Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.88 Billion |

| Market Size (2031) | USD 3.82 Billion |

| Growth Rate (2026 - 2031) | 5.82% CAGR |

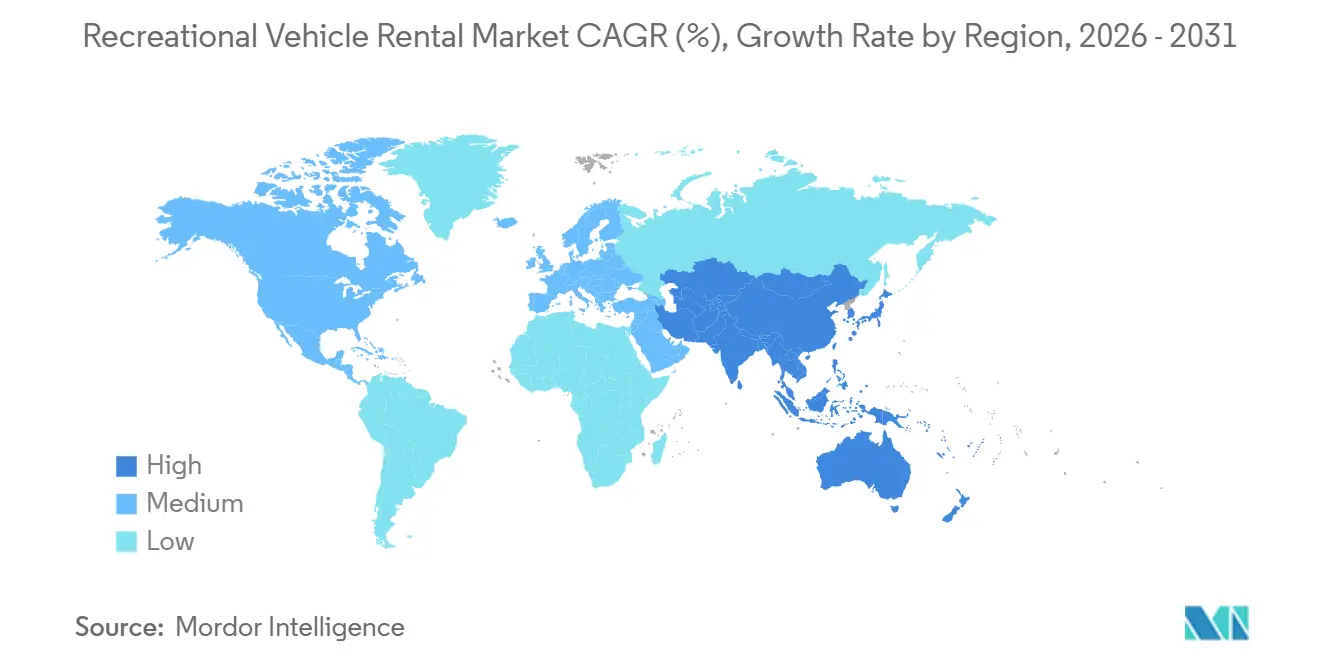

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Recreational Vehicle Rental Market Analysis by Mordor Intelligence

The Recreational vehicle Rental market size is projected to expand from USD 2.72 billion in 2025 and USD 2.88 billion in 2026 to USD 3.82 billion by 2031, registering a 5.82% CAGR between 2026 to 2031. The growing preference for experiential travel among younger cohorts, the rapid adoption of peer-to-peer platforms, and the initial electrification of rental fleets are reshaping supplier economics and traveler expectations. Experience-oriented consumers favor road trips that combine flexible itineraries with access to remote natural sites, a shift that boosts vehicle days and reduces ownership barriers. Digitally native renters demand instant booking and transparent pricing, pushing operators toward dynamic pricing models that raise average transaction value. Early fleet electrification signals a premium-segment opportunity, even as charging infrastructure remains sparse.

Key Report Takeaways

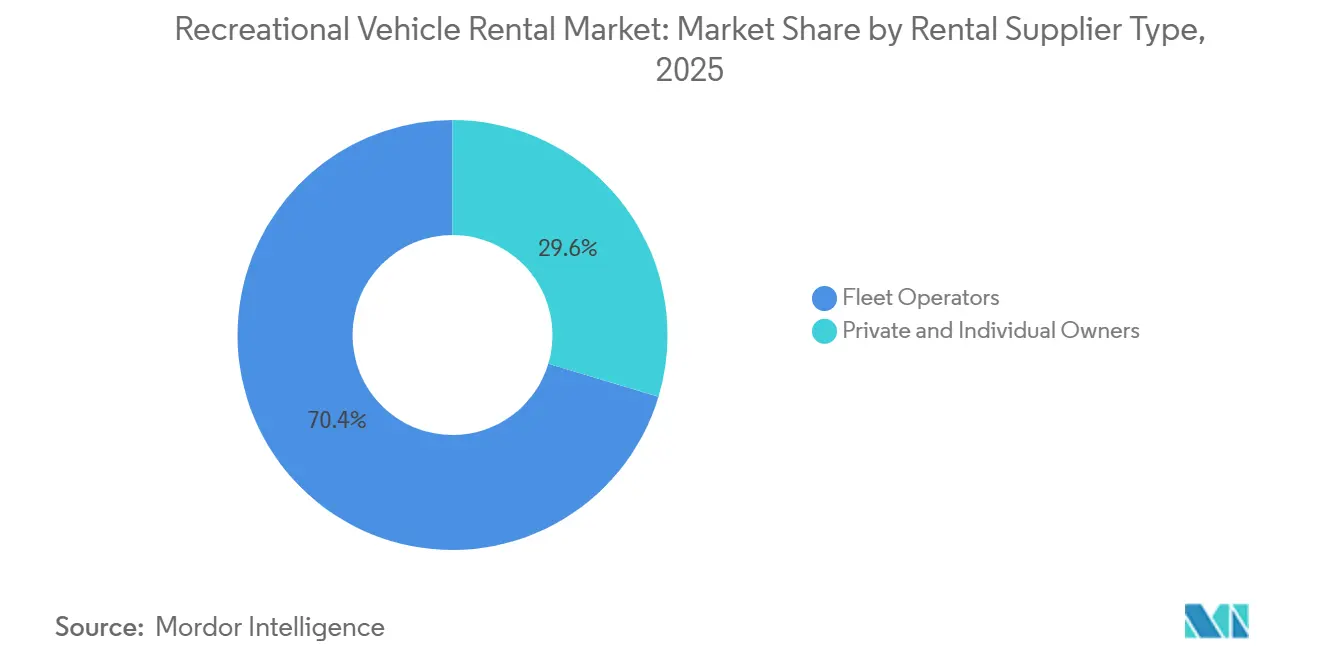

- By rental supplier type, fleet operators held 70.37% of the Recreational Vehicle Rental Market share in 2025, while individual owners recorded the fastest projected CAGR at 6.95% to 2031.

- By booking type, the online segment accounted for 61.55% of 2025 revenue, growing at an 8.01% CAGR through 2031.

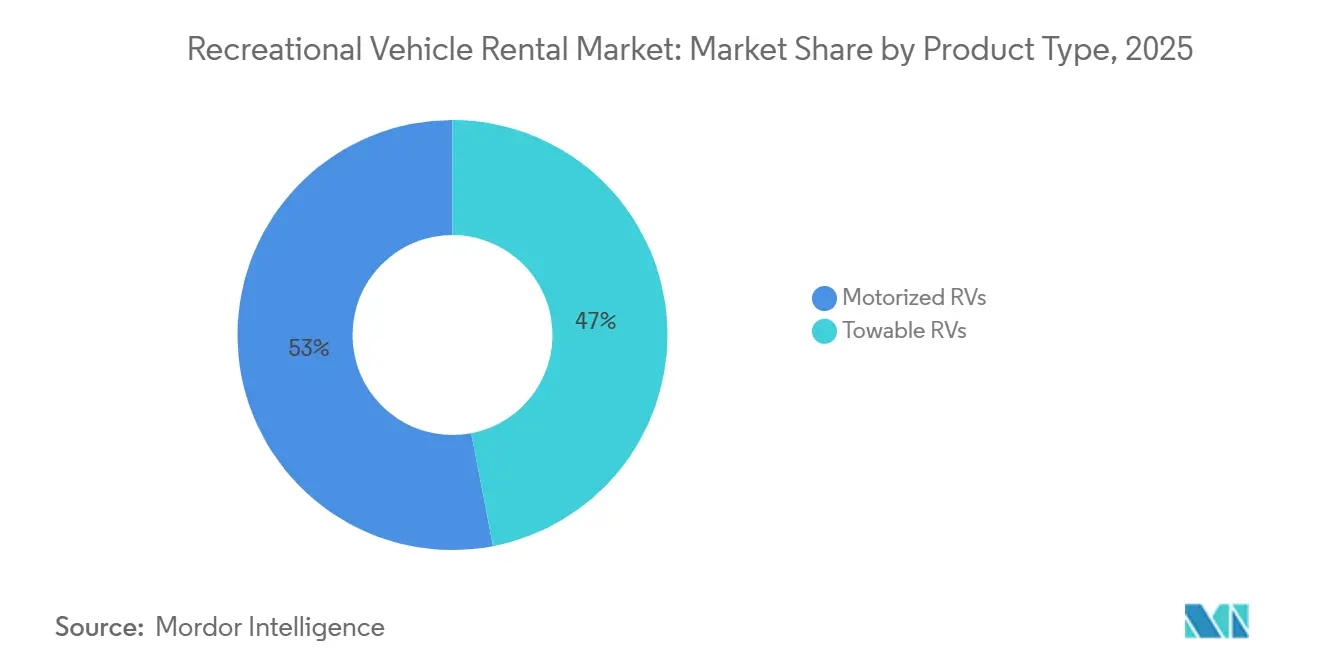

- By product type, motorized RVs led with 53.01% revenue share in 2025; towables are projected to expand at an 8.66% CAGR through 2031.

- By rental duration, short-term rentals accounted for 52.82% of the total market in 2025, yet mid-term rentals are projected to grow at 8.94% through 2031.

- By geography, North America accounted for 46.78% of 2025 revenue; Asia-Pacific is slated to post the highest regional CAGR of 11.35% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Recreational Vehicle Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Domestic Tourism | +1.2% | Global, with highest impact in North America & Europe | Short term (≤ 2 years) |

| Expansion of Peer-to-Peer Rentals | +1.0% | Global, led by North America, expanding to APAC & Europe | Medium term (2-4 years) |

| Rising Disposable Income | +0.9% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Zero-Emission RV Incentives | +0.6% | North America (California + 9 states), EU | Long term (≥ 4 years) |

| Fleet Uptime Optimization | +0.5% | North America & Europe, spreading to APAC | Medium term (2-4 years) |

| Corporate Use | +0.2% | North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Domestic Road-Trip Tourism

Leisure travelers are redirecting budgets from overseas flights to drivable vacations, reinforcing the appeal of open-road itineraries. In 2024-25, Australia witnessed 8.40 million international visitor arrivals, up from 7.97 million in 2023-24[1] "Overseas arrivals and departures, Australia - 2024-25 financial year" Australian Bureau of Statistics, abs.gov.au. Heavier visitation at national parks tightens campground capacity and nudges renters toward dispersed public-land sites. Industry surveys show that millions of households now plan at least one RV trip each year, confirming a lasting behavioral shift from air to road travel. Operators that package vehicles with campsite reservations and pre-planned routes capture first-time renters who value convenience. Flexibility, avoidance of crowded airports, and access to remote scenery remain the primary pull factors for this driver segment.

Expansion of Peer-to-Peer (P2P) Rental Platforms

Digital marketplaces unlock income for idle privately owned RVs while giving renters a wider selection of vehicle styles. The model shifts maintenance and depreciation risk to owners, allowing platforms to scale without heavy capital outlay. Trust hinges on effective verification procedures and purpose-built insurance that protects both parties during each booking. Dynamic pricing engines help owners reach occupancy targets while keeping rates attractive for budget-sensitive travelers. As transactions grow, platform loyalty rises due to ease of booking, transparent reviews, and responsive customer support.

Rising Disposable Income Among Millennials and Gen-Z

A younger demographic is entering the peak earning years and channeling discretionary spending toward experiences rather than possessions. Social-media influence and remote-work policies encourage longer, more immersive RV adventures that blur the lines between vacation and daily life. These travelers gravitate to Wi-Fi-enabled motorized units and often comparison-shop across multiple apps before committing. Visual storytelling drives demand for units with stylish interiors and photogenic exteriors. Brands that partner with influencers and emphasize sustainability cues resonate strongly with this audience.

Zero-Emission RV Incentives Accelerating Electrified Fleets

Government incentives lower the upfront cost of adopting electric powertrains and charging infrastructure for rental fleets. Early prototypes of battery-assisted motorhomes show that premium renters will pay more for silent operation and lower emissions. Operators promoting green credentials differentiate themselves in urban and corporate segments where sustainability policies guide purchasing decisions. Limited rural charging networks remain a constraint, but also create opportunities for businesses that install fast chargers at depots and destination campgrounds. Early adopters enjoy marketing advantages and favorable press coverage that reinforce brand equity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Maintenance and Insurance Costs | -1.1% | Global, most acute in North America & Europe | Short term (≤ 2 years) |

| Seasonality-Driven Low Asset Utilization | -0.8% | Northern hemisphere markets, moderate in APAC | Medium term (2-4 years) |

| Overnight Parking Restrictions | -0.6% | Urban centers in North America & Europe | Short term (≤ 2 years) |

| Supply Bottlenecks | -0.4% | Global, concentrated in complex motorized units | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Maintenance and Insurance Costs

Routine service on engines, tires, and onboard appliances, coupled with comprehensive insurance, compresses margins for small operators. Platforms mitigate some expenses through telematics that flag issues before breakdowns and through pooled purchasing of parts. Skilled labor for RV repair remains scarce, keeping hourly shop rates high and turnaround times unpredictable. Owners sometimes pass rising costs to renters, though price sensitivity places an upper limit on surcharges. Cost containment, therefore, relies on predictive maintenance, in-house service teams, and negotiated insurance coverage.

Seasonality-Driven Low Asset Utilization

Demand soars in warm months and falls sharply during colder seasons, leaving significant idle inventory at depots. Operators experiment with repositioning vehicles to year-round climates, but transport logistics and regulatory hurdles limit scale. Off-peak discounts attract retirees and digital nomads, yet narrow profit margins. Diversifying into corporate mobile offices or film-production support helps fill winter gaps but requires specialized vehicle layouts. Balancing fleet mix and exploring counter-cyclical use cases remain essential to smoothing utilization curves.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rental Supplier Type: Fleet Consolidation Drives Scale Advantages

Fleet operators accounted for 70.37% of the recreational vehicle rental market in 2025, reflecting well-organized networks that offer standardized fleets, reliable service, and comprehensive maintenance. Their scale ensures steady availability of Class A, B, and C motorhomes, attracting renters who value convenience and consistent quality. Strong brand recognition and established customer support also make trip planning easier for long-distance travelers. As RV vacations grow among families, retirees, and overseas visitors, large operators maintain their lead by modernizing their fleets and expanding coverage along major tourist routes, reinforcing their dominance in the overall market.

Private and individual owners form the fastest-expanding category, growing at a 6.95% CAGR through 2031 as peer-to-peer platforms gain momentum. Easy-to-use apps let owners earn income from underused vehicles, expanding supply in suburban and rural areas. Renters appreciate the unique models and budget-friendly prices often found outside corporate fleets. Trust in digital verification, bundled insurance, and driveway delivery services is rising among younger travelers, accelerating adoption and diversifying market demand.

By Booking Type: Digital Transformation Accelerates Online Adoption

Online booking accounted for 61.55% of the 2025 market size and is the fastest-growing channel, growing at an 8.01% CAGR as travelers increasingly expect digital convenience. Mobile platforms let users compare prices, view layouts, and secure a vehicle in minutes. Built-in GPS planners, digital check-ins, and instructional videos streamline the process, while last-minute weekend trips have become easier to arrange online. User reviews, seamless payments, and personalized recommendations are cementing the internet as the preferred route for reservations.

Offline reservations accounted for 38.45% of rentals in 2025. Many first-time RV travelers look for personal guidance on insurance, equipment use, and route planning, so in-person service at rental centers near national parks and highway hubs remains important. Customers arranging complex itineraries or lengthy trips still prefer face-to-face advice, keeping offline channels central to market revenue.

By Product Type: Motorized Dominance Reflects Self-Contained Preference

Motorized RVs led with a 53.01% share in 2025 because renters favor self-contained travel without towing. Class A units attract vacationers who need space and luxury; Class B vans appeal to younger, more mobile renters; and Class C models remain popular with families for practicality and ease of driving. Their comfort and versatility make motorized units the core of rental fleets, especially in regions with strong national park tourism.

Motorized RVs are also the fastest-growing product group, climbing at an 8.66% CAGR. Demand keeps rising for fully equipped vehicles with kitchens, bathrooms, and climate control. Manufacturers are improving interiors, safety features, and fuel economy, broadening appeal to newcomers. Longer-weekend travel habits and remote-work lifestyles favor comfortable on-the-road living, keeping motorized RVs at the center of market expansion.

By Rental Duration: Extended Stays Reflect Lifestyle Evolution

Short-term rentals of 1–7 days captured 52.82% of the market in 2025, mirroring the popularity of weekend getaways and quick vacations. These bookings offer low-commitment experiences ideal for families, young couples, and first-time renters. Companies support the trend with flexible pickup options, mid-week discounts, and curated short-route packages, ensuring short trips remain the backbone of demand.

As digital nomads and remote workers opt for extended travel, rentals spanning 8–30 days have emerged as the fastest-growing segment, boasting an 8.94% CAGR. These multi-week journeys allow travelers to seamlessly blend work and leisure while discovering picturesque locales. RVs, equipped with features such as solar panels, dedicated workspaces, and reliable connectivity, cater perfectly to this slow-travel trend, bolstering the mid-term category's role in market expansion. By 2025, the median annual RV usage surged to 30 days, marking a notable 50% increase from the 20 days recorded in the 2021 study[2]"Go RVing RV Owner Demographic Profile" RV Industry Association, rvia.org.

Geography Analysis

North America remains the largest revenue pool for RV rentals, accounting for 46.78% of the 2025 market, supported by a deep road-trip culture and an extensive campground network. Dispersed camping on public land adds capacity, though parking bans in dense urban areas deter spontaneous overnight stays. Cross-border rentals between the United States and Canada gain traction as insurance products become more standardized. Mexico attracts snowbird travelers seeking warmer winters, yet concerns over roadside assistance and vehicle security slow broader adoption. Continued consolidation among suppliers is likely as brands chase economies of scale in servicing and marketing.

Asia-Pacific is expected to grow at the fastest rate of 11.35% to 2031, driven by established outdoor-lifestyle cultures in Australia and emerging demand in China and India. Government initiatives to build rest areas and campgrounds accelerate first-time adoption among middle-class families. Insurance availability and right-hand-drive compatibility influence fleet composition, while compact vehicle formats meet urban parking constraints. Social-media-driven wanderlust pushes operators to curate photo-friendly itineraries that combine iconic landscapes with reliable connectivity. Partnerships with regional tourism boards provide credibility and marketing reach for early movers.

Europe benefits from visa-free Schengen travel and a dense supplier network that enables one-way, cross-border journeys. Seasonal shifts between northern and southern climates let operators rebalance fleets but also expose them to fuel-price volatility and evolving emissions regulations. Compact campervans remain popular due to tight village roads and higher fuel costs. Fragmented ownership creates space for local specialists to coexist alongside pan-European aggregators. Electrification pilots gain attention as cities adopt low-emission zones and travelers seek greener holiday options.

Competitive Landscape

The recreational vehicle rental market is moderately concentrated. Incumbent fleet operators pursue electrification pilots, telematics integration, and concierge add-ons such as guaranteed campsite bookings. These moves aim to deepen customer loyalty while defending against price erosion. Data-driven preventive maintenance reduces downtime and positions large fleets as reliable choices for risk-averse travelers. Marketing narratives increasingly emphasize safety certifications, 24-hour roadside assistance, and seamless booking to differentiate from smaller rivals. Strategic investment in charging infrastructure begins to shape long-term competitive moats.

Peer-to-peer platforms expand consumer choice by listing everything from vintage trailers to luxury motorhomes at a range of price points. Transparent reviews and owner-to-renter messaging foster trust, yet quality control remains an ongoing challenge. Insurance products tailored to one-off rentals reduce friction and build confidence among hesitant newcomers. Algorithmic pricing nudges owners toward market-clearing rates while rewarding early bookings. As platform liquidity improves, network effects make it harder for latecomers to gain traction without unique service propositions.

Mid-scale challengers focus on design-forward camper vans, pan-regional one-way drop-offs, and influencer-friendly branding to stand out. Urban regulations that restrict overnight parking push these companies to negotiate bespoke campground partnerships near destination cities. Venture funding fuels quick fleet expansion and the rollout of app-based customer touchpoints. Collaborations with outdoor-gear brands create cross-promotion opportunities that attract adventure-seeking millennials. Over time, ecosystem alliances around insurance, roadside assistance, and route planning are expected to drive partial consolidation within the segment.

Recreational Vehicle Rental Industry Leaders

-

Cruise America

-

Apollo Tourism & Leisure Ltd (ATL)

-

Outdoorsy Inc.

-

RV Share

-

McRent (Rental Alliance GmbH)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: RVshare, the largest community for RV owners and renters, unveiled new offerings to simplify RV travel for both novices and seasoned road trippers. With the peak travel season approaching, RVshare introduced One-Way Rentals, RVshare Getaways, and a dedicated RV Rental Advisor team. These additions provide travelers with flexible planning options, curated experiences at iconic national parks, and expert trip guidance.

- November 2025: Uber India broadened its Intercity luxury caravan service, launching in three major cities. Following its debut in Delhi, Uber's Intercity motorhomes are now rolling out in Mumbai, Pune, and Bangalore.

- August 2025: Roadsurfer, a camper van rental provider, clinched EUR 85 million (~USD 90 million) in funding. The Germany-based firm stated that the funds will fuel its "rapid growth" and bolster its fleet across North America and Europe.

- June 2025: Indie Campers, a prominent player in the recreational vehicle rental arena, is set for further global expansion. This comes on the heels of the company's successful EUR 62.5 million (~USD 66 million) funding round over the past year, which includes a freshly secured EUR 27.5 million (~USD 29 million) second tranche.

Global Recreational Vehicle Rental Market Report Scope

A recreational vehicle is a mobile dwelling vehicle that incorporates living quarters specifically designed for accommodation. RV rental is a service in which RVs are made available to users for hourly or daily rates, with the fee usually covering the rental period and mileage. The recreational vehicle rental market report covers the latest trends and technological developments.

The recreational Vehicle Rental market is segmented by rental supplier type, booking type, product type, rental duration, and geography. By Rental Supplier Type, the market is segmented into Private and Individual Owners and Fleet Operators. By Booking Type, the market is segmented into Offline Booking and Online Booking. By Product Type, the market is segmented into Motorized RVs (Class A Motorhomes, Class B Motorhomes, Class C Motorhomes) and Towable RVs (Fifth-Wheel Trailers, Travel Trailers, Truck Campers, and Sports Utility Trailers). By Rental Duration, the market is segmented into Short-term (1-7 days), Mid-term (8-30 days), and Long-term (More than 30 days). By Geography, the market is segmented into North America (United States, Canada, and Rest of North America), South America (Brazil, Argentina, and Rest of South America), Europe (Germany, United Kingdom, France, Spain, Italy, Russia, and Rest of Europe), Asia-Pacific (China, India, Japan, South Korea, Australia, and Rest of Asia-Pacific), and Middle East and Africa (United Arab Emirates, Saudi Arabia, Turkey, South Africa, and Rest of Middle East and Africa).

The report offers the market size and forecast in value (USD) for all the above segments.

By Rental Supplier Type

| Private and Individual Owners |

| Fleet Operators |

By Booking Type

| Offline Booking |

| Online Booking |

By Product Type

| Motorized RVs | Class A Motorhomes |

| Class B Motorhomes | |

| Class C Motorhomes | |

| Towable RVs | Fifth-Wheel Trailers |

| Travel Trailers | |

| Truck Campers | |

| Sports Utility Trailers |

By Rental Duration

| Short-term (1-7 days) |

| Mid-term (8-30 days) |

| Long-term (More than 30 days) |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Rental Supplier Type | Private and Individual Owners | |

| Fleet Operators | ||

| By Booking Type | Offline Booking | |

| Online Booking | ||

| By Product Type | Motorized RVs | Class A Motorhomes |

| Class B Motorhomes | ||

| Class C Motorhomes | ||

| Towable RVs | Fifth-Wheel Trailers | |

| Travel Trailers | ||

| Truck Campers | ||

| Sports Utility Trailers | ||

| By Rental Duration | Short-term (1-7 days) | |

| Mid-term (8-30 days) | ||

| Long-term (More than 30 days) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the recreational vehicle rental market growing through 2031?

It is forecasted to post a 5.82% CAGR between 2026 and 2031, lifted by peer-to-peer adoption and expanding digital bookings.

Which region offers the highest growth potential?

Asia-Pacific shows the fastest trajectory, with a projected 11.35% CAGR as infrastructure investment and rising incomes unlock first-time hires

Why are motorized RVs overtaking towables in rentals?

Integrated living amenities and easier setup appeal to remote workers and urban renters, pushing motorized RV revenue to 53.01% in 2025.

What is driving mid-term rental demand?

Remote-work policies encourage trips of 8-30 days, and operators now bundle discounts and co-working access to attract this segment.

How are operators addressing seasonality challenges?

Strategies include geographic repositioning to warmer states, dynamic off-season discounts, and diversification into corporate pop-up rentals.

Page last updated on: