Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

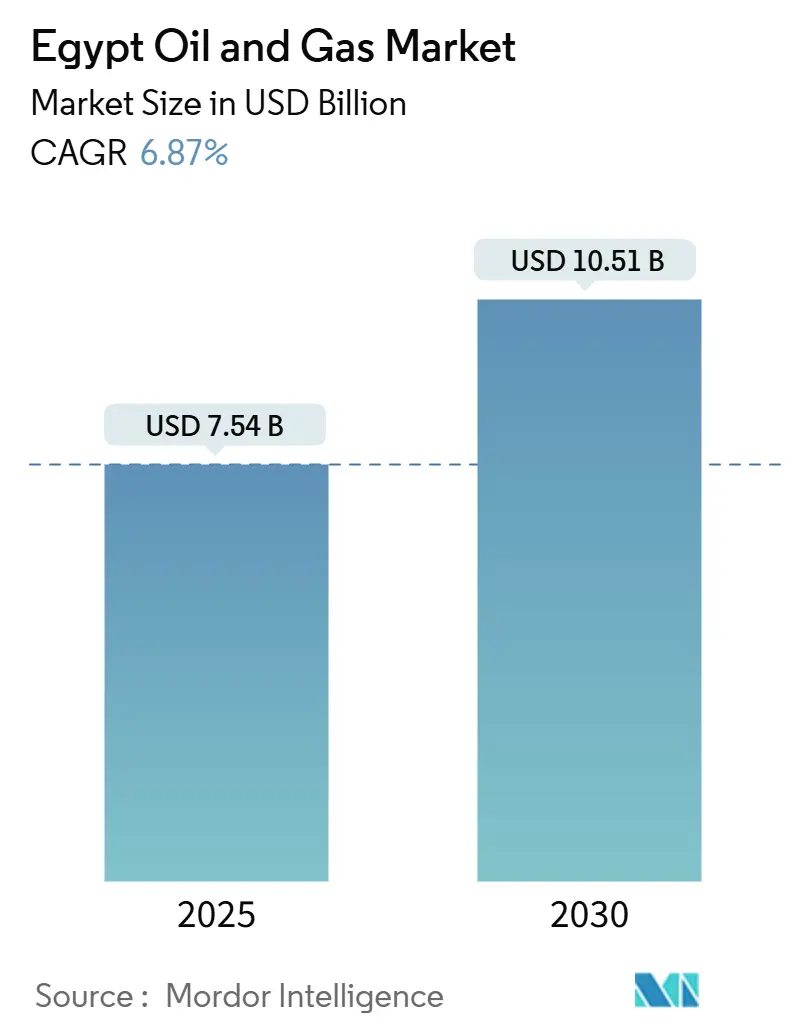

| Market Size (2025) | USD 7.54 Billion |

| Market Size (2030) | USD 10.51 Billion |

| Growth Rate (2025 - 2030) | 6.87% CAGR |

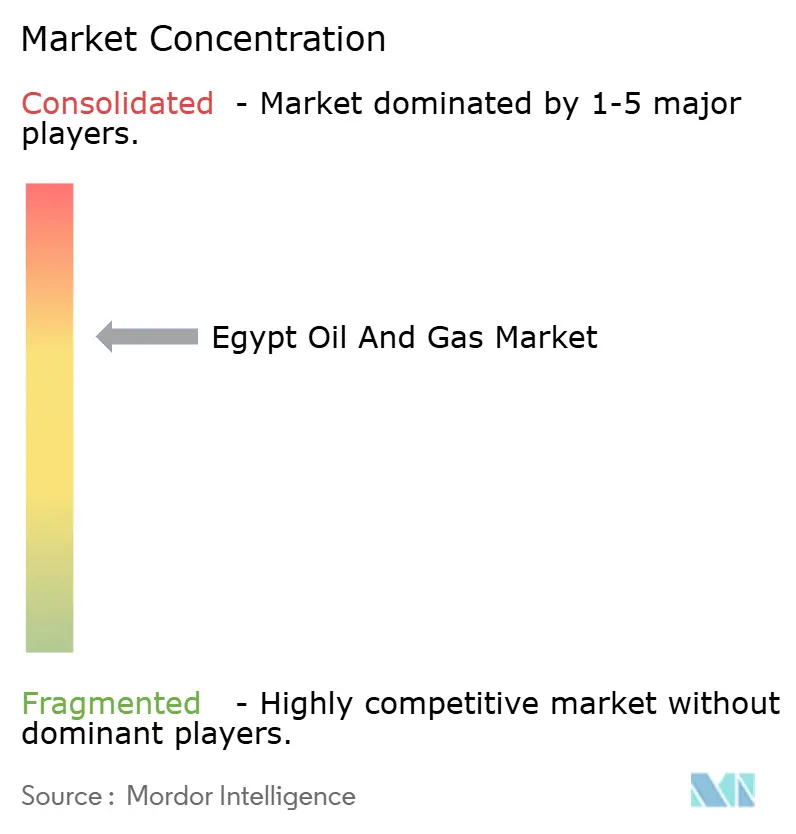

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Egypt Oil And Gas Market Analysis by Mordor Intelligence

The Egypt Oil And Gas Market size is estimated at USD 7.54 billion in 2025, and is expected to reach USD 10.51 billion by 2030, at a CAGR of 6.87% during the forecast period (2025-2030).

Investment momentum originates from offshore gas discoveries, revived megaprojects, and a renewed financing cycle led by international majors. Rising domestic demand, a maturing asset base, and an improving fiscal regime combine with Egypt’s position as a Mediterranean energy corridor to sustain upstream capital flows even as the country intermittently turns to LNG imports during peak‐load months.[1]“BP to Spend USD 3.5 Billion on Egypt Exploration,” reuters.com Construction spending continues to dominate overall outlays, yet maintenance and turnaround services expand faster as operators pivot from capacity additions toward efficiency gains in a tightening cost environment. Digital oilfield adoption, together with fiscal and regulatory reforms that improve project IRRs by roughly 200-300 basis points, lowers break-even costs and shortens payback cycles, making Egyptian prospects increasingly attractive relative to neighboring plays.[2]“Digital Gateway Accelerates Licensing,” energycentral.com Geopolitical proximity to European gas demand and the government’s East-Med hub vision create commercial optionality for surplus volumes, while fast-track gas-to-power programs protect revenues during commodity price swings.

Key Report Takeaways

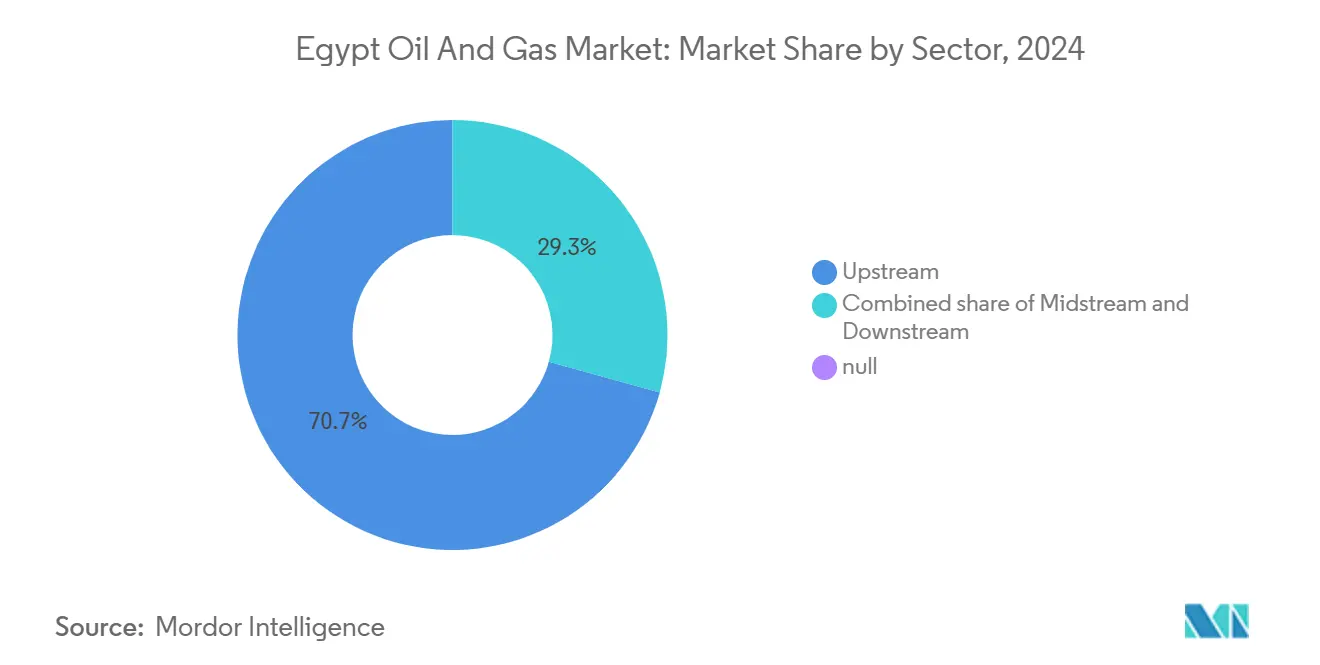

- By sector, upstream commanded 70.7% of Egypt's oil and gas market share in 2024 and is projected to grow at a 7.2% CAGR through 2030.

- By location, onshore sites delivered 56.0% of 2024 revenue, whereas offshore developments are forecast to expand at a 7.4% CAGR between 2025-2030.

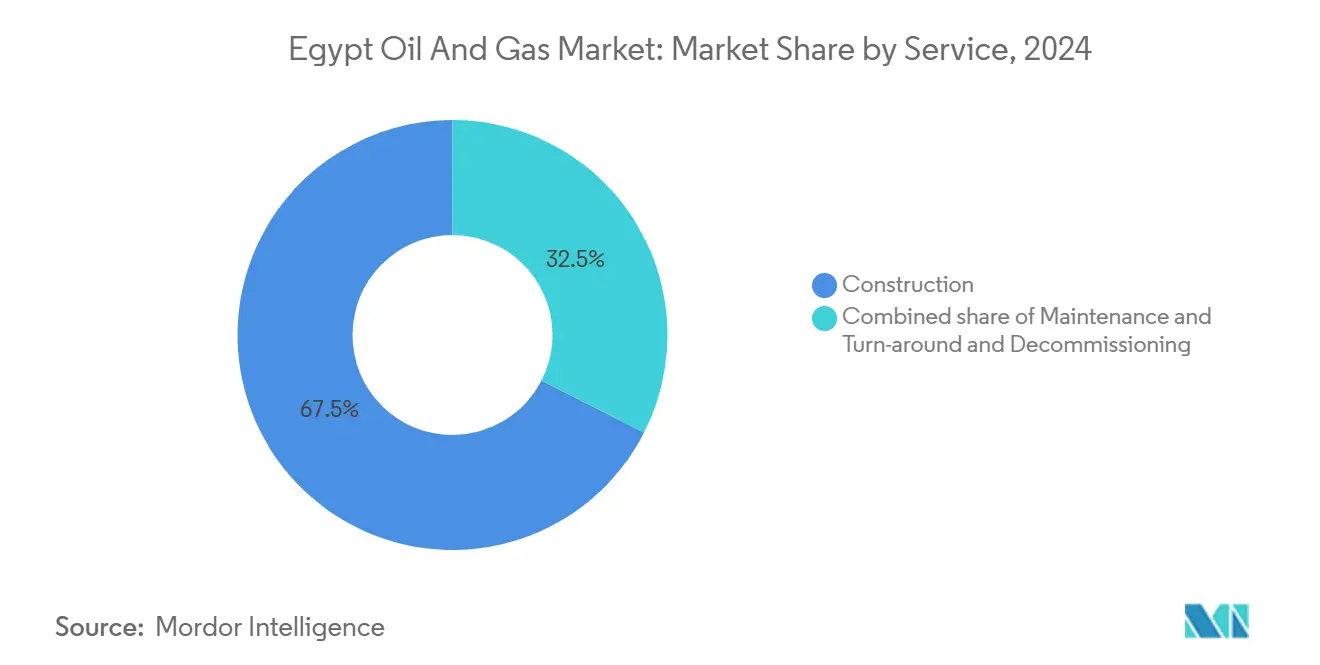

- By service, construction accounted for 67.5% of Egypt's oil and gas market size in 2024; maintenance and turnaround services represent the fastest-growing asset class with a 7.7% CAGR to 2030.

Egypt Oil And Gas Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Revival of offshore gas megaprojects | 1.80% | Mediterranean offshore blocks, Eastern Delta | Medium term (2-4 years) |

| Accelerated IOC & NOC upstream CAPEX commitments | 1.50% | National, Western Desert and offshore | Short term (≤ 2 years) |

| Fast-track gas-to-power programs | 1.20% | Nationwide, industrial zones | Medium term (2-4 years) |

| Fiscal-regime reforms improving project IRRs | 0.90% | National licensing rounds | Long term (≥ 4 years) |

| Adoption of digital oilfield & remote operations | 0.70% | Western Desert, Gulf of Suez mature fields | Short term (≤ 2 years) |

| Planned East-Med gas hub & LNG re-export vision | 0.60% | Eastern Mediterranean | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Revival of Offshore Gas Megaprojects (e.g., Zohr)

Zohr’s January 2025 drilling restart restored momentum to Egypt’s offshore renaissance and renewed confidence in deep-water prospects.[3]“Eni Restarts Zohr Drilling,” reuters.com Fresh wells and tie-backs shorten ramp-up times, allowing Eni to monetize incremental reserves while de-risking adjacent acreage held by BP and Chevron. Project economics benefit from shared pipelines and processing facilities, which lower per-unit costs and improve field-level break-even thresholds. Success at Zohr also underpins Egypt’s diplomatic leverage in European energy security discussions as buyers seek diversified gas supply corridors. As a bellwether for the Egyptian oil and gas market, Zohr’s performance shapes capital-allocation decisions across the wider Mediterranean play.

Accelerated IOC & NOC Upstream CAPEX Commitments

International oil companies have earmarked more than USD 17 billion for Egyptian upstream activity through 2030, the largest pledge since the 2011 transition.[4]Ministry of Petroleum, “Gas Grid Expansion Update,” sis.gov.eg BP’s USD 3.5 billion three-year program, Shell’s USD 340 million Cheiron partnership, and Chevron’s new Western Desert acreage exemplify the deal flow. The prompt settlement of USD 1.5 billion in arrears removed a key credit risk overhang and unblocked suspended drilling plans. This fresh capital intensifies rig demand, accelerates seismic acquisition, and opens technology transfer pathways that raise local service quality benchmarks. Competitive pressures are therefore reshaping the Egyptian oil and gas market as agile, technology-focused independents challenge long-entrenched majors in select blocks.

Fast-Track Gas-to-Power Programs to Curb Power Deficit

Power generation currently absorbs roughly 75-80% of national gas output, anchoring offtake for new upstream barrels even during price slumps. The state has connected 9 million homes to the gas grid within nine years and aims to reach 15 million by 2030, thereby embedding long-term demand. Vehicle conversions to compressed natural gas topped 540,000 units by early 2025, diversifying end-use markets. Although the 42% renewables goal will curb incremental gas burn, utilities continue to rely on gas-fired plants as a reliability back-stop, mitigating demand volatility. World Bank loan support for generation upgrades further locks in offtake for upstream producers.

Fiscal-Regime Reforms Improving Project IRRs

Egypt’s revised production-sharing terms ease cost-recovery limits, reduce signature bonuses, and introduce accelerated depreciation schedules that lift project IRRs by an estimated 200-300 basis points. A digital one-stop portal expedites licensing approvals, trimming cycle times and administrative costs. The reforms render marginal fields and EOR projects commercially viable, unlocking reserves previously stranded by high lifting costs. Payment‐arrears resolution signals fiscal reliability, a pivotal factor for credit committees. Combined, these measures nudge the Egyptian oil and gas market toward a more competitive global cost curve.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising renewable-energy share in power mix | -1.10% | Upper Egypt solar zones, national grid | Medium term (2-4 years) |

| Ongoing fuel-subsidy rationalization | -0.80% | Nationwide petroleum markets | Short term (≤ 2 years) |

| Water-scarcity constraints on fracking & EOR | -0.50% | Western Desert, Upper Egypt | Long term (≥ 4 years) |

| Prospective EU carbon border taxes | -0.30% | Export-oriented refineries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Renewable-Energy Share in Egypt's Power Mix

The 42% renewables target for 2030 will increase solar and wind penetration from 12% in 2024, thereby directly reducing the dispatch of gas-fired power. Utility-scale projects under the Nexus of Water-Food-Energy program add 4.2 GW, backed by USD 3.9 billion in concessional finance. Grid upgrades worth EGP 7.6 billion (USD 154 million) enable higher renewable utilization while retaining gas plants for inertia and peak shaving. As the levelized costs of solar fall below gas parity, dispatch orders shift, curtailing gas offtake during daytime hours. Backup capacity requirements nevertheless preserve a baseline market for upstream producers, moderating but not eliminating the impact on the Egyptian oil and gas market.

Ongoing Fuel-Subsidy Rationalization

Monthly subsidy outlays of EGP 10 billion (USD 197 million) are being phased out to meet a 2025 elimination deadline. Rising pump prices erode demand for gasoline and fuel oil, accelerating a modal shift toward CNG vehicles and prompting industrial fuel switching. The World Bank-advised glide path aims to minimize social unrest, yet consumption elasticity is already evident in lower refined-product uplift at distribution terminals. Reduced domestic burn frees barrels for export, partially offsetting revenue losses but exposing refiners to international spreads and prospective carbon border adjustments. The subsidy rollback, therefore, creates both demand-side drag and portfolio-mix challenges that operators must navigate in the Egyptian oil and gas market.

Segment Analysis

By Sector: Upstream Dominance Drives Digital Transformation

The upstream segment generated 70.7% of 2024 revenue, underscoring its central role in the Egyptian oil and gas market. It is also the fastest-growing, set to rise at a 7.2% CAGR through 2030 as operators fast-track drilling across Zohr, North Dabaa, and Raven blocks. International commitments exceeding USD 17 billion provide the capital base for 3D seismic surveys, high-specification rigs, and subsea tie-backs, aimed at lifting national output back above 2.5 million barrels of oil equivalent per day. Digital subsurface interpretation on the Egypt Upstream Gateway accelerates prospect maturation, while AI well-placement tools optimize drainage patterns and cut dry-hole risk. Consequently, upstream cost structures continue to compress, enhancing netbacks despite volatile benchmarks.

Midstream infrastructure remains the logistical backbone of the Egyptian oil and gas market, yet it captures a smaller share of new spending. Pipeline connectivity to Israeli fields and capacity upgrades at the Idku and Damietta LNG terminals expand regional optionality, but the newbuild cadence is paced to align with the commissioning of upstream phases. Downstream growth faces headwinds from fuel-subsidy reforms and looming carbon levies, prompting refiners to pursue integration with petrochemical complexes and to pilot energy-efficiency retrofits. Collectively, the sectoral balance is shifting toward a technology-enabled, export-oriented upstream while the downstream focuses on resilience and decarbonization.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Location: Offshore Expansion Challenges Onshore Maturity

Onshore assets contributed 56.0% of 2024 turnover, reflecting Egypt's legacy production base across the Western Desert and Gulf of Suez. These mature fields benefit from existing infrastructure, providing low-cost barrels that underpin cash flow supportive of corporate dividend policies. Enhanced recovery pilots employing polymer floods and CO₂ injection aim to arrest natural decline rates. However, water scarcity and gas reinjection limitations cap the scalable upside, rendering most onshore additions marginal in terms of volume.

Offshore acreage is set to eclipse onshore growth, expanding at a 7.4% CAGR and reshaping the Egypt oil and gas market share profile to favor deep-water plays. Eni's success at Zohr has validated the carbonate play concept, sparking interest in bid rounds for contiguous blocks. Although capex intensity is higher—subsea trees, FPSOs, and high-spec jack-ups drive day rates upward—economies of scale emerge through shared export pipelines and processing topsides. The state's payment-settlement program has further reduced the perceived risk of offshore receivables, shifting portfolio allocation within IOC budgets toward Mediterranean prospects. Consequently, offshore's contribution to Egypt's oil and gas market size is poised to approach parity with onshore volumes by the end of the decade.

By Service: Construction Leads While Maintenance Gains Strategic Importance

Construction activities captured 67.5% of overall spending in 2024, mirroring Egypt’s project-build phase characterized by new pipelines, gas processing trains, and storage caverns. Large-ticket EPC contracts such as the USD 400 million Leviathan tie-in and midstream expansions at GASCO constitute headline award values. Yet operators increasingly scrutinize lifecycle cost and asset reliability, shifting incremental budgets toward brownfield optimization.

Maintenance and turnaround work streams are forecast to grow at a 7.7% CAGR, the fastest within the Egyptian oil and gas market. Digital twin deployment on legacy platforms yields predictive analytics that reduce downtime and defer capex on replacement equipment. Contractors offering integrated inspection-repair packages thus command premium day rates, while regulatory requirements for reducing flares and detecting leaks drive mandatory retrofit cycles. Decommissioning remains in its early stages, primarily limited to aging Gulf of Suez jack-up platforms; however, long-range planning has begun as part of ESG reporting obligations.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Domestic operations remain the primary focus of investment, yet regional linkages are increasingly influencing strategy. Egypt’s central location connects sub-Saharan resources to Mediterranean markets, positioning the country as a pivotal transit node. The Eastern Mediterranean Gas Forum formalizes this role, aligning regulatory frameworks and facilitating pipeline interconnections that could transform trade flows over the next decade. Upstream risk-reward, combined with a stable political climate compared to neighbors, cements Egypt’s draw for capital.

In North Africa, cross-border collaboration remains constrained by security issues in Libya and Algeria’s preference for exporting to Europe. Nevertheless, gas-swap mechanisms via LNG terminals offer interim pathways to optimize regional supply. To the east, ties with Israel and Cyprus deepen, delivering feed gas volumes that compensate for domestic seasonal deficits. These imports, regasified at Damietta or Idku, sustain local supply, though they temper immediate re-export ambitions under the East-Med hub blueprint.

Looking south, Egyptian NOCs and service firms eye sub-Saharan prospects, leveraging experience to secure EPC and O&M contracts in Tanzania, Mozambique, and Uganda. Such outward expansion diversifies revenue and embeds Egypt in pan-African energy networks. Although pipeline logistics remain embryonic, geopolitical alignments aligned with the African Continental Free Trade Area could catalyze future corridor development, further embedding Egypt within continental energy value chains.

Competitive Landscape

The Egyptian oil and gas market is moderately concentrated, with the top five operators—Eni, BP, Shell, Chevron, and Apache—collectively accounting for just under 60% of upstream output. State entities EGPC, EGAS, and GASCO retain sovereign stakes in most concessions and critical infrastructure, ensuring policy alignment and continuity. New entrants, notably Dragon Oil and Cheiron, leverage niche technologies and flexible governance structures to carve share in redeveloped mature fields.

Digitalization serves as the newest competitive battleground. Early adopters of AI-driven reservoir management report double-digit cost savings, a material edge in license bid evaluations. Partnerships between global service majors and local EPC houses facilitate technology assimilation, while the Egypt Upstream Gateway levels the data-access playing field for smaller bidders. Fiscal incentives further entice independents prepared to accept higher operating complexity in exchange for preferential profit-oil splits.

Environmental performance emerges as a differentiator amid tightening EU import standards. Operators are trialling flare-gas recovery, CCS pilots, and solar-powered modular rigs to reduce Scope 1 emissions. Those able to certify lower carbon intensity gain marketing advantage with European refiners and utility buyers, reinforcing brand equity and mitigating future tariff exposure. As a result, competitive dynamics increasingly combine volume metrics with carbon efficiency benchmarks.

Egypt Oil And Gas Industry Leaders

-

Eni SpA

-

BP PLC

-

Shell PLC

-

Apache Corp.

-

Chevron Corp.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: Archeos Energy has opened talks with the Ministry of Petroleum regarding an expanded upstream capital program in Egypt; the financial terms remain undisclosed.

- January 2025: Eni restarted drilling at Zohr after settling receivables, aiming to lift plateau output through additional wells.

- January 2025: The Ministry of Petroleum confirmed incremental production of 200 MMcf/d of gas and 39,000 b/d of crude between July and October 2024, following clearance of arrears.

- October 2024: EGAS and DESFA signed an MoU on CCS technologies; GASCO partnered with DESFA on natural-gas and hydrogen transport; EGPC and Shell launched a health-and-safety training alliance.

Egypt Oil And Gas Market Report Scope

The oil and gas industry is a sector that involves the exploration, extraction, refining, and distribution of petroleum products, natural gas, and other hydrocarbons. It encompasses a wide range of activities, including upstream activities such as exploration and production, midstream activities such as transportation and storage, and downstream activities such as refining and marketing.

Egypt's oil and gas market is segmented by sector. By sector, the market is segmented into upstream, midstream, and downstream.

For each segment, the market sizing and forecasts have been done based on oil consumption and refined capacity (thousands of barrels per day), gas consumption (billion cubic feet per day), and CAPEX (USD).

By Sector

| Upstream |

| Midstream |

| Downstream |

By Location

| Onshore |

| Offshore |

By Asset Type

| Construction |

| Maintenance and Turn-around |

| Decommissioning |

| By Sector | Upstream |

| Midstream | |

| Downstream | |

| By Location | Onshore |

| Offshore | |

| By Asset Type | Construction |

| Maintenance and Turn-around | |

| Decommissioning |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the Egypt oil and gas market in 2030?

The market is expected to reach USD 10.51 billion by 2030 on a 6.87% CAGR.

Which segment leads spending within Egyptian oil and gas?

Upstream dominates with a 70.7% revenue share in 2024.

How fast is offshore activity growing relative to onshore?

Offshore revenue is forecast to increase at a 7.4% CAGR, outpacing onshore’s growth rate.

What fiscal reforms are attracting foreign investment?

Reduced signature bonuses, accelerated depreciation and improved cost-recovery terms have lifted project IRRs by roughly 200-300 basis points.

How is Egypt addressing gas demand from the power sector?

The state has connected 9 million homes to the gas grid and relies on gas-fired plants for 75-80% of power generation, even as renewables rise.

Which digital tools are reshaping Egyptian upstream operations?

AI-driven reservoir modeling, digital twins and the Egypt Upstream Gateway are lowering exploration risk and boosting recovery factors.

Page last updated on: