Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

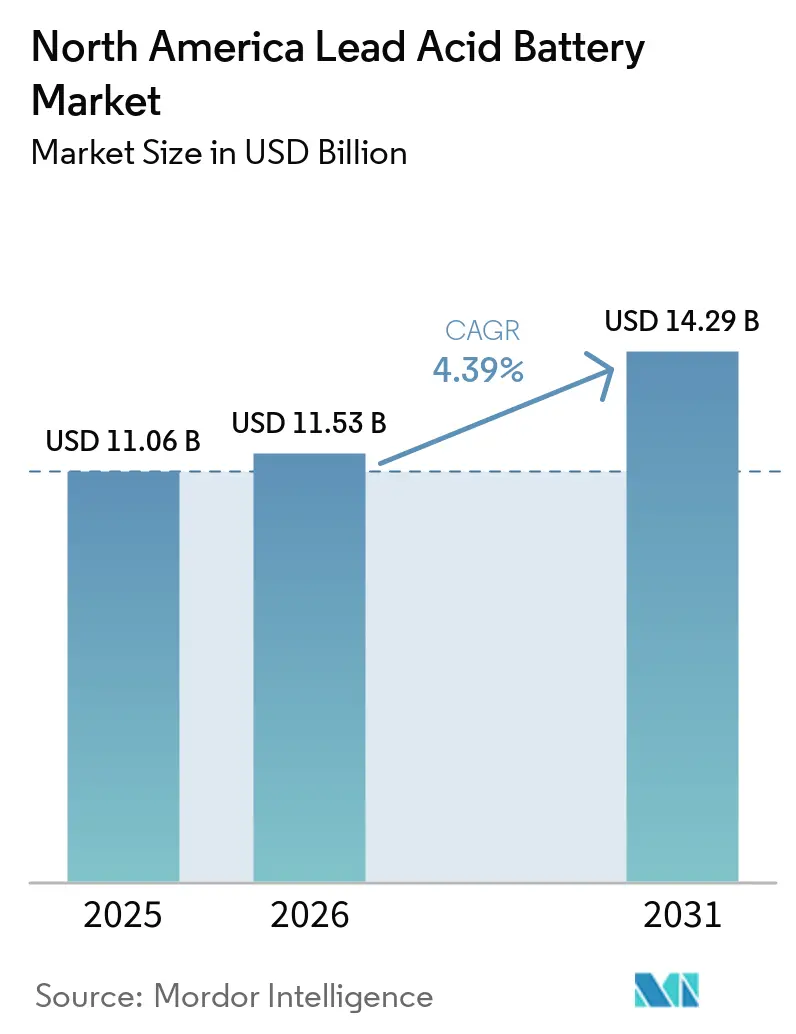

| Base Year Market Size (2025) | USD 11.06 Billion |

| Market Size (2026) | USD 11.53 Billion |

| Market Size (2031) | USD 14.29 Billion |

| Growth Rate (2026 - 2031) | 4.39% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Lead-Acid Battery Market Analysis by Mordor Intelligence

The North America Lead-Acid Battery Market size is expected to increase from USD 11.06 billion in 2025 to USD 11.53 billion in 2026 and reach USD 14.29 billion by 2031, growing at a CAGR of 4.39% over 2026-2031. The steady pace reflects a mature ecosystem balancing two cross-currents: a dependable replacement cycle linked to the aging internal-combustion vehicle fleet and a wave of stationary power investments, even as lithium-ion makes inroads in multi-shift industrial use cases and environmental oversight tightens. The average age of U.S. light vehicles hit 12.6 years in 2024, locking in frequent SLI battery swaps that anchor more than half of regional volume.[1]Associated Equipment, “Know Your Power: State of the Automotive Battery Industry,” associatedequipment.com At the same time, hyperscale data-center developers and 5G carriers are installing uninterruptible-power-supply (UPS) systems at unprecedented speed, a sweet spot where valve-regulated lead acid (VRLA) batteries still enjoy cost and recycling advantages despite lithium-ion’s narrowing total cost-of-ownership (TCO) gap.[2]International Energy Agency, “Electricity 2024,” iea.org Competitive dynamics remain intense as the leading producers Clarios, EnerSys, C&D Technologies Inc, Leoch International Technology Limited, and GS Yuasa Corporation control roughly two-thirds of production capacity and routinely deploy vertical integration to blunt raw-material volatility.[3]Clarios, “U.S. Investment Announcement,” clarios.com

Key Report Takeaways

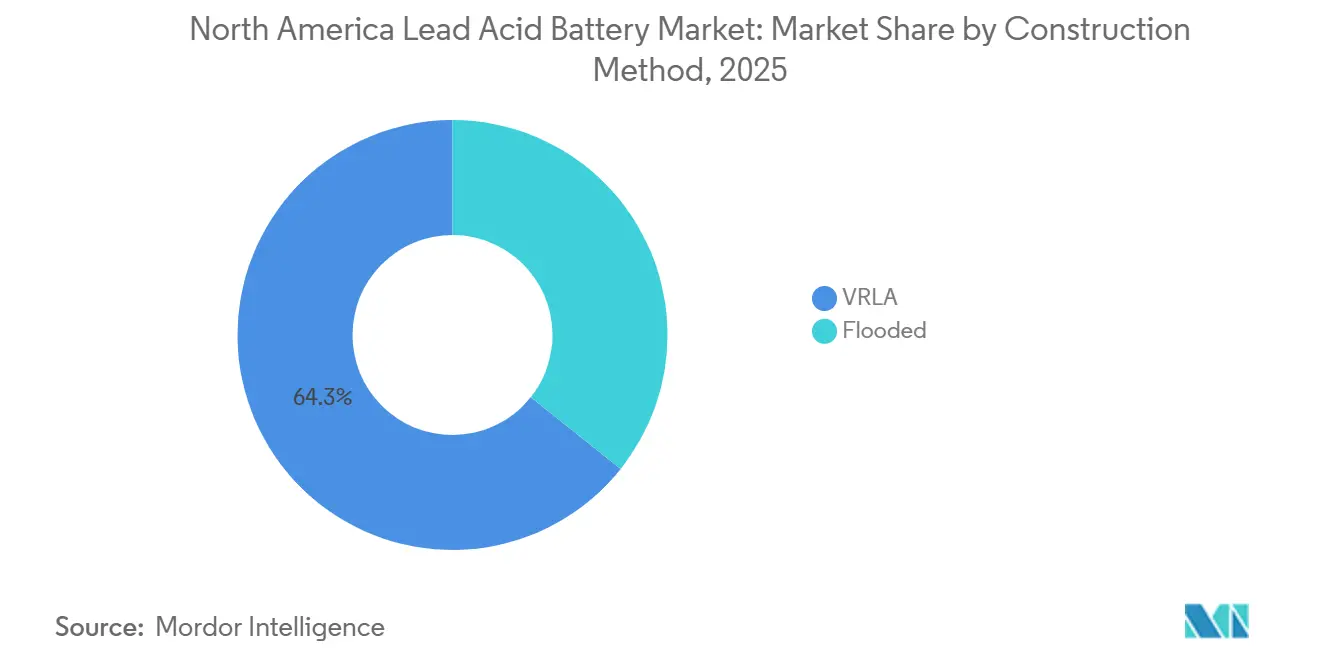

- By construction method, VRLA controlled 64.3% of the North America Lead-Acid Battery Market share in 2025 and is expected to advance at a 5.7% CAGR through 2031.

