Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 9.16 Billion |

| Market Size (2026) | USD 9.49 Billion |

| Market Size (2031) | USD 11.46 Billion |

| Growth Rate (2026 - 2031) | 3.84% CAGR |

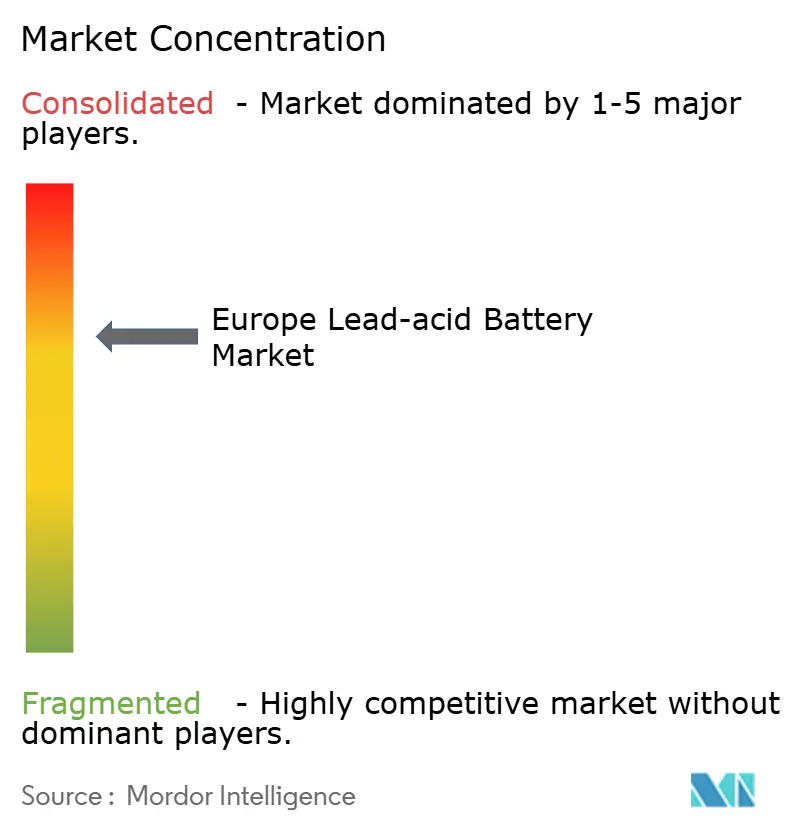

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Lead-acid Battery Market Analysis by Mordor Intelligence

The Europe Lead-acid Battery Market size is expected to increase from USD 9.16 billion in 2025 to USD 9.49 billion in 2026 and reach USD 11.46 billion by 2031, growing at a CAGR of 3.84% over 2026-2031. Structural demand tied to internal-combustion and hybrid vehicles, telecom backup, and warehouse automation continues to underpin growth despite lithium-ion cost compression. Starting-lighting-ignition (SLI) requirements remain dominant because 83% of new European cars sold in 2025 still use engines that need a high-cranking auxiliary battery. Stationary installations for data centers and 5G towers are rising faster than the headline rate, leveraging valve-regulated designs that deliver maintenance-free service at a lower upfront cost than lithium-ion. Meanwhile, the EU Batteries Regulation 2023/1542 codifies a 99% collection and recycling infrastructure, locking in a circular-economy moat that favors the European lead-acid battery market over chemistries with nascent recovery channels.[1]European Commission, “Regulation (EU) 2023/1542,” europa.eu

