Market Overview

| Study Period | 2021 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

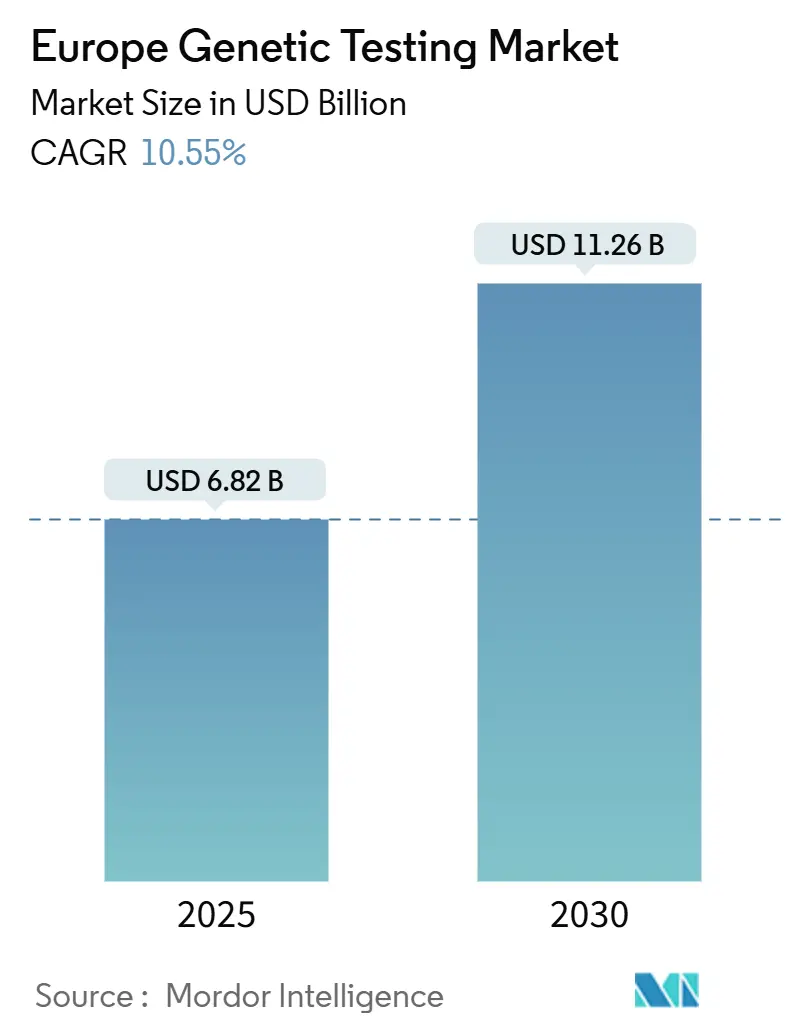

| Market Size (2025) | USD 6.82 Billion |

| Market Size (2030) | USD 11.26 Billion |

| Growth Rate (2025 - 2030) | 10.55% CAGR |

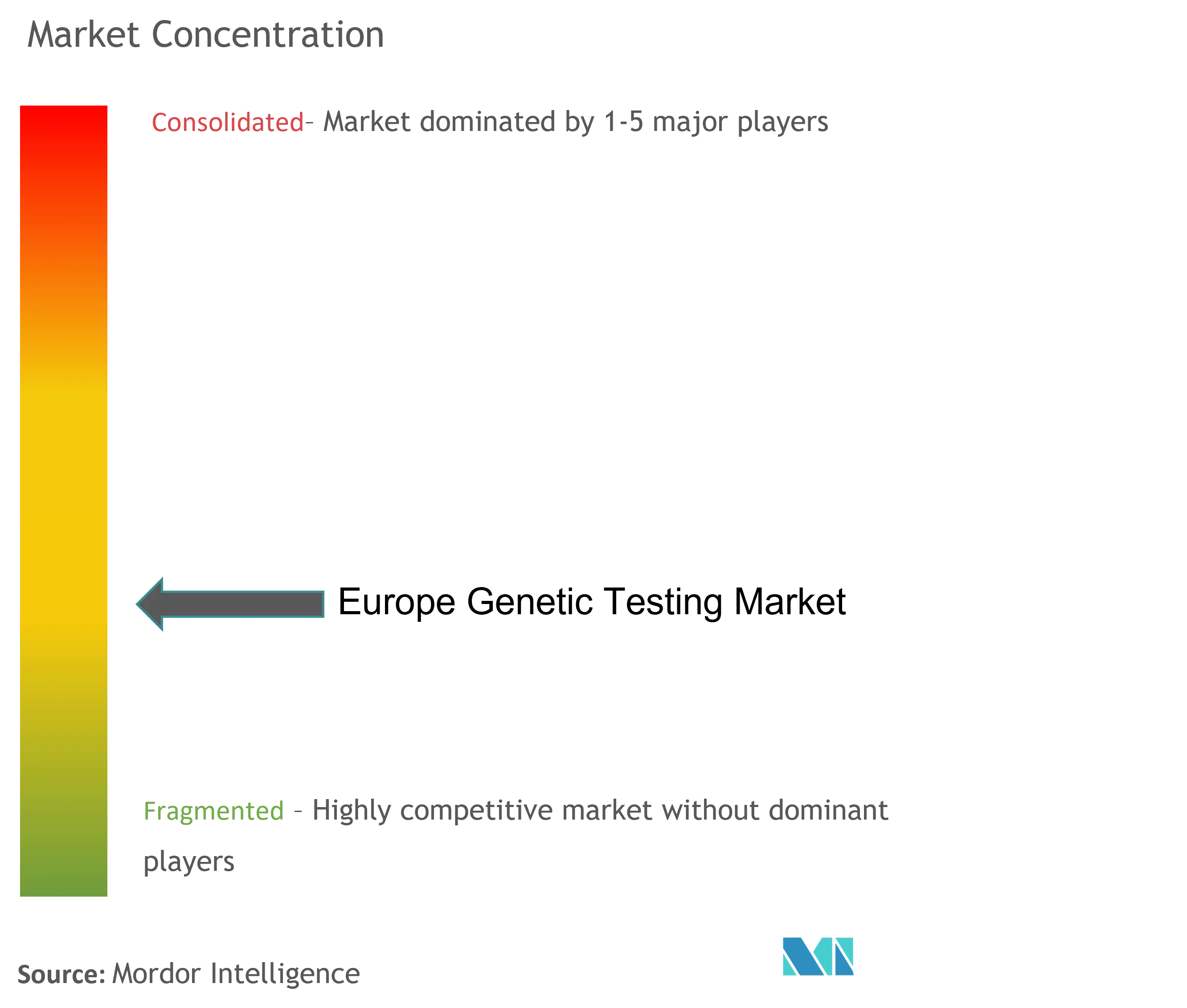

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Genetic Testing Market Analysis by Mordor Intelligence

The Europe genetic testing market size is USD 6.82 billion in 2025 and is forecast to reach USD 11.26 billion by 2030, advancing at a 10.55% CAGR through the period. Robust growth reflects the continent’s cohesive precision-medicine policies under the EU In Vitro Diagnostic Regulation (IVDR), sharp declines in sequencing costs, and expanded newborn as well as population-level genomic screening programs. Tumor profiling, hereditary-cancer testing, and direct-to-consumer wellness kits underpin demand as hospitals embed molecular diagnostics into oncology, rare-disease, and pharmacogenomics pathways. Meanwhile, IVDR-driven quality requirements and the region’s integrated electronic-health-record architecture encourage laboratories to adopt automated next-generation sequencing (NGS) workflows that shorten turnaround times and support same-week clinical decision making. Competition intensifies as platform leaders acquire complementary omics assets, exemplified by Illumina’s USD 350 million purchase of SomaLogic in 2024, while mid-tier laboratories consolidate to meet CE-IVD certification thresholds.

Key Report Takeaways

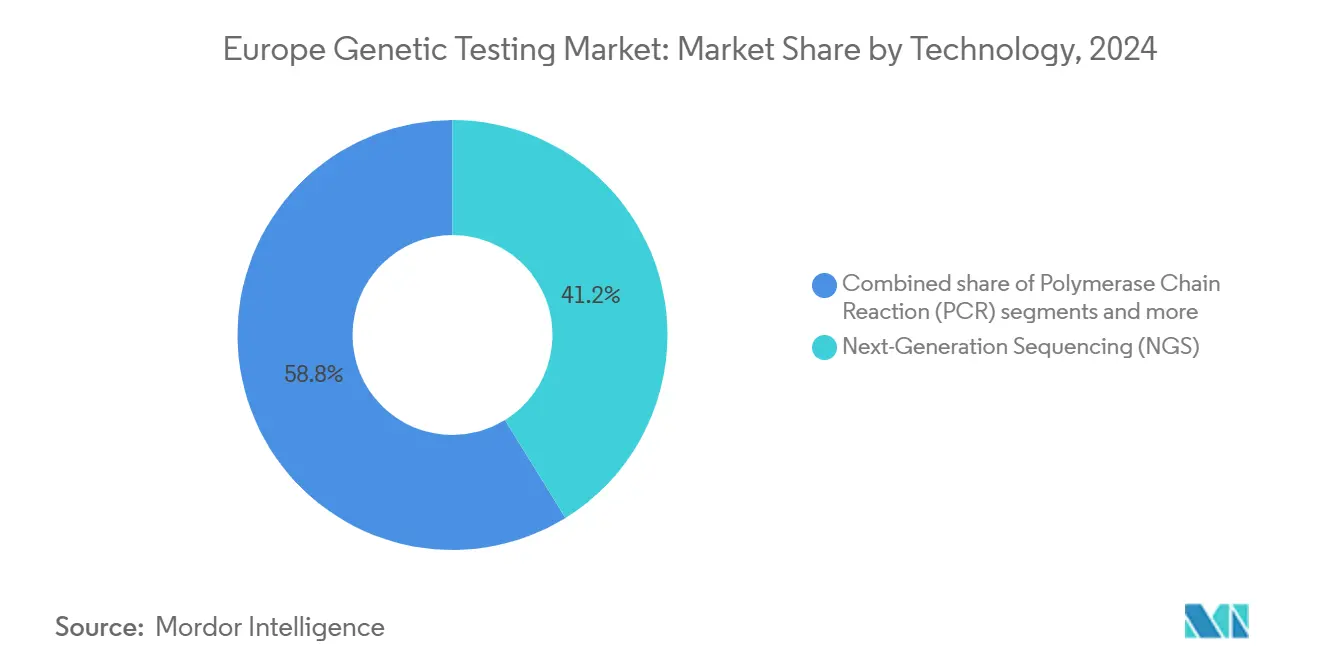

By technology, NGS held 41.20% of Europe genetic testing market share in 2024, whereas PCR platforms are projected to record the fastest 11.02% CAGR to 2030.

By application, cancer diagnosis & prognosis captured 47.89% of Europe genetic testing market size in 2024, while ancestry & wellness testing is anticipated to expand at a 11.21% CAGR between 2025-2030.

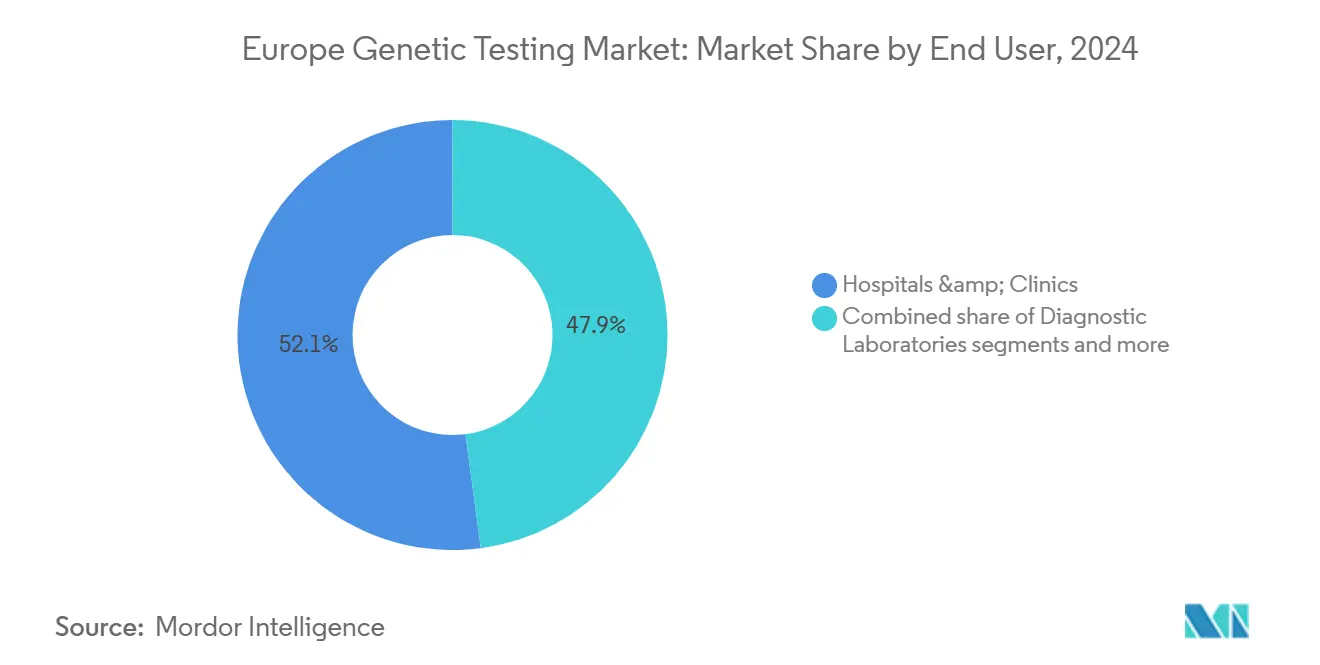

By end user, hospitals & clinics accounted for 52.09% of Europe genetic testing market share in 2024; diagnostic laboratories are set to post the highest 11.78% CAGR through 2030.

By geography, Germany led with a 24.38% contribution to Europe genetic testing market size in 2024, whereas Rest of Europe—anchored by Eastern EU members—will rise at a 11.98% CAGR over the forecast horizon.

Europe Genetic Testing Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of NGS-based comprehensive panels | +2.1% | Germany, UK, France, Nordic countries | Medium term (2-4 years) |

| Expansion of newborn and population genomic screening programs | +1.8% | Belgium, UK, Netherlands, Central Europe | Long term (≥ 4 years) |

| Falling sequencing costs from regional infrastructure investment | +1.4% | Germany, UK, France | Short term (≤ 2 years) |

| Rising prevalence of hereditary cancers boosting BRCA & multigene demand | +1.2% | UK, Germany, France | Medium term (2-4 years) |

| EU IVDR-led shift to high-quality CE-IVD kits | +0.9% | EU-wide, early in Germany & Netherlands | Short term (≤ 2 years) |

| Cross-border tele-genetics outreach in underserved Eastern Europe | +0.7% | Eastern Europe & Baltics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of NGS-Based Comprehensive Panels by European Healthcare Systems

National health systems now reimburse NGS tumor and rare-disease panels, raising diagnostic yields above 40% versus 25% for sequential single-gene tests. Germany’s Molecular Tumor Board network covers comprehensive genomic profiling for advanced cancers, while the UK’s NHS offers free BRCA screening to Jewish women over 30, demonstrating a policy shift toward preventive genomics. Reimbursement clarity pushes laboratories to upgrade capacity, stimulate reagent demand, and invest in cloud-based bioinformatics that integrate directly with electronic clinical records. Device makers respond by launching CE-IVD marked comprehensive assays that bundle tumor mutation burden, microsatellite instability, and gene-fusion profiling in a single test run.

Expansion of Newborn and Population Genomic Screening Programs in EU States

Belgium’s BabyDetect initiative screens newborns for more than 200 disorders—supported by EUR 25 million in federal funds—and delivers results within two weeks, catching treatable metabolic and immunodeficiency syndromes earlier than biochemical panels. The UK’s Newborn Genomes Programme is sequencing 200,000 babies to assess actionable variants that can benefit from early interventions such as enzyme-replacement or dietary modifications. These pilots leverage Screen4Care, a EUR 15 million Horizon Europe grant, to standardize genomic data pipelines across seven member states. Data show a 35% rise in early detection of rare diseases, validating program scalability and reinforcing demand for high-throughput sequencers as well as variant-interpretation software.

Falling Sequencing Costs Due to European Infrastructure Investments

Continuous chemistry upgrades and flow-cell redesigns drove whole-genome sequencing below USD 500 per sample in 2024, halving costs since 2022 and broadening clinical utility for pharmacogenomics, pediatric neurology, and complex oncology cases. The Genome of Europe consortium, funded at EUR 1 billion, pools procurement across public laboratories to negotiate reagent discounts and share high-end fleet capacity, reducing per-run overhead. Genomics England processes hospital samples in under 14 days for below USD 400 through robotic sample prep and AI-assisted variant filtration, setting a cost-performance benchmark adopted by German university centers.

Rising Prevalence of Hereditary Cancers Driving Demand for BRCA & Multigene Tests

Updated European oncology guidelines recommend germline testing for all breast- or ovarian-cancer patients under 50, expanding the test-eligible cohort fourfold compared with 2022. Private labs in the UK price multigene cancer panels between GBP 399 and GBP 1,400 (USD 499–1,750), creating an affordable complement to publicly reimbursed single-gene tests. France’s 2025-initiated National Cancer Plan earmarked EUR 50 million to fund family cascade testing, which identifies actionable mutations in 12–15% of relatives versus 5–8% for BRCA-only screening. Resulting demand stimulates counseling and tele-oncology service expansion, while laboratories integrate reflex RNA-based fusion assays to maximize actionable findings from the same biopsy sample.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Delays in reimbursement approvals across national health insurers | -1.3% | Southern Europe, Eastern Europe, with particular challenges in Italy, Spain | Medium term (2-4 years) |

| Shortage of certified genetic counselors limiting test uptake | -0.8% | EU-wide, with acute shortages in Eastern Europe, rural areas | Long term (≥ 4 years) |

| Data sovereignty rules complicating pan-European genomic data sharing | -0.6% | EU-wide, with cross-border implications for Germany, Austria, Netherlands | Medium term (2-4 years) |

| Scarcity of validated polygenic risk scores for non-European ancestries in Europe's migrant populations | -0.4% | Western Europe urban centers, particularly Germany, France, UK | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Delays in Reimbursement Approvals Across National Health Insurers

Italian providers wait 18–24 months for genetic‐test reimbursement decisions, triple the time required in Germany or the Netherlands, undermining equitable access and slowing revenue realization for innovators. Spain’s autonomous regions each apply divergent coverage criteria, prompting laboratories to navigate 17 distinct approval pathways. The 2024 joint EU Health Technology Assessment Regulation aims to harmonize requirements, but transitional overlap with IVDR doubles dossier workload and prolongs market entry timelines for pharmacogenomics and broad tumor panels. Providers frequently rely on private payment or research grants, dampening volume growth and constraining economies of scale.

Shortage of Certified Genetic Counselors Limiting Test Uptake

Europe requires 4,000 additional certified genetic counselors to meet existing caseloads, yet universities graduate fewer than 200 annually, leaving hospitals to adopt “mainstreaming” models that train oncologists and cardiologists to provide limited counseling. The UK employs about 400 counselors for 67 million citizens—well below the recommended ratio of 1 per 100,000—forcing reliance on tele-genetics and group counseling sessions. Eastern Europe faces acute shortages, where cross-border clinics in Vienna and Berlin supply virtual consultations for Baltic and Balkan patients. Prolonged wait times for pre- and post-test counseling discourage physician referrals, particularly for complex prenatal or oncology panels that demand nuanced risk communication.

Segment Analysis

By Technology: NGS Dominates Clinical Adoption

NGS commanded 41.20% of Europe genetic testing market share in 2024, reflecting its cost-efficient multigene capability and entrenched role in oncology and rare-disease diagnostics. PCR platforms trail yet post the segment’s fastest 11.02% CAGR as hospitals deploy real-time kits for neonatal sepsis and pharmacogenomics where same-day decisions are critical.

Hospital laboratories standardize workflows around dual-platform strategies that leverage NGS for comprehensive insights and PCR for urgent triage, enabling continuity of operations during instrument maintenance windows. EU IVDR compliance favors vendors with integrated quality-management documentation, prompting smaller kit manufacturers to partner with multinational distributors. As throughput increases, reagent-rental contracts lower upfront costs, supporting wider adoption among mid-size pathology networks.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Cancer Leads, Wellness Accelerates

Oncology accounted for 47.89% of Europe genetic testing market size in 2024 as molecular tumor boards embedded profiling into every advanced-cancer case, unlocking targeted-therapy reimbursements. Conversely, ancestry & wellness use cases climb fastest at 11.21% CAGR, propelled by social-media-driven consumer demand for lifestyle insights.

Diagnostic labs expand somatic-plus-germline combo tests that inform both therapy and familial risk, boosting panel average selling prices. Direct-to-consumer firms localize websites in 23 EU languages and partner with pharmacies for sample logistics, mitigating regulatory scrutiny over cross-border data transfers. Wellness kits increasingly upsell pharmacogenomic add-ons that convert casual users into repeat purchasers through app-based medication dashboards.

By End User: Hospitals Anchor, Labs Accelerate

Hospitals & clinics captured 52.09% of Europe genetic testing market share in 2024 thanks to embedded precision-oncology and neonatal screening services. Diagnostic laboratories, however, will grow fastest at 11.78% CAGR as payers push outpatient models and specialists outsource complex bioinformatics.

University hospitals build hub-and-spoke models in which regional clinics send samples centrally, ensuring uniform variant interpretation. Commercial labs differentiate through 48-hour panel turnaround and AI-powered reports that flag clinical-trial eligibility, enticing oncologists seeking real-time therapeutic pathways. Remote counseling platforms integrate lab portals with certified genetic counselors in under-served geographies, expanding patient reach while reducing referral leakage.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Germany contributed 24.38% of Europe genetic testing market size in 2024 by virtue of universal health-insurance reimbursement for tumor and pharmacogenomic panels and a dense network of academic genomics centers. The United Kingdom remains pivotal, leveraging the NHS Genomic Medicine Service’s single-payer purchasing power to standardize test menus and volume-based discounts. France follows through a EUR 670 million national strategy that builds 30 sequencing hubs linked to secure cloud analytics, accelerating rare-disease case resolutions from 22 to 12 months.

Italy and Spain show improving uptake yet continue to face fragmented reimbursement, prompting patients to seek private tests or cross-border referrals. Eastern European markets—Bulgaria, Romania, Poland, and the Baltics—post the fastest 11.98% CAGR as EU structural funds finance infrastructure and tele-genetics bridges supply shortages. Vienna’s Medical University, for example, supports variant interpretation for Balkan oncology centers via encrypted cloud pipelines, evidencing collaborative momentum. Harmonized GDPR protocols ease cross-border data exchange, enhancing multinational research consortia that accelerate variant re-classification and clinical guideline updates.

Competitive Landscape

The arena remains moderately fragmented: Illumina, Roche, and Quest Diagnostics anchor high-throughput sequencing and distribution, while Centogene, Eurofins Scientific, and Oxford Nanopore supply region-specific assays and long-read platforms. Consolidation is gaining pace; Eurofins’ EUR 120 million acquisition of SYNLAB Spain added 15 labs and doubled Iberian capacity, whereas Labcorp partnered with SYNLAB to broaden reach in Central and Eastern Europe.

Technology differentiation centers on AI-assisted interpretation and multi-omics capability. Oxford Nanopore invested EUR 50 million in German manufacturing to localize supply and comply with IVDR batch-release documentation. Emerging entrants leverage tele-counseling and direct-to-consumer storefronts but must overcome rising compliance costs that favor well-capitalized players. Patent filings for bioinformatics algorithms at the European Patent Office surged 23% in 2024, signaling intensifying innovation races around variant-classification and polygenic-risk scoring.

Europe Genetic Testing Industry Leaders

-

Abbott Laboratories

-

Illumina Inc.

-

23andMe Inc.

-

Qiagen

-

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Illumina finalized a USD 350 million acquisition of SomaLogic to integrate high-plex proteomics with oncology and inherited-disease panels across European labs

- April 2024: Eurofins bought SYNLAB’s Spanish labs for EUR 120 million to strengthen Iberian diagnostic coverage

Europe Genetic Testing Market Report Scope

As per the scope of this report, genetic testing is a test performed to identify the presence of a particular gene/s with a particular sequence of the genome. The gene/s can be identified either directly through sequencing or indirectly through various methods.

The European Genetic Testing market is segmented by type (carrier testing, diagnostic testing, newborn screening, predictive and presymptomatic testing, prenatal testing, other types), by disease (Alzheimer's disease, cancer, cystic fibrosis, sickle cell anemia, Duchenne muscular dystrophy, thalassemia, Huntington's disease, other diseases), by technology (cytogenetic testing, biochemical testing, and molecular testing), and geography (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe).

The report offers the value (in USD million) for the above segments.

By Technology (Value)

| Next-Generation Sequencing (NGS) |

| Polymerase Chain Reaction (PCR) |

| Microarray |

| Fluorescence In Situ Hybridization (FISH) |

| Sanger Sequencing |

| Other Technologies |

By Application (Value)

| Cancer Diagnosis & Prognosis |

| Cardiovascular Disease Diagnosis |

| Neurological Disorder Diagnosis |

| Ancestry & Wellness |

| Other Applications |

By End User (Value)

| Hospitals & Clinics |

| Diagnostic Laboratories |

| Academic & Research Institutes |

| Direct-to-Consumer Companies |

| Other End Users |

Europe

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Technology (Value) | Next-Generation Sequencing (NGS) |

| Polymerase Chain Reaction (PCR) | |

| Microarray | |

| Fluorescence In Situ Hybridization (FISH) | |

| Sanger Sequencing | |

| Other Technologies | |

| By Application (Value) | Cancer Diagnosis & Prognosis |

| Cardiovascular Disease Diagnosis | |

| Neurological Disorder Diagnosis | |

| Ancestry & Wellness | |

| Other Applications | |

| By End User (Value) | Hospitals & Clinics |

| Diagnostic Laboratories | |

| Academic & Research Institutes | |

| Direct-to-Consumer Companies | |

| Other End Users | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Europe genetic testing market in 2025?

The market is valued at USD 6.82 billion in 2025 with a forecast 10.55% CAGR to 2030.

Which technology leads clinical adoption across Europe?

Next-generation sequencing holds 41.20% share, firmly anchoring complex oncology and rare-disease diagnostics.

Why is Germany the largest national contributor?

Germany's universal reimbursement, academic genomics hubs, and Molecular Tumor?Board network secure a 24.38% share of regional revenues.

What hampers faster expansion in Southern Europe?

Lengthy reimbursement approvals18-24 months in Italy and similar delays in Spain slow public adoption of new tests.

How are newborn screening programs evolving?

Initiatives like Belgium's BabyDetect and the UK's Newborn Genomes Programme add whole-genome sequencing to traditional panels, improving early rare-disease detection by 35%.

Which segment shows the fastest future growth?

Direct-to-consumer ancestry & wellness testing is projected to rise at a 6.21% CAGR as consumers embrace personalized health insights.

Page last updated on: