Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

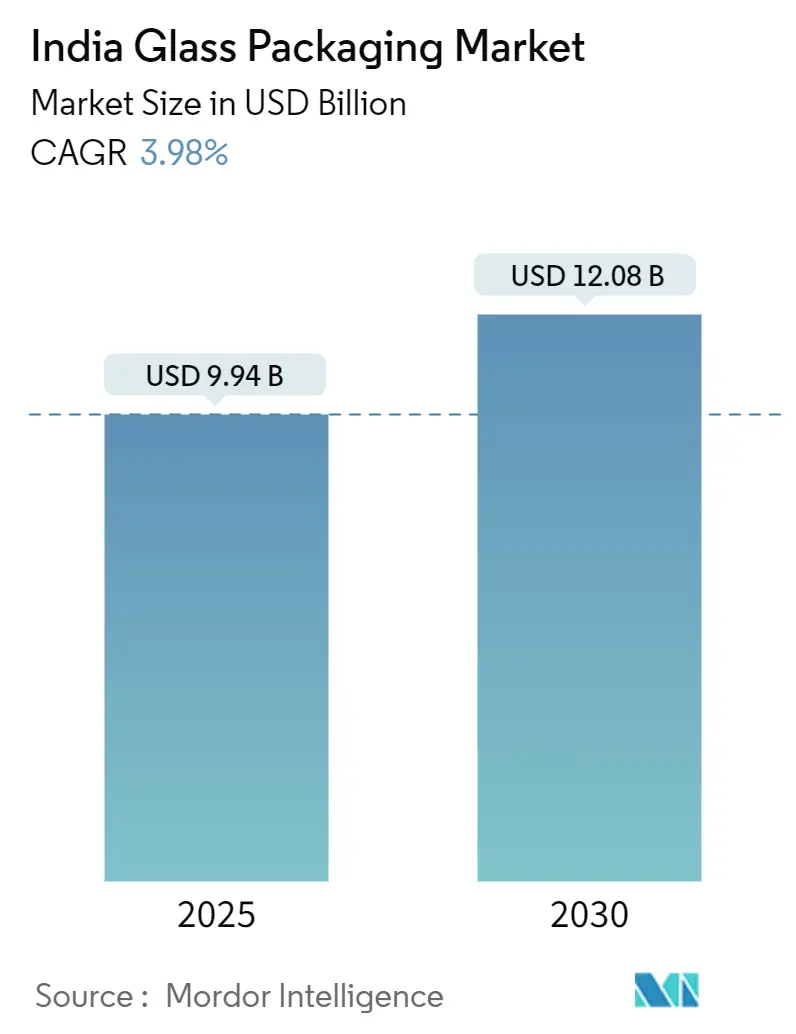

| Market Size (2025) | USD 9.94 Billion |

| Market Size (2030) | USD 12.08 Billion |

| Growth Rate (2025 - 2030) | 3.98% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Glass Packaging Market Analysis by Mordor Intelligence

The India glass packaging market size stood at USD 9.94 billion in 2025 and is forecast to reach USD 12.08 billion by 2030, expanding at a 3.98% CAGR over 2025-2030 . Mature demand from mainstream beverages anchors current volumes, while momentum shifts toward pharmaceutical vials, premium craft spirits, and sustainability-driven substitution from plastic underpin fresh growth pockets. Central and state bans on single-use plastics, coupled with traceability mandates effective July 2025, accelerate the adoption of returnable or recycled glass formats. Production-Linked Incentive (PLI) investments worth INR 1.61 lakh crore across 14 sectors upgrade domestic furnace, cullet, and logistics networks, trimming input costs and raising output reliability. [1]Press Information Bureau, “Compulsory ban on polythene bags,” pib.gov.in Pharmaceutical export ambitions, crystallized by the US Biosecure Act and 27 new greenfield bulk-drug projects, pivot demand toward Type I borosilicate vials that command higher margins. Meanwhile, craft distilleries and microbreweries increasingly specify bespoke flint bottles that elevate visual branding and justify premium shelf prices.

Key Report Takeaways

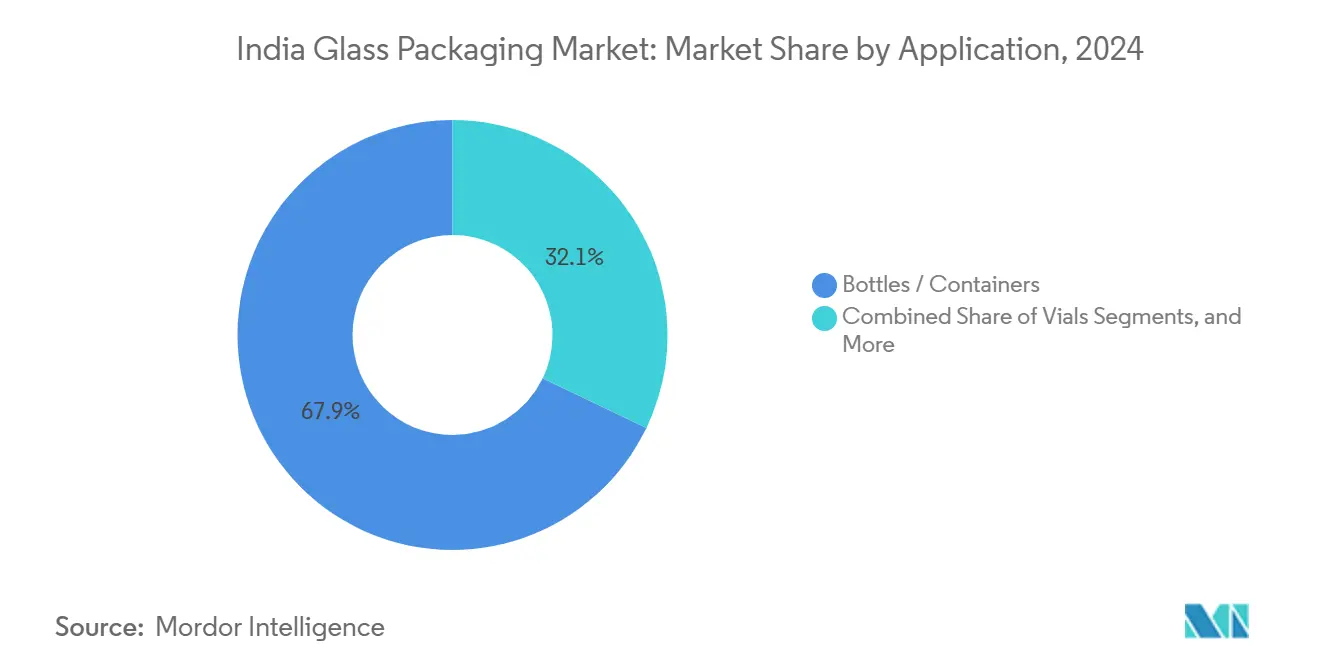

- By product, Bottles/Containers led with 67.89% of the India glass packaging market share in 2024, while Vials recorded the fastest 4.37% CAGR between 2025-2030.

- By glass type, Type III soda-lime accounted for 58.35% market share, whereas Type I borosilicate is forecast to grow at a 4.28% CAGR between 2025-2030.

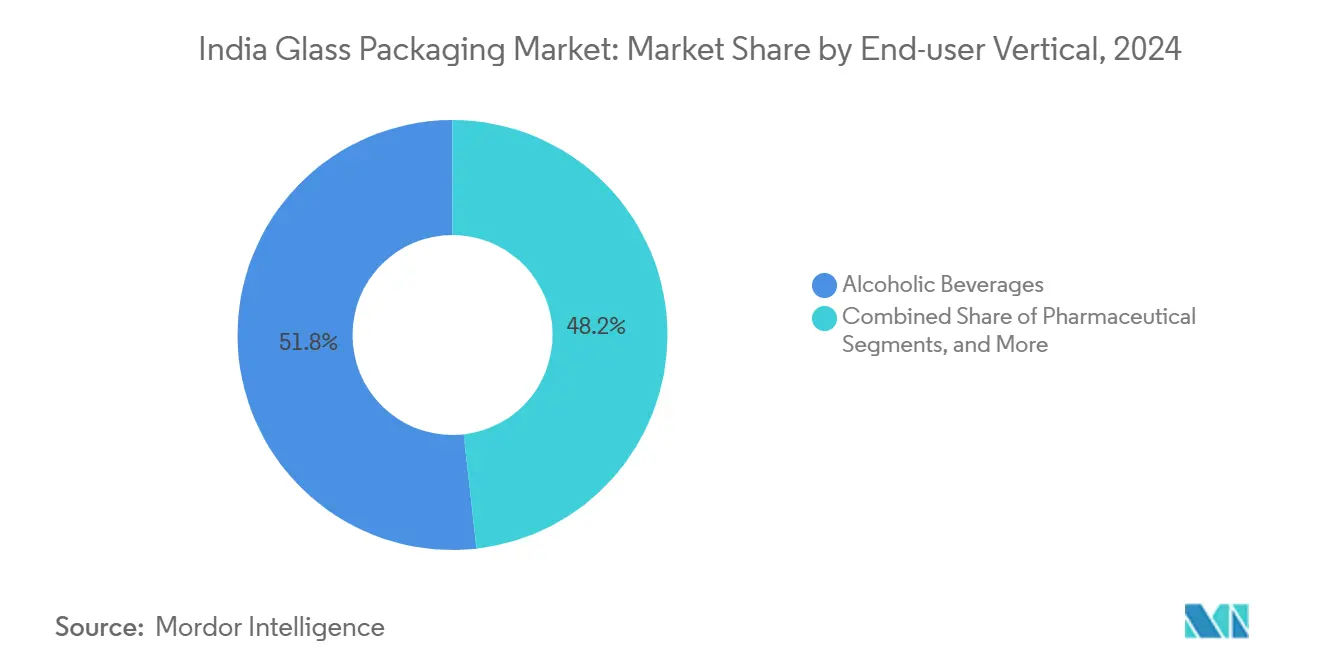

- By end-user vertical, Alcoholic Beverages held 51.78% market share in 2024; Pharmaceutical applications are advancing at a 4.43% CAGR between 2025-2030.

- By capacity range, 100-500 ml formats captured 37.43% market share, yet <30 ml containers are set to expand at a 4.16% CAGR between 2025-2030.

- By geography, North India contributed a 30.92% market share in 2024, while South India is projected to post the quickest 3.12% CAGR between 2025-2030.

India Glass Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Craft spirits and RTDs lift premium flint-bottle demand | +0.8% | Mumbai, Bangalore, Delhi; national spread | Medium term (2-4 years) |

| Vaccine exports and biologics capacity drive Type I vial uptake | +0.9% | South India core; West India spill-over | Long term (≥ 4 years) |

| D2C beauty brands shift to glass jars for sustainability | +0.5% | Metro and Tier-1 cities | Short term (≤ 2 years) |

| Micro-breweries and craft distilleries want bespoke formats | +0.6% | Maharashtra, Karnataka, Goa, Haryana | Medium term (2-4 years) |

| State single-use-plastic bans boost returnable glass | +0.7% | Progressive states nationwide | Short term (≤ 2 years) |

| PLI-backed cullet plants cut costs, spur recycled glass demand | +0.4% | Maharashtra, Telangana, Gujarat | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Craft Spirits Revolution Drives Premium Glass Demand

Consumer migration from standard beer to craft spirits and ready-to-drink cocktails widens opportunities for bespoke bottles in the India glass packaging market. Exports of alcoholic beverages rose to USD 375.09 million in FY 2024, signaling premiumization that spills into domestic shelves.[2]Agricultural and Processed Food Products Export Development Authority, “Alcoholic and Non-Alcoholic Beverages,” apeda.gov.in Micro-breweries in Maharashtra and Karnataka commission proprietary molds in flint and amber variants that bolster brand storytelling. Streamlined state licensing and tourism-centric policies sustain this trajectory, although compliance with Bureau of Indian Standards food-grade norms remains compulsory. Glass makers able to deliver small-batch run flexibility and intricate embossing gain a pricing edge over mass-production peers. The result is a diversified revenue stream less exposed to volume swings in mainstream beer.

Pharmaceutical Export Ambitions Fuel Type I Vial Growth

The India glass packaging market benefits directly from the US Biosecure Act, which channels contract manufacturing away from Chinese suppliers toward Indian CDMOs. SGD Pharma’s joint venture with Corning in Telangana establishes Velocity Vials capacity aligned with global biologic fill-finish standards. Borosilicate compositions withstand thermal shock and chemical reactivity posed by complex drugs, justifying premium selling prices. India’s CDMO revenue is projected to climb from USD 15.63 billion in 2023 to USD 26.73 billion by 2028, ensuring sturdy downstream demand. Government PLI incentives covering 27 bulk-drug parks lower capex hurdles, while dedicated pharma freight corridors shorten export lead times. Collectively, these factors lock in a robust demand pipeline for high-purity vials.

Sustainability Mandates Accelerate Glass Substitution

Plastic Waste Management Amendment Rules, effective July 2025, demand QR-code traceability that inflates compliance costs for multilayer plastic, thereby nudging brands toward infinitely recyclable glass. D2C beauty labels in metro cities embrace glass jars to signal eco-consciousness, with PGP Glass already incorporating 33% cullet and targeting 80% renewable energy by 2030. State-level bans on single-use plastics add further impetus. Although reverse-logistics gaps persist outside metros, policy-backed recycling networks and consumer take-back programs steadily expand. Brands gain reputational capital and shelf differentiation, reinforcing the virtuous cycle for the India glass packaging market.

PLI-Backed Cullet Processing Reduces Cost Base

PLI allocations worth INR 1.61 lakh crore unlock funding for new cullet-processing units in Maharashtra and Telangana, trimming raw-material costs and cutting furnace energy consumption. Container glass recycling rates hover near 32% globally, leaving ample upside for India to narrow the gap. Advanced optical sorters and color-separation systems enhance cullet purity, allowing higher feed ratios without compromising clarity. Over the long term, greater cullet use positions domestic producers to meet multinational buyers’ recycled-content targets, reinforcing export competitiveness.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PET bottles outcompete glass in edible oil and soft drinks | -0.9% | National price-sensitive segments | Short term (≤ 2 years) |

| Volatile LNG and power prices compress container margins | -0.6% | Major manufacturing hubs | Medium term (2-4 years) |

| Weak reverse-logistics for returnable glass | -0.4% | Rural and semi-urban markets | Long term (≥ 4 years) |

| Lenders cautious on long-payback furnace rebuilds | -0.3% | Nationwide expansion plans | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

PET Competition Intensifies in Price-Sensitive Segments

Government mandates for 30% recycled PET content in beverage bottles by April 2025, climbing to 60% by FY 2029, spur rapid scale-up of rPET capacity that sustains PET’s cost advantage. Ganesha Ecopet alone plans to recycle 42,000 tonnes annually by 2026, capturing roughly one-quarter of national bottle waste. Beverage giants deploy lightweight PET and crystallizable hot-fill grades to replace glass in edible oils and carbonated drinks, where freight and breakage costs weigh heavily. Unless glass makers unlock cost-effective returnable models, PET will continue capturing incremental share in mass-market beverages.

Energy Cost Volatility Pressures Manufacturing Economics

Continuous-furnace glass production relies on natural gas and electricity, exposing margins to fuel swings. Industrial gas demand is set to triple by 2050, ensuring structurally elevated prices.[3]U.S. Energy Information Administration, “Industry to drive tripling of natural gas consumption in India by 2050,” eia.gov While India targets 500 GW of renewables by 2030, intermittent supply and grid charges inject uncertainty over the transition window. Furnace rebuilds costing USD 40-60 million require 15-20 year paybacks, making lenders cautious. Smaller players may delay upgrades, risking capacity constraints or quality lapses that could erode the competitiveness of the India glass packaging market.

Segment Analysis

By Product: Vials Outpace Legacy Containers

Bottles and jars retained the largest 2024 share at 67.89% of the India glass packaging market size, anchored by mainstream food and beverage usage. However, vials are advancing at a 4.37% CAGR as pharmaceutical exports pivot toward biologics that require Type I borosilicate formats. The India glass packaging market share held by vials could therefore climb meaningfully by 2030 as CDMOs scale capacity. Ampoules and syringes deliver steady baseline demand, yet premium vial specifications capture value-added margins for specialized converters.

The shift compels container glass majors to diversify into smaller formats or risk over-concentration in legacy beverage lines. Early movers are installing modular forming machines capable of rapid changeovers from 500 ml bottles to 10 ml vials, reducing downtime and broadening customer reach. Pharmaceutical compliance audits drive investments in on-line camera inspection and ISO 15378 cleanroom environments, lifting barriers to entry for new firms but consolidating revenues for integrated players.

Note: Segment shares of all individual segments available upon report purchase

By Glass Type: Borosilicate Extends Premium Edge

Type III soda-lime constituted 58.35% of 2024 revenue thanks to its cost-effectiveness in edible oils and sauces. Yet Type I borosilicate is on a 4.28% CAGR trajectory, propelled by stringent pharmacopeia norms and export-oriented biologics demand. The India glass packaging market size for borosilicate vials is forecast to expand steadily as Telangana and Gujarat commission new melting tanks with low-alkali formulations.

Soda-lime volumes remain essential for scale economics, but margin uplift increasingly hinges on borosilicate. Producers integrating oxy-fuel burners and batch pre-heaters curb energy intensity, narrowing cost gaps. Treated soda-lime (Type II) and UV-shielding amber variants continue to serve vaccines and craft beverages, respectively, underpinning a diversified product stack that insulates revenue streams.

By End-User Vertical: Pharma Inches Closer to Beverage Dominance

Alcoholic beverages represented 51.78% of 2024 demand, anchored in spirits, beer, and wine. Yet pharmaceutical demand is forecast to post a faster 4.43% CAGR, reflecting CDMO expansion and regulatory diversification away from China. Food and soft-drink uses face PET encroachment, prompting glass producers to reposition toward premium sauces, condiments, and craft sodas where glass conveys purity cues.

Personal care and cosmetics emerge as niche engines as D2C brands tout glass’ sustainability credentials. Diageo India’s pledge to cut packaging weight by 10% by 2030 will gradually temper spirits volume growth, but create parallel opportunities in lightweighting technology.

Note: Segment shares of all individual segments available upon report purchase

By Capacity Range: Small Formats Command Premiums

Containers sized 100-500 ml captured 37.43% of 2024 shipments, yet <30 ml units are on course for 4.16% CAGR as pharma and high-proof miniatures proliferate. Integrating narrow-neck press-and-blow lines enables efficient runs of sub-30 ml vials while maintaining wall-thickness precision. The India glass packaging market size for mini formats is poised for durable gains as health-care sampling, travel retail and craft spirits adopt smaller SKUs for operational flexibility.

Larger 500-1,000 ml formats lose ground to PET in mass beverages, driving glass players to pursue lightweight redesign and higher recycled-content ratios. Those unable to optimize logistics may cede share, underscoring the importance of SKU rationalization strategies across capacity brackets.

Geography Analysis

Northern states commanded a 30.92% share in 2024, underpinned by dense consumption across Delhi NCR and Punjab’s agri-processing clusters. Proximity to Rajasthan silica mines keeps raw-glass costs competitive, while six-lane highway grids ensure quick dispatch to bottlers. Regional container plants leverage integrated cullet yards and multi-feeder furnaces that align with high-volume beverage contracts.

Western India combines Maharashtra’s wine corridor with 46 registered wineries and Gujarat’s chemical belt supporting pharma and food ingredients. Although precise India glass packaging market share numbers remain undisclosed at the firm level, steady spirits and wine bottling sustain baseline throughput. Contract glass decorators around Nashik add value via hot stamping and screen printing, feeding premiumization in alcoholic beverages.

South India posts the steepest 3.12% CAGR thanks to Hyderabad’s pharma corridor and Bangalore’s craft-beer boom. SGD Pharma-Corning’s Velocity Vials plant in Telangana exemplifies investments primed for export accreditation. Government fast-tracks environmental clearances and offers power subsidies to lure glass furnaces into industrial estates. Eastern states lag due to limited pharma output and weaker reverse-logistics infrastructure, but F&B players in Kolkata sustain modest soda-lime demand.

Competitive Landscape

The India glass packaging market gravitates toward an oligopoly in mainstream containers but fragments in specialty segments. Hindustan National Glass’s insolvency proceeding, now leaning toward an INSCO-led revival, may release stranded capacity or trigger asset sales that redistribute volume shares. PGP Glass differentiates through 33% cullet usage and an EcoVadis Platinum score, positioning itself as a sustainability reference customer for global beauty and spirits brands.

Gerresheimer leverages proprietary RTF (Ready-to-Fill) vial technology, reporting 2.6% organic growth in Q3 2024 despite destocking. Borosil Glass Works commits INR 250 crore toward Gujarat and Jaipur upgrades to double revenue in four years. Smaller craft-focused converters explore partnerships with tubes and closure suppliers, offering turnkey solutions that speed time-to-market for new beverage SKUs. Reverse-logistics start-ups test refill-and-return models in Bengaluru and Delhi, hinting at emerging service niches.

India Glass Packaging Industry Leaders

-

AGI Greenpac Limited

-

Gerresheimer AG

-

Hindustan National Glass and Industries Limited

-

Piramal Glass Private Limited

-

Haldyn Glass Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Ministry of Environment enforced Plastic Waste Management Amendment Rules mandating QR-code traceability on all primary packaging, advancing recyclability protocols that favor glass.

- March 2025: DPIIT announced cumulative manufacturing output of INR 14 lakh crore and exports of INR 5.3 lakh crore under PLI, creating 1.15 million jobs and wider supply-chain knock-on effects.

- January 2025: Supreme Court voided AGI Greenpac’s resolution bid for Hindustan National Glass, paving the way for INSCO’s plan.

- December 2024: Borosil Group mapped a USD 30 million capex to lift capacity in Gujarat and Rajasthan, targeting revenue of INR 7,000 crore by 2028.

India Glass Packaging Market Report Scope

Glass is one of the most preferred packaging materials for consumers concerned about their health and the environment. It is made from all-natural, sustainable raw materials. Glass packaging preserves the product's taste or flavor and maintains the integrity or healthiness of food and beverages.

The study tracks the market for glass packaging in India based on the analysis of products and end-user industries. It provides a detailed assessment of the glass packaging market based on the underlying factors related to the demand for glass packaging products. The India Glass Packaging Market is segmented by type (bottles/containers, vials, ampoules, syringe/cartridges) and end-user vertical (food, beverage ((soft drinks, milk, alcoholic beverages, and other beverage types)), cosmetics, perfumery, and personal care, and pharmaceuticals).

The market sizes and forecasts are in terms of value (USD million) for all the above segments.

By Product

| Bottles / Containers |

| Vials |

| Ampoules |

| Syringes / Cartridges |

By Glass Type

| Type I (Borosilicate) |

| Type II (Treated Soda-lime) |

| Type III (Soda-lime) |

By End-user Vertical

| Food |

| Soft-drink Beverages |

| Alcoholic Beverages |

| Cosmetics and Personal Care |

| Pharmaceutical |

By Capacity Range

| <30 ml |

| 30 - 100 ml |

| 100 - 500 ml |

| 500 - 1 000 ml |

By Region

| North India |

| West India |

| South India |

| East India |

| By Product | Bottles / Containers |

| Vials | |

| Ampoules | |

| Syringes / Cartridges | |

| By Glass Type | Type I (Borosilicate) |

| Type II (Treated Soda-lime) | |

| Type III (Soda-lime) | |

| By End-user Vertical | Food |

| Soft-drink Beverages | |

| Alcoholic Beverages | |

| Cosmetics and Personal Care | |

| Pharmaceutical | |

| By Capacity Range | <30 ml |

| 30 - 100 ml | |

| 100 - 500 ml | |

| 500 - 1 000 ml | |

| By Region | North India |

| West India | |

| South India | |

| East India |

Key Questions Answered in the Report

What is the 2025 value of the India glass packaging market?

The India glass packaging market size reached USD 9.94 billion in 2025.

How fast will pharmaceutical vials grow within Indian demand?

Vials are projected to register a 4.37% CAGR through 2030, the quickest among product categories.

Which region offers the fastest growth opportunity?

South India leads with a forecast 3.12% CAGR, powered by pharma clusters in Telangana and Karnataka.

How are plastic bans influencing glass demand?

Single-use plastic bans and QR-code traceability rules are steering FMCG and beauty brands toward recyclable glass containers.

Why are energy costs a concern for Indian glass makers?

Continuous furnaces rely on natural gas; projected tripling of industrial gas demand by 2050 raises long-term fuel cost risks.

Who are key players shaping market sustainability trends?

PGP Glass, Gerresheimer and Borosil are advancing cullet usage, renewable energy and lightweight designs to align with ESG goals.

Page last updated on: