Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

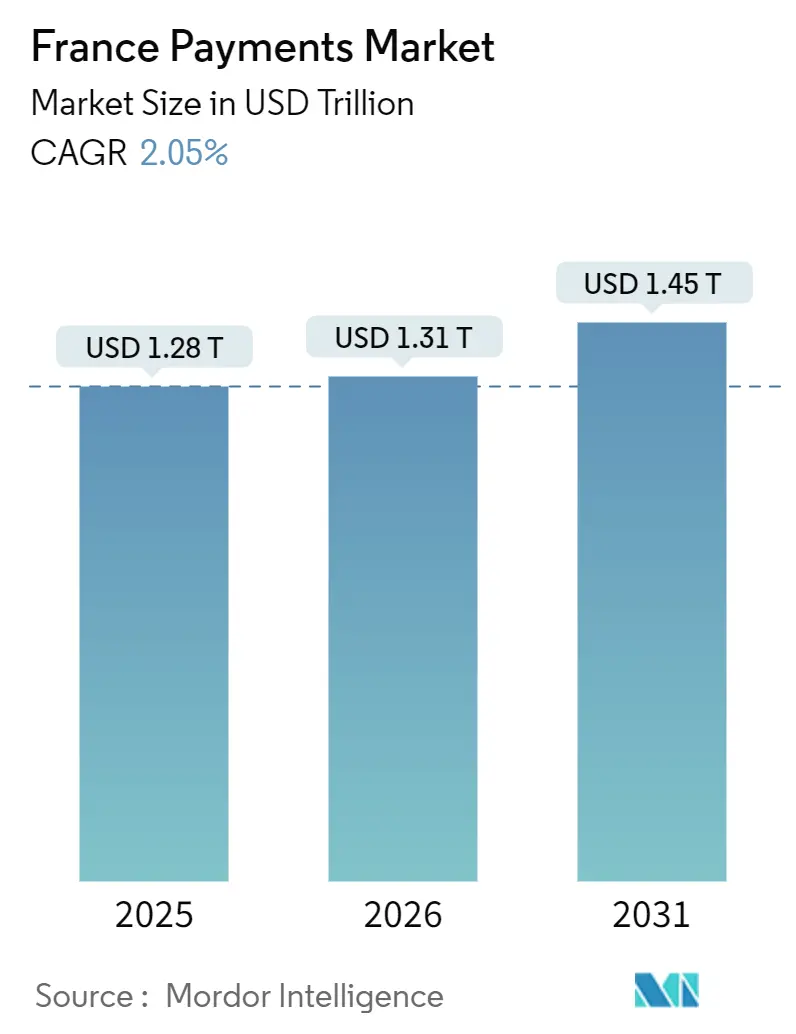

| Base Year Market Size (2025) | USD 1.28 Trillion |

| Market Size (2026) | USD 1.31 Trillion |

| Market Size (2031) | USD 1.45 Trillion |

| Growth Rate (2026 - 2031) | 2.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Payments Market Analysis by Mordor Intelligence

The France payments market size is expected to increase from USD 1.28 trillion in 2025 to USD 1.31 trillion in 2026 and reach USD 1.45 trillion by 2031, growing at a CAGR of 2.05% over 2026-2031. Ongoing implementation of SEPA Instant settlement, rising digital-wallet penetration among Gen-Z shoppers, and bank-led alternatives to international card networks are redrawing competitive boundaries. Real-time rails now settle funds in under 10 seconds, eroding the historical advantage of card authorization and clearing cycles. Simultaneously, SoftPOS technology is lowering acceptance costs for micro-merchants, while artificial-intelligence fraud engines lift authorization rates and reduce chargebacks. These forces combine to give account-to-account (A2A) transactions a credible path to scale even as contactless cards maintain primacy at point of sale.

Key Report Takeaways

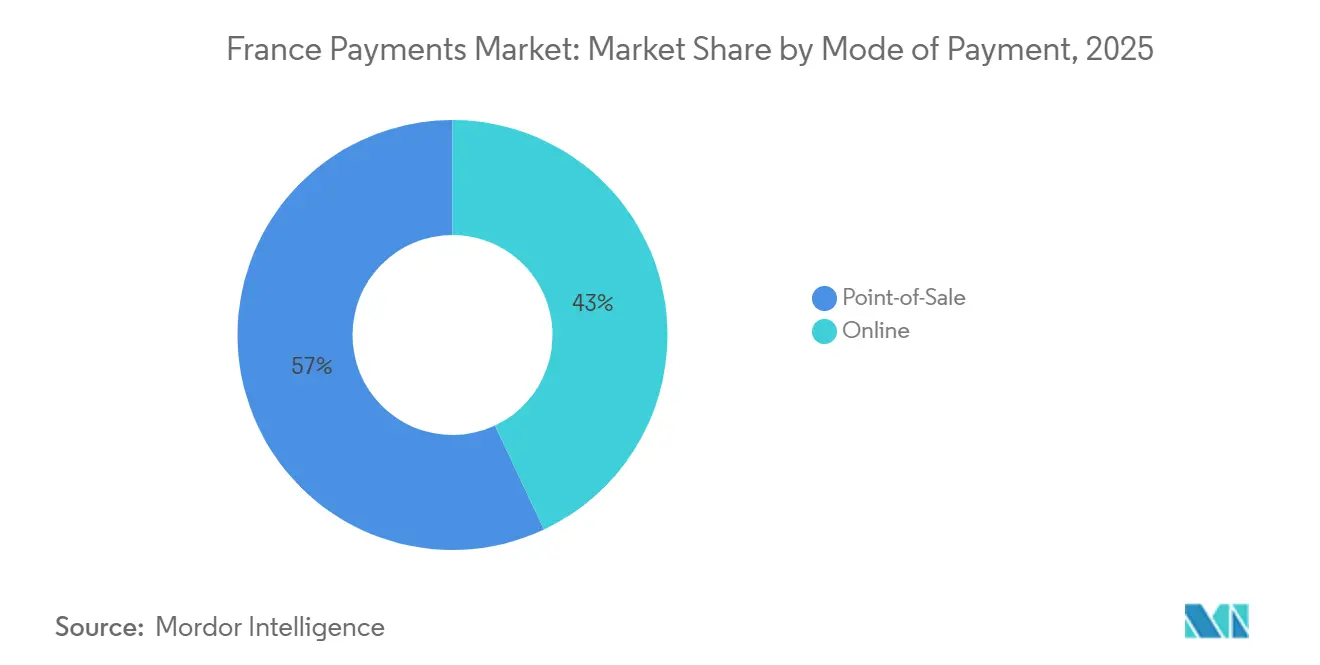

- By mode of payment, point-of-sale transactions led with 57.89% of France payments market share in 2025, whereas online channels are projected to post a 3.07% CAGR through 2031.

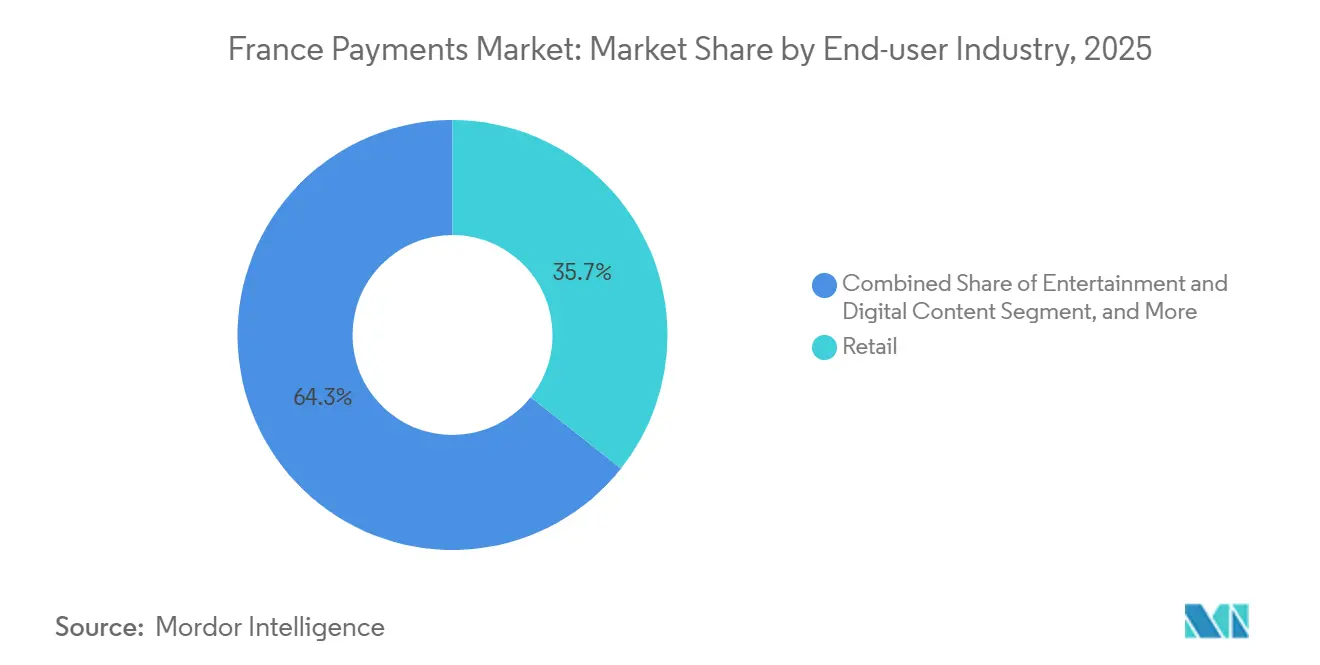

- By end-user industry, retail accounted for 35.67% of the France payments market size in 2025, while hospitality and travel are advancing at a 3.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Payments Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PSD2-Enabled Open-Banking Fuels Instant Account-to-Account Payments | +0.6% | France, broader EU alignment with SEPA Instant mandate | Medium term (2-4 years) |

| E-Commerce and M-Commerce Boom Among Gen-Z Spurs Digital Wallet Uptake | +0.5% | National, concentrated in Paris, Lyon, Marseille metropolitan areas | Short term (≤ 2 years) |

| Regulatory Increase of Contactless-Spend Limit Accelerates Tap-and-Go Transactions | +0.3% | National, higher adoption in urban centers | Short term (≤ 2 years) |

| Merchant Adoption of SoftPOS Turns Smartphones into Acceptance Terminals | +0.2% | National, early gains in micro-merchant and service sectors | Medium term (2-4 years) |

| Wero Wallet Launch Catalyzes A2A Real-Time Retail Payments Adoption | +0.2% | France with spillover to Germany and Belgium | Medium term (2-4 years) |

| AI-Driven Risk Decisioning Lifts Authorization Rates While Reducing Chargebacks | +0.1% | Global, used by major French issuers and acquirers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PSD2-Enabled Open-Banking Fuels Instant Account-to-Account Payments

Revised open-banking rules required French banks to expose application-programming interfaces, yet customer uptake remained limited until the SEPA Instant mandate took hold in 2025. The regulation now obliges every payment service provider to both receive and send real-time euro transfers, collapsing settlement windows from days to seconds.[1]European Central Bank, “SEPA Instant Payments Regulation Implementation,” ecb.europa.eu E-commerce platforms promptly embedded “Pay by Bank” buttons that authorize funds directly from current accounts, bypassing interchange altogether. Interoperability is assured because over 80% of French banks support the STET API framework.[2]STET, “French API Standardization Framework,” stet.eu Merchants enjoy lower costs and faster confirmation, while consumers gain a familiar, friction-free checkout that mirrors card tap-to-pay convenience.

E-Commerce and M-Commerce Boom Among Gen-Z Spurs Digital Wallet Uptake

French online spending reached EUR 150 billion (USD 160 billion) in 2024, with mobile devices capturing 43% of transactions.[3]Fédération du e-commerce et de la vente à distance, “E-commerce Statistics 2024,” fevad.com A 2025 survey found 62% of shoppers aged 18-25 store at least one credential in Apple Pay, Google Pay, Lydia, or Paylib. These wallets bundle loyalty IDs, transport passes, and tickets alongside payment instruments, trimming checkout to a single biometric confirmation. Lydia’s user base climbed to 8 million by late 2025, aided by QR acceptance and installment finance options. As Gen-Z purchasing power expands, merchants that optimize for mobile wallets record higher conversion and larger average order values.

Regulatory Increase of Contactless-Spend Limit Accelerates Tap-and-Go Transactions

Elimination of the EUR 50 (USD 54.4) ceiling in 2024 removed the last psychological hurdle to contactless adoption. Consumers now tap cards or NFC phones for everyday baskets without a second thought, and retailers report checkout-time reductions of roughly 15% after rolling out multi-purpose tap flows that combine payment with loyalty and e-receipt delivery.[4]NFC Forum, “Multi-Purpose Tap Specifications,” nfc-forum.org Compliance with tokenization mandates in PCI DSS 4.0 further reduces fraud risk, persuading risk-averse grocers and fuel stations to steer customers toward tap-and-go experiences.

Merchant Adoption of SoftPOS Turns Smartphones into Acceptance Terminals

Certification of Ingenico’s AXIUM platform under France’s FRv6 security standard in February 2026 lets any modern Android handset accept EMV contactless payments. Micro-merchants such as food-truck operators and tradespeople avoid hardware rental fees and onboard in minutes through their acquirer’s app. Worldline reported French SoftPOS activations expanded 34% quarter-on-quarter during 2025, signaling strong latent demand for low-cost acceptance. As acceptance fragments, competition among acquirers intensifies and legacy terminal vendors pivot toward software-as-a-service revenue.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Card Interchange and Scheme Fees Pressure SME Margins | -0.4% | National, acute for small and medium enterprises | Short term (≤ 2 years) |

| Ageing and Rural Population’s Persistent Cash Preference | -0.3% | Rural departments, peripheral regions | Long term (≥ 4 years) |

| Dependency on Non-European Card Processors Heightens Sovereignty and Cost Risks | -0.2% | France, broader EU concern | Medium term (2-4 years) |

| Real-Time Authorized Push-Payment Fraud Undermines Consumer Trust in Instant Rails | -0.2% | National, cross-border implications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Card Interchange and Scheme Fees Pressure SME Margins

Although EU law caps interchange at 0.2% on debit and 0.3% on credit, unregulated scheme fees continue to rise and can lift the effective charge well above 1%. For a neighborhood bakery turning over EUR 200,000 (USD 237,440) annually, that difference erodes thin operating margins and discourages card acceptance. Many SMEs are experimenting with Wero or Carte Bancaires A2A options that levy flat-fee or subscription pricing, but cross-border reach remains limited, complicating e-commerce ambitions.

Ageing and Rural Population’s Persistent Cash Preference

One-fifth of France’s residents are 65 years or older, and surveys show 59% of consumers still rely on cash for at least some purchases. Rural communes, where broadband coverage and smartphone penetration trail urban averages, typically lag 18-24 months in adopting contactless or wallet payments. The Banque de France guarantees cash availability through 2030, obliging providers to run dual infrastructures even as digital volumes grow. This requirement inflates operating costs and dilutes the efficiency benefits of an all-electronic ecosystem.

Segment Analysis

By Mode of Payment: Online Channels Gain Share as Instant Rails Mature

Online transactions represented 42.11% of total value in 2025 and are forecast to post a 3.07% CAGR through 2031, outpacing headline France payments market growth. Point-of-sale still leads, yet the share of tap-to-pay wallets inside physical stores climbed steadily as EMV acceptance reached 98% of terminals. Instant SEPA transfers embedded in checkout flows remove the need to enter 16-digit card numbers, trimming abandonment rates and lowering merchant costs.

Digital wallets aggregate debit cards, credit cards, and A2A mandates within a single interface, encouraging users to toggle between instruments without leaving the merchant page. Klarna’s installment pay option gained 22% more French merchants in 2025, illustrating consumer appetite for deferred settlement. As tokenization under EMVCo standards becomes ubiquitous, the France payments market size for online channels will continue to rise on the back of lower fraud and higher approval rates.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Hospitality Rebounds as Travel Normalizes

Retail maintained a 35.67% share of France payments market value in 2025, supported by high-frequency grocery and fuel baskets and broad contactless terminal penetration. Hospitality and travel, however, recorded the fastest growth at a 3.24% CAGR, buoyed by tourist inflows and the sector’s investment in tap-and-go experiences. Hotels and restaurants processed EUR 42 billion (USD 45 billion) in 2025, with mobile-wallet usage hitting 61%.

Entertainment, streaming, and gaming rely heavily on stored credentials and recurring billing, positioning tokenized cards and digital wallets as the default rails. Government agencies likewise accelerate digital adoption, with 78% of personal tax payments completed online in 2025. Healthcare is digitizing the Carte Vitale into a smartphone app, opening a new front in real-time copayment processing and broadening the addressable France payments industry opportunity.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

France’s integration into SEPA provides a unified legal and technical framework for real-time euro payments across 36 countries. Domestic banks invested more than EUR 500 million (USD 535 million) during 2024-2025 to retrofit core systems for instant transfers and to embed Wero wallet functionality. These upgrades give French acquirers an early-mover advantage over peers in Southern Europe, where instant implementation lags.

Urban centers dominate digital adoption: Paris, Lyon, Marseille, and Toulouse account for nearly half of wallet-based transactions though they represent only one-third of the population. Younger demographics, higher smartphone penetration, and denser acceptance networks explain the outperformance. Rural departments such as Creuse and Lozère remain cash-centric, reflecting older demographics and patchy broadband.

Cross-border commerce benefits from Wero’s rollout into Germany, Belgium, and Luxembourg, offering 60 million consumers a pan-European A2A option that bypasses U.S. card networks. Draft PSD3 rules will add Confirmation of Payee checks on transfers above EUR 100 (USD 118.7), harmonizing fraud-control standards across SEPA and bolstering trust in instant rails.

Competitive Landscape

The France payments market balances concentrated global card schemes with a mosaic of domestic and regional challengers. Visa and Mastercard still clear the majority of transaction value, but Wero processed more than 200 million transfers in its first full year, proving bank-led initiatives can scale when aligned with regulation. Worldline’s 2025 acquisitions expanded its French merchant base beyond 1 million acceptance points, creating data scale that underpins machine-learning fraud models.

Stripe’s Radar analyzes hundreds of behavioral signals per transaction and lifted approval rates for domestic merchants by 3.2 percentage points in 2025. Ingenico responded by shifting from hardware sales to AXIUM subscription bundles after SoftPOS began to commoditize basic acceptance. Lydia leverages its eight-million-strong user base to pitch installment finance, QR payments, and loyalty integration, effectively unbundling traditional acquirer economics.

Regulation accelerates competitive churn. SEPA Instant settlement forces acquirers to build out 24×7 liquidity management, PSD2 APIs open account data to third parties, and upcoming PSD3 rules tighten fraud liability. Players unable to fund real-time risk engines or open-banking integrations risk ceding share to agile fintechs, especially in online and micro-merchant niches.

France Payments Industry Leaders

Apple Inc. (Apple Pay)

Paylib SAS

Samsung Electronics Co., Ltd. (Samsung Pay)

Carrefour S.A. (Carrefour Pay)

Google LLC (Google Pay)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2026: Ingenico launched AXIUM, a SoftPOS solution certified under France’s FRv6 standard, enabling Android phones to accept contactless payments.

- October 2025: The European Central Bank confirmed all French providers met the SEPA Instant sending deadline, completing nationwide real-time coverage.

- July 2025: Stripe reported its Radar engine raised French merchant authorization rates by 3.2 percentage points during 2025.

- July 2025: Worldline disclosed that French SoftPOS activations rose 34% quarter-on-quarter, pushing its acceptance footprint past 1 million outlets.

France Payments Market Report Scope

The payments market in France refers to the various ways in which individuals and businesses make transactions and transfer funds within the country. This includes traditional payment methods like cash, checks, and bank transfers, as well as electronic and mobile payments, such as credit and debit cards, e-wallets, and mobile payment apps.

The France Payments Market Report is Segmented by Mode of Payment (Point of Sale, Online Sale, Digital Wallets), End-user Industry (Retail, Entertainment and Digital Content, Healthcare, Hospitality and Travel, Government and Utilities), and Geography (France). The Market Forecasts are Provided in Terms of Value (USD).

By Mode of Payment

| By Point of Sale | Card Payments | Debit Cards |

| Credit Cards | ||

| Bank Financing Prepaid Cards | ||

| Digital Wallets (includes Mobile Wallet) | ||

| Other Point of Sale | ||

| By Online Sale | Card Payments | Debit Cards |

| Credit Cards | ||

| Bank Financing Prepaid Cards | ||

| Digital Wallets | ||

| Other Online Sales (includes Cash on Delivery, Bank Transfer, and Buy Now Pay Later) | ||

| Digital Wallets | ||

| Other Online Sales (includes Cash on Delivery, Bank Transfer, and Buy Now Pay Later) |

By End-user Industry

| Retail |

| Entertainment and Digital Content |

| Healthcare |

| Hospitality and Travel |

| Government and Utilities |

| Other End-user Industries |

| By Mode of Payment | By Point of Sale | Card Payments | Debit Cards |

| Credit Cards | |||

| Bank Financing Prepaid Cards | |||

| Digital Wallets (includes Mobile Wallet) | |||

| Other Point of Sale | |||

| By Online Sale | Card Payments | Debit Cards | |

| Credit Cards | |||

| Bank Financing Prepaid Cards | |||

| Digital Wallets | |||

| Other Online Sales (includes Cash on Delivery, Bank Transfer, and Buy Now Pay Later) | |||

| Digital Wallets | |||

| Other Online Sales (includes Cash on Delivery, Bank Transfer, and Buy Now Pay Later) | |||

| By End-user Industry | Retail | ||

| Entertainment and Digital Content | |||

| Healthcare | |||

| Hospitality and Travel | |||

| Government and Utilities | |||

| Other End-user Industries | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the France payments market in 2031?

It is expected to reach USD 1.45 trillion by 2031, reflecting a 2.05% CAGR over 2026-2031.

Which payment mode is expanding fastest?

Online channels are forecast to grow at a 3.07% CAGR to 2031, outpacing point-of-sale transactions.

How large is retail's share of transaction value?

Retail accounted for 35.67% of total value in 2025, the largest share among end-user industries.

Why are SoftPOS solutions important for micro-merchants?

They convert Android phones into terminals, eliminating hardware rental fees and broadening digital acceptance in cash-heavy segments.

What competitive threat do Wero and similar A2A wallets pose?

They bypass interchange-based card rails, offering real-time settlement and lower merchant costs that challenge Visa and Mastercard's dominance.