Stationary Lead-acid Battery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

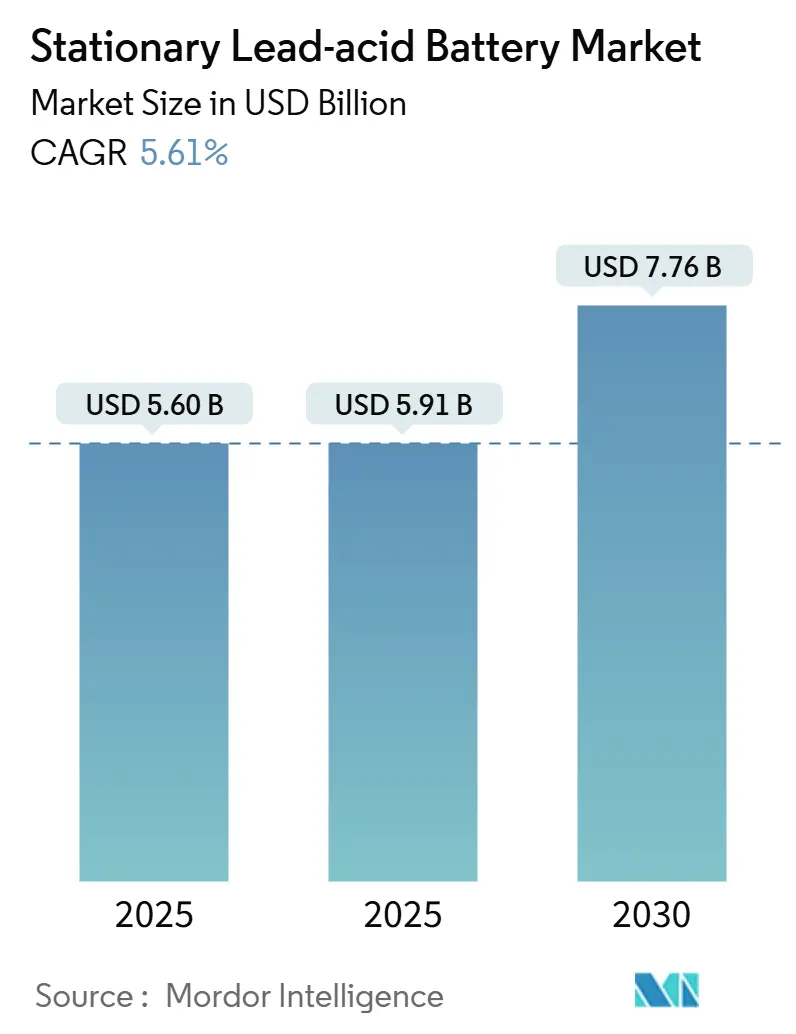

| Market Size (2026) | USD 5.91 Billion |

| Market Size (2031) | USD 7.76 Billion |

| Growth Rate (2025 - 2030) | 5.61% CAGR |

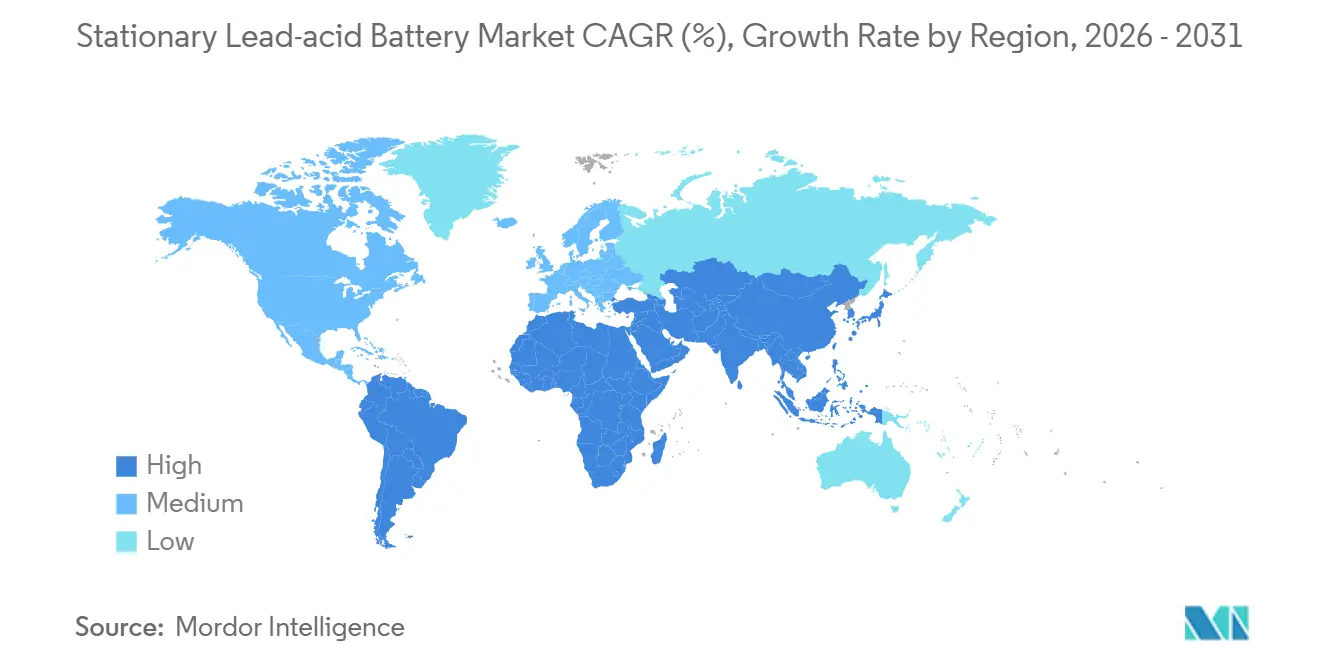

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stationary Lead-acid Battery Market Analysis by Mordor Intelligence

The Stationary Lead-acid Battery Market size is expected to increase from USD 5.60 billion in 2025 to USD 5.91 billion in 2026 and reach USD 7.76 billion by 2031, growing at a CAGR of 5.61% over 2026-2031.

Operators in data centers, telecom towers, and utility storage projects continue to select the chemistry because it delivers predictable performance, long float life, and a mature 99% recycling loop that already meets incoming EU rules. The January 2025 Moss Landing lithium-ion fire pushed hyperscale clients toward proven solutions that present no thermal-runaway risk. At the same time, flooded designs regain favor in high-temperature rooms after Pacific Gas & Electric reported elevated failure rates for sealed VRLA strings. Asia-Pacific anchors both supply and demand, yet the Middle East & Africa posts double-digit order books tied to new renewable roll-outs, signaling a broadening customer footprint for the stationary lead-acid battery market.

Financial incentives for domestic content in the United States and stricter recycling quotas in Europe reward manufacturers that control end-of-life streams, improving their margins even as raw-lead volatility persists. Mature safety codes, low total cost of ownership, and the ability to provide high surge currents keep the stationary lead-acid battery market embedded in mission-critical sites where downtime is not an option. Hybrid lead-carbon variants extend cycle life under partial state-of-charge duty, supporting renewable smoothing in cost-sensitive grids. Together, these forces protect lead chemistry from wholesale displacement by higher energy density rivals and sustain a steady multi-year growth runway.

Key Report Takeaways

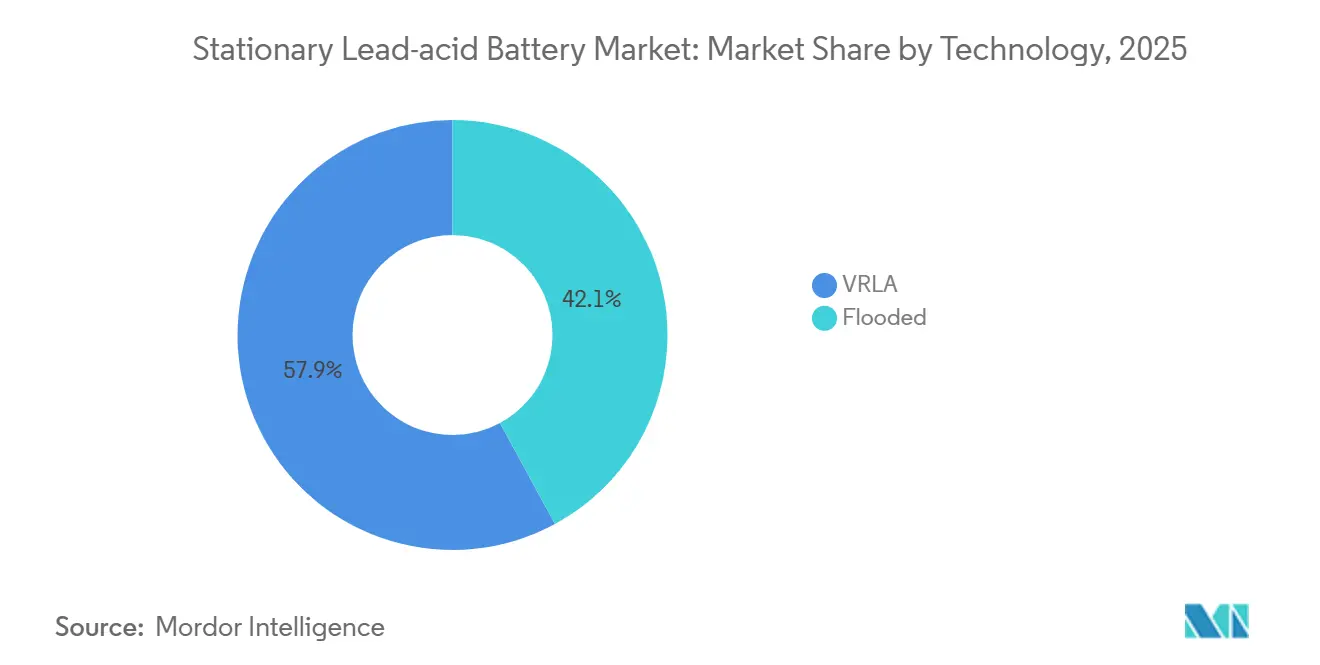

- By technology, VRLA batteries captured 57.9% of the stationary lead-acid battery market share in 2025, while flooded formats are projected to expand at a 6.8% CAGR through 2031.

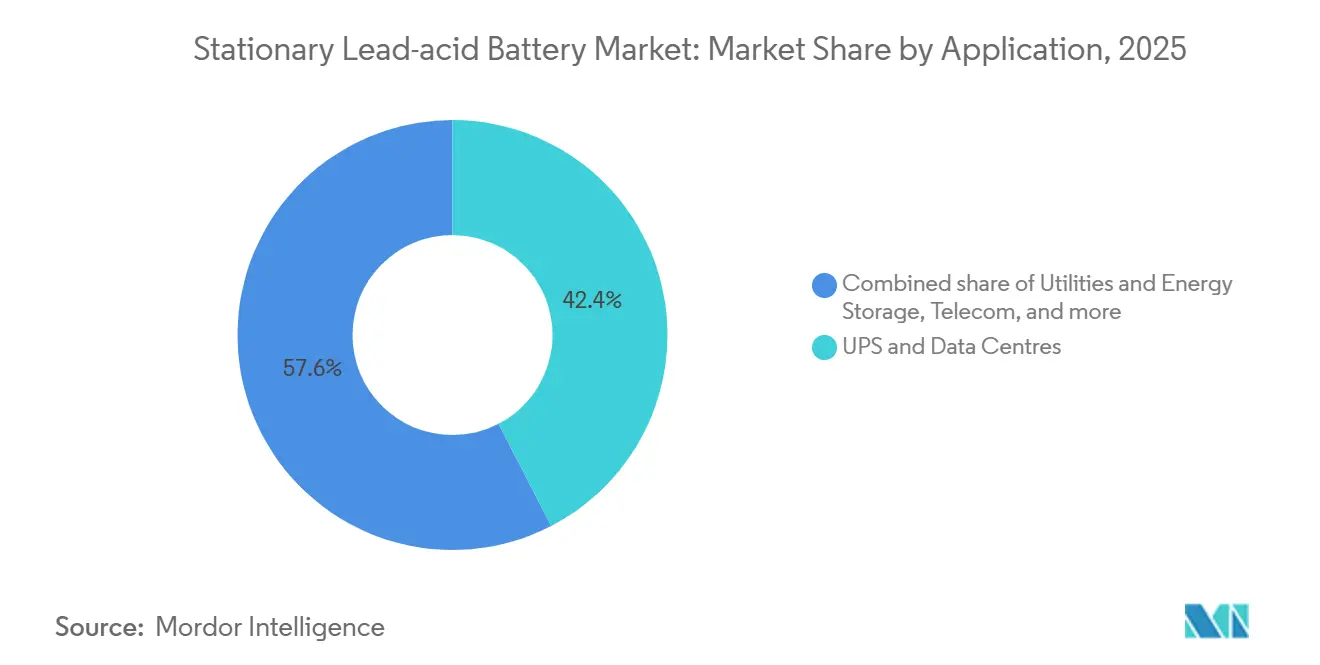

- By application, UPS and data-center systems commanded 42.4% of the stationary lead-acid battery market size in 2025, whereas utility and energy-storage projects are on track for an 8.1% CAGR between 2026-2031.

- By geography, Asia-Pacific generated 44.6% of 2025 revenue and is forecast to grow at a 6.0% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Stationary Lead-acid Battery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-center back-up renaissance | +1.2% | Global, with concentration in North America & Asia-Pacific | Medium term (2-4 years) |

| Telecom tower densification in rural Asia Pacific & Africa | +1.0% | Asia-Pacific core, spill-over to MEA | Short term (≤ 2 years) |

| Grid-scale renewable smoothing in cost-sensitive nations | +0.8% | Global, with early gains in South America & MEA | Long term (≥ 4 years) |

| Mining & oil-&-gas off-grid electrification mandates | +0.6% | MEA, South America, Australia & Canada | Medium term (2-4 years) |

| Safety-driven pivot from lithium in critical infrastructure | +0.4% | North America & EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Re-industrialisation programs in South America | +0.5% | South America, with secondary effects in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-center Back-Up Renaissance

Explosive growth in global data-center footprints has reset expectations for battery reliability. Operators now rank thermal stability above volumetric efficiency after the January 2025 Moss Landing incident damaged part of a 400 MW lithium-ion site, prompting California regulators to toughen safety inspections.[1]California Energy Storage Alliance, “Vistra Battery Blaze Spurs Review,” storagealliance.org EnerSys responded with high-rate flooded racks that integrate advanced monitoring firmware to guarantee 99.99% uptime without introducing fire-suppression retrofits. Survey data from the Uptime Institute shows 74% of hyperscale managers have added thermal-runaway scoring to procurement checklists, directly benefiting lead chemistry. Pacific Gas & Electric subsequently halted new sealed VRLA purchases for high-temperature rooms, citing superior longevity from ventilated flooded strings.

Telecom Tower Densification in Rural Asia-Pacific & Africa

Fifth-generation networks require dense tower grids, many in off-grid or weak-grid zones of India, Indonesia, and Nigeria. GSMA research confirms that 58% of rural base-stations in low-income countries remain diesel-battery hybrids, and more than 70% of those hybrids specify lead-acid packs for cost and maintenance simplicity. The Rockefeller Foundation identified telecom anchors as prime customers for mini-grid developers, kick-starting orders for 2 V industrial cells that handle deep daily cycles.[2]Rockefeller Foundation, “Mini-Grids and Telecom Synergies,” rockefellerfoundation.org Lead-acid tolerance for partial state of charge, high ambient heat, and rough handling keeps service intervals long, a decisive factor when sites are hundreds of kilometers from service hubs. This demand surge lifts regional shipment volumes and injects a full point of CAGR uplift into the global stationary lead-acid battery market.

Grid-Scale Renewable Smoothing in Cost-Sensitive Nations

Utilities in Brazil, South Africa, and Vietnam must integrate rising solar and wind output without over-building transmission. Levelized cost modeling by the U.S. Department of Energy places large lead-acid installations at USD 0.380 kWh by 2030, with paths to USD 0.097 kWh through improved current collectors and automated casting lines. Because duration rather than energy density drives four-hour applications, grid planners view lead solutions as bankable, recyclable, and financeable under multilateral lending terms. Brazil’s Powersafe plant pairs 10 MW of PV with containerized flooded strings, proving commercial viability in warm climates. An Inter-American Development Bank grant reinforces confidence, enabling replication across Latin America.

Mining & Oil-and-Gas Off-Grid Electrification Mandates

Commodity producers in the Pilbara, Québec, and the Atacama Desert confront decarbonisation mandates that require diesel offset. Heavy-duty VRLA banks in remote area power supply systems deliver 8-10 year life while coping with day-night thermal swings from -20 °C to 45 °C.[3]International Lead Zinc Research Organization, “RAPS System Longevity,” ilzro.org Clarios earmarked USD 1 billion for a U.S. metals-recovery hub to secure antimony and refine closed-loop alloy streams, insulating clients from price shocks. High surge currents for crusher and pump starts, along with simple field servicing, make flooded lead batteries the default choice.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Li-ion TCO parity below 5 kWh systems | -0.7% | Global, with early impact in North America & EU | Short term (≤ 2 years) |

| Stricter EU lead-recycling quotas hitting new capacity | -0.4% | EU core, regulatory spill-over to North America | Medium term (2-4 years) |

| Volatile lead prices squeezing OEM margins | -0.3% | Global | Short term (≤ 2 years) |

| Public-sector cap-ex deferrals post 2027 in MEA | -0.2% | MEA, with secondary effects in South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Li-ion TCO Parity Below 5 kWh Systems

Lithium-ion costs are falling fast enough to narrow the total-cost gap in small backup units. Argonne data place U.S. pack expenses at USD 86 kWh by 2035, and tax credits may trim that to USD 56 kWh by 2029.[4]Argonne National Laboratory, “Lithium-Ion Pack Cost Roadmap,” argonnelab.gov When installers compare a 3 kWh wall-mount set, the slimmer footprint, lower maintenance, and lighter structure all offset the lead’s lower sticker price. Chinese exporters already ship sub-USD 100 kWh cells despite tariffs, making swap-outs tempting for retail banking UPS rooms and emergency lighting arrays. Nature Energy modeling shows sodium-ion lines could join the contest after 2030, adding further margin strain. As a result, the stationary lead-acid battery market concedes share in light-duty categories even while holding ground in heavy float service.

Stricter EU Lead-Recycling Quotas Hitting New Capacity

Regulation 2023/1542 lifts the required recycling efficiency to 80% by 2030 and demands 95% lead recovery by 2031.[5]European Commission, “Battery Regulation 2023/1542,” europa.eu Integrated giants already run closed-loop smelters, but small assemblers face capital outlays for furnace upgrades, digital passports, and third-party audits. Minespider estimates IT compliance alone at EUR 1.7 million per midsize plant, enough to freeze expansion plans for several regional firms.

Segment Analysis

By Technology – Flooded Reliability Comeback

Flooded units controlled 42.1% of the stationary lead-acid battery market share in 2025 and are forecast to grow at a 6.8% CAGR. Pacific Gas & Electric’s decision to retire sealed VRLA strings in high-temperature rooms revived interest in vented designs that tolerate sustained 35 °C without capacity fade. The stationary lead-acid battery market size attached to flooded formats is projected at USD 3.48 billion by 2031, helped by thin-plate casting upgrades that slash water loss.

Advanced TPPL and lead-carbon hybrids sit between flooded robustness and VRLA convenience. They capture telecom shelters where partial-state cycling is routine, yet price premiums cap penetration. VRLA still owns the largest revenue pool at a 57.9% 2025 share, but its curve moderates as end-users accept limited onsite maintenance in exchange for longer service life from flooded racks. Continuous alloy R&D and automated formation lines should keep all three chemistries profitable, preserving breadth in the stationary lead-acid battery market.

Note: Segment shares of all individual segments available upon report purchase

By Application – UPS Dominance Mirrors Data-Center Surge

UPS rooms and data-center galleries held 42.4% of 2025 revenue and are expected to climb to 45.2% by 2031, tracking hyperscale square-foot growth of 12% yearly. The segment alone accounts for USD 3.52 billion of the projected stationary lead-acid battery market size in 2031. Operators choose high-rate flooded blocks that meet 15-minute ride-through specs and interface seamlessly with modern static switchgear.

Telecom backup remains essential yet slides from 27.8% to 25.6% share as tower consolidation tempers unit adds. Utilities and energy-storage arrays expand at an 8.1% CAGR because four-hour smoothing commands larger Ah totals per install. Mining, oil and gas, and motive-power niches post steady mid-single-digit gains, each reinforcing the diversified demand profile that underpins the stationary lead-acid battery market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific generated the largest 44.6% slice in 2025 as China, India, and ASEAN telecom operators stocked rural sites with 48 V racks. The stationary lead-acid battery market size in the region is forecast to surpass USD 3.5 billion by 2031 on a 6.0% CAGR. Stricter Chinese smelter standards turned the nation into a net refined-lead importer, tightening regional supply but boosting profits for integrated local brands. Japan and South Korea provide predictable replacement cycles in metro and rail projects, while Australian miners deploy heavy VRLA packs to electrify haul trucks and camps.

North America remains replacement-driven, tied to data-center rebuilds in Virginia and Texas and to hospital code upgrades. The Inflation Reduction Act adders reward domestically cast grids, enabling EnerSys to shift volumes from a closed Mexican site to new Pennsylvania lines. Europe concentrates on compliance. Recycling quotas spur Clarios and Exide to modernize German, Spanish, and Czech furnaces, locking in supply for OEM and stationary channels despite lower headline unit growth.

The Middle East & Africa posts the fastest 9.2% CAGR through 2031, chasing Saudi Arabia’s 48 GWh target and Egypt’s early standalone projects supported by AfDB finance. South Africa’s 1 GW storage awards and the UAE’s 800 MWh procurement illustrate breadth, yet fiscal risk lingers for post-2027 tenders. South America rides Brazil’s Mover program and private EV supply-chain commitments. Combined, these patterns underscore why the stationary lead-acid battery market continues spreading beyond its traditional strongholds.

Competitive Landscape

Incumbent strength rests with Johnson Controls, EnerSys, and Exide, which command 62% of global shipments through multi-continent factories and service crews. EnerSys spent USD 208 million on Bren-Tronics and secured a USD 199 million grant to erect a lithium-ion gigafactory, showing a hedge while retaining lead core cash flows. Exide automates casting lines in Spain and India to trim labor costs and defend margins when lead spikes. Clarios invests USD 1 billion in a U.S. critical-minerals hub to stabilize antimony and lead feedstock, insulating supply for AGM and flooded grids.

Regional challengers such as Narada, Stryten Energy, and Amara Raja pursue targeted niches. Narada bundles containerized telecom power in Southeast Asia, Stryten partners with Georgia Tech on R&D for next-gen lead chemistry, and Amara Raja licenses lithium-ion tech to broaden its catalog while defending VRLA volumes. Compliance with EU battery passports and U.S. domestic-content clauses creates cost hurdles for new entrants, tilting the field toward players able to absorb certification overhead.

Technology differentiation now lives in alloy mixes, carbon additives, and high-speed curing ovens rather than radical chemistry shifts. Automation, predictive analytics for service life, and vertically integrated recycling give scale leaders structural cost headroom. The stationary lead-acid battery marke, therefore, stays moderately concentrated yet competitive enough for pricing discipline to hold.

Stationary Lead-acid Battery Industry Leaders

East Penn Manufacturing Co.

EnerSys

GS Yuasa Corporation

Johnson Controls

Exide Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Clarios began site selection for a USD 1 billion U.S. recovery plant that targets improved recycling efficiency and reduced dependency on imported antimony.

- March 2025: Clarios announced a USD 6 billion American Energy Manufacturing Strategy to scale U.S. low-voltage battery output, including USD 2.5 billion for advanced production lines and USD 1.9 billion for critical minerals processing.

- August 2024: Clarios committed EUR 200 million to boost European AGM capacity by 50% between 2022 and 2026, creating 150 jobs across four countries.

- June 2024: Clarios completed a USD 16 million upgrade to its AGM component plant in South Carolina, expanding output for modern vehicles.

Global Stationary Lead-acid Battery Market Report Scope

The stationary lead-acid battery market report include:

| Flooded |

| VRLA |

| Telecom |

| UPS and Data Centres |

| Utilities and Energy Storage |

| Industrial Equipment and Motive Power |

| Oil and Gas and Mining |

| Security and Emergency Lighting |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Technology | Flooded | |

| VRLA | ||

| By Application | Telecom | |

| UPS and Data Centres | ||

| Utilities and Energy Storage | ||

| Industrial Equipment and Motive Power | ||

| Oil and Gas and Mining | ||

| Security and Emergency Lighting | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big will the stationary lead-acid battery space be in 2031?

Forecasts place revenue at USD 7.79 billion, up from USD 5.91 billion in 2026 on a 5.61% CAGR.

Which end-use accounts for the greatest demand today?

UPS and data-center backup rooms generate 42.4% of purchases thanks to hyperscale expansion.

Why are flooded designs regaining traction?

They tolerate higher ambient heat and deliver longer service life, addressing concerns raised by sealed VRLA failures.

What region shows the fastest expansion?

Asia-Pacific is projected to advance at a 6% CAGR through 2031 as governments add large renewable portfolios.

How does EU Regulation 2023/1542 affect suppliers?

It tightens recycling and digital-tracking rules, raising costs for small producers but favoring established firms with in-house smelters.

Will lithium-ion replace lead in small UPS units?

Rapid cost declines mean lithium-ion reaches total-cost parity below 5 kWh by 2029, so substitution is likely in compact systems even as lead remains preferred for large, fire-sensitive sites.