Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

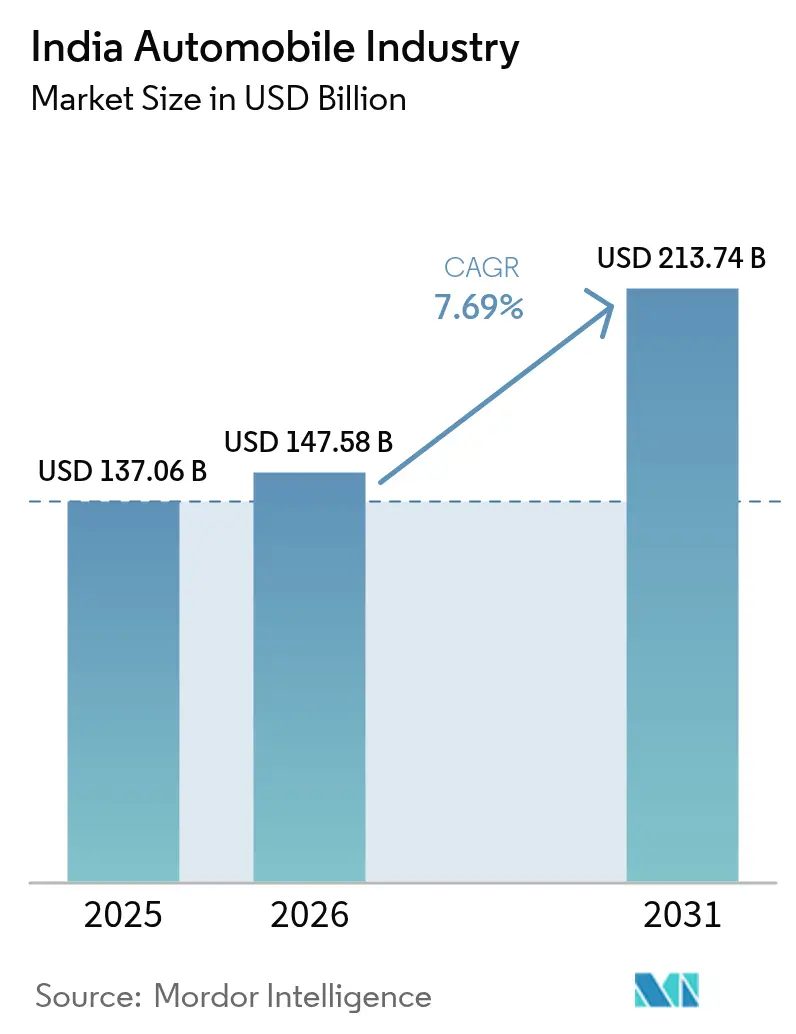

| Base Year Market Size (2025) | USD 137.06 Billion |

| Market Size (2026) | USD 147.58 Billion |

| Market Size (2031) | USD 213.74 Billion |

| Growth Rate (2026 - 2031) | 7.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Automobile Industry Analysis by Mordor Intelligence

The India automobile market size is expected to grow from USD 137.06 billion in 2025 to USD 147.58 billion in 2026 and is forecast to reach USD 213.74 billion by 2031 at 7.69% CAGR over 2026-2031. Demand is buoyed by population‐led consumption, rising household incomes, policy-backed electrification, and a manufacturing base that produced 28.43 million vehicles in FY 2024[1]“Automobile Industry in India,”, Invest India, investindia.gov.in. Sustained output across two-wheelers, passenger cars, commercial vehicles, and three-wheelers keeps the sector resilient, while infrastructure programs such as Pradhan Mantri Gram Sadak Yojana widen geographic reach. Competitive dynamics remain intense, yet opportunities persist in electric models, subscription ownership, and corporate fleet decarbonization. Semiconductor self-reliance, rural road density, and digital retail are additional levers set to lift the India automobile market through the decade.

Key Report Takeaways

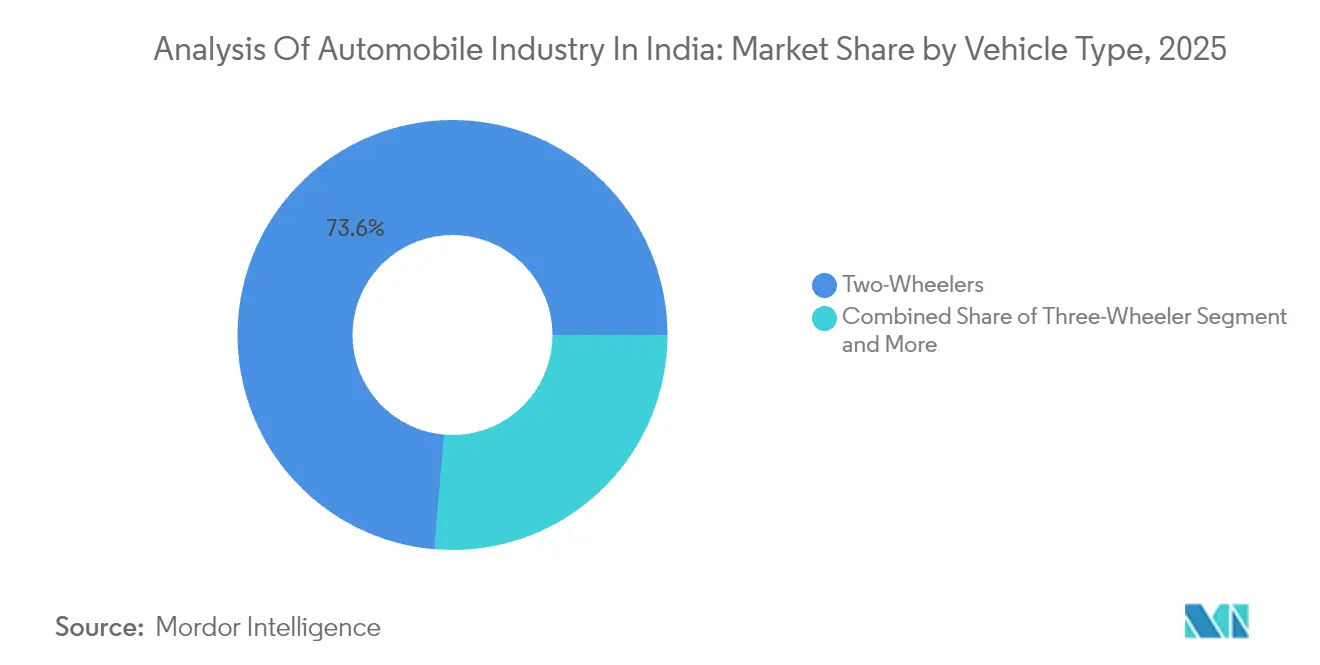

- By vehicle type, two-wheelers captured 73.64% of India automobile market share in 2025; passenger cars are advancing at the fastest 8.84% CAGR to 2031.

- By fuel type, petrol vehicles accounted for 59.27% of the India automobile market size in 2025, whereas battery electric vehicles are forecast to register a 10.02% CAGR between 2026 and 2031.

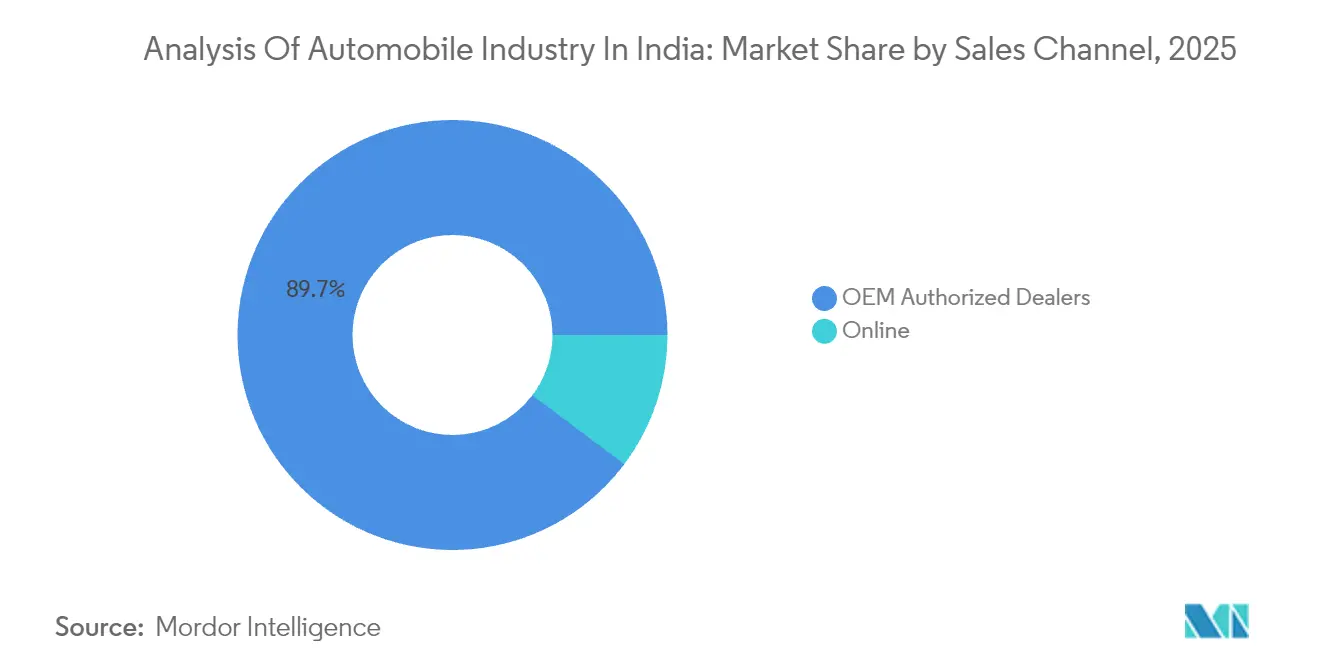

- By sales channel, OEM-authorized dealerships retained 89.73% share of the India automobile market in 2025, yet online sales are set to climb at a 9.11% CAGR through 2031.

- By ownership, personal vehicles commanded 75.94% of India automobile market size in 2025, while commercial fleets are expanding at a 9.16% CAGR to 2031.

- By region, North India led with 31.92% revenue share of the India automobile market in 2025, while South India is projected to grow at a 9.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Automobile Industry Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Disposable Incomes and Rapid Urbanization | +1.5% | Nationwide; Tier-2 cities | Medium term (2-4 years) |

| Government EV and FAME-II Incentives | +1.2% | Metropolitan clusters | Short term (≤2 years) |

| Expansion of National Highway and Rural Road Network | +1.0% | Rural corridors | Long term (≥4 years) |

| Subscription-based Ownership and Leasing | +0.8% | Urban premium markets | Medium term (2-4 years) |

| Local Semiconductor Fabrication Investments | +0.7% | Tamil Nadu, Gujarat hubs | Long term (≥4 years) |

| Corporate Fleet-decarbonization Mandates | +0.6% | Industrial corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes and Rapid Urbanization

Income growth is enlarging the consumer base for the Indian automobile market, especially in Tier-2 and Tier-3 cities, where land availability and lower congestion make vehicle ownership attractive. Sixty-five percent of the population is under 35, aligning prime earning years with first-time purchases. Migration from rural districts stimulates dual demand, urban buyers seek mobility, while remittances finance upgrades back home. The spread of suburban employment hubs reduces dependence on mass transit and supports two-wheelers and compact cars. Subscription programs extend access by sidestepping hefty down payments, further deepening penetration.

Government EV and FAME-II Incentives

India's FAME (Faster Adoption and Manufacturing of Hybrid & Electric Vehicles) Scheme Phase-II, launched in 2019, comes with a hefty budget of INR 11,500 crore (USD 1.31 billion), set to span five years. This initiative aims to boost the sales of electric vehicles, covering e-2Ws, e-3Ws, and e-4Ws. [2]“Annual Report 2025,”, Ministry of Commerce & Industry, commerce.gov.in. State add-ons in Tamil Nadu and Gujarat enhance regional differentials, while the planned FAME-III revision aims to broaden support into heavier segments. These incentives shorten payback periods, encouraging personal buyers and fleet operators to pivot toward zero-emission models.

Expansion of National Highway and Rural Road Network

Connecting more than 159,000 habitations has raised non-farm employment and improved freight efficiency[3]“Rural Roads Project Impact Evaluation,”, World Bank, worldbank.org. Improved roads shorten transit times, lessen vehicle wear, and expand dealer catchment areas, thereby significantly bolstering the long-term outlook for India's automobile market. These advancements not only enhance accessibility for dealers but also create opportunities for market penetration in previously untapped regions. Furthermore, better road infrastructure facilitates smoother transportation of goods, reducing delays and ensuring timely deliveries. Additionally, manufacturers benefit from streamlined logistics, which improve supply chain efficiency and enhance their cost competitiveness both domestically and in export markets. This infrastructure development also supports the growth of ancillary industries, such as auto components and logistics services, further strengthening the overall ecosystem of the automobile market in India.

Subscription-Based Ownership and Leasing Models

Digitally native consumers are prioritizing flexibility instead of outright ownership. With app-based subscriptions, users enjoy month-to-month access, which conveniently includes insurance, service, and roadside assistance. This model allows OEMs to capture lifecycle revenue and provides valuable data that informs design iterations and predictive maintenance services. Additionally, it enables OEMs to build stronger customer relationships by offering tailored services and fostering brand loyalty. The key to scaling this model lies in managing residual values and ensuring liquidity in the secondary market, a feat currently bolstered by partnerships between carmakers and global leasing giants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Changes, Safety Standards and GST Shifts | -1.2% | Nationwide | Short term (≤2 years) |

| Global Semiconductor Supply-chain Volatility | -0.8% | Key manufacturing hubs | Medium term (2-4 years) |

| Urban Congestion-driven Usage Restrictions | -0.6% | Major metros | Medium term (2-4 years) |

| Rising Telematics-linked Insurance Premiums | -0.4% | Urban fleets | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Regulatory Changes, Safety Standards and GST Shifts

As India implements BS-VII norms and mandates safety gear, small assemblers grapple with costly powertrain upgrades and validations, squeezing their model margins. These upgrades require significant research and development investments and rigorous testing to meet compliance standards. Meanwhile, GST realignments on components introduce pricing uncertainties, impacting the overall cost structure for manufacturers. Adding to the challenge, varying state road-tax regimes complicate compliance, as manufacturers must navigate differing tax policies across regions. These factors lead to noticeable price hikes for consumers, potentially delaying their purchases and dampening immediate demand in the Indian automobile market. Additionally, the increased costs may push manufacturers to explore alternative strategies, such as the localization of components, to mitigate the financial burden.

Global Semiconductor Supply-Chain Volatility

Even with diversification efforts, lead times for automotive-grade microcontrollers continue to be prolonged, creating significant challenges for manufacturers to meet demand efficiently and maintain production schedules. The sector's limited global bargaining power further complicates secure allocations, making it increasingly difficult to negotiate favorable terms with suppliers or ensure consistent supply. The heavy reliance on overseas wafer fabrication exposes local plants to vulnerabilities, such as logistical delays, geopolitical tensions, or supply chain disruptions, which can severely impact operations. While inventory buffers act as a safeguard to maintain production continuity by ensuring a steady supply of components, they also lead to increased working-capital requirements. This, in turn, compresses profitability and places additional financial strain on manufacturers until domestic fabrication capacity is expanded to address these challenges and meet the growing demand effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Two-Wheelers Sustain Dominance Despite Premium Shift

In the Indian auto market, two-wheelers reign supreme, commanding a significant 73.64% share. This dominance highlights the preference for two-wheelers among Indian consumers, driven by factors such as affordability, fuel efficiency, and ease of navigation in congested urban areas. Although smaller, passenger cars are posting the swiftest 8.84% CAGR on the back of SUV and crossover launches tuned to aspirational middle-class tastes. Scooter sales climbed 21% versus the motorcycle segment’s 10% gain, highlighting urban preference for automatic transmissions and ease of use.

Growth momentum continues as electric two-wheelers enter mainstream price points and as financiers extend longer tenures to first-time buyers. Conversely, commercial vehicles hinge on infrastructure budgets and industrial output cycles but benefit from ongoing highway upgrades. Three-wheelers retain relevance for last-mile goods and passenger movement in Tier-2 centers. Regulatory emission upgrades funnel investments toward modular platforms, potentially elevating scale efficiencies for incumbents in the Indian automobile market.

By Fuel Type: Electrification Accelerates Despite ICE Dominance

Petrol engines retained 59.27% of the India automobile market share in 2025, buoyed by refinery capacity and lower purchase prices relative to diesel. Battery electric vehicles, though smaller in volume, are advancing at a 10.02% CAGR thanks to tax rebates, FAME-II subsidies and falling lithium-ion cell costs. Hybrids bridge range-anxiety gaps, offering efficiency gains without new-energy infrastructure dependence.

Policy commitments to domestic power generation and stricter fuel-economy norms will gradually shift OEM portfolios toward electrified drivetrains. LPG/CNG use expands in commercial fleets seeking operating-cost relief. Meanwhile, fuel-cell technology remains exploratory due to hydrogen supply gaps. Charging-network rollouts and battery-swapping pilots dictate adoption pace but indicators already point to accelerating consumer acceptance across segments in the India automobile market.

By Sales Channel: Digital Transformation Reshapes Distribution

Authorized dealerships still handled 89.73% of 2025 transactions, reflecting entrenched trust and after-sales service networks. Online platforms, however, are scaling at a 9.11% CAGR as digital-first buyers pursue transparent pricing and home delivery. Electric-vehicle makers push direct-to-consumer storefronts that compress costs and deliver end-to-end brand control.

Traditional retailers respond by integrating virtual showrooms, click-to-book tools, and doorstep test drives. Due to connectivity gaps and personal relationship expectations, rural reach hinges on physical outlets. Over time, omnichannel hybrids will dominate, blending digital discovery with tactile verification to secure loyalty in the India automobile market.

By Ownership Type: Commercial Segment Drives Growth Acceleration

Personal users formed 75.94% of the Indian automobile market in 2025, mirroring the cultural value attached to vehicle possession. Commercial demand, growing at 9.16% CAGR, is powered by e-commerce fulfillment, ride-sharing expansion, and the formalization of logistics SMEs. Government incentives and accelerated depreciation schedules strengthen fleet business cases, especially for electric light commercial vehicles that clock high daily mileage.

Telematics, route optimization, and predictive maintenance lift fleet utilization and depress per-kilometer costs, reinforcing a shift toward organized operations. Subscription fleets blur traditional personal–commercial boundaries by offering vehicle access over ownership, widening service revenue streams for OEMs.

Geography Analysis

North India delivered 31.92% of 2025 revenue for the India automobile market, anchored by the National Capital Region’s manufacturing and administrative influence. Proximity to policy centers and a dense supplier base grant scalability, yet stringent congestion and emission controls could temper volume expansion ahead. Dealer saturation prompts OEMs to pivot toward digital sales and rural catchments within the region.

South India is projected to clock the fastest 9.18% CAGR to 2031, leveraging Tamil Nadu’s integrated supply chain, skilled labor pool, and seaport access. Early adoption of charging corridors and dedicated EV policies accelerates electrification, positioning the south as a proving ground for new-energy platforms. R&D investments in Chennai and Bengaluru foster technology spillovers that enhance local product sophistication.

West India, led by Maharashtra and Gujarat, combines diversified industry, export-ready ports, and investor-friendly regulations to attract fresh capacity. Gujarat’s low-cost power and single-window clearances lure marquee projects from domestic and global automakers. East India trails in per-capita income and infrastructure, yet offers untapped volume potential once connectivity upgrades materialize. Across geographies, decentralizing economic growth disperses demand, compelling OEMs to recalibrate inventory, financing and service models to suit local preferences.

Regulatory Landscape

India automobile regulation is anchored by the Ministry of Road Transport and Highways (MoRTH) through the Central Motor Vehicles Rules (CMVR), 1989 and Automotive Industry Standards (AIS) developed under the Automotive Industry Standards Committee (AISC), with ARAI acting as the AISC secretariat and test agencies such as iCAT and CIRT supporting type approval and compliance. In May 2026, a CMVR amendment (G.S.R. 417(E)) tightened emission compliance for certain imported gasoline-fuelled M1 and L-category vehicles by requiring a Type-I exhaust emission compliance report on E20 reference fuel, reinforcing the parallel push toward ethanol blending and fuel-compatibility validation.

Policy instruments continue to influence technology direction and localization depth. The Ministry of Heavy Industries PLI-Auto scheme (2021-2027) supports Advanced Automotive Technology (AAT) products with a total outlay of INR 25,938 crore, with focus areas including BEVs and hydrogen fuel-cell vehicles. For demand-side support and model eligibility, the PM E-DRIVE framework uses an active online model approval and registration platform for OEMs, shaping how electric models are certified, listed, and made eligible for incentives.

Value Chain Analysis

India's automobile value chain covers raw materials and power-intensive processing (steel, aluminum, plastics, rubber) into casting/forging and component manufacturing, then vehicle assembly and testing, followed by distribution via road and rail to OEM-authorized dealerships and an expanding online-led discovery layer. Component ecosystems are organized around major hubs in North, West, and South India, with formal interfaces to certification and homologation via agencies such as ARAI and iCAT. Electrification also shifts upstream dependencies toward cells, BMS, power electronics, and software, while increasing the role of approved-model portals and incentive compliance processes under programs such as PM E-DRIVE.

Logistics and energy inputs have also surfaced as key constraints on resilience. During high-demand periods, shortage of car carriers has constrained factory-to-dealer movement, prompting OEMs such as Mahindra and Mahindra to rely more on rail and adjust dispatch planning. Energy security has emerged as another operational risk, with March 2026 reporting highlighting production slowdowns in parts of the supply base tied to gas availability for heat-intensive processes like forging and casting. On capability-building, new entrant activity shows how software, electronics, and external technology sourcing are being integrated into the chain, including JSW Motors partnerships (2025) for new-energy vehicle technology and digital backbone development.

Competitive Landscape

Major Players Maruti Suzuki, Hyundai, Tata Motors, Mahindra & Mahindra, Kia, and Toyota—command a significant share of unit sales, conferring procurement leverage and brand visibility that raise entry hurdles. Maruti Suzuki extends cost leadership through lightweight platforms and vendor co-location, whereas Hyundai targets design and feature differentiation. Tata Motors scales modular EV architectures across passenger and commercial lines, extracting synergies in battery sourcing.

Platform sharing, standard drivetrains, and software-defined features underpin cost reduction and faster model cycles. Chinese-origin challengers such as MG Motor and BYD exploit electric expertise and aggressive pricing to chip away at premium niches. Strategic investments in domestic semiconductor design, battery joint ventures, and flexible manufacturing aim to secure long-term resilience for incumbents.

Mergers, technology alliances, and capacity expansions punctuate the competitive narrative. Toyota’s tie-up with Suzuki pools hybrid know-how, while Mahindra partners with Volkswagen’s MEB platform to accelerate BEV rollout. Across the Indian automobile market, data monetization, over-the-air upgrades, and service subscriptions emerge as future revenue pillars.

India Automobile Market Leaders

Hero MotoCorp

Honda

TVS Motor Company

Maruti Suzuki

Bajaj Auto

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Large-scale capacity additions and cluster-led manufacturing investment create demand for suppliers across logistics, tooling, automation, and localized component ecosystems. In July 2026, Maruti Suzuki inaugurated its IMT Kharkhoda, Haryana manufacturing facility as a scalable plant (0.5 million units capacity with a pathway to 1 million units per annum) backed by a stated total investment of INR 35,000 crore, reinforcing demand for nearby vendor parks and tiered supply networks. In May 2026, Toyota announced a greenfield facility in the Bidkin Industrial Area, Maharashtra with an initial capacity of 100,000 vehicles per year and a planned production start in the first half of 2029, signaling continued OEM commitment to long-horizon capacity and supplier localization in new industrial corridors.

Technology and compliance requirements expand the opportunity set in connected, software-defined, and alternative-fuel product stacks. MoRTH draft actions around AIS-189 (cybersecurity management) increase demand for secure E/E architectures, OTA-ready software update management, validation, and cyber testing services. Separately, the May 2026 CMVR change requiring Type-I emission compliance reporting on E20 reference fuel for certain imported gasoline vehicles supports product and testing activity around ethanol compatibility. On the policy side, Budget 2026-27 earmarked INR 5,939.87 crore for the PLI Scheme for Automobiles and Auto Components, and the Ministry of Heavy Industries has also been formulating a component-focused incentive scheme above INR 5,000 crore to strengthen export-oriented manufacturing, widening the addressable space for high-value powertrain, electronics, and advanced materials suppliers.

Recent Industry Developments

- July 2026: Maruti Suzuki inaugurated its vehicle manufacturing facility at IMT Kharkhoda, Haryana, adding a major scalable production node with an initial capacity of 0.5 million units and a pathway to 1.0 million units per annum, backed by a stated total investment of INR 35,000 crore. The project reinforces North India as a high-volume manufacturing cluster and tightens the competitive emphasis on cost, throughput, and supplier co-location. The inauguration also reinforces the role of new plants designed around higher automation and sustainability programs in mainstream passenger vehicles.

- June 2026: Hero MotoCorp announced its first flex-fuel motorcycles, Splendor+ and HF Deluxe, engineered for ethanol blends from E20 to E85 with a phased retail rollout beginning in July 2026. The move aligns mass-market two-wheelers with India’s ethanol-blending roadmap and adds a compliance-driven differentiation lever beyond pure electrification. It also pulls more of the fuel-system, calibration, and testing value chain toward ethanol-compatible components and validation.

- July 2024: TVS Mobility (TVS Group) formed a strategic alliance with Mitsubishi Corporation, with Mitsubishi investing INR 300 crore (about USD 40 million) into TVS Vehicles Mobility Solutions (TVS VMS) for a 32% stake. The investment bolstered capability-building in mobility services and distribution-oriented platforms adjacent to vehicle sales. It also highlighted expanding cross-border partnerships that connect Indian automotive groups with global capital and operational networks.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market means the total value generated from the manufacturing and sale of automobiles within India, counted at the vehicle level across major on-road categories and sales routes.

Scope exclusions: We exclude auto components-only revenues, aftermarket services, and fuels and charging sales unless they are bundled into the vehicle transaction value.

Segmentation Overview

- By Vehicle Type

- Two-wheelers

- Three-wheelers

- Passenger Cars

- Commercial Vehicles

- By Fuel Type

- Petrol / Gasoline

- Diesel

- LPG / CNG

- Battery Electric Vehicles

- Hybrid Electric Vehicles

- Plug-in Hybrid Electric Vehicles

- Fuel-Cell Electric Vehicles

- By Sales Channel

- OEM-Authorised Dealers

- Online

- By Ownership Type

- Personal Use

- Commercial Use

- By Region

- North India

- South India

- East India

- West India

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the boundary of what is counted as an automobile sale in India and to build the first set of demand and supply signals. We referenced public sources such as SIAM releases, Ministry of Road Transport and Highways vehicle registration dashboards, and policy updates from the Ministry of Heavy Industries to understand how volumes shift by category and by regulation.

To anchor pricing and mix shifts, we also used sources such as customs trade statistics for key vehicle and sub-assembly flows, RBI macro series for inflation and FX context, and peer reviewed articles that track electrification and ownership trends. Company filings, investor presentations, and reputed press were then used to cross-check capacity additions, product launches, and channel changes, and a paid subscription for India private company financials helped fill financial gaps for unlisted players where needed. These sources are illustrative and not exhaustive, and other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating the market boundary and the mix between two-wheelers, passenger cars, commercial vehicles, and three-wheelers, then pressure-testing ASP movements and dealer channel margins. We spoke with a spread of OEM side and downstream participants such as dealers, fleet operators, and financing and insurance linked stakeholders across India, so desk assumptions could be corrected where ground conditions differ by region.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 15% | |

| Mid tier: 44% | Functional/Unit leaders: 41% | |

| Smaller Players: 22% | Managers: 44% |

Market-Sizing & Forecasting

Sizing was started using a top-down build that reconstructs India vehicle demand from official registration and industry dispatch patterns, then translated into value using representative price bands and mix by category. We then used selective bottom-up approximations, mainly sampled model-wise ASP multiplied by volumes, dealer channel checks, and a roll-up of reported revenues for a subset of suppliers and assemblers, so the totals stayed realistic and were adjusted when gaps appeared.

Key inputs that shaped the model included new vehicle registrations and production dispatch trends, financing penetration and interest-rate sensitivity, EV adoption signals tied to policy and model availability, rural and urban road and infrastructure progress, and import-export movement for selected vehicle classes and assemblies. For forecasting, scenario analysis was used around consumer demand, fuel and powertrain mix, and credit availability, and then the final path was aligned to what interviewees considered the most likely case. Where bottom-up evidence was missing for smaller categories, we used conservative mix shares derived from published volume splits and validated the implied value per vehicle against the primary checks.

Data Validation & Update Cycle

Totals were validated through triangulation across independent signals, then reviewed for unusual jumps in mix, price, and implied revenue per vehicle. Any large variance versus registration, dispatch, or trade cues triggered a second pass on assumptions and a re-contact with selected interviewees before sign-off.

The report is refreshed annually, and interim updates are made when material events occur such as major policy shifts, sharp credit tightening, or significant production disruptions. Before delivery, a final analyst pass is completed so clients receive the latest market view with the same scope and steps applied consistently.

Mordor Intelligence's India Analysis of Automobile Market Sizing Compared With Other Published Estimates

Published market values for India automobiles often do not match because the boundaries and the year used for comparison are not the same across sources. Differences in whether estimates track registrations, dispatches, or broader mobility spend can also shift the reported total.

Registration and dispatch trends, along with category mix checks from primary conversations, are the evidence points that keep Mordor Intelligence tied to vehicle-level sales value in India, rather than a wider automotive spend bucket. Other estimates can move lower or higher when they start from a different base year, use a different currency timing, or apply a different ASP progression for two-wheelers versus passenger vehicles.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 137.06 B (2025) | |

| Industry Research Publisher A | USD 121.50 B (2024) | Uses an earlier reference year and a base-year setup that starts forecasting from 2024, which can understate the 2025 value when price and mix uplift is not carried through uniformly across vehicle categories. |

| Market Data Publisher B | USD 113.83 B (2024) | The published figure is anchored to a 2024 value and a longer horizon, and the scope can differ based on how the source treats revenue recognition and the split between vehicle sales value and adjacent automotive activity. |

Across the three figures, the spread mainly comes from year alignment and what is counted inside the automotive value pool. By keeping the scope at vehicle-level sales in India and checking the implied value against observable volume signals and interview feedback, the estimate stays explainable and repeatable for decision-making.

Key Questions Answered in the Report

What is the projected value of the India automobile market by 2031?

The India automobile market is forecast to reach USD 213.74 billion by 2031.

Which vehicle type is growing fastest in India?

Passenger cars are expanding at a 8.84% CAGR through 2031, making them the fastest-growing category.

Why is South India important for automakers?

South India offers integrated supply chains, skilled labor and EV-friendly policies, supporting a 9.18% regional CAGR to 2031.

How dominant are electric vehicles in India’s fuel mix?

Battery electric vehicles currently hold a modest share but are rising at a 10.02% CAGR owing to subsidies and charging build-out.

What is the market size in 2026?

USD 147.58 billion in 2026.

What challenges could slow market growth?

Tougher emission norms, semiconductor shortages and urban congestion policies may trim the market’s CAGR in the near term.

Page last updated on: