Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

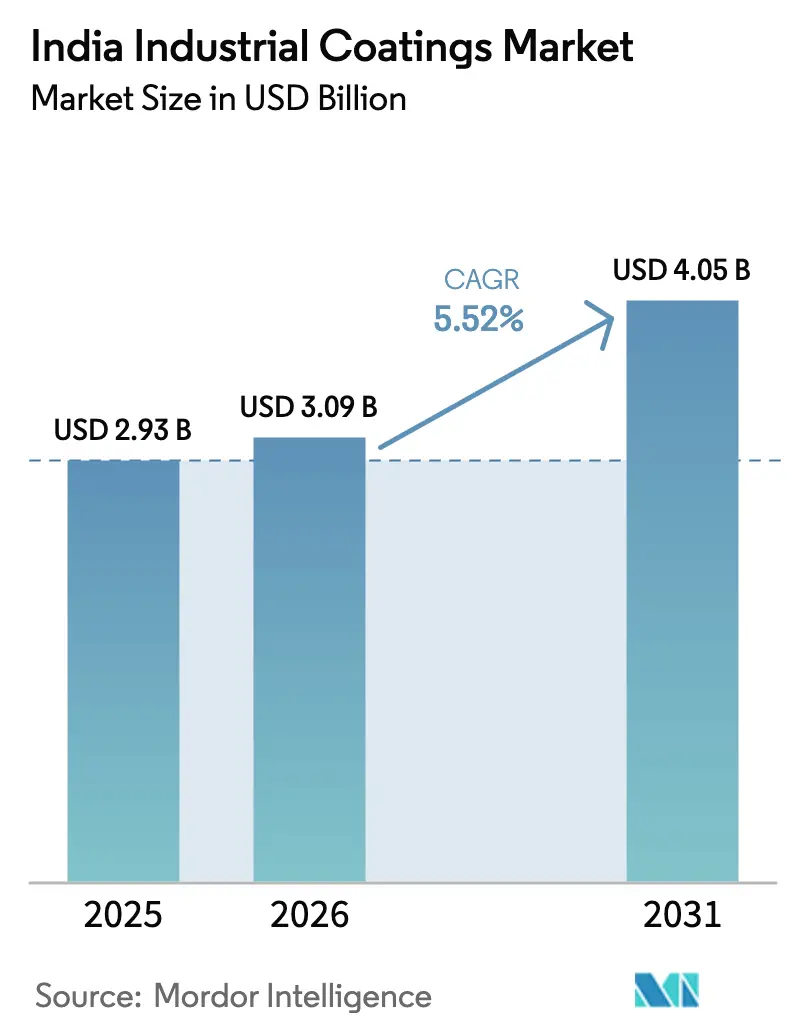

| Base Year Market Size (2025) | USD 2.93 Billion |

| Market Size (2026) | USD 3.09 Billion |

| Market Size (2031) | USD 4.05 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Industrial Coatings Market Analysis by Mordor Intelligence

The India Industrial Coatings market is expected to grow from USD 2.93 billion in 2025 to USD 3.09 billion in 2026 and is forecast to reach USD 4.05 billion by 2031 at 5.52% CAGR over 2026-2031. Stable demand from machinery, automotive, energy, and infrastructure projects underpins this outlook, while resin and technology upgrades are widening the price–performance spectrum across segments. Resin suppliers are scaling epoxy capacity to serve pipeline and marine projects, yet polyurethane chemistries are gaining share as OEMs require flexible, high-build finishes for electric-vehicle battery housings. Tighter volatile organic compound (VOC) norms are expected to accelerate investment in waterborne and powder plants, particularly in western and southern manufacturing hubs. Competitive intensity is rising as multinationals deepen joint ventures that fuse global R&D with local feedstock integration, while regional specialists leverage rapid technical service responses to protect mid-tier accounts. Currency risks and volatility in crude-based raw materials continue to squeeze working capital cycles, pushing formulators toward bio-based and high-solids systems that reduce solvent exposure.

Key Report Takeaways

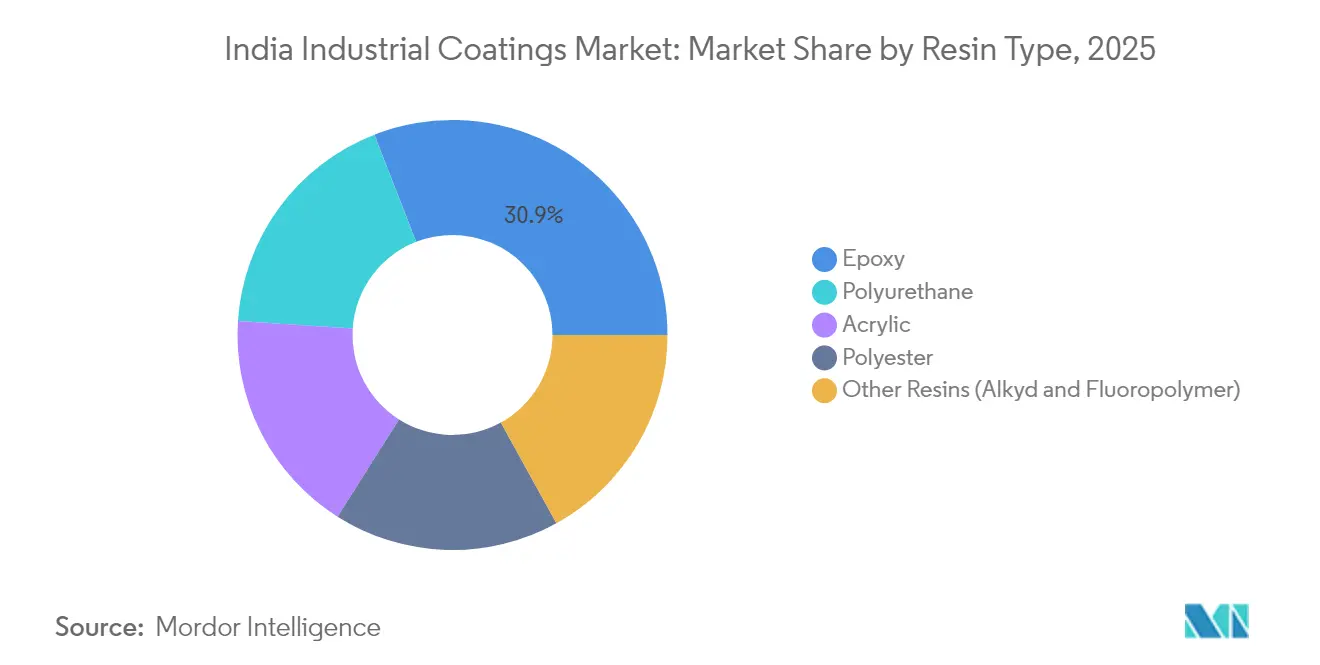

- By resin type, epoxy held 30.92% of the India Industrial Coatings market share in 2025. Polyurethane is forecast to post the fastest 6.01% CAGR through 2031.

- By technology, solvent-borne systems led with 37.68% revenue in 2025, while water-borne alternatives are expected to advance at a 6.22% CAGR through 2031.

- By end-user, the General Industrial segment captured 59.05% of the revenue in 2025 and is expected to increase at a CAGR of 5.72% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Industrial Coatings Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding manufacturing and infrastructure projects | +1.8% | Gujarat, Maharashtra, Tamil Nadu | Medium term (2-4 years) |

| Rising automotive production and refurbishment demand | +1.2% | Chennai, Pune, Gurugram | Short term (≤ 2 years) |

| Growing demand for corrosion-protection in oil and gas pipelines | +0.9% | Western & Eastern coastal belts | Long term (≥ 4 years) |

| Government push for high-performance coatings in strategic sectors | +0.7% | National | Medium term (2-4 years) |

| Renewable-energy installations requiring specialized coatings | +0.6% | Rajasthan, Gujarat, Karnataka | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Manufacturing and Infrastructure Projects

Large-scale petrochemical, mining, and transportation corridors are providing multi-year visibility into the India Industrial Coatings market, as EPC contractors specify higher build and longer-life systems for harsh on-site conditions. State-led chemical parks in Gujarat and Odisha simplify feedstock logistics, supporting plant-level just-in-time deliveries for epoxy primers and polyurethane finishes. Coaters that colocate service centers near these clusters lower freight costs and provide faster turnaround for in-process quality audits. Integrated steel plants, wind-tower yards, and port facilities require surface-tolerant coatings with rapid recoat windows, which shorten project schedules. The resulting shift from single-pack to two-pack systems is lifting average selling prices and strengthening margins for formulators that have backward-integrated resin assets.

Rising Automotive Production and Refurbishment Demand

India’s vehicle output rebound and sustained growth in the car parc are expanding paint-shop throughput and refinish activities, lifting consumption across pretreatment, primer-surfacer, basecoat, and clearcoat stages. Battery-electric vehicles require highly insulative and thermally conductive coatings on packs and power-electronics, nearly tripling coating grams per vehicle compared with internal-combustion equivalents. OEM tier-1 suppliers are migrating to powder for chassis and suspension arms, citing 98% transfer efficiency and zero solvent emissions. Refinish shops in Tier-2 cities are upgrading to low-VOC polyurethane clearcoats to comply with local pollution-control board checks, creating a ripple effect in demand for matched hardeners and thinners.

Growing Demand for Corrosion-Protection in Oil and Gas Pipelines

Three-layer polyethylene (3LPE) and fusion-bonded epoxy (FBE) are the dominant materials in new transmission lines, as operators target 25-year life cycles and lower maintenance costs. Refineries on the western coast have mandated 200-micron DFT FBE interiors for crude-feed lines, boosting orders for high-temperature epoxy powders. City gas-distribution grids now specify ISO 21809-compliant dual-layer systems, driving qualification activities at independent test labs in Mumbai and Surat. Offshore trunk lines require reinforced polypropylene topcoats for mechanical impact resistance, creating niche opportunities for suppliers with subsea track records[1]Hempel A/S, “Coating Solutions for Indian Oil and Gas Pipelines,” hempel.com.

Government Push for High-Performance Coatings in Strategic Sectors

Defense shipyards and aerospace OEMs are adopting polysiloxane hybrids and fluoropolymer topcoats that endure high-UV, seawater, and chemical exposure, spurring domestic formulators to license chemistries from global majors. The solar-photovoltaic production-linked-incentive scheme stipulates anti-soiling, high-transmission coatings on glass and the back sheet, thereby widening the addressable pool of specialty coatings. Public-sector procurement norms now award preference margin points to suppliers with more than 60% local value addition, prompting foreign players to blend and mill resins at Indian sites rather than import finished paints.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC and solvent-emission regulations | -1.10% | National, stricter enforcement in industrial clusters | Short term (≤ 2 years) |

| Volatility in crude-oil based raw-material prices | -0.80% | National, higher impact on solvent-borne coating manufacturers | Short term (≤ 2 years) |

| Lack of skilled industrial-coating applicators | -0.70% | National, acute shortage in tier-2 and tier-3 manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC and Solvent-Emission Regulations

Rule 123-M of the Model Factory Rules enforces closed-loop transfer of Class-I solvents, prompting capex on vapor recovery and explosion-proof motors[2]Directorate General Factory Advice Service and Labour Institutes, “Model Factory Rules Under The Factories Act, 1948,” dgfasli.gov.in. Plants lacking regenerative thermal oxidizers are limited by batch size and are shifting toward high-solids or water-reducible binders. Formulators must re-qualify systems with customers when replacing xylene or MEK, stretching R&D resources and lengthening commercialization timelines. Smaller job shops are outsourcing finishing to larger toll coaters, consolidating demand among players that can finance environmental upgrades. The regulation also caps shift-time exposure levels for painters, intensifying demand for faster-curing coatings that reduce booth occupancy.

Volatility in Crude-Oil Based Raw-Material Prices

Brent-linked epoxy and polyester resin prices have swung 22% in the last 18 months, complicating quarterly pricing negotiations with OEMs. Imported shipments of titanium dioxide and isocyanate face seasonal congestion charges at the Nhava Sheva port, adding unexpected cost layers. Formulators are establishing dual-vendor policies and hedging feedstock with longer call contracts, yet sudden spikes still erode contribution margins. The need to carry buffer inventory inflates working-capital needs, particularly for water-borne dispersions that have shorter shelf lives. The parallel development of alkyds from castor oil and epoxy diluents from cardanol is gaining momentum as a structural hedge against petrochemical volatility.

Segment Analysis

By Resin Type: Polyurethane Closing the Gap with Epoxy

The epoxy resin type had the largest share of 30.92% in the India Industrial Coatings Market in 2025, reflecting its entrenched status in infrastructure and marine protection. The market share of polyurethane resin types is growing at the fastest CAGR of 6.01% during the forecast period (2026-2031) due to OEM uptake in automotive trim, electric-vehicle battery packs, and wind-blade shells. Epoxy’s low permeation and strong adhesion continue to outperform in acidic or alkaline environments; however, two-component polyurethanes now deliver comparable salt-spray performance with superior flexibility. Non-isocyanate polyurethane (NIPU) is emerging as an eco-friendlier alternative, delivering 30-50% higher chemical resistance than traditional polyurethane without the hazards of free isocyanate.

Resin formulators with vertical integration into liquid epoxy monomer (LEM) and polyether polyol production capture better margins and supply reliability. The India Industrial Coatings market share of acrylics remains niche in heavy-duty services but dominates in applications such as appliances, HVAC, and façade panels, where color retention is paramount. Polyester dominates interior furniture powder lines, supported by rising demand for modular kitchens and office furniture. Suppliers are pilot-running bio-based epoxies from lignin and soybean-oil routes to cut carbon footprints while preserving mechanical performance.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Technology: Water-borne Momentum Challenges Solvent-borne Lead

Solvent-borne formulations still hold the largest India Industrial Coatings market share at 37.68% in 2025, favored for quick curing and wide-temperature application windows. Water-borne lines, however, are catching up fast, projecting a 6.22% CAGR thanks to newer self-crosslinking acrylic and hybrid polyurethane dispersions that equal solvent systems in salt-spray and gloss retention. Powder coatings hold near-total dominance in appliance side panels and wheel rims, driven by transfer efficiencies exceeding 95% and zero VOC emissions. UV-curable formulations, which were previously niche, are gaining traction in luxury vinyl tile topcoats and electronics due to their one-minute full cure and shrinking factory footprint.

OEMs are redesigning paint shops with multistage pre-treatment systems that are compatible with both e-coat and waterborne primers, enabling a phased transition from solvent to water. Paint-booth air-handling units now incorporate downdraft systems with water curtains, curbing fugitive solvent emissions. Architects promoting “green building” labels are influencing industrial landlords to specify low-VOC coatings on structural steel, thereby expanding the scope of water-borne products beyond traditional consumer segments. High-solids alkyds are gaining uptake where water is impractical, such as cold or humid maintenance sites.

By End-user Industry: General Industrial Remains the Workhorse

The General Industrial basket accounted for 59.05% of the market revenue in 2025, representing the largest share of the India Industrial Coatings market size. Moreover, the market share of this sector is expected to increase at a CAGR of 5.72% during the forecast period (2026-2031). It spans machinery, fabricated metals, white goods, and textile machinery—segments that benefit from the government’s focus on domestic capital-goods self-sufficiency. Anti-corrosion primers specified by engineering, procurement, and construction firms for transmission-line towers require 240-micron DFT zinc-rich epoxies, which increase volume and value. OEM compressor plants in Pune and Vadodara are adopting textured powder finishes that enhance scratch resistance and conceal weld marks, thereby improving the first-pass yield.

Protective coatings for oil-and-gas, power generation, and marine sectors form the highest-margin niche within the basket. Upstream equipment refurbishment yards in Visakhapatnam demand quick-return polyurea topcoats, trimming dry-dock stays by 30%. Wind-tower fabricators in Gujarat prefer three-coat polyurethane-epoxy-polyurethane systems to meet the IEC 61400 exposure class, consuming approximately 120 kg of paint per tower. Mining conveyor manufacturers in Odisha are transitioning from solvent-borne alkyds to high-solids epoxies, following end-users' reports of downtime caused by premature chalking in acidic overburden environments.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Gujarat anchors the India Industrial Coatings market with its dense petrochemical complexes, downstream engineering parks, and two deep-water ports that streamline the import of titanium dioxide, solvents, and specialty additives. Coating majors cluster production here to exploit access to feedstock and dedicated hazardous-waste infrastructure, resulting in shorter lead times for western and northern customers. Maharashtra follows, driven by Pune’s automotive cluster and Mumbai’s offshore energy fabrication yards, which specify ISO 12944 C5-M systems. Tamil Nadu’s Chennai-Hosur corridor is home to a diverse range of industries, including automotive OEMs, leather goods, and wind-blade factories, generating a multi-chemistry demand, from water-borne basecoats to gel-coat resins.

Eastern growth pockets in West Bengal and Odisha are driven by new steel flats and mining expansions, which in turn increase calls for high-build epoxy novolacs to handle high-temperature slurry. Northern states, such as Haryana and Punjab, contribute through agricultural equipment plants that require mid-performance alkyd and polyester powders to balance cost and durability under rural service conditions. Karnataka, Rajasthan, and Gujarat solar corridors are emerging as hotspots for anti-soiling and high-transmission coatings on mounting structures and glass. Diverse climatic extremes—from high-salinity coasts to arid deserts—necessitate region-specific testing, compelling formulators to maintain multiple grade SKUs to meet geographic performance codes.

Concentration of regulatory enforcement differs by region: Maharashtra Pollution Control Board conducts quarterly solvent-recovery audits, whereas Tamil Nadu’s inspectorate focuses on wastewater-COD compliance from pre-treatment lines. Such regional nuances influence technology uptake rates, with higher water-borne penetration in the west and south where infrastructure for deionized water recycling is better. Transportation projects like the Delhi-Mumbai Industrial Corridor create linear demand corridors for bridge-deck and girder coatings, enabling batching efficiencies and just-in-time deliveries.

Competitive Landscape

The India Industrial Coatings market features moderate concentration. Sustainability credentials are becoming a decisive factor in tender evaluations; ISO 14001 accreditation helped Berger win several metro-rail maintenance contracts. Global majors hold extensive patent portfolios for phenolic and epoxy compounds, yet local firms are closing the gap by licensing technology and investing in pilot reactors for high-solids alkyd and hybrid polyurethane dispersions. Consolidation could accelerate as mid-tier firms seek to scale up to fund environmental retrofits and expand their application labs.

India Industrial Coatings Industry Leaders

Asian Paints PPG Pvt. Ltd.

AkzoNobel India Ltd.

Berger Paints India Ltd.

Kansai Nerolac Paints Limited

Jotun

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: Stahl, the global player in specialty coatings, including industrial coatings for flexible materials, announced the reopening of its advanced coatings facility in Ranipet, India. The reopening reinforces Stahl’s commitment to innovation, sustainability, and customer collaboration through the production of locally sourced, high-performance specialty coatings.

- August 2025: PPG Industries, Inc. and Asian Paints Ltd. have renewed their joint venture agreement in India for an additional 15 years. This renewal enables the two companies to keep catering to India's diverse clientele, spanning industrial, protective, marine, packaging, automotive, and powder coatings sectors. Set to commence in 2026, the extension will be valid until 2041.

India Industrial Coatings Market Report Scope

Industrial coatings are polymer substances that are primarily used to meet industrial design requirements such as non-stick performance, noncorrosive, and chemical protection to the applied surface. India's industrial coatings market is segmented by resin type, technology, and end-user industry. By resin type, the market is segmented into epoxy, acrylic, polyurethane, polyester, and other resin types. By technology, the market is segmented into water-borne coatings, solvent-borne coatings, and other technology types. By end-user industry, the market is segmented into automotive, oil and gas, electrical and electronics, aircraft, decorative, marine, and other end-user industries. For each segment, the market sizing and forecasts have been done based on revenue (USD million).

By Resin Type

| Epoxy |

| Polyurethane |

| Acrylic |

| Polyester |

| Other Resins (Alkyd, Fluoropolymer) |

By Technology

| Water-borne |

| Solvent-borne |

| Powder Coatings |

| Other Technologies (UV-/EB-Cured and High Solids) |

By End-user Industry

| General Industrial | |

| Protective Coatings | Oil and Gas |

| Power Generation | |

| Infrastructure | |

| Mining | |

| Other Protective Coatings |

| By Resin Type | Epoxy | |

| Polyurethane | ||

| Acrylic | ||

| Polyester | ||

| Other Resins (Alkyd, Fluoropolymer) | ||

| By Technology | Water-borne | |

| Solvent-borne | ||

| Powder Coatings | ||

| Other Technologies (UV-/EB-Cured and High Solids) | ||

| By End-user Industry | General Industrial | |

| Protective Coatings | Oil and Gas | |

| Power Generation | ||

| Infrastructure | ||

| Mining | ||

| Other Protective Coatings | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the India Industrial Coatings market?

It is valued at USD 3.09 billion in 2026 and is forecast to reach USD 4.05 billion by 2031.

Which resin type leads demand?

Epoxy accounts for 30.92% share, driven by infrastructure and marine applications.

How fast are water-borne technologies growing?

Water-borne coatings are advancing at a 6.22% CAGR through 2031 due to stricter VOC rules.

Which end-user contributes most to revenue?

The General Industrial segment contributes 59.05% of 2025 revenue across machinery and fabricated-metal applications.

What factors restrain growth?

Stringent VOC regulations and crude-linked raw-material price swings reduce margins and slow capacity expansion.