025, the FDA updated its definition of “healthy,” which now excludes high-intensity sweeteners from being counted as added sugars[1]Source: Food and Drug Administration, "Use of the 'Healthy' Claim on Food Labeling," fda.gov. This update provides brands with a significant advantage in marketing their products as healthier choices. Sustainability concerns are influencing this trend. Stevia has a much lower carbon footprint compared to traditional cane sugar. Companies like Tate & Lyle plc are taking proactive measures. For instance, in 2024, Tate & Lyle plc partnered with Manus Bio to produce Reb M stevia entirely within the Americas. This collaboration demonstrates how clean-label preferences are transforming supply chains to align with consumer demand for healthier, more sustainable, and environmentally friendly options.

Expansion of low/no-sugar products fueling market growth

The growing demand for low and no-sugar products is driving the use of low-calorie sweeteners as food and beverage companies adjust to changing consumer preferences. A 2024 IFIC Food and Health survey shows that 66% of consumers are interested in reduced-sugar products, highlighting a shift toward healthier choices[2]Source: Food Insights, "2024 IFIC Food and Health Survey," foodinsight.org. This trend is especially noticeable in the beverage industry. For instance, Coca-Cola HBC reported that 21% of its 2024 revenue came from low or no-sugar drinks. Similarly, PepsiCo launched Gatorade Hydration Booster in 2024, a product with no artificial sweeteners or flavors, aimed at consumers looking for cleaner labels. These examples show how major brands are using low-calorie sweeteners to stay relevant with health-conscious buyers. The increasing use of GLP-1 weight management drugs is influencing food choices, as these medications lead users to cut back on sweetened products. This has further boosted the demand for sugar substitutes. For example, Cargill launched the EverSweet + ClearFlo Stevia System in North America, which combines steviol glycosides with a taste-enhancing agent to improve flavor, solubility, and stability.

Soaring diabetes rates fueling demand for low-calorie sweeteners

The increasing prevalence of diabetes across North America is significantly boosting the demand for low-calorie sweeteners. With healthcare professionals and public health initiatives encouraging people to reduce sugar intake to manage blood sugar levels, these sweeteners are becoming more essential. According to the International Diabetes Federation (IDF), as of 2024, number of deaths before the age of 80 due to diabetes was 526,000 in North America and Caribbean[3]Source: International Diabetes Federation, "IDF Diabetes Atlas 2025", diabetesatlas.org. To support patients in adhering to their treatment plans, pharmaceutical companies are incorporating sweeteners like xylitol, maltitol, and stevia into medications. These sweeteners enhance the taste of medicines without causing spikes in blood sugar levels. Meanwhile, regulatory bodies like the FDA are working on new front-of-pack labeling systems, such as a “traffic light” approach, to clearly indicate added sugar content. The diabetes epidemic drives regulatory support for sugar reduction initiatives, as evidenced by the FDA's proposed front-of-package labeling requirements highlighting added sugar content. This health crisis creates long-term market stability for sugar substitutes, as diabetes management requires sustained dietary modifications rather than temporary consumption changes.

Rising Shift to Lower-Carbon Footprint Ingredients

Rising corporate and regulatory pressure to decarbonize supply chains is steering buyers toward sweeteners with verifiable low-emission footprints. Major beverage and snack companies have tied executive bonuses to science-based climate targets, so procurement teams now favor emissions-audited options such as bioconverted Reb M and corn-fermented erythritol. New disclosure laws in California and Canada mandate granular reporting of ingredient-level emissions, making carbon data as pivotal as nutritional data for compliance according to U.S Food and Drug. California's new climate disclosure laws, specifically SB 253 and SB 261, mandate that large companies doing business in the state publicly report their greenhouse gas (GHG) emissions and climate-related financial risks. These dynamics add lift to the North America sugar substitutes market’s CAGR, as suppliers that pair health claims with climate credentials capture outsized demand.

Restraints Impact Analysis

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE | |||

|---|---|---|---|---|---|---|

Regulatory

ambiguity around novel sweeteners

Regulatory

ambiguity around novel sweeteners

| -0.6% | North America, particularly affecting United States GRAS pathway reforms | Short term (≤ 2 years) |

(~)

% IMPACT ON CAGR FORECAST

:

-0.6%

|

GEOGRAPHIC

RELEVANCE

:North

America, particularly affecting United States GRAS pathway reforms |

IMPACT

TIMELINE

:

Short

term (≤ 2 years)

|

Consumer

safety perception issues around artificial sweeteners

Consumer

safety perception issues around artificial sweeteners

| -0.4% | North America, with stronger impact in health-conscious demographics | Medium term (2-4 years) | |||

Stevia leaf

supply-chain vulnerability amid logistic disruptions

Stevia leaf

supply-chain vulnerability amid logistic disruptions

| -0.3% | supply chains affecting North American processors | Short term (≤ 2 years) | |||

Competition from natural sugars Competition from natural sugars | -0.5% | North America, limiting adoption in premium food applications | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Regulatory ambiguity around novel sweeteners

Regulations for new sweeteners are becoming more challenging, creating significant obstacles for companies, especially smaller or newer ones. In March 2025, the U.S. Department of Health and Human Services (HHS) removed the option for companies to self-declare their ingredients as GRAS (Generally Recognized As Safe). This means that all new sweeteners must now go through a full FDA approval process before they can be sold. This change has made it more expensive and time-consuming for companies to introduce new ingredients, as they now need to conduct extensive safety testing. As of late 2024, over 50 GRAS applications are still waiting for FDA review, including innovative ingredients like enzyme-modified stevia and sweet proteins. These delays in approval are slowing down innovation and making it harder for brands to access new, clean-label sweeteners that consumers increasingly prefer. For smaller companies, this regulatory shift adds significant pressure, as they often lack the resources to navigate the lengthy and costly approval process.

Consumer safety perception issues around artificial sweeteners

Although artificial sweeteners like sucralose and aspartame have been approved as safe by regulatory bodies, many consumers remain doubtful about their safety. This distrust is often driven by misinformation spread through social media and concerns highlighted by environmental studies. For example, the U.S. Geological Survey (USGS) has revealed that compounds such as sucralose can persist in wastewater systems, even though the detected levels are not harmful to human health. To address these concerns, brands are increasingly adopting blended sweetener systems that combine artificial sweeteners with natural alternatives like stevia or monk fruit. This strategy helps alleviate consumer apprehensions while maintaining the desired taste and functionality of the products. On the other hand, products that exclusively use artificial sweeteners are now being targeted more toward cost-conscious consumers, where affordability is prioritized over ingredient preferences, rather than the broader health-focused market.

Segment Analysis

By Type: Polyols Drive Functional Innovation

Sugar polyols are expected to grow significantly, with a projected CAGR of 4.03%, as they increasingly replace high-intensity sweeteners in certain applications. These polyols, such as xylitol and erythritol, are gaining popularity due to their ability to provide bulk and retain moisture, making them highly effective in products like tablet coatings and controlled-release capsules. These functional benefits are driving their adoption in the pharmaceutical sector, where they help ensure the required compression strength and moisture control. Advancements in production technologies, such as circular-economy fermentation using lignocellulosic biomass, are reducing manufacturing costs. This cost reduction is encouraging more companies to incorporate polyols into their formulations.

Despite the growth of polyols, high-intensity sweeteners remain the dominant segment in the North America sugar substitutes market, holding a 59.12% share in 2025. These sweeteners have maintained their position due to their long-established safety records and cost efficiency. However, their growth has slowed as regulatory scrutiny increases and consumer preferences shift toward natural and less processed options. To stay competitive, manufacturers of high-intensity sweeteners are focusing on developing next-generation products like brazzein and sucrose-binding sweet proteins. These innovations aim to enhance taste by reducing bitterness without the need for bulking agents.

Note: Segment shares of all individual segments available upon report purchase

By Origin: Natural Sweeteners Accelerate Despite Synthetic Dominance

Synthetic sugar substitutes accounted for 65.54% of the market share in 2025, driven by their widespread use in legacy formulations and cost advantages. These synthetic variants remain a preferred choice, especially in industrial bakeries, due to their superior heat stability and affordability. Despite their dominance, the market is witnessing a gradual shift as natural sweeteners gain traction. Natural sugar substitutes, such as enzyme-converted Reb M and monk fruit extracts, are growing at a CAGR of 5.07%. This growth is fueled by increasing consumer demand for clean-label products and sustainability-focused narratives. Innovations like Cargill’s yeast-based EverSweet production method enable large-scale manufacturing of nature-identical molecules, which meet "from natural sources" labeling requirements without relying on traditional crop yields.

The trend toward natural sweeteners is particularly evident in premium product ranges, where "natural" is becoming a standard expectation. Industries such as brewing, dairy, and nutraceuticals are increasingly adopting fermented steviol glycosides to ensure a consistent supply while mitigating risks associated with agricultural dependency. On the other hand, synthetic sweetener suppliers are responding to this shift by offering large-volume discounts and enhanced technical support to retain their customer base. However, they face growing challenges, including rising input costs for corn-based raw materials, which are putting pressure on profit margins. The competition between synthetic and natural sugar substitutes is expected to intensify, with natural options gaining more ground in response to consumer preferences and sustainability concerns.

By Form: Liquid Applications Drive Innovation

Liquid formulations are experiencing the fastest growth, with a CAGR of 5.01%, as beverage manufacturers increasingly adopt continuous blending systems. These systems are better suited for handling liquid sweeteners compared to traditional dry-loading methods. Innovations, such as enhanced mineral-salt complexes in liquid sweeteners, have improved their taste profile by reducing lingering sweetness. This advancement has driven their adoption in zero-sugar colas and flavored waters, making liquid sweeteners a key growth area in the North America sugar substitutes market. The convenience and efficiency of liquid formulations are expected to support their steady rise in demand through 2031.

Powdered sweeteners, which currently account for 57.72% of the market, continue to evolve with advancements like micro-encapsulation and low-dust granulation techniques. These improvements enhance flowability and make powdered sweeteners more suitable for industrial applications, such as bakery premixes. Additionally, powdered stevia blends now include carrier fibers that improve dispersibility, further expanding their usability in large-scale food production. For consumers, powdered sweeteners remain a popular choice in table-top packets due to their portability and ease of portion control, ensuring their continued relevance in the market.

Note: Segment shares of all individual segments available upon report purchase

By Application: Pharmaceuticals Lead Growth Acceleration

The pharmaceutical sector is witnessing remarkable growth, with a strong CAGR of 4.74%, making it the fastest-growing channel in the sugar substitutes market. This growth is primarily driven by the increasing use of polyols in chewable tablets and syrups, as they improve taste and make medications more palatable. Stevia-based sweeteners are also gaining popularity in pediatric antibiotic formulations due to their ability to effectively mask bitterness, ensuring better compliance among children. Saccharin is being explored for its potential antimicrobial properties, which could add therapeutic value alongside its role as a sweetener, further boosting its demand in the pharmaceutical industry.

The beverage industry continues to dominate the sugar substitutes market, contributing 28.45% of sales in 2025. Although its growth rate is slower compared to other segments, it remains a key driver of market volume. Beverage manufacturers are prioritizing the enhancement of taste and texture to improve the sensory experience of their products, rather than focusing on expanding product lines. At the same time, the bakery and confectionery sectors are actively reformulating their offerings to incorporate sugar substitutes, ensuring their relevance in the market. Niche applications, such as personal care and industrial uses, are emerging as profitable opportunities.

Geography Analysis

The United States leads the North America sugar substitutes market, contributing 74.01% of the revenue share in 2025. This dominance is supported by a well-established regulatory framework and a strong research and development ecosystem, which foster consumer trust and enable the rapid adoption of innovative ingredients. The FDA’s proposed changes, such as front-of-package traffic-light labeling and potential revisions to the GRAS (Generally Recognized as Safe) pathway, are expected to reshape market dynamics. The U.S. Food and Drug Administration has extended the comment period for the proposed front-of-package (FOP) nutrition labeling rule to July 15, 2025, providing an additional 60 days for feedback. These changes aim to enhance safety standards and transparency, further strengthening consumer confidence.

Canada plays a crucial role as a secondary market, with its regulatory environment driving innovation and reformulation. Health Canada’s upcoming front-of-pack labeling requirement, set to take effect in January 2026, is pushing manufacturers to reformulate their products to meet new standards. The harmonization of additive regulations and streamlined marketing authorizations has reduced approval timelines, enabling Canadian companies to innovate more efficiently. Furthermore, the emergence of stevia extraction and fermentation start-ups in regions like Vancouver and Montreal highlights the growing expertise and capacity within the country.

Mexico is the fastest-growing market in the region, with a projected CAGR of 4.92%. Rising urban incomes, mandatory sugar-warning labels, and the benefits of duty-free ingredient movement under the USMCA agreement fuel this growth. Domestic manufacturers are increasingly sourcing locally grown agave and cane to produce inulin-polyol blends, which enhances supply chain resilience. Additionally, cross-border co-manufacturing partnerships with beverage plants in Texas and California are enabling efficient scaling and the transfer of advanced sweetener technologies. These collaborations are helping Mexican producers incorporate innovative sweet proteins into their reformulated products, further driving market growth.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

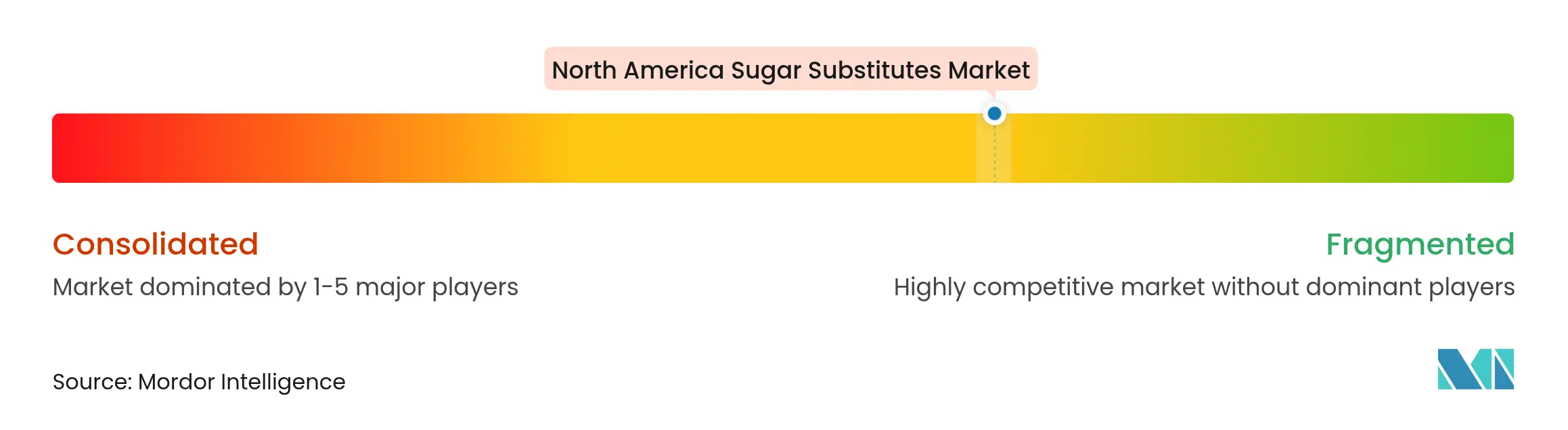

Market Concentration

The North American sugar substitutes market is moderately fragmented. Some of the prominent market players include Cargill, Incorporated, Ingredion Incorporated, Archer Daniels Midland Company, Tate & Lyle PLC, and International Flavors & Fragrances Inc., among others. A notable development in the market was Tate & Lyle's acquisition of CP Kelco for USD 1.8 billion in November 2024. This acquisition significantly expanded Tate & Lyle’s portfolio of hydrocolloids and sweeteners, enabling the company to offer combined solutions for texturizing and sweetening. The deal is expected to generate annual cooperation of USD 50 million, highlighting the growing trend of consolidation in the industry as companies aim to strengthen their market positions and enhance supply chain efficiency.

Innovation continues to play a critical role in driving competition within the market. For instance, Cargill’s EverSweet platform uses precision fermentation technology to produce rebaudioside M, a high-purity stevia sweetener, without relying on agricultural cycles. This ensures a consistent supply for beverage manufacturers seeking natural sweetener options. Additionally, patent disputes are shaping the competitive landscape. In January 2024, SweeGen won an appellate case against PureCircle, which invalidated key patents related to Reb M production. This legal victory has opened up opportunities for smaller players and independent bottlers to access advanced sweetener technologies. Meanwhile, niche players are focusing on specialized applications, such as supplying co-processed polyol blends for pharmaceutical uses like orodispersible tablets, which offer high margins despite lower volumes.

Regulatory adaptability is becoming a key competitive advantage in the sugar substitutes market. Companies with in-house toxicology and legal expertise are better positioned to navigate evolving regulations, such as the U.S. Department of Health and Human Services’ (HHS) shift away from self-affirmed GRAS (Generally Recognized as Safe) approvals, which now require more comprehensive data submissions. To mitigate agricultural risks, some suppliers are relocating stevia leaf production closer to North American demand centers by adopting greenhouse cultivation and bioconversion technologies. These strategies not only enhance supply chain resilience but also support the growing demand for sustainable and locally sourced ingredients.

North America Sugar Substitutes Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Ingredion's PureCircle introduced a stevia sweetener that directly replaces sugar in formulations. The natural sweetener functions similarly to sugar without requiring additional ingredients and is suitable for beverages, syrups, and sauces.

- January 2024: North Carolina-based Elo Life Systems closed a USD 20.5 million Series A2 round to accelerate the development of a natural high-intensity sweetener and Cavendish bananas engineered to resist the devastating Fusarium wilt fungal disease (TR4).

Table of Contents for North America Sugar Substitutes Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Clean-Label Movement Accelerating Adoption for Natural Sweeteners

- 4.2.2Expansion of Low/No-Sugar Products Fueling Market Growth

- 4.2.3Soaring Diabetes Rates Fuelling Demand for Low-Calorie Sweeteners

- 4.2.4Rising Shift to Lower-Carbon Footprint Ingredients

- 4.2.5Advances In Extraction and Processing Technologies Reduce Production Costs

- 4.2.6Sugar Substitutes Offer Customizable Sweetness and Texture Profile

- 4.3Market Restraints

- 4.3.1Regulatory Ambiguity Around Novel Sweeteners

- 4.3.2Consumer Safety Perception Issues Around Artificial Sweeteners

- 4.3.3Stevia Leaf Supply-Chain Vulnerability Amid Logistic Disruptions

- 4.3.4Competition from Natural Sugars

- 4.4Supply Chain Analysis

- 4.5Regulatory Outlook

- 4.6Porter's Five Forces

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers/Consumers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitute Products

- 4.6.5Intensity of Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Type

- 5.1.1High-Intensity Sweeteners

- 5.1.1.1Acesulfame Potassium

- 5.1.1.2Advantame

- 5.1.1.3Aspartame

- 5.1.1.4Neotame

- 5.1.1.5Saccharin

- 5.1.1.6Sucralose

- 5.1.1.7Stevia

- 5.1.1.8Monk Fruit

- 5.1.1.9Other High-Intensity Sweeteners

- 5.1.2Sugar Polyols

- 5.1.2.1Sorbitol

- 5.1.2.2Xylitol

- 5.1.2.3Maltitol

- 5.1.2.4Erythritol

- 5.1.2.5Other Sugar Polyols

- 5.2By Origin

- 5.2.1Plant-Derived

- 5.2.2Synthetic

- 5.2.3Biotechnologically Fermented

- 5.3By Form

- 5.3.1Powder

- 5.3.2Liquid

- 5.4By Application

- 5.4.1Food

- 5.4.1.1Bakery and Cereals

- 5.4.1.2Confectionery

- 5.4.1.3Dairy and Dairy Alternatives

- 5.4.1.4Sauces, Condiments and Dressings

- 5.4.1.5Other Food Applications

- 5.4.2Beverage

- 5.4.2.1Carbonated Soft Drinks

- 5.4.2.2RTD Tea and Coffee

- 5.4.2.3Sports and Energy Drinks

- 5.4.2.4Other Beverages

- 5.4.3Pharmaceuticals

- 5.4.4Other Applications

- 5.5By Geography

- 5.5.1United States

- 5.5.2Canada

- 5.5.3Mexico

- 5.5.4Rest of North America

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Positioning Analysis

- 6.4Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1Cargill, Incorporated

- 6.4.2Ingredion Incorporated

- 6.4.3Archer Daniels Midland Company

- 6.4.4Tate & Lyle PLC

- 6.4.5International Flavors & Fragrances Inc.

- 6.4.6BioNeutra Global Corporation

- 6.4.7Pyure Brands, LLC

- 6.4.8Roquette Freres

- 6.4.9SweeGen, Inc.

- 6.4.10GLG Life Tech Corporation

- 6.4.11Ajinomoto Co., Inc.

- 6.4.12Celanese Corporation

- 6.4.13Merck KGaA

- 6.4.14JK Sucralose Inc.

- 6.4.15HYET Sweet B.V.

- 6.4.16Lallemand Inc

- 6.4.17Steviva Brands, Inc.

- 6.4.18NutraEx Food Inc

- 6.4.19Cumberland Worldwide Holdings, Inc

- 6.4.20Kerry Group PLC

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

North America Sugar Substitutes Market Report Scope

The North American sugar substitute market is segmented by type, origin, form, application, and geography. By type, the market is segmented into high-intensity sweeteners (acesulfame potassium, advantame, aspartame, neotame, saccharin, sucralose, stevia, monk fruit and others) and sugar polyols (sorbitol, xylitol, maltitol, erythritol and others). By origin, the market is segmented into plant-derived, synthetic and biotechnologically fermented. By form, into powder and liquid. By application, the market is segmented into food, beverage, pharmaceuticals and others. The food segment is further segmented into bakery and cereals, confectionery, dairy and dairy alternatives, sauces, condiments, and dressings, and other food applications. The beverage segment is further segmented into carbonated soft drinks, RTD tea and coffee, sports and energy drinks and other beverages. This report further analyses the scenario in the United States, Canada, Mexico, and the rest of North America.