Key Report Takeaways

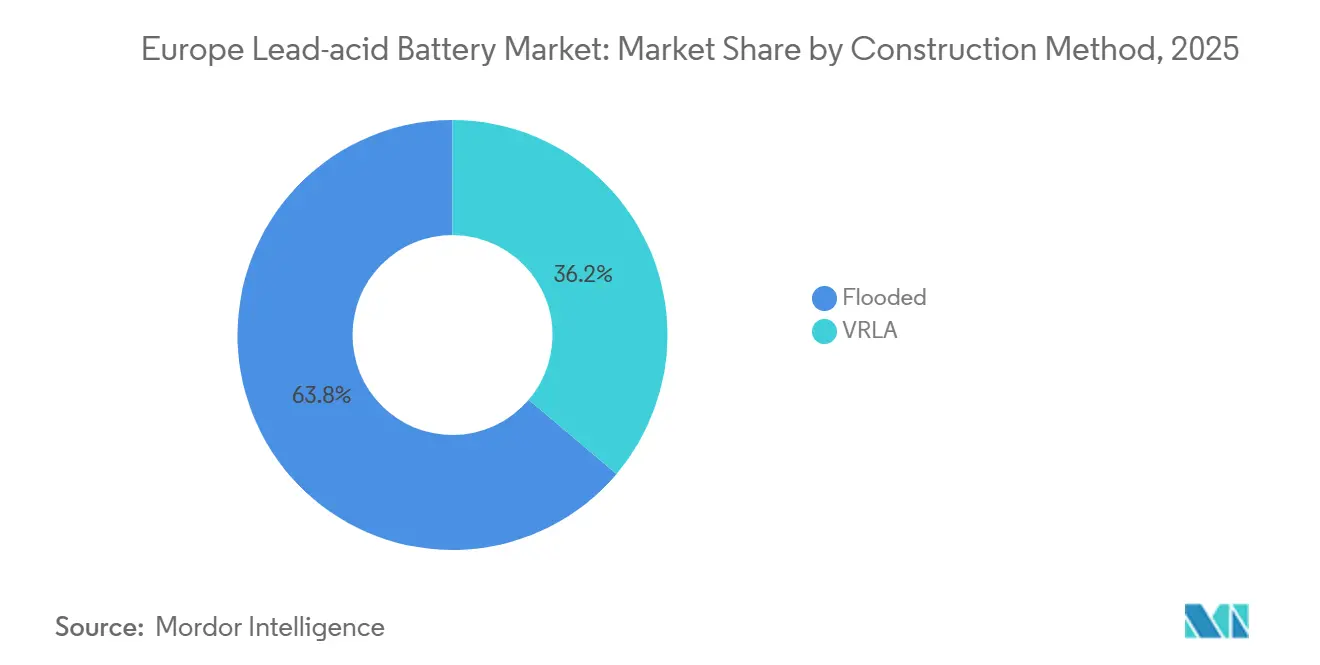

- By construction method, flooded batteries led with 63.8% of the European lead-acid battery market share in 2025, while valve-regulated types are projected to expand at a 6.1% CAGR to 2031.

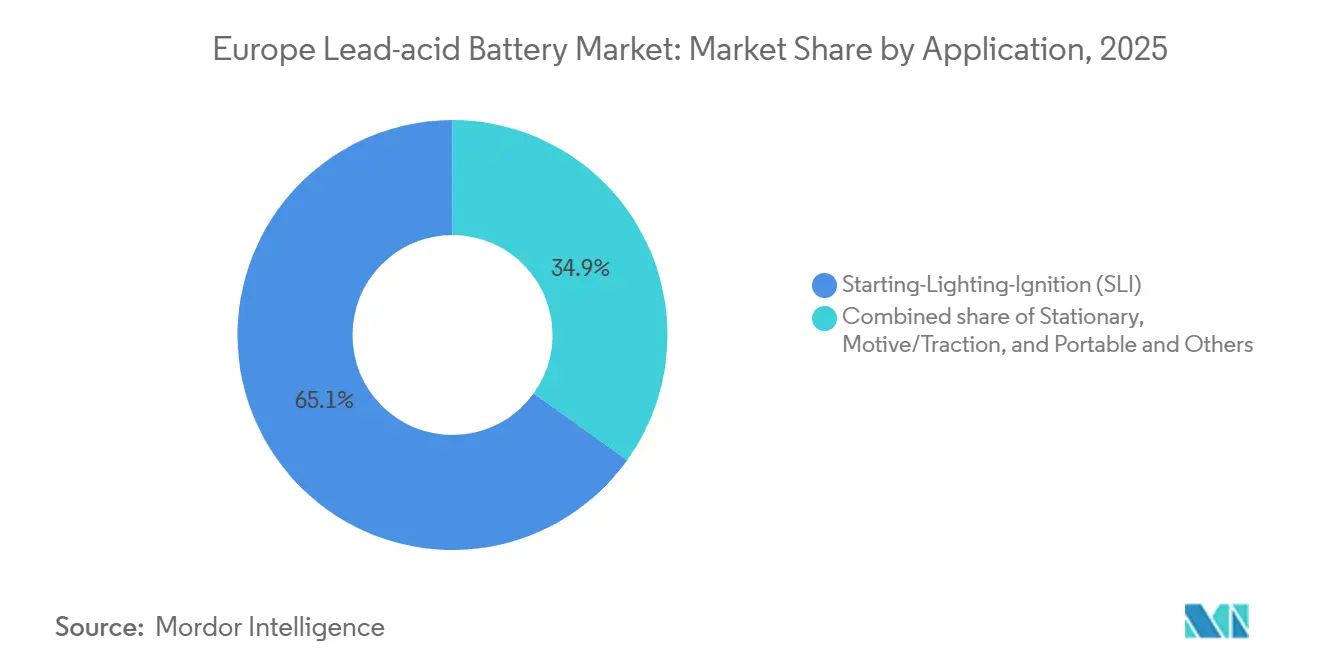

- By application, SLI accounted for 65.1% of the European lead-acid battery market size in 2025, and stationary systems are advancing at a 7.2% CAGR through 2031.

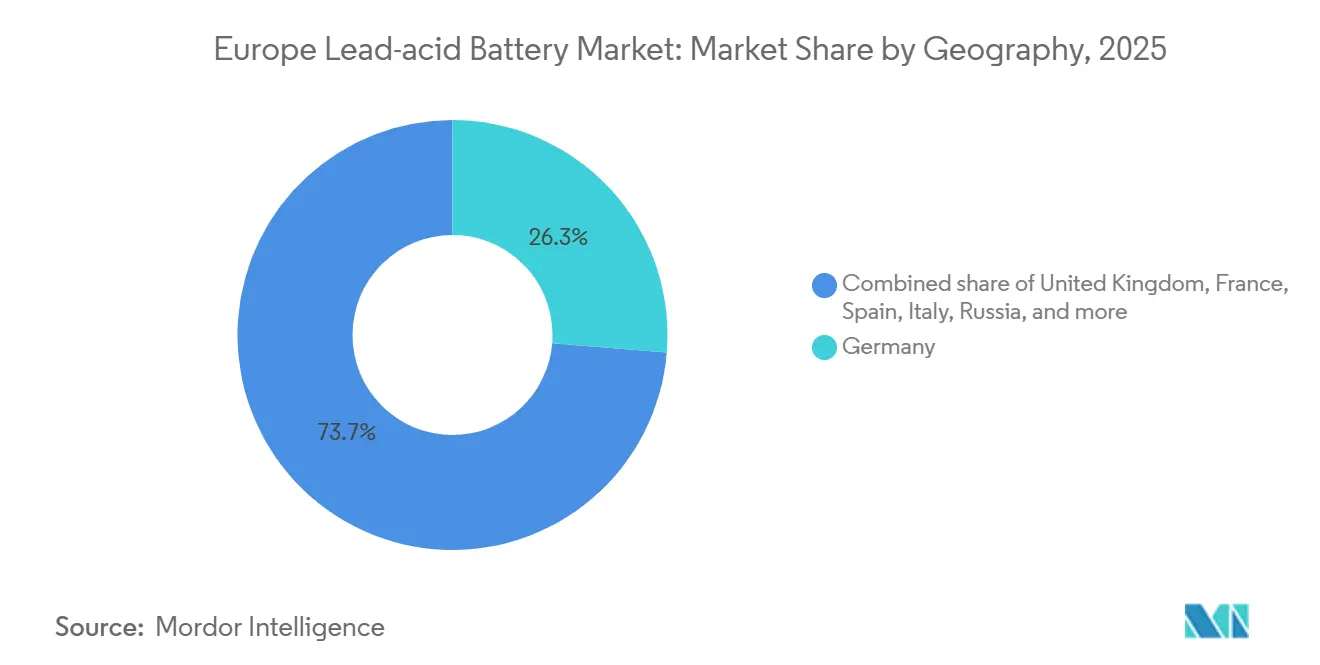

- By geography, Germany contributed 26.3% of revenue in 2025, whereas Spain recorded the fastest 6.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Lead-acid Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising sales of ICE & micro-hybrid vehicles | +1.2% | Germany, Italy, Eastern Europe (Russia, Poland, Czech Republic) | Medium term (2-4 years) |

| Expanding data-center & UPS installations | +0.9% | Germany, France, UK, Netherlands (Frankfurt, Amsterdam, London hubs) | Long term (≥ 4 years) |

| EU directives driving residential solar-plus-storage | +0.7% | Spain, Italy, Germany (residential and small-commercial segments) | Medium term (2-4 years) |

| Warehouse automation boosting motive-power demand | +0.5% | Germany, Netherlands, France (logistics and manufacturing hubs) | Long term (≥ 4 years) |

| Partial-state-of-charge lead-carbon advances | +0.4% | Spain, Germany, UK (grid-stabilization and solar applications) | Long term (≥ 4 years) |

| EU circular-economy rules favouring 99% recyclability | +0.3% | Europe-wide (regulatory compliance and supply-chain resilience) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Sales of ICE and Micro-hybrid Vehicles

Internal-combustion and hybrid drivetrains represented 83% of European new-car registrations through November 2025, preserving a wide installed base that must replace auxiliary batteries every 4-6 years. Germany produced 4.1 million vehicles in 2024, most of which integrate 48-volt mild-hybrid systems needing advanced flooded or absorbed-glass-mat (AGM) units. Russia’s 1.47 million light-vehicle sales in 2024 showed battery-electric penetration below 1%, extending demand for conventional SLI batteries across Eastern Europe. Italy reported only a 4.2% battery-electric share in 2024, highlighting regional divergence that benefits the European lead-acid battery market. A fleet age near nine years across the continent sustains predictable aftermarket cycles.

Expanding Data-center and UPS Installations

European data-center capacity reached 10 GW in 2024 and is growing 8-10% annually as cloud and edge operators scale facilities in Frankfurt, Amsterdam, London, and Paris.[2]CBRE, “Europe Data Centre MarketView Q4 2025,” cbre.com Valve-regulated lead-acid (VRLA) batteries still dominate roughly 80% of UPS deployments where backup duration is under 15 minutes and cost discipline outweighs lithium-ion’s energy-density advantage. Telecom carriers operate about 500,000 tower sites and will add 100,000 5G small cells by 2025, each relying on 48-volt VRLA strings tolerant of temperature swings.[3]GSMA Intelligence, “Europe 5G Roll-out Tracker 2025,” gsma.com New pure-lead AGM designs extend cycle life by 20% in partial-state-of-charge duty, reducing total cost for operators. Edge data centers that support latency-sensitive workloads favor sealed units requiring no active ventilation.

EU Directives Driving Residential Solar-plus-storage

Royal Decree-Law 7/2025 earmarked EUR 700 million for standalone batteries in Spain and mandated flexibility services that encourage behind-the-meter adoption.[4]Ministry for the Ecological Transition – Spain, “Royal Decree-Law 7/2025,” boe.es Twenty-six percent of Spanish rooftop PV installs in 2024 already included storage, and many chose VRLA because of lower acquisition cost and simpler recycling logistics. Germany’s amended Renewable Energy Sources Act now allows virtual power-plant aggregation, expanding revenue streams for residential batteries. Italy’s Superbonus tax credit covers 110% of energy-efficiency spending, pushing uptake among households in regions with unreliable grids. EU regulation requiring 85% recycled lead content by 2031 strengthens the European lead-acid battery market’s positioning in distributed storage.

Warehouse Automation Boosting Motive-power Demand

Automated guided vehicles and autonomous mobile robots are proliferating in European warehouses that serve automotive, food, and e-commerce sectors. These platforms cycle batteries several times a day and value chemistries that handle opportunity charging without degradation. Lead-carbon and advanced flooded traction batteries can deliver 1,500-2,000 deep cycles at cost levels still below lithium-ion. ISO 3691-4 safety certification, mandatory for automated forklifts, favors suppliers with decades of field data and limits new entrants. Robotics-as-a-service contracts bundle batteries into monthly fees, amplifying the installed base for VRLA designs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid cost decline of Li-ion chemistries | -1.1% | Western Europe (Germany, France, UK) for stationary and premium automotive | Short term (≤ 2 years) |

| Stringent lead-emission limits & compliance costs | -0.6% | Europe-wide (manufacturing facilities under REACH Directive 98/24/EC) | Medium term (2-4 years) |

| Tight supply of high-purity primary lead concentrate | -0.3% | Europe-wide (manufacturers reliant on mined concentrate vs. recycled streams) | Medium term (2-4 years) |

| Growing OEM trials of solid-state starter batteries | -0.2% | Germany (premium automotive OEMs: BMW, Mercedes-Benz, Volkswagen) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Cost Decline of Lithium-ion Chemistries

Lithium-ion pack prices slipped below USD 140 per kWh in 2023 and are set to fall another 40% by 2030, narrowing the total-cost-of-ownership gap with VRLA in many stationary uses. Hyperscale operators in Frankfurt and Amsterdam already specify lithium-ion backup for new builds to gain 15-year life and 80% depth of discharge. Spain’s 10.5 GW utility-scale battery pipeline is almost entirely lithium-ion for two-to-four-hour energy-shifting projects, sidelining lead-acid to shorter-duration roles. Plunging lithium-carbonate prices removed a materials-cost advantage that previously supported the European lead-acid battery market. Even so, cold-weather performance and recycling leadership preserve defensible niches.

Stringent Lead-emission Limits and Compliance Costs

EU REACH Directive 98/24/EC caps workplace lead exposure at 0.15 mg/m³ over eight hours, compelling factories to invest EUR 5 million to EUR 15 million each in filtration and closed-loop handling. The EU Batteries Regulation now demands 90% lead recovery by 2027 and 95% by 2031, plus 85% recycled content in new batteries. Integrated players like Clarios mitigate these costs through captive recycling assets, but smaller firms dependent on primary concentrate face squeezed margins, especially with mined lead trading near USD 2,400 per tonne in 2024. Non-compliance can trigger EUR 500,000 fines in markets such as Germany, raising barriers for new entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Construction Method: Flooded Designs Dominate Volume, VRLA Drives Growth

Flooded products delivered 63.8% revenue in 2025, thanks to cost-focused automotive aftermarket buyers who replace SLI units every four to six years. VRLA, encompassing AGM and gel types, is growing 6.1% annually as telecom carriers and data centers prioritize sealed operation and reduced ventilation demands. Flooded technology continues to refine calcium-silver grids that extend micro-hybrid start-stop life to 300,000 cycles. AGM already holds 25% of premium SLI demand and benefits from EUR 200 million of new capacity added by Clarios in Hanover, Zwickau, and Spain. Gel variants, though smaller in absolute volume, win share in solar-storage and marine segments where vibration resistance and deep-discharge capability justify higher price points.

Advanced flooded traction batteries remain entrenched in forklifts across German, Dutch, and French logistics hubs that rely on established charging rooms. The EU’s 85% recycled-content mandate poses no hurdle to either construction type because the European lead-acid battery market already meets a 99% collection and recycling rate, whereas lithium-ion recyclers remain in early scale-up stages.

By Application: SLI Resilience Meets a Stationary Surge

SLI batteries retained a 65.1% share of the European lead-acid battery market size in 2025, underpinned by an 83% share of internal-combustion and hybrid powertrains in new European registrations. Vehicle age near nine years ensures steady aftermarket rotation, and cold-cranking performance continues to favor lead-acid in Nordic climates. Stationary systems are advancing 7.2% per year as data-center capacity climbs and telecom operators add 100,000 5G small cells. VRLA accounts for 80% of UPS cabinets because a five-to-seven-year service life at low cost still outweighs lithium-ion’s density advantage for short-duration backup. Residential solar-plus-storage in Spain and Italy provides another growth pocket, where lead-carbon variants can offer 1,500-2,000 deep cycles for households averse to lithium-ion premiums. Motive-power batteries for forklifts, golf carts, and automated-guided vehicles hold a mid-teens share, supported by ISO 3691-4 certified designs proven in demanding warehouse duty.

Geography Analysis

Germany led the European lead-acid battery market with 26.3% of revenue in 2025, supported by 4.1 million vehicles produced in 2024 and an installed parc of 48 million cars averaging 10 years old. Tier-1 suppliers such as Clarios and Bosch are adding AGM lines that lift micro-hybrid supply security. Spain is the fastest-growing country at 6.8% CAGR through 2031. A 10.5 GW standalone battery pipeline, a new capacity market in 2025, and EUR 700 million in EU FEDER funding are catalyzing both utility-scale and residential storage. The United Kingdom posted 1.95 million light-vehicle registrations in 2024, with 65% still relying on engines that require SLI batteries, while France’s 39-million vehicle parc guarantees replacement demand despite rising hybrid uptake. Italy’s 4.2% battery-electric share, the lowest among large markets, underscores Southern Europe’s slower electrification path, which benefits flooded and AGM products.

Nordic countries highlight lead-acid’s cold-weather resilience, as winter temperatures of -20 °C to -40 °C cut lithium-ion capacity up to 40%, sustaining replacement business across Norway’s 2.8 million engine vehicles. Eastern European markets such as Poland, the Czech Republic, and Russia remain cost-sensitive; Russia’s 1.47 million car sales in 2024 had sub-1% electric penetration, preserving a multi-year window for SLI volume growth. Rest-of-Europe territories in the Balkans and Baltics add mid-single-digit share and follow EU regulatory harmonization that entrenches high recycling rates.

Competitive Landscape

Competition is moderate. The top three suppliers, Clarios, Exide Technologies, and GS Yuasa, hold 55-60% of regional sales through vertical integration in recycling, proprietary alloy chemistries, and long-term OEM contracts. Clarios bought three Ecobat recycling plants in Germany and Austria in August 2025, integrating 150,000 tonnes of annual secondary lead and meeting future 85% recycled-content rules in advance. EnerSys grew thin-plate pure-lead capacity to USD 1.4 billion equivalent by 2025 and focuses on data-center UPS and telecom segments. Mid-tier firms, Banner, FIAMM, Hoppecke, and BAE, carve out niches: Banner in premium aftermarket, FIAMM leveraging Italian cost structures, and Hoppecke dominating industrial traction with ISO-certified batteries.

Chinese entrants such as Narada Power and Leoch International target Eastern Europe, where environmental enforcement is lighter, shifting price dynamics for cost-focused buyers. Technology differentiation centers on calcium-silver grids that boost start-stop life tenfold compared with standard flooded designs, justifying 15-20% premiums. Compliance with EU REACH air-quality limits requires heavy capex, favoring incumbents able to amortize environmental systems. Primary-lead deficits reported by the International Lead and Zinc Study Group keep raw-material volatility high, further rewarding firms with in-house recycling.

Europe Lead-acid Battery Industry Leaders

Clarios (ex-Johnson Controls)

Exide Technologies

EnerSys

GS Yuasa

Banner GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The European Commission unveiled its "Battery Booster Strategy," marking a significant step for the European lead-acid battery industry. This initiative aims to bolster battery manufacturing, enhance recycling efforts, and fortify the supply chain across Europe. As a result, both advanced lead batteries and various other chemistries—crucial for automotive, industrial backup power, and energy-storage applications—stand to gain.

- August 2025: Ecobat, a battery recycling company, has agreed to sell its German and Austrian operations to energy storage firm Clarios, reflecting the industry's shift toward EV battery recycling amid growing demand.

- March 2025: CS VRLA AGM Batteries Set Sail for Europe, ensuring reliable backup power solutions. A fresh consignment of CS Series VRLA AGM batteries has been successfully loaded and is now on its way to Europe. These high-performance batteries are designed to provide exceptional reliability and extended lifespan, making them the ideal choice for backup power applications.

Europe Lead-acid Battery Market Report Scope

The lead-acid battery is a rechargeable battery that consists of two electrodes submerged in an electrolyte of sulfuric acid. The positive electrode is made of grains of metallic lead oxide, while the negative electrode is attached to a grid of metallic lead.

The European lead-acid battery market is segmented by construction method, application, and geography. By construction method, the market is segmented into flooded and VRLA. By application, the market is segmented into SLI, stationary, motive/traction, and portable and others. The report also covers the market size and forecasts for the European lead-acid battery market across major countries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Construction Method

| Flooded |

| VRLA |

By Application

| Starting-Lighting-Ignition (SLI) |

| Stationary |

| Motive/Traction (Forklifts, Golf-carts) |

| Portable and Others |

By Geography

| Germany |

| United Kingdom |

| France |

| Spain |

| Italy |

| NORDIC Countries |

| Russia |

| Rest of Europe |

| By Construction Method | Flooded |

| VRLA | |

| By Application | Starting-Lighting-Ignition (SLI) |

| Stationary | |

| Motive/Traction (Forklifts, Golf-carts) | |

| Portable and Others | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe lead-acid battery market today?

The market stood at USD 9.49 billion in 2026 and is on track to reach USD 11.46 billion by 2031 at a 3.84% CAGR.

Which application segment is growing fastest?

Stationary systems for telecom, data centers, and residential backup are expanding at 7.2% per year, outpacing overall market growth.

Why does lead-acid remain competitive against lithium-ion?

Superior cold-cranking performance, a 99% recycling rate already aligned with EU regulations, and lower upfront cost keep lead-acid attractive in many use cases.

Which country will add the most incremental demand?

Spain, supported by a 6.8% CAGR and 10.5 GW of planned storage projects, will add the largest incremental revenue through 2031.

Who are the market leaders?

Clarios, Exide Technologies, and GS Yuasa control roughly 55-60% of regional sales through integrated recycling and long-term OEM contracts.

What regulation shapes the market outlook?

EU Regulation 2023/1542 mandates 85% recycled lead content and up to 95% recovery efficiency by 2031, reinforcing the circular advantages of lead-acid systems.

Page last updated on: