Executive Summary

- What Happened: The EU and India concluded FTA negotiations on 27 Jan 2026, zero tariffs on 97.5% of Indian chemicals exports, reciprocal duty elimination on EU exports to India.

- What it Means: Tariff removal reshapes competitive dynamics on both sides: Indian exporters gain EU market access, while European suppliers gain cost advantages in India's downstream market.

- Who Wins: Specialty chemicals and performance plastics players (both Indian and European) with compliance-ready portfolios, regulatory fluency, and differentiated offerings.

- What to Watch: REACH, PPWR, and microplastics rules will determine market access velocity; domestic competition in India will intensify as EU inputs enter duty-free.

- Timeline: Deal subject to legal scrub and approvals; benefits begin only after entry into force.

The EU and India just concluded negotiations on what both sides are calling their largest-ever trade deal. For chemicals and plastics, it's a dual-sided market reset: tariff elimination opens doors in both directions, but the players who scale will be those who treat regulatory readiness and competitive differentiation as strategic imperatives, not afterthoughts

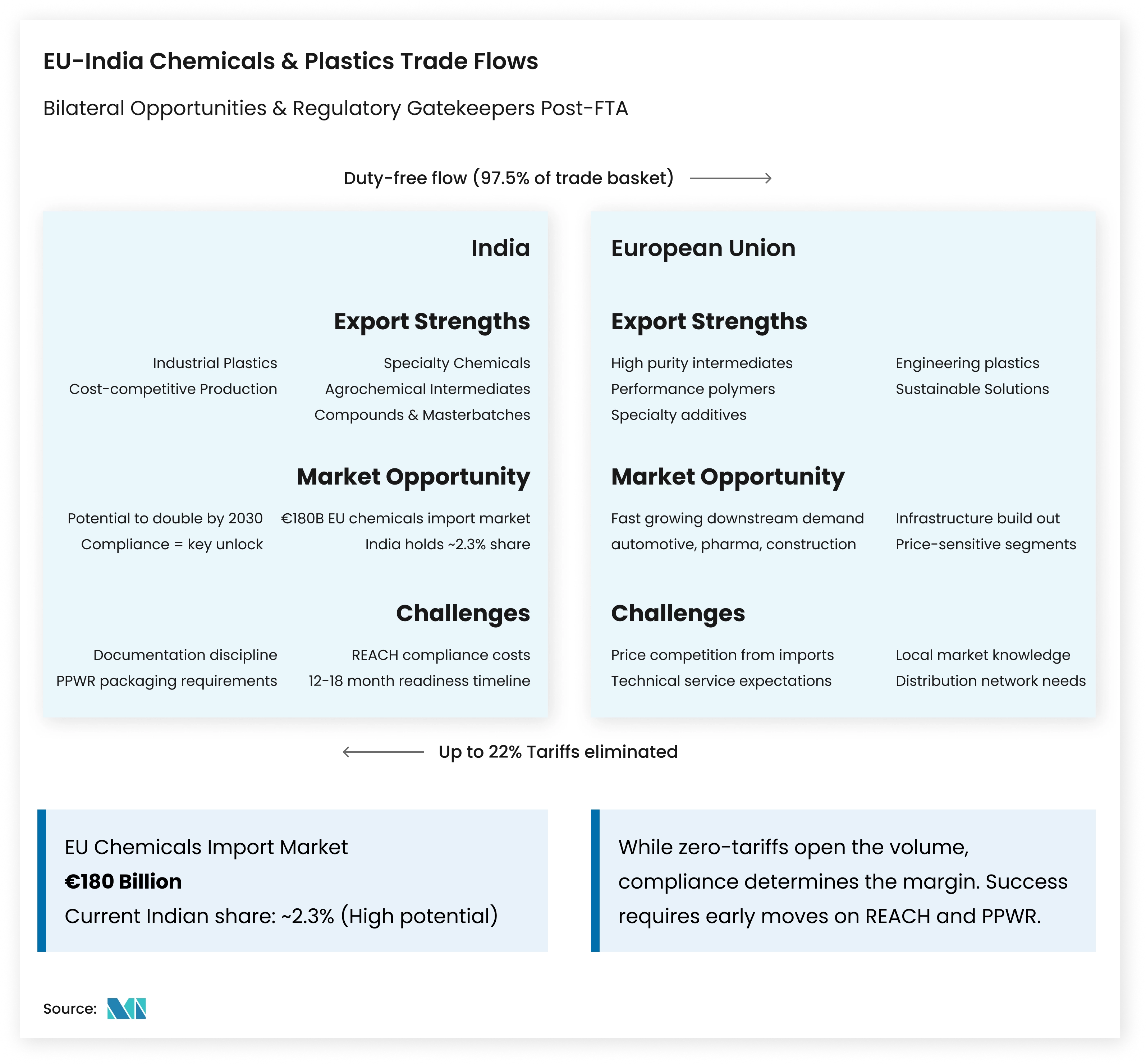

On 27 January 2026, the European Union and India announced the conclusion of FTA negotiations. For chemicals and plastics, the agreement creates a two-way corridor: Indian exporters gain preferential access to a EUR 600+ billion (USD 700+ billion) European market, while European suppliers gain lower-cost entry into India's fast-growing downstream sectors.

The strategic context matters. As global supply chains recalibrate around resilience, regulatory alignment, and geopolitical risk, this FTA positions both regions as preferred partners, for players who can navigate the compliance architecture that increasingly defines market access in developed economies.

Tariff Walls Are Set to Fall on Both Sides

For Indian exporters, the headline is clear. Key labour-intensive sectors, including chemicals and plastics, rubber, are slated for zero-duty access from entry into force, improving landed-cost competitiveness in the EU market.

For European suppliers, the reverse is equally consequential. India’s current tariffs on EU chemicals (up to 22%) and plastics (up to 16.5%) are expected to fall to zero for almost all products. This can reduce input costs for Indian downstream users, while simultaneously intensifying competitive pressure for domestic producers.

For Indian producers, tariff elimination improves access to EU markets but simultaneously intensifies domestic competition as EU inputs enter duty-free, reshaping cost structures and value-chain dynamics across the industry, a shift examined in our Analysis of the Plastic Industry in India.

The practical implication is nuanced. The EU-India FTA can simultaneously:

- Expand EU demand access for Indian suppliers.

- Lower the cost base for Indian manufacturers reliant on imported intermediates.

This creates two parallel opportunity paths: export-led scale for compliant suppliers, and margin or quality uplift for downstream users able to leverage lower-duty imports.

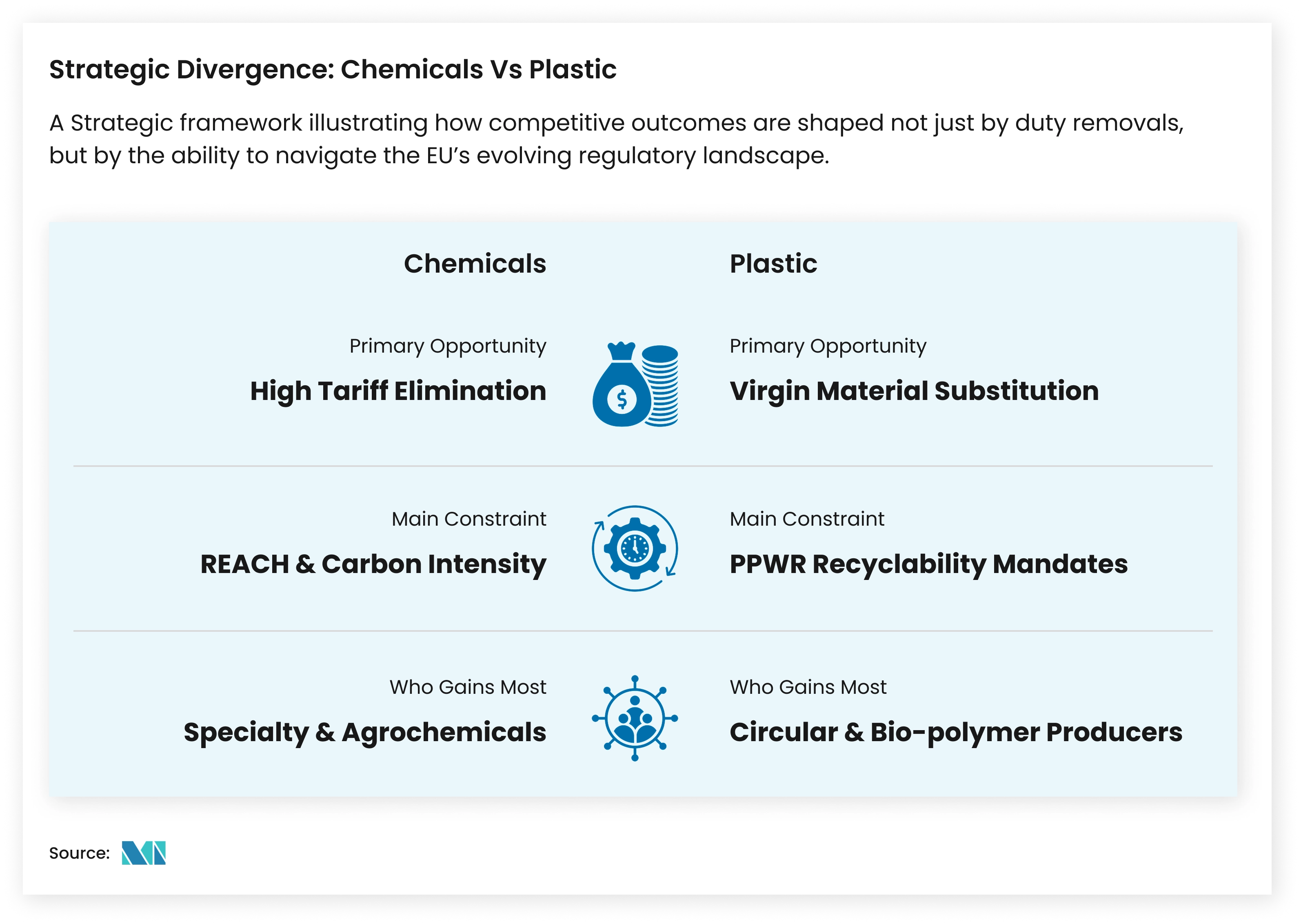

Chemicals: An Export “Unlock,” But Only for Compliant Product Baskets

The EU imported approximately EUR 180 billion (USD 212.22 billion) in chemicals in 2024, with India accounting for around 2.3% of total imports. India’s specialty chemicals exports to the EU could grow at an 18 to 22% CAGR post-FTA, assuming compliance readiness across priority categories.

As the EU opens preferential access, the real upside concentrates in specialty chemicals with compliance-ready portfolios, where regulatory readiness and product differentiation increasingly determine export growth within the Specialty Chemicals Market.

What emerges is not a one-way export story, but a rebalancing of trade flows and partnership models with implications for pricing power, product positioning, and collaboration depth.

How the EU–India FTA Translates into Strategic Choices

| What the EU-India FTA Changes | What It Enables | What Leaders Need to Decide |

| Zero duty on most Indian chemical exports to the EU | Improved landed-cost competitiveness in the EU market. | Which product baskets justify full compliance investment. |

| Elimination of duties of up to 12.8% |

Margin headroom for specialty and regulated-grade products. | Where to prioritize portfolio focus over volume expansion. |

| Reduced tariffs on EU chemicals entering India |

Access to higher-quality intermediates and additives. | How to manage increased domestic competition. |

| Two-way tariff liberalization |

New partnership and joint development models. | Whether to reposition as an EU-aligned supplier or remain cost-led. |

Source: Mordor Intelligence

Plastics: The Opportunity Goes Beyond Polymers

Plastics and rubber products benefit from the same zero-duty framing on India’s side, with the EU identified as a large and high-potential destination market. Yet the most durable opportunities are unlikely to sit in undifferentiated commodity resins.

In Europe, engineering-grade plastics are gaining share in automotive, electrical, and high-reliability applications, as consistency, traceability, and compliance increasingly outweigh scale considerations across the Europe Engineering Plastics Market.

Competitive Outcomes Under Tariff Relief and Compliance Constraints

| Segment Focus |

What EU Buyers Prioritize | Why This Segment Wins |

| Commodity Polymers | Price competitiveness | Tariff relief alone is insufficient without differentiation or compliance depth. |

| Compounds & Masterbatches | OEM-specific formulations and consistency | Rewards engineering depth and the ability to meet precise EU automotive, electrical, and appliance specifications. |

| Compliant Packaging Formats | Recyclability, documentation, and packaging-waste alignment | Supplier qualification increasingly depends on packaging compliance, not just product performance. |

| High-consistency Industrial Plastics | Process control and traceability | Enables access to medical, consumer durables, and infrastructure applications where reliability outweighs scale. |

Source: Mordor Intelligence

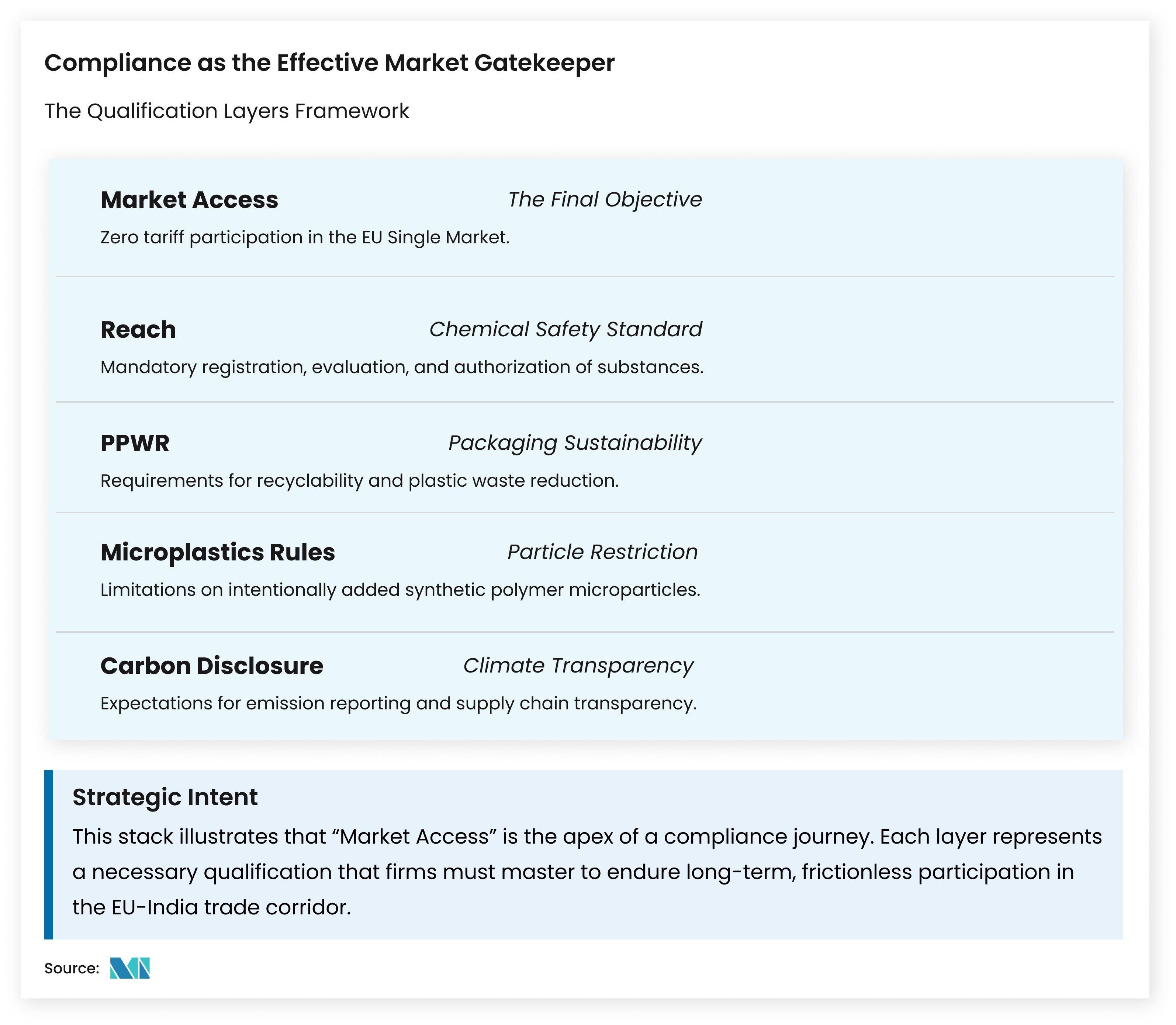

Compliance as the Effective Market Gatekeeper

Tariff relief is a prerequisite, not a guarantee. In practice, several EU regulatory regimes materially shape whether preferential access can be converted into actual sales.

1. REACH: “No Data, No Market” is Non-Negotiable

Under REACH, the burden of proof sits with industry. Substances, typically those manufactured or imported at or above one tonne per year per company, require registration dossiers. For Indian exporters, this reshapes the economics of serving Europe unless compliance pathways and cost-sharing models are designed upfront.

For non-EU exporters, this reshapes economics unless:

- Compliance pathways are designed upfront (often 12–18 months).

- Cost-sharing models are negotiated with buyers, importers, or consortia.

- Documentation is treated as a continuous process, not a one-time project.

REACH compliance costs for a mid-sized specialty chemicals exporter range from EUR 50,000 to EUR 200,000 (USD 59,000 to USD 230,000) per substance, making SKU prioritization commercially critical.

2. Packaging Rules Tighten

The EU’s Packaging and Packaging Waste Regulation has entered into force, with broad application from 12 August 2026. For exporters of packaged chemicals, formulations, or plastic goods, packaging compliance is no longer a downstream buyer issue. It increasingly becomes a supplier qualification threshold.

3. Microplastics Restrictions Are Active

Restrictions on intentionally added microplastics are now part of the regulatory landscape. Even when base polymers are not directly targeted, downstream applications including additives, coatings, detergents, cosmetics, or agricultural uses, can trigger scrutiny, forcing reformulation or detailed disclosure.

4. CBAM in the Background Shapes Buyer Behaviour

CBAM’s definitive regime begins on 1 January 2026. Plastics are not currently included in the initial CBAM sector list. Even so, the mechanism matters. It accelerates expectations around carbon transparency across supply chains, particularly where chemicals intersect with fertilisers, hydrogen, electricity-linked intermediates, or energy-intensive upstream steps.

For both Indian and European exporters, Carbon footprint documentation is becoming a qualification requirement, not a differentiator.

Two Exporter Paths Are Beginning to Diverge

In early discussions with market participants, two distinct approaches to the EU opportunity are starting to emerge. One group is narrowing its EU exposure to a smaller set of highly compliant, differentiated SKUs where tariff removal can clearly outweigh compliance costs. Another is attempting to maintain broad catalog coverage, only to discover that compliance effort scales faster than revenue in low-margin long tails. The FTA does not eliminate this trade-off. It sharpens it.

The Winner’s Playbook

For Indian Producers

Lower duties on EU chemicals and plastics will improve input availability and quality for downstream converters, but also compress margins for domestic suppliers. Move up the value curve or lock in vertical integration.

For European Producers

Increased competition from Indian imports in price-sensitive segments will pressure commodity players. Differentiation through technical service, application support, and sustainability credentials becomes critical.

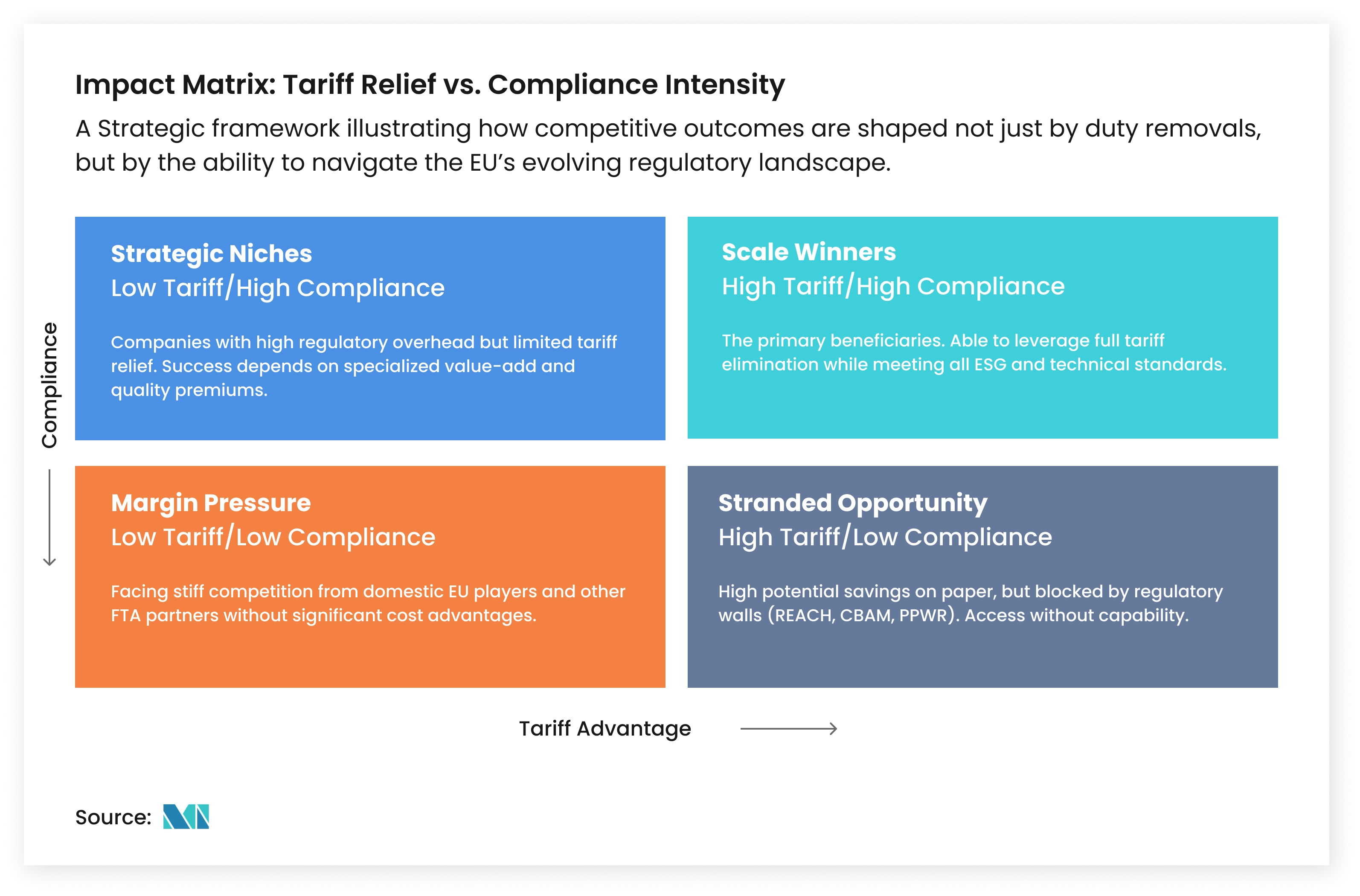

How the Landscape Is Likely to Settle by 2028–2030

If compliance readiness and differentiation drive market outcomes, we're likely to see three distinct tiers emerge in both regions.

Tier 1: Scale Winners

Specialty chemicals and performance plastics players with compliance-registered portfolios, market-specific manufacturing capabilities, and transparent supply chains. These companies capture disproportionate share of cross-border demand growth.

Tier 2: Niche Players

Mid-sized exporters serving specific applications or geographies where compliance barriers are lower (e.g., non-REACH substances, B2B intermediates with buyer-led registration, or domestic-focused production). Steady but limited growth.

Tier 3: Stranded Opportunity or Margin Compression

Commodity producers with tariff advantage but no compliance pathway or differentiation. Unable to convert preferential access into revenue or facing intensified domestic competition from duty-free imports.

How Does This FTA Fit Into Broader Supply Chain Recalibration?

This agreement doesn't happen in isolation. Global buyers, especially in Europe and North America, are actively de-risking dominant exposure across chemicals, APIs, agrochemicals, and specialty polymers.

India's Positioning Benefits From

- Preferential market access (zero duties).

- Regulatory alignment (democratic governance, IP protection, trade dispute mechanisms).

- Geopolitical trust (Quad member, strategic autonomy narrative).

Europe's Positioning Benefits From

- Diversified sourcing options for critical inputs.

- Regulatory leverage (REACH, CBAM, sustainability frameworks shape global supplier behavior).

- Access to India's fast-growing downstream demand (automotive, pharma, construction, packaging).

What This Means for Different Stakeholders

From Market Access to Action: Stakeholder Implications of the EU–India FTA

| Stakeholder | What Changes | Priority Actions |

| Exporters (India & EU) | Preferential access raises demand for compliant, differentiated products. | Audit portfolios for EU-ready SKUs and budget early for REACH, packaging, and carbon documentation. |

| Manufacturers & Converters | Lower-duty imports improve input quality but intensify competition. | Differentiate through technical service, application development, or vertical integration. |

| Buyers & Distributors | Both markets become more attractive sourcing bases. | Build compliance-aligned supplier partnerships and strengthen qualification processes. |

| Policymakers & Trade Bodies | Market access depends on regulatory readiness at cluster level. | Invest in REACH consortia, packaging compliance tools, carbon frameworks, and technical assistance. |

Source: Mordor Intelligence

Final Thought: Access Opens. Capability Decides.

The EU–India FTA creates a significant two-way opportunity for chemicals and plastics: preferential access, scale potential, and a platform for deeper value-chain integration.

The companies that win, on both sides, won't be the ones with the loudest press releases. They'll be the ones that combine tariff advantage with regulatory fitness, documentation discipline, and product-level differentiation.

We're observing early shifts in sourcing strategies and competitive positioning, not a full-scale pivot yet, but the signs are emerging. Players who move now on compliance infrastructure and differentiation will be the ones capturing disproportionate share when the market fully opens.

Want deeper insights into how the EU–India FTA is reshaping the chemicals and plastics trade? Explore our latest reports on Plastics & Polymers and Specialty Chemicals.