Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

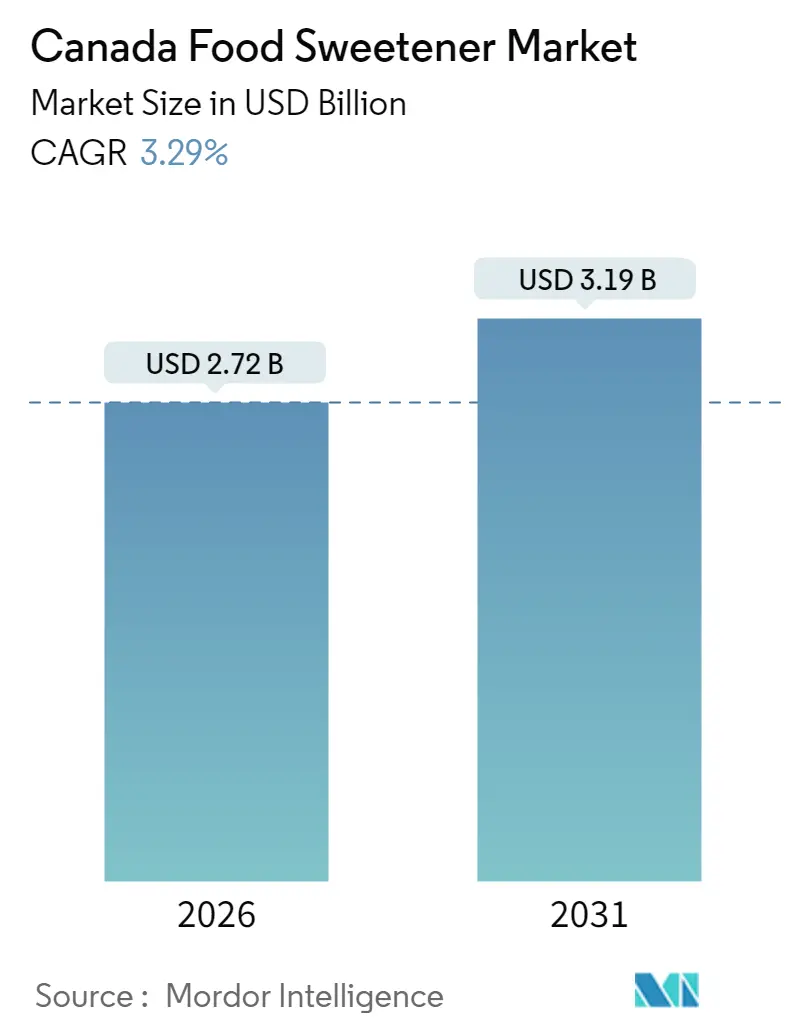

| Market Size (2026) | USD 2.72 Billion |

| Market Size (2031) | USD 3.19 Billion |

| Growth Rate (2026 - 2031) | 3.29% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canada Food Sweetener Market Analysis by Mordor Intelligence

Canada food sweeteners market size in 2026 is estimated at USD 2.72 billion, growing from 2025 value of USD 2.63 billion with 2031 projections showing USD 3.19 billion, growing at 3.29% CAGR over 2026-2031. The market demonstrates maturity while experiencing a fundamental shift toward healthier sweetening alternatives, influenced by increasingly strict regulatory requirements and evolving consumer preferences for natural and low-calorie options. Canada's robust food processing sector, which maintains its position as the country's second-largest manufacturing industry, provides essential market stability through established distribution networks and production capabilities. Additionally, government initiatives support this sector. Under the Sustainable Canadian Agriculture Partnership (Sustainable CAP), the Canadian and Manitoba governments are investing in major capital infrastructure projects to expand food processing capacity in Manitoba. These investments aim to enhance the competitiveness of the food processing industry, create job opportunities, and support sustainable agricultural practices, ensuring long-term growth and resilience in the sector. [1]Annex Business Media, "Canada and Manitoba invest $15.4M to modernize food processing facilities", www.mromagazine.com

Key Report Takeaways

- By region, Central Canada held 74.62% share of the Canada sweeteners market in 2025 and is forecast to expand at 4.36% CAGR through 2031.

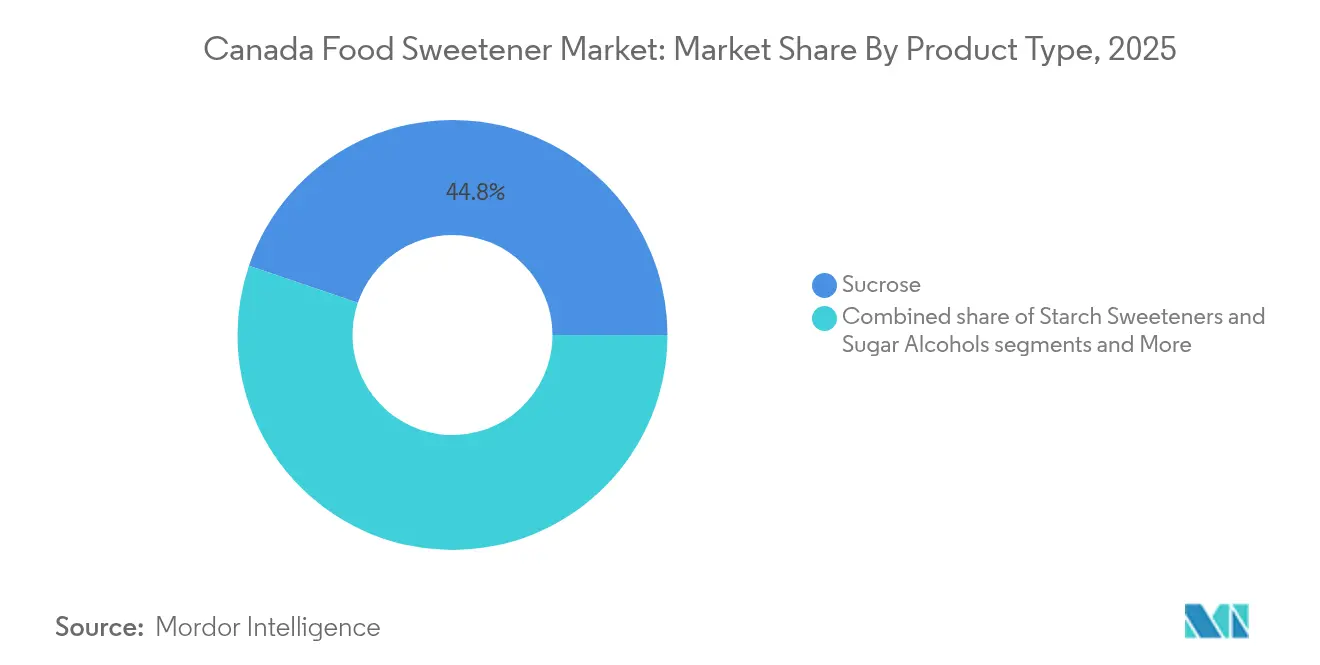

- By product type, sucrose led with a 44.78% revenue share in 2025; high-intensity sweeteners will grow at a 4.98% CAGR to 2031.

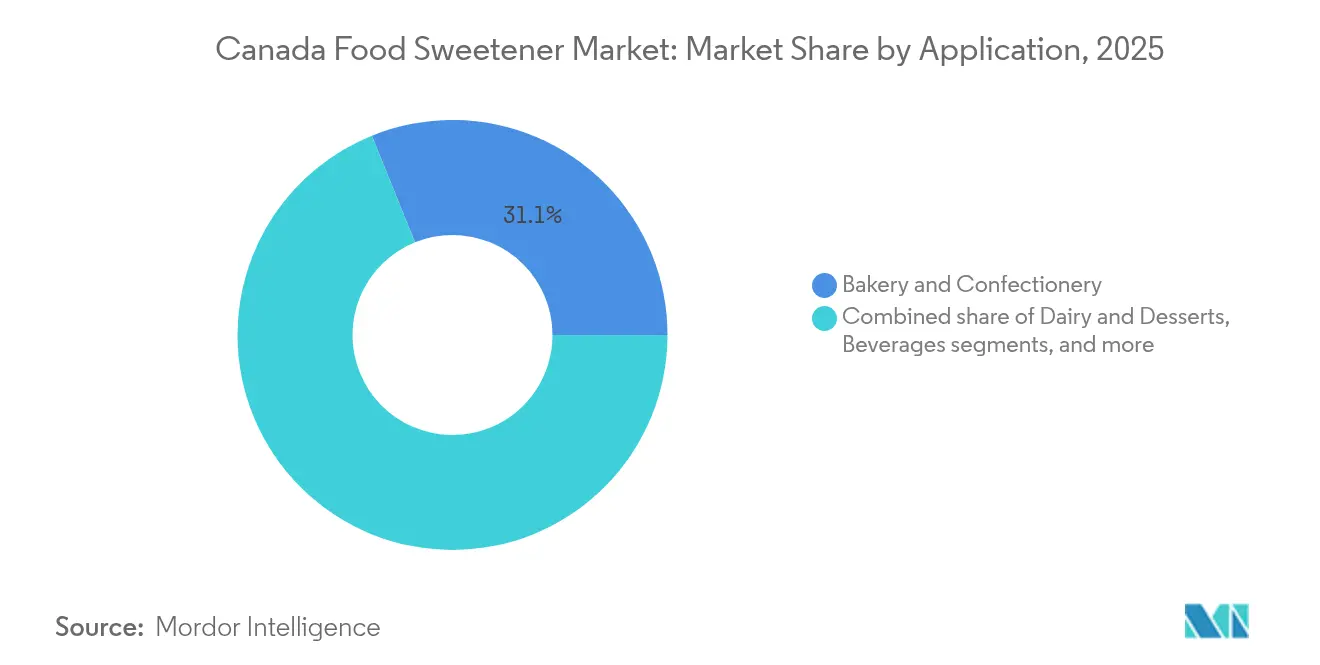

- By application, bakery and confectionery accounted for a 31.12% revenue share in 2025, while the beverages segment will expand at a 4.52% CAGR.

- By form, powder captured 56.05% market share in 2025; liquid is set for 4.66% CAGR.

- By category, conventional products held 92.05% market share in 2025; organic will grow at 4.72% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Food Sweetener Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of obesity and diabetes | +0.8% | National, with higher concentration in urban centers | Medium term (2-4 years) |

| Consumer preference for natural and plant-based sweeteners | +0.7% | National, with premium adoption in Central Canada | Long term (≥ 4 years) |

| Regulatory expansion of permitted natural sweeteners | +0.5% | National regulatory framework | Short term (≤ 2 years) |

| Strong presence of domestic maple syrup and honey producers | +0.4% | Quebec and Eastern provinces primarily | Long term (≥ 4 years) |

| Innovation in blends and flavor optimization | +0.6% | National, with R&D centers in Central Canada | Medium term (2-4 years) |

| Health-driven shift to low/no-calorie sweeteners | +0.9% | National, with urban market leadership | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Obesity and Diabetes

In 2024, approximately 3.8 million Canadians had diabetes, while obesity rates increased across all age groups. [2]Government of Canada, "Diabetes in Canada,"canada.ca. The focus on preventive nutrition by employers and provincial health systems has led food brands to reduce sugar content substantially while maintaining familiar tastes. The introduction of GLP-1 weight-loss medications has increased consumer awareness of added sugars, leading to greater use of high-intensity sweeteners in snacks and beverages. Food manufacturers are using advanced blending techniques and flavor-masking technologies to achieve considerable calorie reductions while preserving product texture. Food processors are implementing early reformulation strategies to gain competitive advantages in domestic and export markets, preparing for anticipated regulations on school meals and front-of-pack labeling regarding added sugar content. The industry's commitment to sugar reduction reflects broader health initiatives, with companies investing in innovative solutions to meet evolving consumer preferences and regulatory requirements while ensuring product quality and taste satisfaction.

Consumer Preference for Natural and Plant-based Sweeteners

Consumer preferences are shifting toward natural sweetening solutions, driven by concerns about food processing and ingredient transparency. A significant portion of consumers now prioritize sweetener types in their food and beverage purchases. The shift toward alternative sweeteners has driven innovation in plant-based solutions. In June 2025, Elo Life Sciences developed watermelons that produce mogrosides, delivering monk fruit sweetness at higher potency levels through agricultural techniques. The sweetener industry has expanded to include functional properties, as demonstrated by tagatose becoming the first sweetener to receive NutraStrong™ Prebiotic Verified certification, which combines sugar reduction with gut health advantages.

Regulatory Expansion of Permitted Natural Sweeteners

Health Canada's regulatory framework enables market access for new sweetening solutions through streamlined approval processes. The agency approved monk fruit extract under the Food and Drug Act and expanded permissions for stevia-based formulations across food categories. Regulatory amendments in December 2024 simplified food additive approval processes while maintaining safety standards, creating defined pathways for new sweeteners to enter the Canadian market. The framework permits innovative products such as Glyvia™, a Health Canada-approved plant-based sweetener that combines glycosides and amino acids. This sweetener supports blood sugar metabolism without a bitter aftertaste. Health Canada's less restrictive regulatory approach compared to other markets makes Canada favorable for sweetener innovation and product development. The agency's updates to permitted preservatives and supplemental ingredients demonstrate its focus on evidence-based regulations that balance innovation with consumer safety.

Strong Presence of Domestic Maple Syrup and Honey Producers

Canada's dominance in maple syrup production, accounting for over 73% of global supply with 19.9 million gallons harvested in 2024, creates unique competitive advantages in the natural sweeteners segment that extend far beyond commodity pricing. The ~91% production increase in 2024, driven by favorable weather conditions and expanded tapping operations, demonstrates the sector's capacity for rapid scaling while maintaining quality standards [3]Statistics Canada, "Maple product," statcan.gc.ca. Quebec's maple syrup industry manages its supply chain through the strategic reserve system and the Maple Syrup Producers Association's production capacity expansion, as of March 2025. This infrastructure enables the industry to meet market demand while maintaining stable prices. Canadian companies have integrated vertically into value-added processing, developing diverse maple-based sweetener blends and concentrated formulations for industrial applications, strengthening their position in the global market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer skepticism toward artificial sweeteners | -0.4% | National, with higher resistance in rural areas | Medium term (2-4 years) |

| Higher costs and price sensitivity for natural sweeteners | -0.6% | National, with acute impact on price-sensitive segments | Short term (≤ 2 years) |

| Taste and aftertaste issues with some sweeteners | -0.3% | National consumer acceptance challenges | Medium term (2-4 years) |

| Formulation challenges in dairy and confectionery applications | -0.2% | Central Canada manufacturing centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consumer Skepticism Toward Artificial Sweeteners

Traditional food preferences and concerns about processed ingredients limit the adoption of synthetic alternatives, particularly among older demographics and rural populations. Food service operators and retailers have adjusted their purchasing decisions in response to demands for products with transparent ingredient lists. Health Canada's proposal in May 2024 to remove brominated vegetable oil from permitted food additives due to safety concerns has intensified consumer skepticism about the long-term safety of regulatory-approved ingredients. This market environment creates opportunities for natural sweetener alternatives while constraining overall market growth as manufacturers adapt their formulations to meet consumer preferences within regulatory requirements.

Higher Costs and Price Sensitivity for Natural Sweeteners

The high cost of natural sweeteners limits their widespread adoption, especially in price-sensitive food categories where consumers prioritize cost over health benefits. Natural high-intensity sweeteners, such as stevia and monk fruit, cost several times more than conventional sugar per unit, creating challenges for manufacturers who aim to maintain competitive pricing while offering clean-label products. Organic-certified sweeteners command substantial premiums over conventional natural alternatives, restricting their use primarily to premium product segments where consumers demonstrate greater willingness to pay for perceived quality and health benefits. Canadian food manufacturers face additional pressure from U.S. competition, where different regulatory frameworks and supply chain structures can create cost advantages for imported products. The challenge is compounded by volatility in raw material pricing, exemplified by cocoa and sugar price fluctuations that tighten margins for sweet product manufacturers and reduce willingness to invest in premium sweetening solutions [4]Farm Credit Canada, "Bakery and tortilla products: 2024,"fcc-fac.ca. Price sensitivity is creating market segmentation, where premium brands can command higher prices for natural sweetener formulations while mass market products remain constrained by conventional sweetening economics.

Segment Analysis

By Product Type: High-Intensity Solutions Accelerate Reformulation

High-intensity sweeteners are projected to grow at a CAGR of 4.98%, while sucrose holds a 44.78% market share in 2025. The Canadian sweeteners market is experiencing increased adoption of high-intensity formats as beverage and functional food manufacturers reduce bulk sugar content to lower calorie counts. Starch-based syrups and polyols fulfill intermediate functionality requirements by providing bulk and moisture retention in bakery products. The emerging innovation segment includes rare sugars and sweet proteins such as tagatose, allulose, and brazzein, which offer metabolic health benefits alongside favorable taste profiles.

Sucrose maintains its market leadership due to established infrastructure and cost advantages, particularly in export-oriented bakery production. The category continues to evolve through co-crystallization with stevia and the incorporation of flavor modulators, enabling 20-30% usage reduction without processing modifications. In confectionery applications, sugar alcohol combinations of erythritol, soluble fiber, and monk fruit enhance digestive tolerance. Ingredient manufacturers now offer complete blend solutions that replicate sucrose's sweetness profile, increasing consumer acceptance and enabling faster reformulation for mid-tier brands.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Form: Liquid Sweeteners Gain Processing Advantages

The powder segment maintains its market dominance with a 56.05% share, benefiting from stability at room temperature and reduced transportation costs. In the Canada sweeteners market, the crystalline nature of powder sweeteners enables their integration into premix applications across bakery, confectionery, and seasoning segments. Liquid sweeteners are projected to grow at a CAGR of 4.66% through 2031, driven by beverage manufacturers' requirements for quick dissolution and inline dosing capabilities. Manufacturers increasingly adopt high-solids syrups and concentrated stevia solutions to enhance batching efficiency.

Crystal-form sweeteners remain essential in retail sachets and food-service tabletop segments where consumers prefer familiar formats. The market sees growth in hybrid encapsulation technology, which combines powder stability with liquid-like dissolution properties, enabling controlled flavor release and moisture resistance in snack applications. Beverage manufacturing facilities now incorporate flow meters designed for high-viscosity syrups, optimizing dosage control and managing sugar tax compliance. Manufacturers improve operational efficiency by creating pre-blended combinations of sweeteners with acidulants and flavoring components, reducing production changeover time.

By Application: Beverages Accelerate Zero-Sugar Transition

The bakery and confectionery segment maintains a dominant 31.12% market share, supported by Canada's export-oriented bread and pastry industry. Manufacturers employ composite sweetening systems to comply with U.S. market requirements while maintaining product characteristics such as crumb structure and browning. In dairy products and desserts, manufacturers combine ultra-filtered milk with monk fruit or allulose to maintain sweetness in reduced-sugar yogurts. The soups, sauces, and dressings category requires heat-stable sweeteners during pasteurization, utilizing combinations of stevia and coconut sugar for balanced flavor and minimal color changes.

Beverages constitute the fastest-growing application segment, with a projected CAGR of 4.52% through 2031. This growth is driven by the increasing number of zero-sugar products across carbonated soft drinks, energy drinks, and ready-to-drink coffees. The Canada sweeteners market is adapting to mandatory and voluntary sugar-reduction targets, with manufacturers using allulose, stevia, and rare-sugar proteins to develop taste profiles comparable to full-sugar products. The functional beverage segment combines sweeteners with adaptogens and electrolytes, increasing the demand for high-intensity sweeteners that remain stable in acidic conditions.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Category: Organic Captures Premium Shelf Space

Conventional sweeteners hold a dominant 92.05% market share through price advantages and widespread availability, but face increasing competition in premium beverage and baby food segments. Organic sweeteners are set to grow at a 4.72% CAGR, driven by consumer demand for regenerative agriculture and pesticide-free products. Export demand from the United States, Germany, and France supports organic-certified processors.

The organic segment faces growth constraints from certification requirements and higher raw material costs in price-sensitive categories. Manufacturers address this challenge by combining organic maple or honey with conventional sweeteners to achieve partial clean-label status at manageable costs. Industry participants implement traceability systems to verify supply chain integrity, meeting retailer ESG requirements. The organic price premium is expected to decrease as operations in Quebec expand and achieve economies of scale.

Geography Analysis

Central Canada holds a 74.62% market share and exhibits a 4.36% CAGR, driven by Ontario and Quebec's concentrated food-processing clusters, integrated transportation networks, and skilled workforce. The Canadian sweeteners market gains stability from Rogers Sugar's Hamilton refinery, which aims to produce 1 million metric tons annually, ensuring domestic supply and reducing exposure to global price fluctuations.

Western Canada's sugar-beet production contributes approximately 8% of domestic refined sugar requirements, supporting regional market stability. The Alberta Food Processors Association implements manufacturing improvements that create opportunities for specialized sweeteners targeting Pacific export markets.

Atlantic Canada and Northern territories represent developing market segments, supported by tourism growth, population changes, and local honey production. While logistics expenses remain challenging, e-commerce platforms and third-party cold chain solutions help address distribution gaps. National freight coordination initiatives, including intermodal facilities in Halifax, reduce delivery times for eastward sweetener transportation, enabling smaller processors to expand their production of value-added condiments and confectionery products.

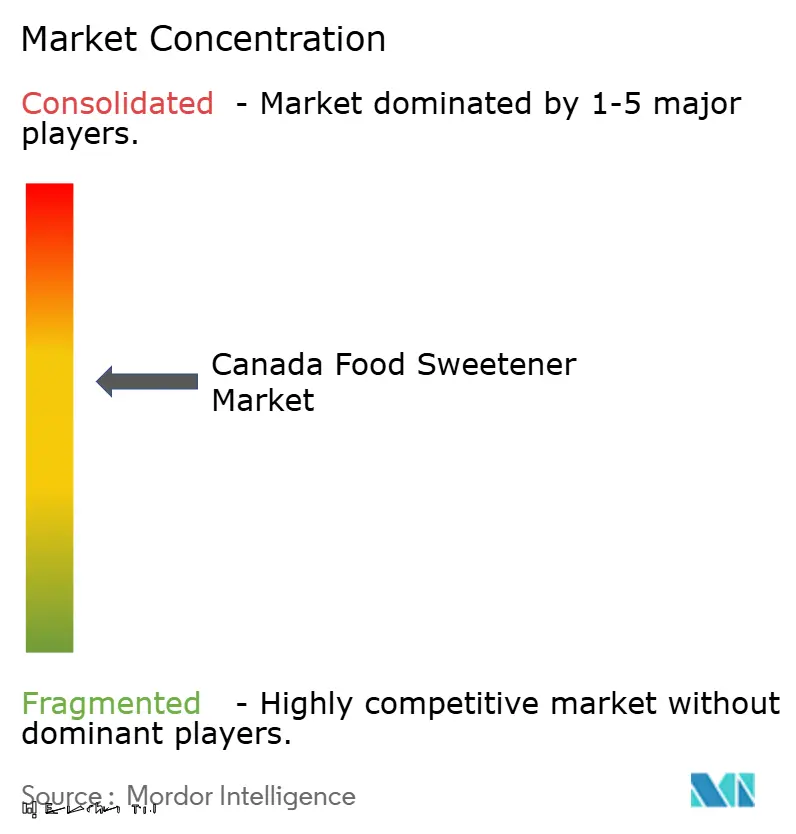

Competitive Landscape

The Canada sweeteners market shows moderate concentration, with competition balanced between established multinational corporations and emerging specialty ingredient companies. Market leaders include Tate & Lyle, Cargill, Rogers Sugar, and Ingredion, each with distinct advantages in global supply chains, processing technologies, and regulatory compliance.

The market's competitive dynamics are intensifying through vertical integration, as demonstrated by Tate & Lyle's acquisition of CP Kelco, which strengthened their capabilities in sweetening, mouthfeel, and fortification solutions. Strategic partnerships, such as the Avansya joint venture between DSM-Firmenich and Cargill, enable companies to combine their expertise in developing fermentation-derived sweeteners and bioconversion technologies.

Companies are differentiating themselves through technology adoption, investing in automation, AI-driven formulation optimization, and precision fermentation for efficient product development and specialized sweetener production. New market entrants are focusing on innovative sweetener categories, including sweet proteins, rare sugars, and botanical synthesis technologies that offer improved sensory characteristics while reducing agricultural dependencies. Growth opportunities exist in functional sweeteners that provide health benefits beyond calorie reduction, and in sustainable production methods that maintain cost efficiency. Recent legal developments, such as SweeGen's victory against PureCircle, are reshaping patent landscapes and potentially reducing entry barriers for innovative sweetener formulations.

Canada Food Sweetener Industry Leaders

-

Tate & Lyle

-

Cargill Inc.

-

Lantic Inc.

-

ADM

-

International Flavors and Fragrances

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2024: Tate & Lyle acquired CP Kelco, a global leader in hydrocolloids and natural ingredients, strengthening its specialty solutions capabilities. The acquisition enhances Tate & Lyle's product portfolio and market presence in the food and beverage industry.

- April 2024: Ingredion introduced PURECIRCLE Clean Taste Solubility Solution (CTSS), a stevia-based sweetener that demonstrates over 100 times higher solubility than Reb M stevia. Consumer panels and sensory testing indicate that CTSS provides superior taste performance compared to artificial sweeteners and other stevia ingredients.

- January 2024: Cargill Inc. and DSM-Firmenich announced that their EverSweet® stevia sweetener received a positive safety assessment from regulatory authorities. The assessment confirms the product's compliance with safety standards and regulations, marking a significant milestone in its market approval process.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Canada food sweetener market as the total annual value of ingredients, sucrose, starch-based sweeteners, and sugar alcohols, plus high-intensity options such as aspartame, sucralose, stevia, and monk fruit sold for use in processed foods and beverages across retail, food-service, and industrial channels.

Scope exclusion: tabletop sachets and bulk sugar sold directly to households are outside this definition.

Segmentation Overview

-

By Product Type

- Sucrose

-

Starch Sweeteners and Sugar Alcohols

- Dextrose

- High Fructose Corn Syrup (HFCS)

- Maltodextrin

- Sorbitol

- Xylitol

- Other Starch Sweeteners and Sugar Alcohols

-

High-Intensity Sweeteners

-

Artificial High-Intensity Sweeteners

- Sucralose

- Aspartame

- Saccharin

- Neotame

- Cyclamate

- Acesulfame Potassium (Ace-K)

- Other Artificial HIS

-

Natural High-Intensity Sweeteners

- Stevia Extract

- Monk Fruit Extract

- Other Natural HIS

-

Artificial High-Intensity Sweeteners

- Other Sweeteners

-

By Application

- Bakery and Confectionery

- Dairy and Desserts

- Beverages

- Soups, Sauces, and Dressings

- Other Applications

-

By Form

- Powder

- Liquid

- Crystal

-

By Category

- Conventional

- Organic

-

By Region

- Western Canada

- Central Canada

- Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed ingredient blenders, regional food-service buyers, and R&D leads in Ontario, Quebec, and British Columbia to validate usage ratios, average selling prices, stevia adoption hurdles, and likely reformulation timelines. Supplemental surveys of dietitians and diabetic-focused consumer groups helped stress-test health-driven demand assumptions.

Desk Research

We, the analyst team, first mapped supply-demand fundamentals using open statistics from Statistics Canada, Agriculture and Agri-Food Canada, Canadian Sugar Institute trade data, and HS-code shipment logs accessed through Volza. Company 10-Ks, CFIA additive approvals, and relevant peer-reviewed journals on caloric reduction trends rounded out context. Paid platforms, including D&B Hoovers for processor revenues and Dow Jones Factiva for deal news, helped size corporate footprints. The sources listed are illustrative; many additional references informed our evidence base.

Market-Sizing & Forecasting

A top-down model begins with per capita sugar and HFCS disappearance data, reconstructs value through trade flows, then layers penetration rates for HIS and polyols. Results are cross-checked with bottom-up processor revenue roll-ups and sampled ASP × volume for key categories. Variables such as beverage launch counts, maple syrup output, diabetic prevalence, and excise tax coverage feed a multivariate regression that produces the 2025-2030 outlook. Gaps where processor splits are opaque are bridged using channel-check ranges validated in interviews.

Data Validation & Update Cycle

Outputs pass anomaly screens, senior analyst peer review, and a pre-publication refresh. Our models are revisited annually, with interim updates triggered by material events like tariff shifts or novel sweetener approvals.

Why Mordor's Canada Food Sweetener Baseline Commands Reliability

Published market values often diverge because each firm picks its own product mix, price points, and refresh rhythm.

Key gap drivers include differing treatment of retail sugar bags, varying ASP escalation paths, and longer refresh cadences that miss rapid stevia penetration in beverages.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.63 B (2025) | Mordor Intelligence | - |

| USD 2.21 B (2023) | Regional Consultancy A | narrower product set; excludes polyols in food service |

| USD 2.14 B (2023) | Trade Journal B | applies static ASP and omits import-re-export adjustments |

Taken together, the comparison shows how Mordor's mixed-method model, annual refresh, and transparent scope give decision-makers a balanced, traceable baseline that sits between conservative and aggressive peer estimates.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Canada sweeteners market?

The market is valued at USD 2.72 billion in 2026 and is projected to reach USD 3.19 billion by 2031.

Which region dominates sweetener demand in Canada?

Central Canada commands 74.62% share thanks to its dense food-processing base and is forecast to grow at 4.36% CAGR through 2031.

Which product segment is expanding fastest?

High-intensity sweeteners will post the highest growth at 4.98% CAGR as brands target aggressive sugar-reduction goals.

How quickly are organic sweeteners growing?

The organic segment is advancing at a 4.72% CAGR, supported by a sharp rise in certified maple syrup output.