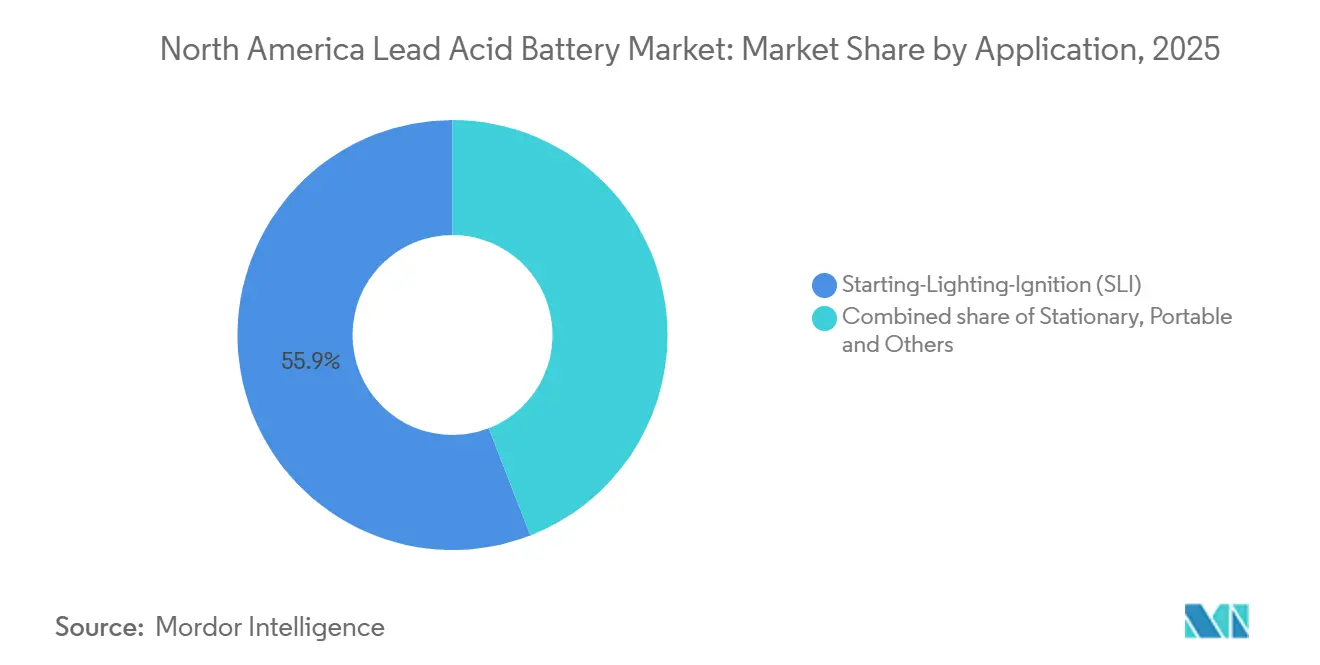

- By application, starting-lighting-ignition controlled 55.9% of the North America Lead-Acid Battery Market share in 2025, while stationary is projected to advance at a 6.4% CAGR through 2031.

- By geography, the United States controlled 73.6% of the North America lead acid battery share in 2025, while Canada is expected to advance at a 5.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Lead-Acid Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Replacement demand from aging ICE-vehicle fleet | +1.2% | United States (primary), Canada, Mexico | Long term (≥ 4 years) |

| Data-center & telecom UPS expansion boom | +0.9% | United States (hyperscale clusters), Canada (edge deployments) | Medium term (2–4 years) |

| Cost competitiveness vs. lithium alternatives in SLI use-cases | +0.5% | United States, Mexico (aftermarket concentration) | Long term (≥ 4 years) |

| 48V mild-hybrid auxiliary battery adoption | +0.4% | United States, Mexico (OEM production hubs) | Medium term (2–4 years) |

| Lead-carbon batteries for remote micro-grids (Canada Arctic, off-grid mining) | +0.3% | Canada (Arctic, remote mining), Alaska (off-grid communities) | Long term (≥ 4 years) |

| Closed-loop recycling mandates accelerating domestic supply security | +0.6% | United States (EPA EPR framework), Canada (provincial EPR) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Replacement Demand from Aging ICE-Vehicle Fleet

The U.S. fleet’s record 12.6-year average age underpins a structural replacement wave because vehicles 11 years or older post a 37% annual battery swap rate. Battery Council International tracked 159 million lead acid units shipped in 2024, the bulk tied to replacement rather than factory-install volume.[4]Battery Council International, “Battery Shipments and Market Data,” batterycouncil.org Growing electrical loads from start-stop technology and driver-assistance features hasten the shift from flooded batteries to absorbed-glass-mat (AGM) VRLA designs, which S&P Global projects will reach 19% of all aftermarket installs by 2027. O’Reilly Auto Parts named East Penn its 2025 Supplier of the Year after the vendor scaled DIN-size AGM output that could cover over 40% of vehicles in operation. Crucially, rural and lower-income buyers who retain internal-combustion vehicles longer slow EV cannibalization, extending the tail of the North America Lead-Acid Battery Market.

Data-Center & Telecom UPS Expansion Boom

Hyperscale builds to serve artificial-intelligence workloads are lifting global data-center electricity demand toward 945 TWh by 2030, up from 460 TWh in 2022. VRLA batteries, especially AGM variants, still held 58% of the USD 4.33 billion global UPS battery segment in 2025. Texas Senate Bill 6 of 2024 requires on-site backup, which is spurring retrofit purchases even while greenfield projects choose lithium-ion for densification advantages. 5G tower roll-outs likewise favor VRLA at remote sites where sealed, maintenance-free units cut service visits. Although lithium-ion offers a 39% lower 10-year TCO, capital budgets and well-established recycling channels preserve VRLA relevance across a large installed base.

48 V Mild-Hybrid Auxiliary Battery Adoption

Automakers use 48 V systems to meet fuel-economy targets at modest cost, and many North American platforms specify lead acid for the auxiliary pack to protect margins on pickups and SUVs. The global 48 V lead acid sub-segment reached USD 2.5 billion in 2025. Clarios added 1.5 million low-antimony AGM units in 2024 and will open a 745,000-unit plant in Toledo, Ohio, in 2026, focused on this niche. The incremental volume extends service-life replacement demand through the early 2030s, cushioning the North America Lead-Acid Battery Market against pure EV substitution.

Closed-Loop Recycling Mandates Accelerating Supply Security

Lead acid enjoys a 99% U.S. recycling rate, and forthcoming federal extended-producer-responsibility rules slated for 2025-2027 aim to codify collection requirements. More than 80% of a new battery’s lead content already comes from recycled stock, dampening exposure to primary-lead price swings. State stewardship laws in California and the Northeast further formalize take-back programs, while only 30,000 tons still enter landfills annually, volumes likely to shrink as enforcement tightens.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid cost decline of lithium-ion packs | -0.8% | United States (data centers, forklifts), Canada (material handling) | Short term (≤ 2 years) |

| Environmental & health concerns over lead toxicity | -0.4% | United States, Canada (public health advocacy, ESG procurement) | Medium term (2–4 years) |

| Impending tighter U.S. EPA ambient-lead limits | -0.5% | United States (secondary smelter concentration zones) | Medium term (2–4 years) |

| Recycled-lead supply volatility from scrap-export flows | -0.4% | United States (import dependency), Mexico (scrap-export dynamics) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Cost Decline of Lithium-Ion Packs

DOE data show lithium-ion pack prices fell to USD 128-133 per kWh in 2024 from USD 150 per kWh in 2022, an 85% drop versus 2014 levels. In UPS service, that translates to a 39% lower 10-year TCO relative to VRLA, thanks to 8–15 year service life and 3,000–5,000 charge cycles. Forklift fleets mirror the shift: lithium-ion units recharge in 1-2 hours and deliver up to 4,000 cycles, saving on battery-swap rooms and spare-pack inventory. Global lithium-ion penetration in electric forklifts could jump from 32% in 2024 to over 70% by 2034, with the U.S. lagging because 50–60% of facilities still need costly electrical upgrades. Nonetheless, once upfront cost parity is crossed, lead acid must lean on its safety and circular-economy image to defend share in high-utilization segments.

Environmental & Health Concerns over Lead Toxicity

EPA’s October 2025 proposed amendments to the National Emission Standards for Hazardous Air Pollutants stop short of mandating wet electrostatic precipitators but impose new hydrocarbon, dioxin, and carbonyl-sulfide limits on the 11 U.S. secondary smelters. Compliance could lift lead acid unit costs by 2–3%, chipping away at its pricing edge. Public-health advocates also press for siting restrictions near residential zones, and hyperscale data-center operators with ESG pledges increasingly prefer lithium-ion UPS solutions despite higher capex. The regulatory trajectory, therefore, exerts a gradual but persistent drag on the North America Lead-Acid Battery Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Construction Method: VRLA Ascendancy Bolstered by Maintenance-Free Design

VRLA units captured 64.3% of the North America Lead-Acid Battery Market in 2025 and are expected to compound at 5.7% annually through 2031, outpacing conventional flooded cells. This leadership stems from sealed architectures that eliminate watering labor, reduce gas emissions, and simplify compliance with OSHA indoor-air rules. Within VRLA, AGM variants command momentum because faster charge acceptance slashes turnaround time for delivery vans and ride-hail vehicles that cycle hundreds of times per year. EnerSys invested USD 6.7 million in Sumter, South Carolina, during 2025 to expand thin-plate-pure-lead (TPPL) and AGM lines that promise 8–10 year life versus 3–5 years for flooded rivals.

Flooded batteries still serve cost-sensitive aftermarket channels and heavy-duty haul trucks where buyers prize deep-cycle robustness and lower list prices. Incremental innovation is emerging through lead-carbon hybrids that embed carbon in negative plates to boost partial-state-of-charge performance; pilot projects in Canadian Arctic micro-grids illustrate the chemistry’s tolerance of -40 °C ambient temperatures without external heaters. Regulatory codes also tilt subtly toward VRLA UL 1989 certification, which is simpler for sealed units, and VRLA’s spill-proof shell satisfies increasingly stringent local fire marshals overseeing data-center retrofit work. These factors collectively sustain VRLA’s expanding role inside the North America Lead-Acid Battery Market size even as flooded sales taper.

By Application: Stationary Outpaces a Steady SLI Core

Starting-lighting-ignition batteries still delivered 55.9% of the North America Lead-Acid Battery Market revenue in 2025, owing to an aging fleet and a 37% replacement rate on older vehicles. However, the stationary category, bolstered by data-center UPS and 5G base-station rollouts, is tracking a 6.4% CAGR, the fastest among use cases. Within the stationary, North America Lead-Acid Battery Market size gains stem from retrofit projects where existing racks favor VRLA form factors, and from edge-computing nodes that choose sealed batteries to minimize truck rolls.

Motive-power applications forklifts, golf carts, and airport ground-support equipment face the sharpest lithium-ion substitution. Yet infrastructure costs delay U.S. crossover until roughly 2032, so single-shift warehouses still view lead acid as the economic baseline. Portable and other segments, such as emergency lighting, security, and medical systems, remain VRLA strongholds; the compact PS-1250 and like models stay price-competitive at small amp-hour ratings where lithium-ion’s cost per kWh loses advantage. Thus, diversification within applications allows the North America Lead-Acid Battery Market to hold volume even while high-utilization niches convert to new chemistries.

Geography Analysis

The United States accounted for 73.6% of North America Lead-Acid Battery Market revenue in 2025, thanks to its 280 million-unit vehicle parc, the world’s largest data-center cluster, and a vast network of distribution centers that rely on motive batteries. Growth is slower than the regional average because lithium-ion is already well-penetrated in Class I forklift fleets and hyperscale UPS rooms. Still, Clarios’ pledge to invest USD 6 billion by 2035, including USD 1.9 billion in critical minerals recycling, signals confidence that legacy automotive and auxiliary-battery demand will remain sticky.

Canada is bolstered by rugged mining and remote micro-grid installations where lead acid’s thermal stability trumps lithium-ion’s heater-dependent designs. The Raglan Mine wind-diesel-storage project in Quebec uses multi-chemistry stacking, and similar Arctic plans are considering lead-carbon variants for renewable-firming because they sustain >4,000 cycles at 70% depth of discharge in cold laboratories. Provincial clean-technology incentives also nudge investment toward domestically sourced batteries, helping local assemblers capture public procurement contracts.

Mexico supplies the balance of regional value, riding its role as an automotive export hub under USMCA rules mandating 75% regional content. ICE vehicle production feeds steady aftermarket pull-through for SLI replacements, and domestic forklift demand is rising in new industrial parks near the U.S. border. Yet OEM retooling budgets of USD 2.5 billion announced for hybrid and EV lines imply a gradual pivot away from traditional 12 V demand. Mexican assemblers thus face a dual strategy: defend the current SLI pipeline while courting auxiliary-battery contracts for forthcoming hybrid platforms.

Competitive Landscape

The North America Lead-Acid Battery Market is consolidated. Clarios maintains the broadest footprint, blending secondary smelters, grid-casting operations, and 30+ assembly plants to secure margin across the chain. Its USD 6 billion investment map covers advanced battery lines, critical minerals recycling, and R&D into next-generation chemistries through 2035. East Penn is doubling down on higher-value AGM by requesting USD 110 million in tax abatements for a Temple, Texas, plant that adds 175,000 square feet of finishing space.

EnerSys is pruning overseas sites and re-shoring capacity to Kentucky and Missouri to qualify for Internal Revenue Code §45X advanced-manufacturing credits, unveiling USD 6.7 million in new TPPL lines in Sumter, South Carolina, in 2025. Stryten Energy, the fourth-largest participant, leverages 11 U.S. factories to supply automotive and reserve-power batteries while piloting vanadium-redox flow systems as a strategic hedge. Complementary technology sprouts from NorthStar’s IoT-enabled ACE platform that delivers predictive maintenance to telecom carriers, and from Aqua Metals, which agreed in February 2026 to buy Lion Energy for USD 25.8 million plus USD 65 million in earn-outs, targeting an integrated lithium-ion recycling and storage portfolio.

White-space opportunities focus on cost-sensitive, harsh-environment niches, off-grid labs, Arctic villages, and marine propulsion, where lead acid’s low-temperature tolerance and closed-loop recycling remain unchallenged. Meanwhile, incumbents are quietly adding lithium-ion SKUs to retain enterprise accounts pushing toward fleet electrification, acknowledging that the North America lead acid battery industry must coexist with, rather than outright resist, the chemistry transition.

North America Lead-Acid Battery Industry Leaders

Clarios (a subsidiary of Brookfield Business Partners)

EnerSys

C&D Technologies Inc

Leoch International Technology Limited

GS Yuasa Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: East Penn Manufacturing sought USD 110 million in Temple, Texas, abatements for a 175,000 sq ft AGM expansion, promising 48 new jobs.

- February 2026: Aqua Metals signed a term sheet to acquire Lion Energy for USD 25.8 million plus up to USD 65 million in earn-outs, integrating lithium-ion recycling with storage solutions.

- February 2026: Trojan Battery enlarged its U.S. distribution agreement with Battery Outfitters in Missouri to widen its reach for deep-cycle and lithium lines.

- February 2026: NextStar Energy, the LG-Stellantis venture, opened a 4.23 million-sq ft lithium-ion plant in Windsor, Ontario, producing 1 million cells by Feb 2026.

North America Lead-Acid Battery Market Report Scope

A lead-acid battery is a rechargeable (secondary) electrochemical cell that stores and releases electrical energy through reversible chemical reactions involving lead plates and a sulfuric acid electrolyte. Invented in 1859 by Gaston Planté, it was the first rechargeable battery developed and continues to be widely used due to its low cost and capability to deliver high surge currents.

The North America Lead-Acid Battery Market is segmented into construction method, application, and geography. By construction method, the market is segmented into flooded and VRLA batteries. By application, the market is segmented into starting-lighting-ignition (SLI), stationary, motive/traction (forklifts, golf carts), portable, and other applications. The report also covers the market size and forecasts for the lead acid battery market across key countries in North America, including the United States, Canada, and Mexico. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Construction Method

| Flooded |

| VRLA |

By Application

| Starting-Lighting-Ignition (SLI) |

| Stationary |

| Motive/Traction (Forklifts, Golf-carts) |

| Portable and Others |

By Geography

| United States |

| Canada |

| Mexico |

| By Construction Method | Flooded |

| VRLA | |

| By Application | Starting-Lighting-Ignition (SLI) |

| Stationary | |

| Motive/Traction (Forklifts, Golf-carts) | |

| Portable and Others | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the current value of the North America Lead-Acid Battery Market?

The market stands at USD 11.53 billion in 2026 and is set to reach USD 14.29 billion by 2031.

How fast is the market expected to grow?

It is forecast to record a 4.39% CAGR from 2026 to 2031.

Which construction method leads regional sales?

Valve-regulated lead acid (VRLA) batteries held 64.3% share in 2025 and will continue to dominate.

Where is the strongest application growth?

Stationary power uses principally data-center and telecom UPS are advancing at a 6.4% CAGR through 2031.

Who are the major market players?

Clarios, East Penn Manufacturing, EnerSys, and Stryten Energy collectively control about two-thirds of capacity.

What major factor threatens lead acid demand?

Rapid lithium-ion price declines and longer service life are eroding lead acid's cost advantage in high-utilization segments.

Page last updated on: