Opening Signal: Trade Policy as a Supply Chain Reset

India’s recently concluded trade agreement with the European Union and the phased trade liberalization framework with the United States mark a structural shift for the global automotive trade and auto ancillary ecosystem. These agreements do not function as short-term demand catalysts. Instead, they alter the underlying economics of tariffs, sourcing, supplier integration, and long-term capital deployment across vehicles and components.

For the automotive sector, the impact unfolds unevenly. Automotive imports respond slowly due to pricing thresholds, dealer economics, and consumer behavior. Auto components and aftermarket segments respond earlier, as tariff changes influence sourcing decisions, supplier qualification, and platform integration.

Together, the two agreements recalibrate how India participates in global automotive supply chain. Between 2026 and 2030, their effects are expected to surface through gradual shifts in export competitiveness, localization strategies, joint venture formation, and aftermarket expansion rather than abrupt market disruption.

India–EU Trade Agreement: Automotive and Component Industry Impact

The European Union is India’s largest trading partner in goods. In FY 2024–25, bilateral merchandise trade exceeded USD 135 billion, with automobiles, transport equipment, and auto components forming a high-value segment of industrial trade.

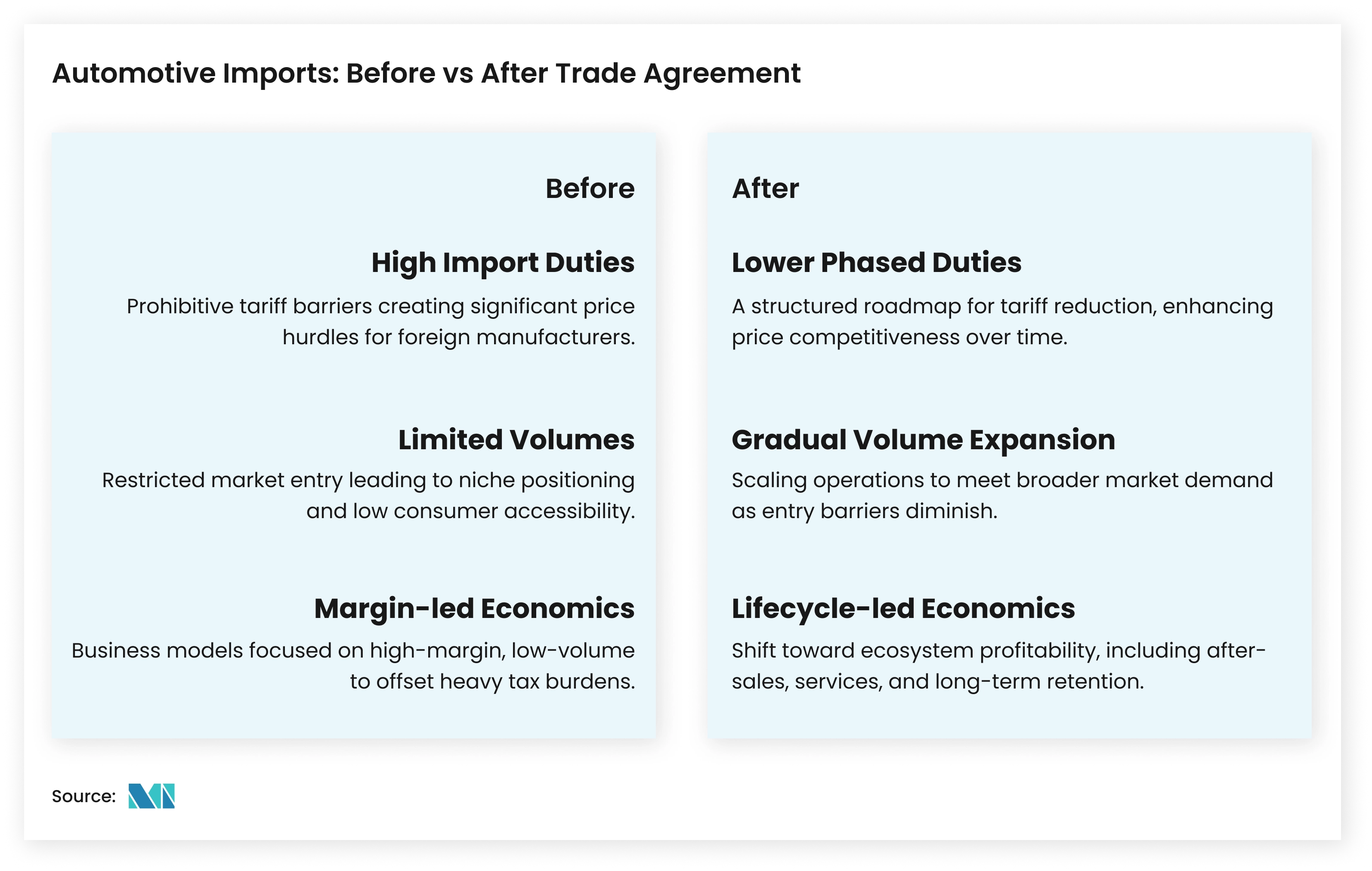

Vehicle Imports: Gradual Repricing of the Premium Segment

Historically, fully built premium and luxury vehicles imported into India were subject to customs duties exceeding 100%. This constrained volumes while protecting margins for original equipment manufacturers.

Under the India EU trade agreement, import duties on premium and luxury passenger vehicles originating from European markets are expected to decline gradually to a range of 10 to 25% under quota-linked mechanisms. This improves affordability over time and supports a controlled expansion of the addressable market rather than a rapid surge in imports.

The downstream effects extend beyond vehicle sales. Lower entry barriers are expected to strengthen dealer networks, increase certified used vehicle circulation, and expand demand for parts, electronics, and service-related aftermarket offerings across India’s premium automotive segment. Beyond vehicle sales, lower entry barriers are expected to expand parts, services, and certified used vehicle activity across the automotive aftermarket market.

Automotive Components and Ancillaries: Export and Integration Effects

India automotive exports in auto components reached approximately USD 23 billion in FY 2024–25, with Europe accounting for over 25% of total shipments. The trade agreement strengthens this position through tariff reduction, regulatory alignment, and improved supplier access. The agreement provides for:

- Progressive tariff reduction on automotive components.

- Improved regulatory compatibility with EU standards.

- Enhanced integration of Indian suppliers into European supply chains.

From a financial perspective, scale-driven export growth supports EBITDA margin expansion, while operating leverage and improved receivables stability support medium-term cash flow generation.

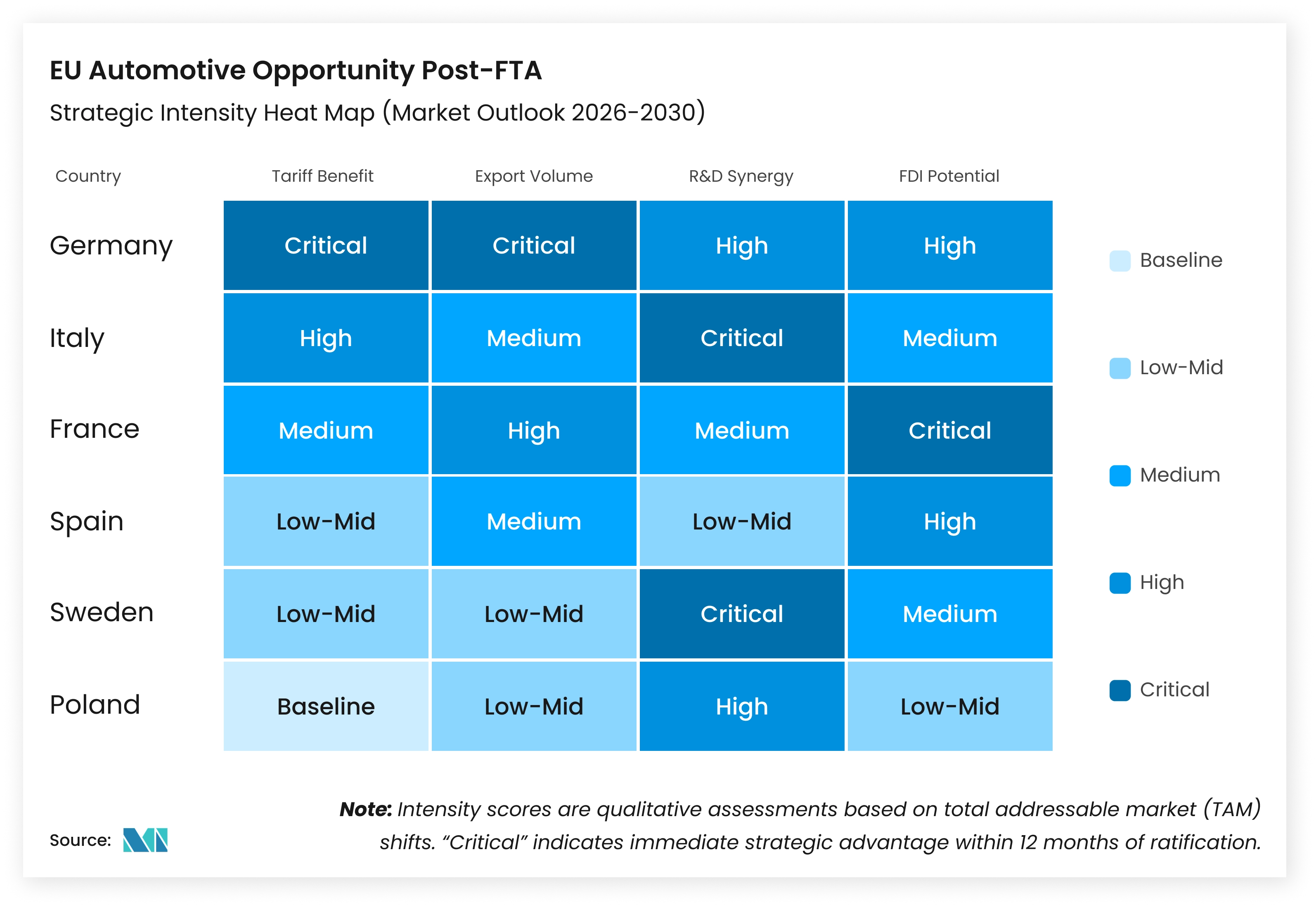

Impact Matrix: Key EU Countries and Automotive Opportunities

Key EU Automotive Export Opportunities to India Post-FTA

| EU Country | Vehicle Exports to India | Key Components | Post-FTA Opportunity |

| Germany | Luxury cars, SUVs | Powertrain, electronics | Volume growth and aftermarket scale |

| France | Premium vehicles | Electronics, rail systems | Joint venture manufacturing |

| Sweden | Safety-focused vehicles | ADAS, sensors | High-value imports |

| Italy | Niche vehicles | Castings, mechanicals | Tier-2 sourcing |

| Spain | Compact vehicles | Body and trim parts | Cost-competitive sourcing |

| Czech Republic | Skoda platforms | Assemblies | Export platform integration |

| Slovakia | SUVs | Drivetrain parts | Supplier localization |

Source: Mordor Intelligence

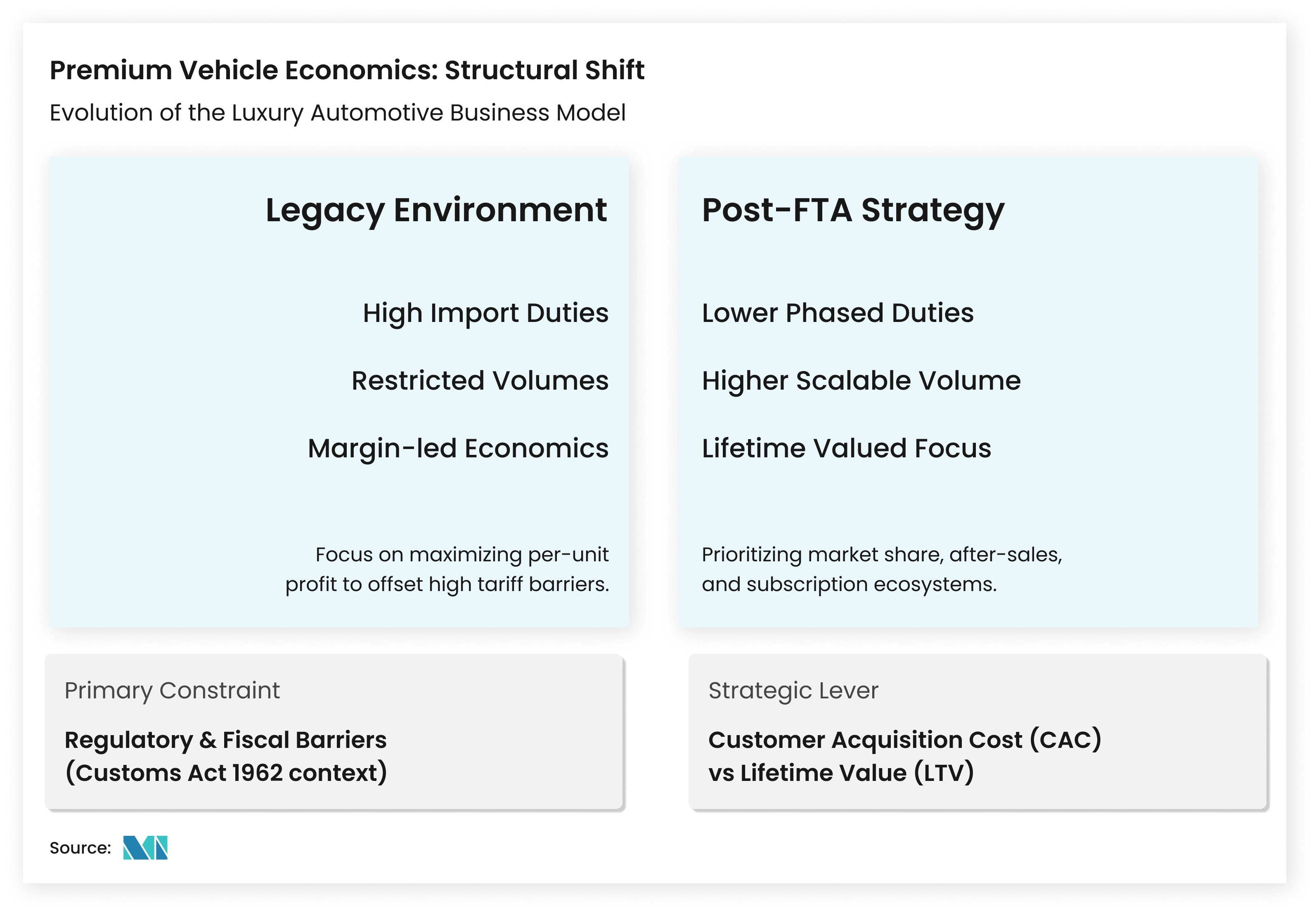

Luxury and Premium Vehicles: Margin Structure Evolution

Before the agreement, high import duties structurally suppressed volumes while supporting per-unit margins. Post-agreement, the model evolves gradually.

Key Shifts Include:

- Import duties reducing to 10–25% on a phased, quota-linked basis.

- Gradual expansion of annual import quotas.

- OEM focus shifting from per-unit margin optimization to lifetime customer value.

Manufacturers with modular platforms and strong premium portfolios are better positioned to benefit from this transition.

India–US Trade Deal: Automotive and Component Industry Impact

India US trade deal influences the automotive sector primarily through auto components rather than finished vehicles. While direct vehicle exports to the U.S. remain limited, supplier integration into North American production networks is material.

According to the Automotive Component Manufacturers Association of India, US automovtive exports accounted for approximately 25% of India’s total component shipments in FY 2024–25. Tariff reductions to around 18% improve cost competitiveness and increase supplier visibility within U.S. manufacturing ecosystems.

Indian suppliers such as Bharat Forge, Samvardhana Motherson International, and Uno Minda are positioned to benefit through deeper integration into U.S. platforms, particularly in powertrain components, wiring harnesses, and electronic modules.

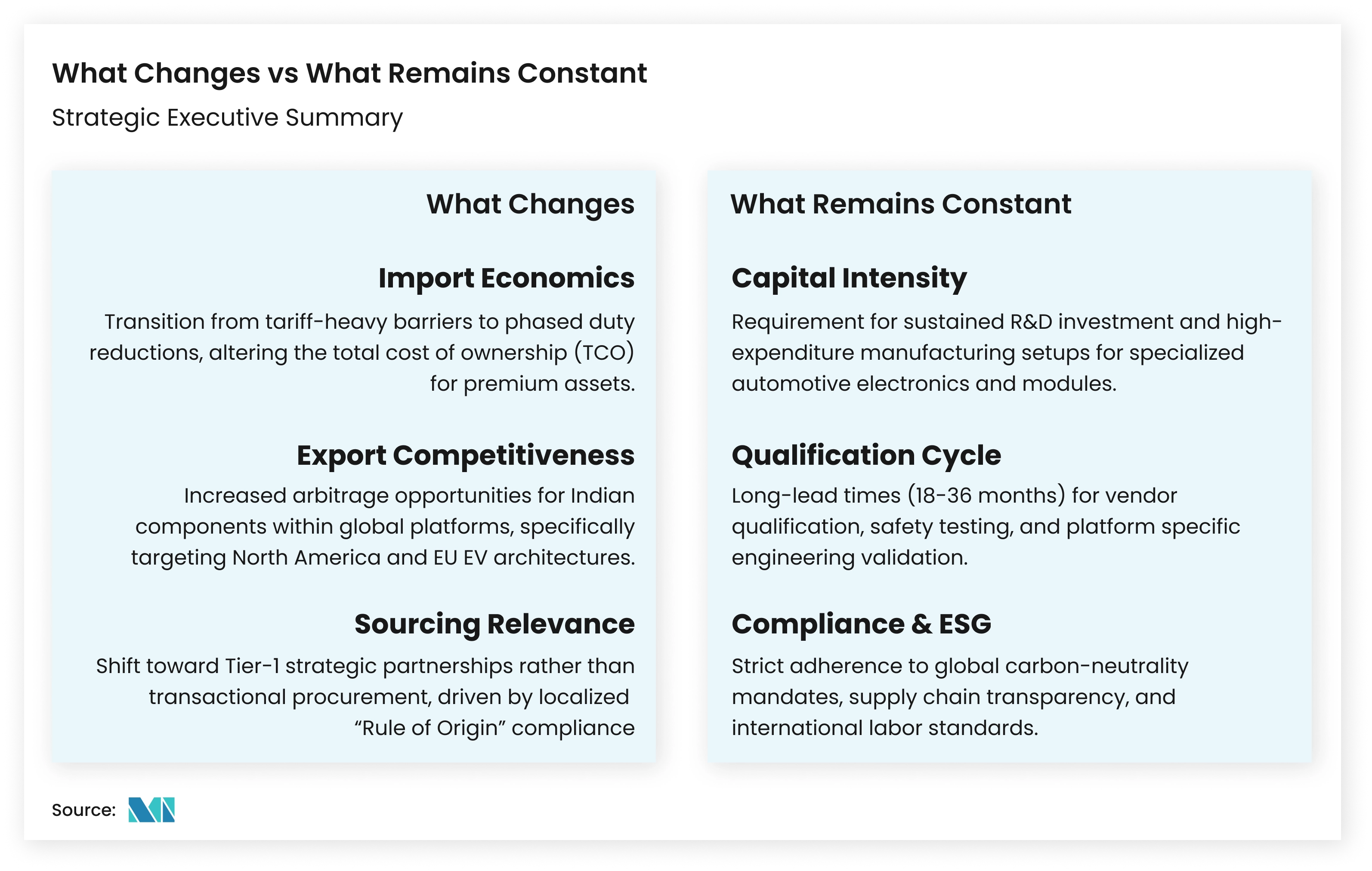

What Changes and What Remains Constant

What Changes

- Import economics for premium vehicles.

- Export competitiveness for auto components.

- Strategic relevance of India in global sourcing decisions.

What Remains Constant

- Capital intensity of automotive manufacturing.

- Long qualification and homologation cycles.

- Dependence on regulatory and quality compliance.

Executive Takeaways

- India–EU and India–US trade agreements recalibrate automotive tariff structures and supply chain economics.

- Auto component exports respond faster than vehicle imports due to shorter sourcing cycles.

- Reduced import duties influence premium vehicle pricing and aftermarket expansion.

- India’s auto ancillary sector strengthens its integration into EU and US production networks.

- Long-term gains depend on localization strategy, regulatory compliance, and EV component capabilities.

Want deeper insights on how India–EU and India–US trade agreements are reshaping automotive imports, auto component exports, and supply chain strategies? Explore our latest Automotive reports and Vehicles research reports.