Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

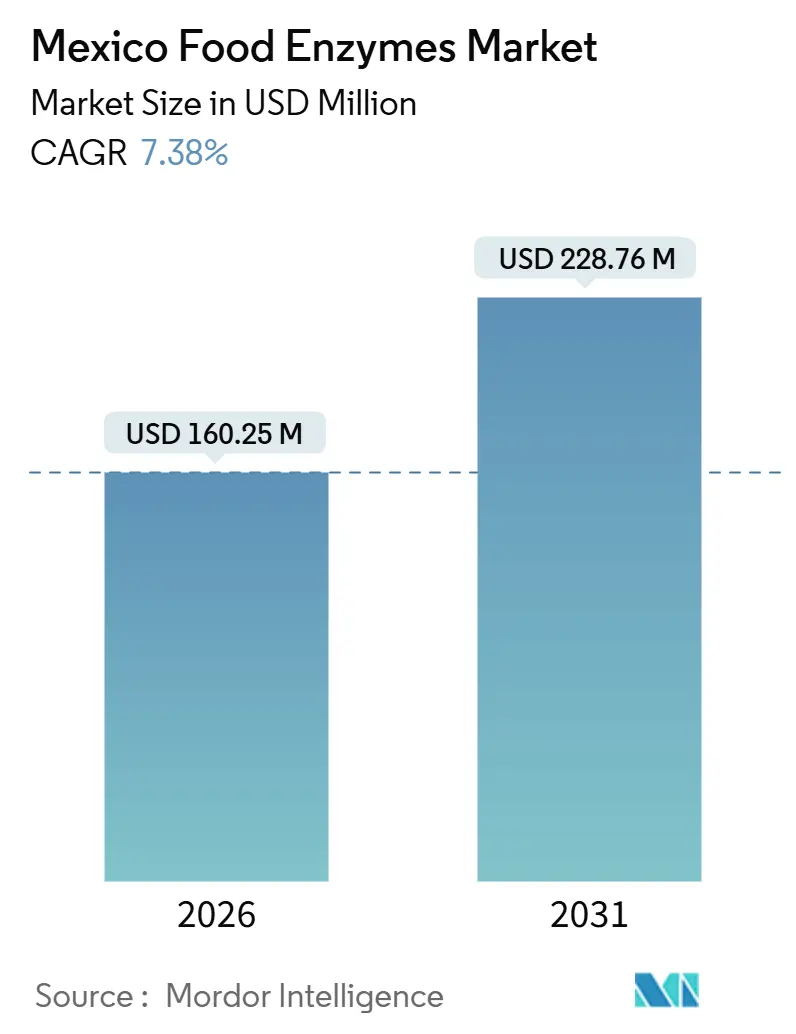

| Market Size (2026) | USD 160.25 Million |

| Market Size (2031) | USD 228.76 Million |

| Growth Rate (2026 - 2031) | 7.38% CAGR |

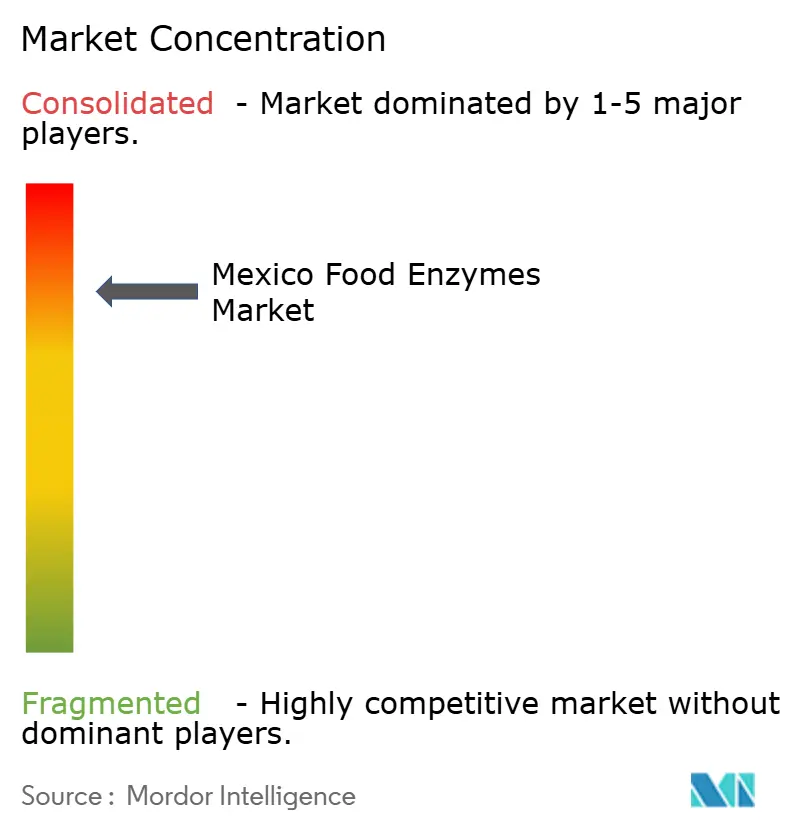

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Food Enzymes Market Analysis by Mordor Intelligence

The Mexico food enzymes market size is expected to reach USD 160.25 million by 2026 and is projected to grow to USD 228.76 million by 2031, registering a CAGR of 7.38%. This growth is driven by Mexico's significant role in North American food processing, increasing demand for clean-label formulations, and the adoption of precision fermentation to ensure cost stability. Key application areas include bakery, beverages, and functional foods, where enzymes are utilized for dough conditioning, lactose removal, and protein modification. The market remains competitive, with multinational companies expanding local capacities. Regulatory oversight by COFEPRIS enforces consistent quality standards, benefiting established players. While price-sensitive processors often compare enzymes with lower-cost chemical additives, clean-label requirements, rising protein costs, and urban convenience trends are broadening market opportunities.

Key Report Takeaways

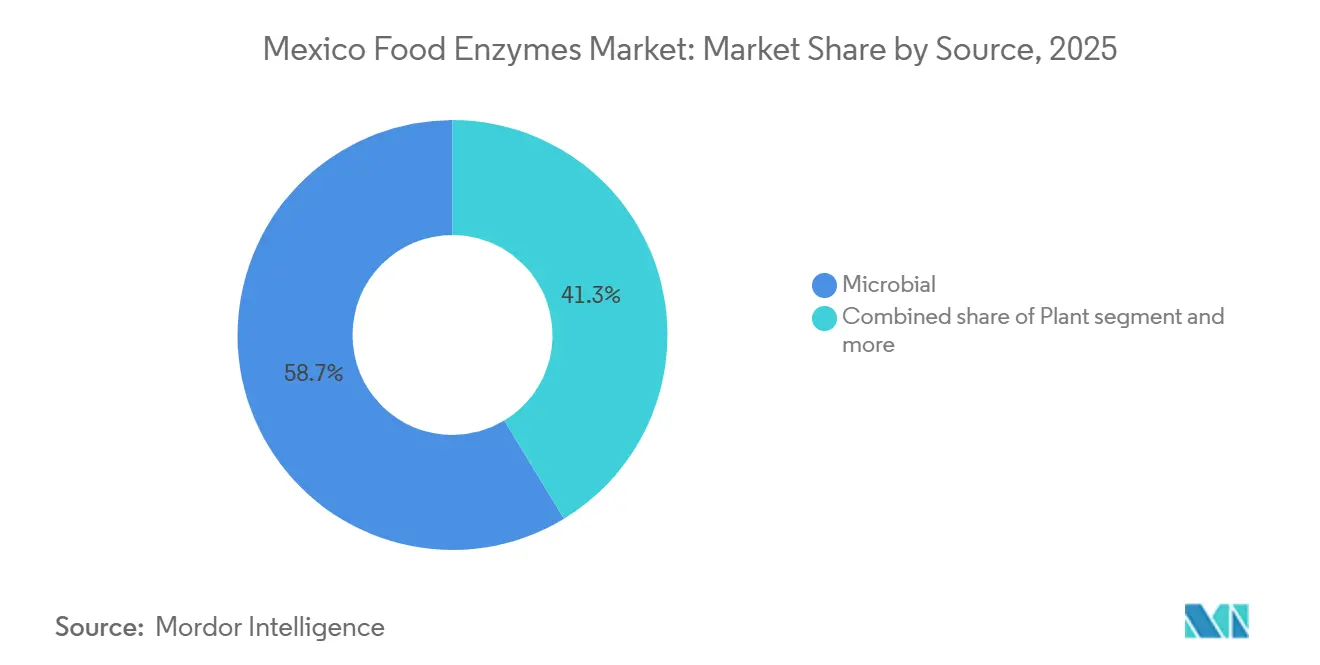

- By source, microbial enzymes held 58.68% of the Mexico food enzymes market share in 2025, while plant-derived variants are advancing at an 8.75% CAGR to 2031.

- By enzyme type, carbohydrases led with 36.45% of the Mexico food enzymes market size in 2025; proteolytic enzymes are expected to register an 8.59% CAGR to 2031.

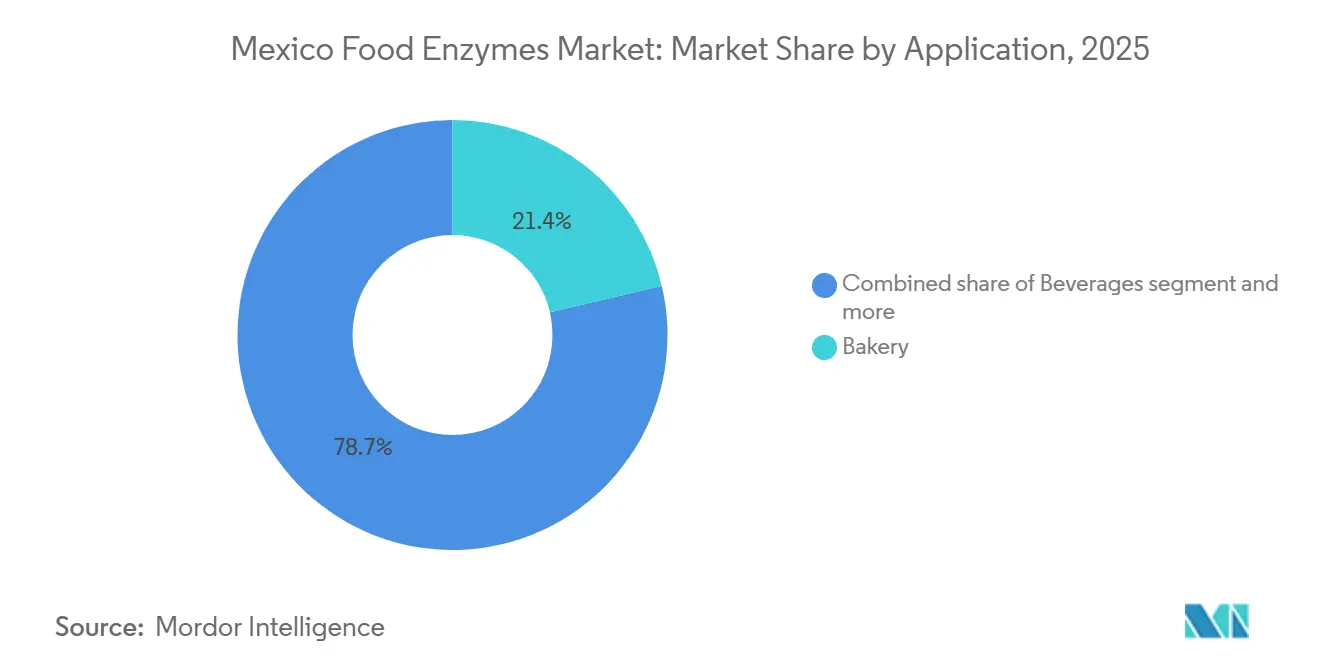

- By application, bakery captured 21.35% of the Mexico food enzymes market share in 2025; beverages are forecast to grow at a 9.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Mexico Food Enzymes Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for processed and convenience foods | +1.2% | National, concentrated in urban centers (Mexico City, Guadalajara, Monterrey) | Medium term (2-4 years) |

| Mexico's expanding bakery processing industry | +1.4% | National, with Grupo Bimbo facilities in Toluca, Azcapotzalco, and export hubs | Long term (≥ 4 years) |

| Clean-label and natural ingredient preference | +1.0% | National, stronger in premium retail channels and export-oriented production | Medium term (2-4 years) |

| Strategic investments by enzyme manufacturers | +0.9% | National, with spillover to Central America via distribution networks | Short term (≤ 2 years) |

| Growth of functional and specialty foods | +0.8% | National, early adoption in metropolitan areas and health-conscious segments | Medium term (2-4 years) |

| Technological advancements in enzyme production | +0.7% | Global, with localized benefits in Mexico through multinational subsidiaries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for processed and convenience foods

The increasing consumption of processed and convenience foods in Mexico is a significant driver for the food enzymes market, largely influenced by growing urbanization. With Mexico’s urbanization rate expected to exceed 80% by 2024, reduced meal-preparation time has led consumers to prefer more shelf-stable bakery products, ready-to-drink beverages, and pre-marinated proteins that align with busy lifestyles [1]Source: World Bank, "Urban population (% of total population) - Mexico", worldbank.org. These convenience-focused products require advanced processing solutions to ensure consistent quality, texture, and flavor, driving demand for enzymatic technologies that enhance industrial production efficiency. Additionally, rising meat consumption in Mexico reinforces this trend, particularly for processed meat products that incorporate marinade systems, improved texture, and extended shelf life. According to USDA Agricultural Projections to 2033, Mexico’s combined consumption of poultry, pork, and beef is projected to reach 82.5 kilograms per capita, approximately two-thirds of the projected U.S. per capita meat consumption (124.0 kilograms) [2]Source: Economic Research Service U.S. DEPARTMENT OF AGRICULTURE, "Meat Consumption in Mexico, Led by Poultry, Will Continue Rising Over Next Decade, USDA Projections Show", usda.gov. This substantial and growing demand for meat, much of it in processed or ready-to-prepare forms, further increases the need for food enzymes such as proteases, amylases, and other catalytic solutions that enhance texture, flavor release, and microbial stability in large-scale production.

Mexico’s expanding bakery processing industry

The growth of Mexico's bakery processing industry is a significant driver for the food enzymes market, fueled by the strong consumer dependence on bread and pasta as daily staples and the increasing industrialization of bakery production. Large-scale bakeries are focusing on improving efficiency, ensuring consistency, and maintaining product quality, which has led to a rising demand for enzymes that enhance dough handling, improve texture, extend shelf life, and streamline production processes. In 2024, per capita bread consumption in Mexico stands at 44 kilograms (97 pounds), while pasta consumption is at 3.2 kilograms (7 pounds), as reported by the U.S. Department of Agriculture, highlighting the consistent demand for these staples and the need for advanced enzymatic solutions [3]Source: U.S. DEPARTMENT OF AGRICULTURE, "Grain and Feed Update", usda.gov. As producers scale operations to meet this demand while minimizing formulation variability and reducing reliance on chemical additives, food enzymes have become critical components, supporting the growth and modernization of Mexico's bakery processing industry.

Clean‑label and natural ingredient preference

Increasing consumer awareness of health, wellness, and transparency is driving the demand for clean-label and natural ingredients in Mexico, influencing product formulation within the food industry. Urban and health-conscious consumers are prioritizing foods with minimal artificial additives, natural flavors, and easily recognizable ingredients. This shift has encouraged manufacturers to adopt enzymatic solutions that provide the desired functionality while maintaining clean-label standards. Food enzymes, including amylases, proteases, and lipases, help improve texture, shelf life, dough performance, and flavor development naturally, serving as alternatives to chemical additives and enhancers. This trend is particularly prominent in bakery products, beverages, dairy alternatives, and convenience foods, where enzyme technology enables producers to meet consumer demands for natural, high-quality, and transparent products while ensuring industrial efficiency and consistent performance.

Strategic investments by enzyme manufacturers

Strategic investments by global and regional enzyme manufacturers are driving the growth of Mexico's food enzymes market through expanded production capacity, enhanced research and development capabilities, and the introduction of enzyme technologies tailored to local food processing requirements. Companies are establishing advanced manufacturing facilities, application laboratories, and co-creation centers to develop enzymes that enhance product quality, processing efficiency, and shelf life across bakery, meat, dairy, and beverage segments. For example, Novozymes invested 2,017 million DKK in research and development in 2023, up from 2,001 million DKK in 2022, demonstrating its commitment to innovation and technological advancement. These investments enable manufacturers to provide solutions such as plant-based, clean-label, and specialty enzymes, addressing evolving consumer preferences while improving supply reliability and technical support for local food producers. By strengthening their presence and capabilities in Mexico, enzyme manufacturers are accelerating the adoption of enzymatic solutions, driving market growth, and solidifying the country's position as a key hub in Latin America's food processing industry.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory process (COFEPRIS) | -0.6% | National, affecting all enzyme imports and domestic production | Long term (≥ 4 years) |

| Raw material and energy cost volatility | -0.5% | National, with acute impact on fermentation facilities in energy-intensive regions | Short term (≤ 2 years) |

| Consumer skepticism over GMO-derived enzymes | -0.4% | National, concentrated in premium retail and organic channels | Medium term (2-4 years) |

| Competition from lower-cost chemical additives | -0.3% | National, strongest in value-tier bakery and confectionery segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Process (COFEPRIS)

On July 1, 2024, COFEPRIS updated Anexo VI (Enzimas), establishing requirements for toxicology data, analytical methods, and manufacturing process descriptions to accompany sanitary import permits. While these permits have a nominal resolution timeline of five days, the process often extends to weeks if dossiers are incomplete or require clarification. Enzyme suppliers must demonstrate that each preparation meets purity standards and is free from pathogenic microorganisms. This requirement tends to favor multinational companies with dedicated regulatory affairs teams, while smaller entrants may face challenges due to limited resources for compiling comprehensive safety dossiers. The regulatory framework aligns with Codex Alimentarius and EFSA guidelines, ensuring that approved enzymes meet international safety standards. However, it also creates obstacles for innovation. Novel enzyme variants derived from precision fermentation or non-traditional microbial hosts face longer approval cycles, as COFEPRIS lacks experience in evaluating recombinant production strains. This situation benefits established players such as Novozymes, DSM-Firmenich, and IFF, who already have legacy enzyme approvals in place. However, it delays the introduction of next-generation formulations that could replace chemical additives or reduce enzyme dosage rates, thereby limiting the market's ability to leverage efficiency gains from technological advancements.

Consumer skepticism over GMO-derived enzymes

Mexican consumers demonstrate significant sensitivity to GMO labeling, influenced by civil society campaigns and media coverage of biosafety concerns. Although industrial enzymes undergo purification processes that remove microbial biomass and genetic material, leaving only the catalytic protein, skepticism persists. This concern is particularly evident in premium retail channels and organic product lines, where processors prefer plant-derived enzymes such as papain, bromelain, and ficin to avoid GMO labeling, despite higher costs and the supply-chain variability associated with tropical agriculture. The Mexican biosafety law mandates GMO labeling for products containing detectable modified DNA or protein. However, it exempts processing aids like enzymes that are removed or inactivated during manufacturing, creating regulatory ambiguity. To address this, processors often adopt precautionary labeling or source non-GMO microbial strains. The divide between industrial acceptance of GMO-derived enzymes and consumer skepticism in retail channels restricts market growth. Processors are unable to fully capitalize on the cost benefits of recombinant enzyme platforms in consumer-facing categories, limiting volume growth. Additionally, suppliers are compelled to maintain dual production streams, increasing complexity and operational costs.

Segment Analysis

By Source: Microbial Dominance Meets Plant-Based Momentum

Precision fermentation platforms are achieving recombinant enzyme titers of 15,435 units per milliliter for alkaline protease and 42,367 units per liter for β-galactosidase, highlighting the scalability of microbial production, which accounted for 58.68% of the market share in 2025. Microbial enzymes provide batch-to-batch consistency, cost efficiency, and the flexibility to engineer substrate specificity through strain selection, making them the preferred option for high-volume applications in the bakery, dairy, and brewing industries. The scalability of microbial enzymes ensures their dominance in industrial applications, where efficiency and reliability are critical.

Plant-derived enzymes, such as papain from papaya, bromelain from pineapple, and ficin from fig, are growing at a compound annual growth rate (CAGR) of 8.75%. This growth is driven by clean-label positioning and non-GMO claims, which appeal to premium retail channels and export markets where processors aim to avoid GMO declarations. However, plant enzymes face supply chain challenges linked to tropical agriculture, including weather disruptions, pest infestations, and competing food-grade demand for papaya and pineapple. These factors contribute to pricing instability, complicating long-term procurement agreements. The balance between microbial scalability and plant-based marketing appeal is expected to sustain dual sourcing strategies through 2031, with enzyme suppliers maintaining production capacity for both platforms to meet diverse customer needs.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Type: Carbohydrases Lead, Proteases Accelerate

Carbohydrases accounted for 36.45% of the type segment in 2025, driven by applications such as amylases, which convert starch into fermentable sugars in brewing and baking; xylanases, which enhance water absorption and dough extensibility; and glucose oxidase, which strengthens gluten networks and extends shelf life. Lipases contribute to flavor development in dairy and bakery products through controlled lipolysis, while oxidoreductases, including glucose oxidase and laccase, improve dough strength and prevent enzymatic browning in fruit processing. The "Others" category, which includes pectinase and cellulase, addresses niche applications such as juice clarification and wine production. Pectinases break down pectin to improve yield and clarity, while cellulases degrade cellulose to enhance extraction efficiency.

Proteolytic enzymes are expanding at an 8.59% CAGR, driven by applications in meat tenderization, lactose-free dairy (where proteases hydrolyze casein to improve digestibility), brewing (gluten modification for haze reduction), and cheese making (accelerated ripening and flavor development). The type segmentation highlights the technical maturity of carbohydrase applications, which are now standard in industrial bakery formulations, compared to the growth potential of proteases in emerging categories such as plant-based dairy and functional meat products. Enzyme suppliers are increasingly investing in multi-enzyme blends that combine carbohydrases, proteases, and lipases to provide synergistic functionality. While this trend complicates regulatory approvals, it offers processors single-SKU solutions that simplify inventory management and dosing processes.

By Application: Bakery Scale Versus Beverage Velocity

Bakery applications accounted for a 21.35% market share in 2025, as companies increasingly replace chemical dough conditioners with enzymes such as amylases, xylanases, and glucose oxidase to maintain product volume, texture, and shelf life. Cookies, biscuits, and bread dominate the use of bakery enzymes, which enable fat reduction, crumb softness, and anti-staling properties, thereby extending distribution reach. Beverages are projected to grow at a CAGR of 9.48%, driven by applications in lactose-free dairy, juice clarification, and brewing. Enzymes like β-galactosidase, pectinases, and amylases enhance yield, clarity, and fermentation efficiency in these processes. The lactose-free dairy segment is expanding significantly, as lactose intolerance affects nearly 50% of the population in Mexico, creating sustained demand for lactase enzymes that convert lactose into glucose and galactose without altering taste or texture.

Confectionery applications utilize lipases for flavor development and texture modification, while dairy products such as cheese and yogurt employ proteases and transglutaminase to accelerate ripening and improve texture. In cereal, grain, and starch processing, amylases are used for modified starch production and glucose syrup manufacturing. Oils and fats applications rely on lipases for interesterification and flavor enhancement. The "Other Applications" category includes niche uses such as fruit processing, wine production, and functional food formulation. The application segmentation highlights a market in transition: while bakery remains the primary volume driver, beverages, dairy, and meat are experiencing faster growth as processors increasingly adopt enzymes to address challenges like lactose intolerance, protein cost pressures, and clean-label requirements that cannot be met with chemical alternatives.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The enzyme market in Mexico is primarily concentrated in the Bajío region (Guanajuato, Querétaro, Jalisco) and the central corridor (Mexico City, Toluca, Puebla). These regions are home to major processing facilities operated by Grupo Bimbo, Gruma, and Sigma Alimentos, which account for a substantial portion of enzyme consumption. The Bajío region, in particular, benefits from its proximity to agricultural raw materials and well-developed logistics infrastructure, making it a strategic location for enzyme-dependent industries. These facilities prioritize compliance with international standards, including clean-label requirements and allergen-avoidance mandates, driving enzyme adoption at rates exceeding domestic market averages.

COFEPRIS regulations are applied consistently across Mexico; however, enforcement intensity varies by region. Processors in metropolitan areas face more frequent inspections and stricter compliance audits compared to those in rural locations, leading to regional differences in enzyme adoption rates. For instance, facilities in urban centers often invest in advanced quality control systems to meet regulatory expectations, while rural processors may adopt enzymes more gradually due to less stringent oversight. Additionally, energy costs differ across regions, with electricity rates in Baja California being 10-15% higher than in Jalisco due to transmission constraints. This affects the economics of fermentation-based enzyme production and influences site-selection decisions for multinational suppliers considering local manufacturing operations. Higher energy costs in certain regions may prompt suppliers to explore alternative energy sources or optimize production processes to mitigate expenses.

The geographic concentration of enzyme demand around major food-processing hubs provides distribution efficiencies for suppliers but also increases vulnerability to regional disruptions. Natural disasters, labor disputes, or infrastructure failures in the Bajío or central corridor could disrupt enzyme supply chains, compelling processors to rely on imported alternatives with longer lead times and higher costs. For example, a significant disruption in the Bajío region could impact the operations of Grupo Bimbo or Gruma, leading to cascading effects on enzyme demand and supply. Suppliers may need to develop contingency plans, such as diversifying distribution networks or maintaining buffer stocks, to mitigate the risks associated with such disruptions.

Competitive Landscape

The Mexico Food Enzymes Market is highly concentrated, with Novonesis (formed from the January 2024 merger of Novozymes and Chr. Hansen), DSM-Firmenich, and IFF holding a significant market share. This dominance is supported by their established regulatory dossiers, technical service networks, and long-term supply agreements. These factors have enabled these companies to maintain a strong foothold in the market.

White-space opportunities exist in enzymatic solutions for sugar reduction in confectionery, protein modification for plant-based meat analogs, and prebiotic generation (galacto-oligosaccharides, fructo-oligosaccharides) in functional beverages. Processors in these areas are willing to co-develop formulations and share technical risks, creating potential for innovation and collaboration. These opportunities highlight the growing demand for tailored enzymatic solutions in emerging applications.

Strategy patterns reveal a shift from transactional enzyme sales toward integrated solutions. Suppliers now offer formulation support, process optimization, and regulatory guidance as bundled services, creating switching costs and strengthening customer relationships. Technology remains a key competitive factor, with investments in strain engineering, fermentation optimization, and downstream purification enabling cost-efficient, application-specific enzymes. In contrast, companies relying on legacy microbial platforms face margin erosion and market share loss in high-growth segments like beverages and functional foods.

Mexico Food Enzymes Industry Leaders

-

Kerry Group PLC

-

Novonesis A/S

-

dsm-firmenich

-

International Flavors & Fragrances (IFF) Inc.

-

El Danes SA de CV

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: IFF announced the opening of a new business hub in Mexico City’s Tecnoparque business complex. This facility consolidates most of its operations to better serve customers across Mexico and Latin America. The hub integrates key segments of the company’s business, Health & Biosciences, Scent, Taste, and Food Ingredients, under one roof. Additionally, the site emphasizes sustainability through the inclusion of green spaces, renewable energy, and responsible resource management.

- September 2024: Corbion expanded its facility in Querétaro, Mexico, with a significant upgrade aimed at increasing production capacity and enhancing customer support for food manufacturers across Mexico, Central America, and Latin America. The upgraded facility includes a new production line, expanded bakery and meat laboratories, and dedicated spaces for product development and testing. These enhancements enable Corbion to provide broader technical support, faster research and development, and more efficient product development services.

- January 2024: Novozymes and Chr. Hansen completed a statutory merger to form Novonesis, a global biosolutions conglomerate. The merger received all necessary regulatory approvals and registrations, creating a worldwide entity with operations across multiple regions, including Latin America and Mexico. The combined entity integrates the research and development, production, and distribution capabilities of both companies to serve the food, beverage, and biosolutions markets with enhanced innovation and global reach.

Mexico Food Enzymes Market Report Scope

The Mexican food enzymes market is segmented by type (carbohydrases, proteases, lipases, and other types) and application (bakery, confectionery, dairy and frozen desserts, meat poultry and seafood products, beverages, and other applications.

By Soure

| Animal |

| Plant |

| Microbial |

By Type

| Carbohydrases |

| Proteolytic Enzymes |

| Lipases |

| Oxidoreductases |

| Others (Pectinase, Cellulase, etc.) |

Application

| Bakery | Cookies and Biscuits |

| Bread | |

| Others | |

| Confectionery | |

| Beverages | |

| Dairy Products | |

| Meat Seafood and Poultry Products | |

| Cereal, Grain and Starch Processing | |

| Oils and Fats | |

| Other Applications |

| By Soure | Animal | |

| Plant | ||

| Microbial | ||

| By Type | Carbohydrases | |

| Proteolytic Enzymes | ||

| Lipases | ||

| Oxidoreductases | ||

| Others (Pectinase, Cellulase, etc.) | ||

| Application | Bakery | Cookies and Biscuits |

| Bread | ||

| Others | ||

| Confectionery | ||

| Beverages | ||

| Dairy Products | ||

| Meat Seafood and Poultry Products | ||

| Cereal, Grain and Starch Processing | ||

| Oils and Fats | ||

| Other Applications | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Mexico food enzymes market?

The market reached USD 160.25 million in 2026 and is projected to reach USD 228.76 million by 2031.

Which segment holds the largest market share?

Bakery applications led with 21.35% of revenue in 2025.

Which enzyme type is growing the fastest?

Proteolytic enzymes are forecast to rise at an 8.59% CAGR through 2031.

How strict is Mexican regulation for food enzymes?

COFEPRIS requires detailed dossiers and often extends reviews beyond the nominal five-day period, favoring suppliers with strong regulatory capabilities.