Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.64 Billion |

| Market Size (2031) | USD 10.56 Billion |

| Growth Rate (2026 - 2031) | 6.68% CAGR |

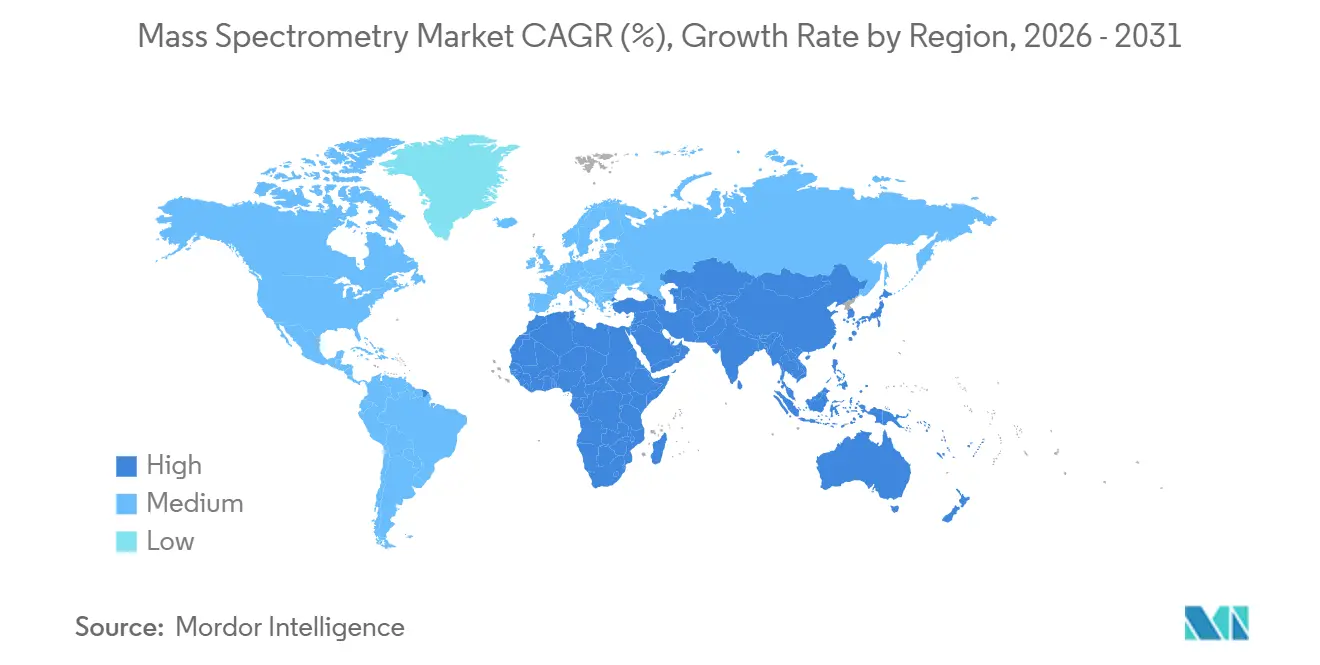

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mass Spectrometry Market Analysis by Mordor Intelligence

The Mass Spectrometry Market size is projected to expand from USD 7.16 billion in 2025 and USD 7.64 billion in 2026 to USD 10.56 billion by 2031, registering a CAGR of 6.68% between 2026 to 2031.

Escalating molecular complexity in biopharmaceutical pipelines, tighter food-safety limits, and the spread of AI-enabled, real-time analytics are compressing analytical cycles from hours to minutes, lifting instrument utilization rates across pharmaceutical, environmental, and clinical-diagnostics settings. High-resolution hybrid systems underpin most upgrade decisions as laboratories chase lower detection limits for PFAS, mycotoxins, and trace-element impurities. Vendors are simultaneously layering cloud software onto aging hardware, allowing laboratories to automate peak annotation and ensure 21 CFR Part 11 compliance without major capital outlays. This confluence of drivers is tilting revenue toward informatics even as hardware retains the lion’s share of spending.

Key Report Takeaways

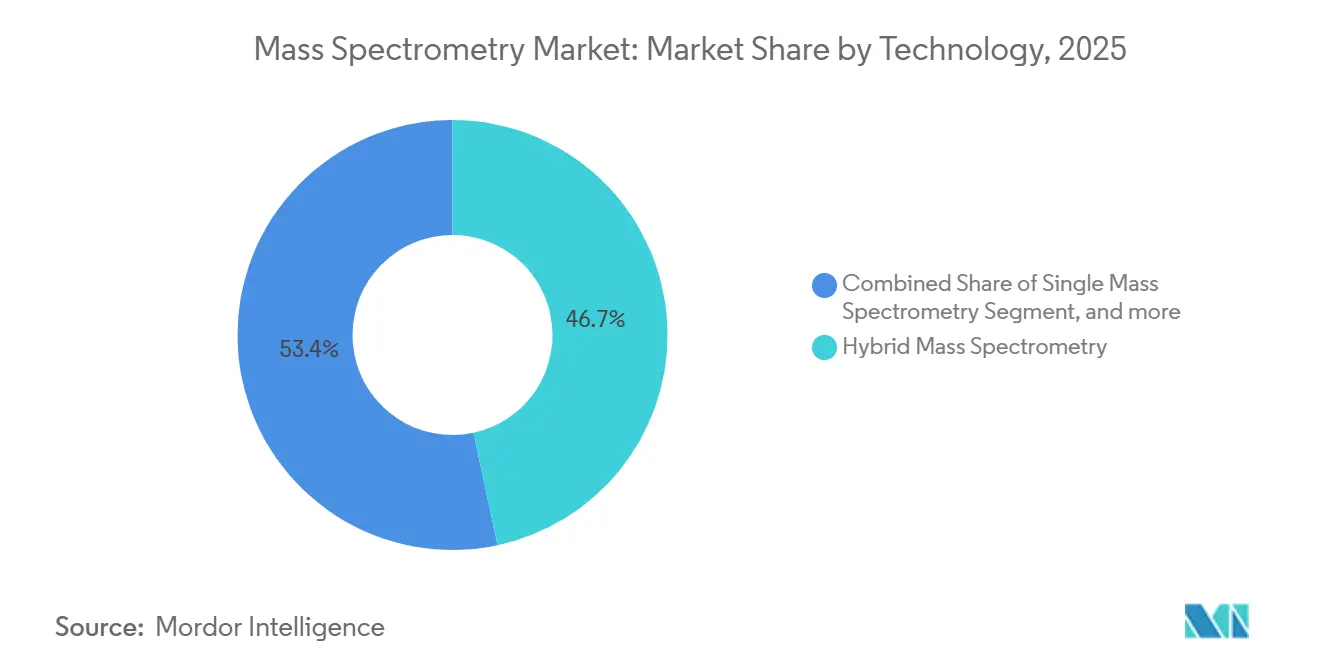

- By technology, hybrid platforms led with 46.65% revenue share in 2025, while MALDI-TOF is forecast to expand at an 8.54% CAGR through 2031, driven by time-critical pathogen identification in clinical microbiology.

- By component, instruments accounted for 70.43% of 2025 revenue; software platforms are advancing at 8.76% CAGR on the back of machine-learning-enabled data interpretation.

- By application, pharmaceutical and biotechnology held 34.56% of 2025 revenue; clinical diagnostics and proteomics are the fastest-growing segments at 9.54% CAGR, powered by precision-medicine rollouts.

- By geography, North America captured 42.65% of 2025 revenue, while Asia-Pacific is expanding at 7.54% as China and India scale biologics manufacturing and environmental surveillance.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mass Spectrometry Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Biopharmaceutical Pipeline Complexity | +1.2% | North America and the European Union dominate; APAC catching up | Medium term (2-4 years) |

| Stringent Global Food Safety Regulations | +1.0% | European Union leads; North America and APAC follow | Short term (≤ 2 years) |

| Rising Multi-Omics Research Funding | +0.9% | North America, European Union, China | Long term (≥ 4 years) |

| Increasing Environmental Monitoring Mandates | +0.8% | North America, European Union core; spill-over to APAC | Medium term (2-4 years) |

| AI-Driven Real-Time Data Interpretation | +0.7% | Early adoption in North America, spreading globally | Short term (≤ 2 years) |

| Proliferation of Portable Systems for Security | +0.5% | Airports and border posts in North America, European Union, Middle-East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Expanding Biopharmaceutical Pipeline Complexity

Antibody-drug conjugates, bispecifics, and cell therapies exceed 40% of the FDA’s active IND docket, and each class demands orthogonal mass spectrometry for intact-mass verification, linker stability, and glycoform mapping[1]Food and Drug Administration, “Investigational New Drug Submissions,” fda.gov. NIH raised its structural-biology and proteomics budget to USD 2.1 billion in fiscal 2025, earmarking funds for Orbitrap and Q-TOF systems to resolve post-translational modifications at single-amino-acid resolution. Contract manufacturers in India and China are installing hybrid quadrupole-time-of-flight platforms to meet Western filing requirements that prioritize mass-based identity testing over legacy chromatographic retention-time checks. Thermo Fisher recorded a 22% rise in Orbitrap shipments to Asia-Pacific biopharma clients during 2025, underscoring the regional pivot toward high-resolution analysis. The shift boosts service revenue as users lock into multi-year maintenance contracts to guarantee 95% uptime.

Stringent Global Food Safety Regulations

The European Union expanded its Maximum Residue Level database to 1,100 pesticide-crop pairs in 2025, obliging food-testing labs to validate each pairing with accredited reference materials. Triple-quadrupole LC-MS/MS dominates because it discerns isobaric pesticides such as chlorpyrifos and chlorpyrifos-methyl in fatty matrices. Japan adopted parallel multi-residue rules in 2024, triggering a 30% jump in LC-MS/MS tenders within 12 months. Brazil followed with mandatory isotope-dilution testing for aflatoxins on all corn exports to the EU starting September 2025. These mandates create a replacement cycle that overrides remaining instrument life, forcing upgrades even for systems purchased after 2020.

Rising Multi-Omics Research Funding

The NIH Molecular Transducers of Physical Activity Consortium committed USD 170 million in 2025 to map exercise-induced metabolomic and proteomic shifts, requiring synchronized LC-MS and GC-MS workflows across 11 clinical sites[2]National Institutes of Health, “FY 2025 Budget in Brief,” nih.gov. China’s science foundation pledged CNY 1.8 billion (USD 250 million) for proteogenomics hardware in 2024, specifying top-down mass spectrometry for variant-to-protein translation. Waters reported that 35% of 2025 order intake from academia bundled software modules that fuse genomics, metabolomics, and proteomics data sets, up from 18% in 2023. Precision-oncology programs now integrate peptide quantitation with next-generation sequencing, demanding instruments offering femtomole sensitivity and 5-log dynamic range.

Increasing Environmental Monitoring Mandates

The EPA’s PFAS rule, effective January 2027, requires quarterly testing for six perfluoroalkyl acids at detection limits below 4 ppt, achievable only with Orbitrap or Q-TOF high-resolution systems. U.S. state labs in Michigan, New Jersey, and California began ordering these platforms in late 2024 as triple-quadrupole units proved susceptible to dissolved-organic-carbon interferences. Europe added 24 emerging contaminants to its Water Framework Directive in March 2025, compelling the use of suspect-screening workflows built on accurate-mass libraries. India’s pollution-control board issued tenders for 50 ICP-MS instruments in 2025 to trace heavy-metal deposition in cities aligning with WHO PM 2.5 targets. Recurrent reagent and software spending equal to 25%–30% of the original purchase price secures long-term vendor revenue.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital and Operating Costs | −0.6% | Global, with pronounced impact in emerging markets | Short term (≤ 2 years) |

| Shortage of Skilled Mass Spectrometry Personnel | −0.5% | North America and the European Union most affected; pressure rising in APAC | Medium term (2 – 4 years) |

| Data Management and Cybersecurity Concerns | −0.4% | Global, highest awareness in regulated pharmaceutical and clinical labs | Medium term (2 – 4 years) |

| Supply Chain Disruptions for Critical Components | −0.3% | North America and APAC fabs reliant on semiconductor parts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Operating Costs

A fully configured LC-MS/MS platform with autosampler and compliance software costs nearly USD 400,000, and users budget another USD 60,000 per year for service and consumables. Leasing programs introduced in 2024 trim upfront cash by 40% yet still leave lessees covering maintenance, which represents 70% of total cost of ownership over five years. Fourier-transform instruments draw 15 kW continuously, costing USD 18,000 per year in electricity at industrial rates, an issue for labs facing unstable grids or high tariffs. EU and Japanese regulators mandate full revalidation when ownership changes, eroding the appeal of refurbished instruments.

Shortage of Skilled Mass Spectrometry Personnel

ASMS reported that 43% of U.S. labs had unfilled mass spectrometry posts for more than 6 months in 2025, with median salaries for experienced staff rising to USD 95,000—up 28% from 2022[3]American Society for Mass Spectrometry, “2025 Workforce Survey,” asms.org. Only 22% of U.S. chemistry PhD programs offer dedicated coursework, and fewer than 10 universities give hands-on access to hybrid or high-resolution systems. Vendor training fills some gaps—Thermo Fisher ran 340 courses in 2025, up from 210 in 2023—but it focuses on routine operations rather than advanced troubleshooting. APAC labs increasingly hire retired North American and European specialists on 12-month contracts costing up to USD 200,000 each, pushing up operating budgets.

Segment Analysis

By Technology: MALDI-TOF Gains Clinical Traction

MALDI-TOF platforms are projected to grow 8.54% annually through 2031, outstripping the broader 6.68% rate as hospital microbiology labs adopt the technology for same-day bacterial and fungal ID. The Bruker MALDI Biotyper, FDA-cleared in 2024 for direct-from-blood-cultur workflows, cuts time-to-result from 48 hours to under 30 minutes, saving USD 3,500 per sepsis case. Hybrid triple-quadrupole LC-MS/MS systems, anchoring 46.65% of 2025 revenue, dominate pharmaceutical QC and multi-residue pesticide testing thanks to unrivaled targeted quantitation. Quadrupole-time-of-flight analyzers are carving space in proteomics for data-independent acquisition, while Orbitrap and FT-ICR remain gold standards for resolving power-intensive tasks despite a modest 12% revenue share. Single-analyzer instruments, once mainstays of teaching labs, are losing ground as hybrid price points fall. ICP-MS demand is accelerating in semiconductor fabs that need to detect metal contaminants at levels below 1 ppb.

Broader technology adoption trends are reshaping the mass spectrometry market. Vendors now market firmware-upgradable platforms that add acquisition modes without hardware swaps, prolonging instrument life and reducing electronic waste. The mass spectrometry market for technology segments is tilting toward systems with embedded ion mobility to decouple isobaric species in complex matrices. Hybrid platforms captured 46.65% of the 2025 mass spectrometry market share, reflecting buyers’ preference for flexibility over single-purpose designs. As regulatory limits tighten, sales of high-resolution, accurate-mass platforms are forecast to reach USD 4.9 billion by 2031, with an 8.1% CAGR led by Orbitrap and Q-TOF. Meanwhile, portable systems priced under USD 100,000 are finding traction in security screening and field environmental testing, opening a secondary upgrade path for legacy benchtops.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Component: Software Outpaces Hardware Growth

Instruments commanded 70.43% of 2025 revenue, but software and informatics are set to climb 8.76% per year as laboratories shift budgets toward automated data processing and regulatory documentation. Thermo Fisher’s Compound Discoverer 3.4 embeds machine learning that cuts false positives by 35% in non-targeted screening. Agilent’s MassHunter Cloud centralizes method libraries across multi-site networks, easing FDA audit trails and driving subscription revenue. The mass spectrometry software market is projected to surpass USD 2.1 billion by 2031, driven by steady annual license renewals.

Detector and ion-source replacements generate predictable aftermarket income, with electron multiplier tubes and microchannel plates swapped every 5 years on average. Service revenue—installation, calibration, preventive maintenance—represents a durable 12% of component turnover and is growing faster than hardware. Waters grew its service line 9% year over year in 2025 as users sought guaranteed uptime amid hiring shortages. SCIEX’s firmware-centric ZenoTOF 7600+ illustrates the pivot toward software-defined instruments: new acquisition modes are downloaded remotely, extending usable life and reducing e-waste. As this shift deepens, participants in the mass spectrometry industry are reevaluating their intellectual property portfolios to emphasize algorithms rather than hardware patents.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Clinical Diagnostics Accelerates

Clinical diagnostics and proteomics are progressing at a 9.54% CAGR through 2031, the steepest among applications. The FDA cleared 14 MS-based laboratory-developed tests in 2025, covering immunosuppressants, vitamin-D metabolites, and expanded newborn panels, validating mass spectrometry in routine pathology. Pharmaceutical and biotechnology work, the largest slice at 34.56% in 2025, is maturing as regulatory techniques stabilize. Food and beverage testing is next, with a 7.1% CAGR, buoyed by expanding pesticide and mycotoxin panels, while environmental analysis grows 7.8% on PFAS and microplastic mandates.

Forensic toxicology labs scaled up purchases to cover 200+ fentanyl analogs that evade immunoassays. Petrochemical operations adopted GC-MS/MS for inline process-stream surveillance, displacing flame-ionization detectors. Academic research, 11% of revenue, mirrors government funding: Horizon Europe allocated EUR 95 billion for 2024-2027, with 18% routed to life-science grants, heavy on MS workflows. Mass spectrometry market share is fragmenting as vendors introduce turnkey kits—lipidomics, glycomics, PFAS—that lower the entry barrier for non-specialists and seed follow-on consumables revenue.

Geography Analysis

North America accounts for 42.65% of 2025 revenue, driven by concentrated pharmaceutical R&D, stringent FDA guidance on MS method validation, and early adoption of environmental testing. The EPA’s PFAS rule alone is expected to drive USD 400 million in instrument sales to state and municipal labs between 2025 and 2027. Canada invested CAD 90 million (USD 66 million) in high-throughput proteomics at UBC, positioning it as a multi-omics hub. Mexico’s expansion in biologics contract manufacturing added 12 facilities in 2024-2025, each ordering multiple LC-MS/MS systems.

Asia-Pacific is the fastest-growing region at 7.54% CAGR through 2031. China’s regulator approved 22 biosimilars in 2025, each requiring mass-spectrometry comparability dossiers, fuelling platform demand. India’s API exports hit USD 28 billion in fiscal 2025, up 19% year on year, with ICP-MS and LC-MS/MS central to impurity profiling. Japan expanded reimbursement for MS-based vitamin-D testing in April 2025, adding 2 million annual assays, while South Korea’s chip fabs deployed ICP-MS for ultrapure-water control at sub-3 nm nodes.

Europe accounted for 28% of 2025 revenue. The Green Deal’s 55% emissions-cut goal is catalyzing VOC and PM composition monitoring using high-resolution MS. The UK expanded its newborn screening panel to 35 disorders in 2024, prompting 14 regional labs to upgrade to tandem-MS platforms. Middle East & Africa, with 6% share, grows 6.9% as GCC states expand food-safety labs, while South America’s 6.2% growth rests on Brazil’s environmental mandates and Argentina’s pharma exports, although currency swings limit capex.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The top five vendors—Thermo Fisher, Agilent, Waters, SCIEX, Shimadzu—command roughly 60% of the global revenue base, giving the mass spectrometry market a moderate concentration. Industry incumbents leverage installed bases and bundled workflows spanning sample prep to cloud analytics. Thermo Fisher’s 2025 takeover of a German AI-software specialist underscores the pivot toward data science as a differentiator. Bruker filed 14 patents in 2024-2025 anchored on trapped-ion-mobility spectrometry, chasing incremental separation in complex proteomes.

Niche challengers are exploiting gaps in portability and cost. Handheld systems under 15 kg priced below USD 100,000 logged 22% sales growth in 2025 as airports and border agencies adopted on-site narcotic and explosive screening. California’s 2025 pilot of handheld pesticide screening at farmers’ markets delivered on-site 10-minute results, foreshadowing decentralized testing models. Vendors now court recurring revenue: Waters’ 2024 consumables subscription guarantees next-day delivery, locking clients into proprietary columns and vials that account for 18% of instrument sales.

Regulatory compliance remains a gatekeeper. New entrants must invest heavily in ISO 17025 quality systems and 21 CFR Part 11 validation to penetrate pharmaceutical and clinical segments. The mass spectrometry industry is therefore witnessing alliances that meld hardware startups with software or reagent specialists, shortening time-to-compliance.

Mass Spectrometry Industry Leaders

Thermo Fisher Scientific Inc.

Agilent Technologies Inc.

Danaher Corporation (SCIEX)

Waters Corporation

Bruker Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: Waters Corporation unveiled the Waters Xevo Charge Detection Mass Spectrometer (CDMS), delivering unmatched measurement and characterization for the broadest range of mega-mass biomolecules central to next-generation therapeutics and structural biology.

- May 2025: Bruker Corporation launched timsMetabo, a peak-performance 4D-Metabolomics mass spectrometer delivering unprecedented sensitivity, separation power, and annotation confidence for small molecules, further enhanced by the novel TIMS 'MoRE' scan-mode.

- December 2024: F. Hoffmann-La Roche Ltd. received CE mark approval for its cobas Mass Spec solution, including the cobas i 601 analyser and the first Ionify reagent pack of four assays for steroid hormones.

Global Mass Spectrometry Market Report Scope

As per the scope of this report, mass spectrometry (MS) is an analytical chemistry technique used to identify the amount and type of chemical species present in a sample, by measuring the mass-to-charge ratio and abundance of gas-phase ions.

The Mass Spectrometry Market is Segmented by Technology (Hybrid Mass Spectrometry (Triple Quadrupole (Tandem), Quadrupole TOF (Q-TOF), and FTMS (Fourier Transform Mass Spectrometry), Single Mass Spectrometry (ION Trap, Quadrupole, and Time-of-Flight (TOF)), and Inductively Coupled Plasma Mass Spectrometry), Application (Chemical Industry, Academic Research, Pharmaceutical and Biotechnology Companies, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

By Technology

| Hybrid Mass Spectrometry | Triple Quadrupole (LC-MS/MS) |

| Quadrupole Time-of-Flight (Q-TOF) | |

| Fourier-Transform (FT-MS) | |

| Single Mass Spectrometry | Quadrupole |

| Time-of-Flight (TOF) | |

| Ion Trap | |

| MALDI-TOF Mass Spectrometry | |

| Inductively Coupled Plasma Mass Spectrometry (ICP-MS) | |

| Other Technologies |

By Component

| Instruments |

| Ionisation Sources |

| Detectors & Analysers |

| Software & Informatics |

| Services |

By Application

| Pharmaceutical & Biotechnology |

| Clinical Diagnostics & Proteomics |

| Food & Beverage Testing |

| Environmental Testing |

| Chemical & Petrochemical |

| Forensic & Toxicology |

| Academia & Research Institutes |

| Other Applications |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Hybrid Mass Spectrometry | Triple Quadrupole (LC-MS/MS) |

| Quadrupole Time-of-Flight (Q-TOF) | ||

| Fourier-Transform (FT-MS) | ||

| Single Mass Spectrometry | Quadrupole | |

| Time-of-Flight (TOF) | ||

| Ion Trap | ||

| MALDI-TOF Mass Spectrometry | ||

| Inductively Coupled Plasma Mass Spectrometry (ICP-MS) | ||

| Other Technologies | ||

| By Component | Instruments | |

| Ionisation Sources | ||

| Detectors & Analysers | ||

| Software & Informatics | ||

| Services | ||

| By Application | Pharmaceutical & Biotechnology | |

| Clinical Diagnostics & Proteomics | ||

| Food & Beverage Testing | ||

| Environmental Testing | ||

| Chemical & Petrochemical | ||

| Forensic & Toxicology | ||

| Academia & Research Institutes | ||

| Other Applications | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What CAGR is forecast for the mass spectrometry market between 2026 and 2031?

A CAGR of 6.68% is projected for the period.

Which technology segment is forecast to grow the fastest?

MALDI-TOF platforms are expected to rise at 8.54% per year through 2031 due to rapid pathogen identification demands.

Why is Asia-Pacific growing faster than other regions?

China and India are scaling biologics manufacturing and tightening environmental monitoring, pushing regional demand up 7.54% annually.

How are software investments changing spending patterns?

Cloud-based analytics and AI-driven interpretation tools are expanding at 8.76% CAGR, outpacing hardware upgrades as labs seek automation.

What is the primary restraint on wider adoption?

High capital and operating costs remain the top barrier, with a fully configured LC-MS/MS system exceeding USD 400,000 plus sizeable annual maintenance.

Which application area is advancing the quickest?

Clinical diagnostics and proteomics leads with a 9.54% CAGR as precision-medicine programs expand mass-spectrometry-based biomarker panels.