Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

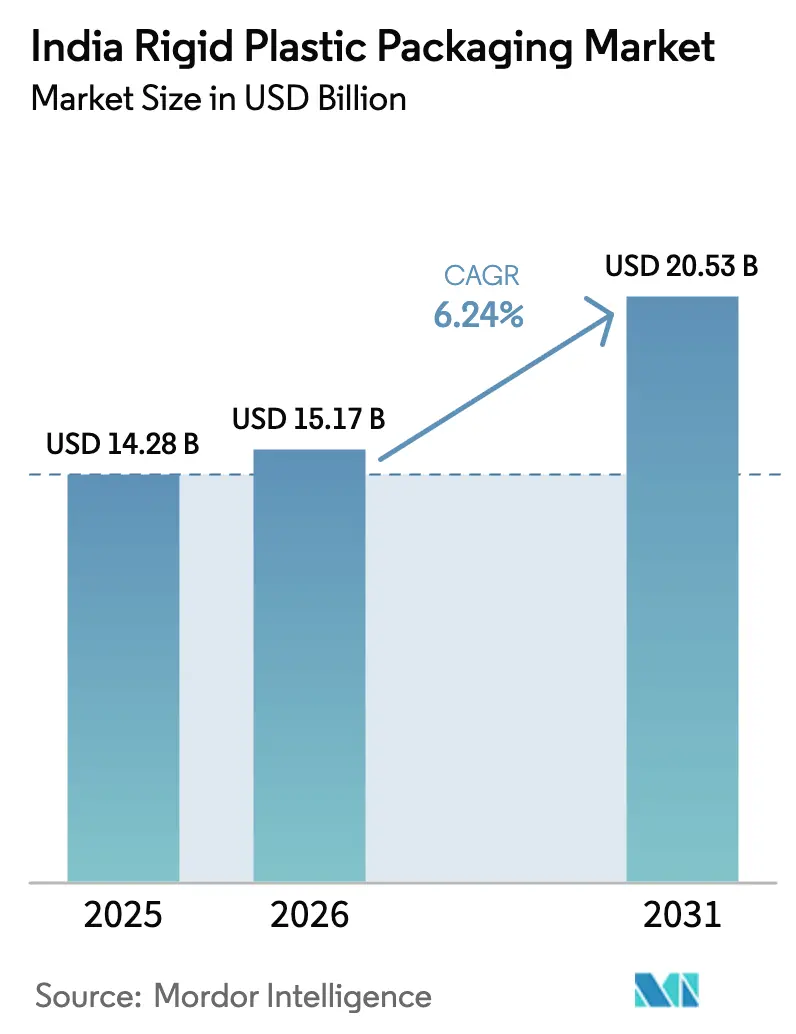

| Base Year Market Size (2025) | USD 14.28 Billion |

| Market Size (2026) | USD 15.17 Billion |

| Market Size (2031) | USD 20.53 Billion |

| Growth Rate (2026 - 2031) | 6.24% CAGR |

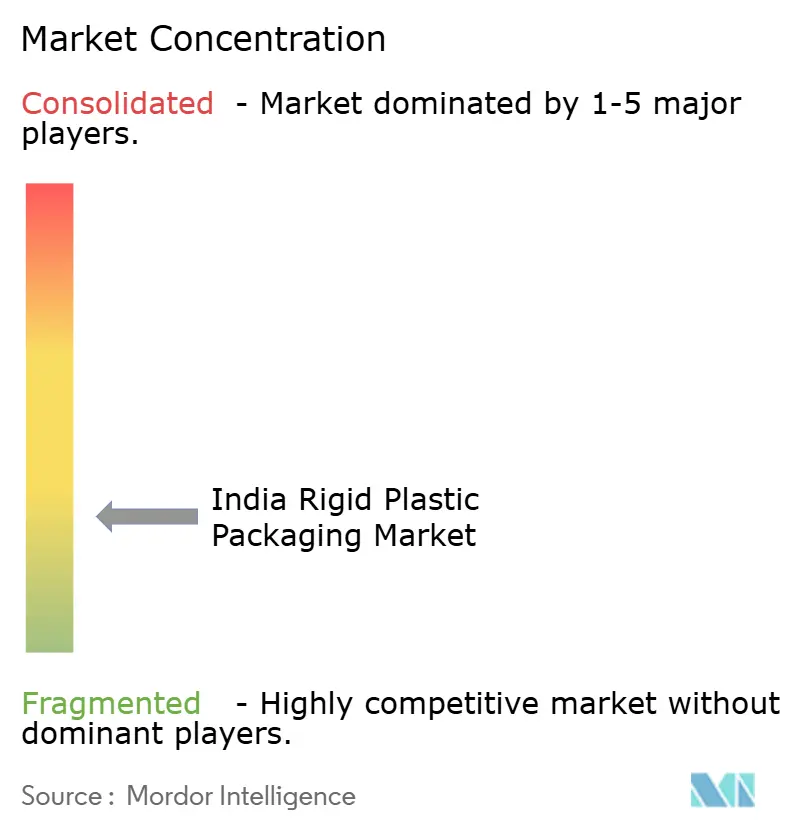

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Rigid Plastic Packaging Market Analysis by Mordor Intelligence

The India rigid plastic packaging market size is expected to grow from USD 14.28 billion in 2025 to USD 15.17 billion in 2026 and is forecast to reach USD 20.53 billion by 2031 at 6.24% CAGR over 2026-2031. Robust dairy output, rapid cold-chain roll-out, and policy-induced demand for ethanol fuel containers underpin steady volume gains. Brand owners are shifting toward packaging that meets recycled-content thresholds, while converters invest in advanced extrusion and injection lines to control unit costs. Tight margins caused by polypropylene price swings are accelerating resin substitution toward rPET where collection infrastructure permits. Strategic acquisitions signal rising consolidation as financial sponsors target scale and specialty capabilities inside the India rigid plastic packaging market.

Key Report Takeaways

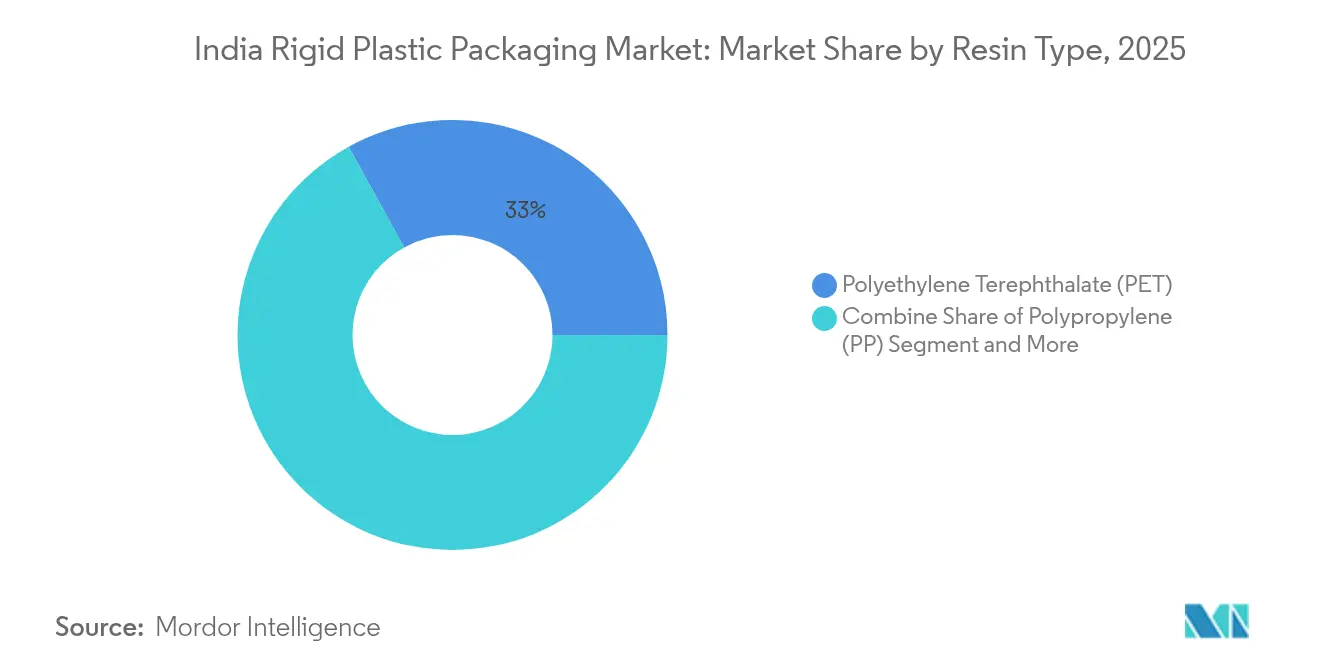

- By resin type, Polyethylene Terephthalate led with 33.02% of the India rigid plastic packaging market share in 2025, whereas Polypropylene is projected to post the fastest 7.42% CAGR through 2031.

- By product type, Bottles & Jars accounted for 35.31% revenue share in 2025; Trays & Containers are expected to expand at a 6.71% CAGR between 2026-2031.

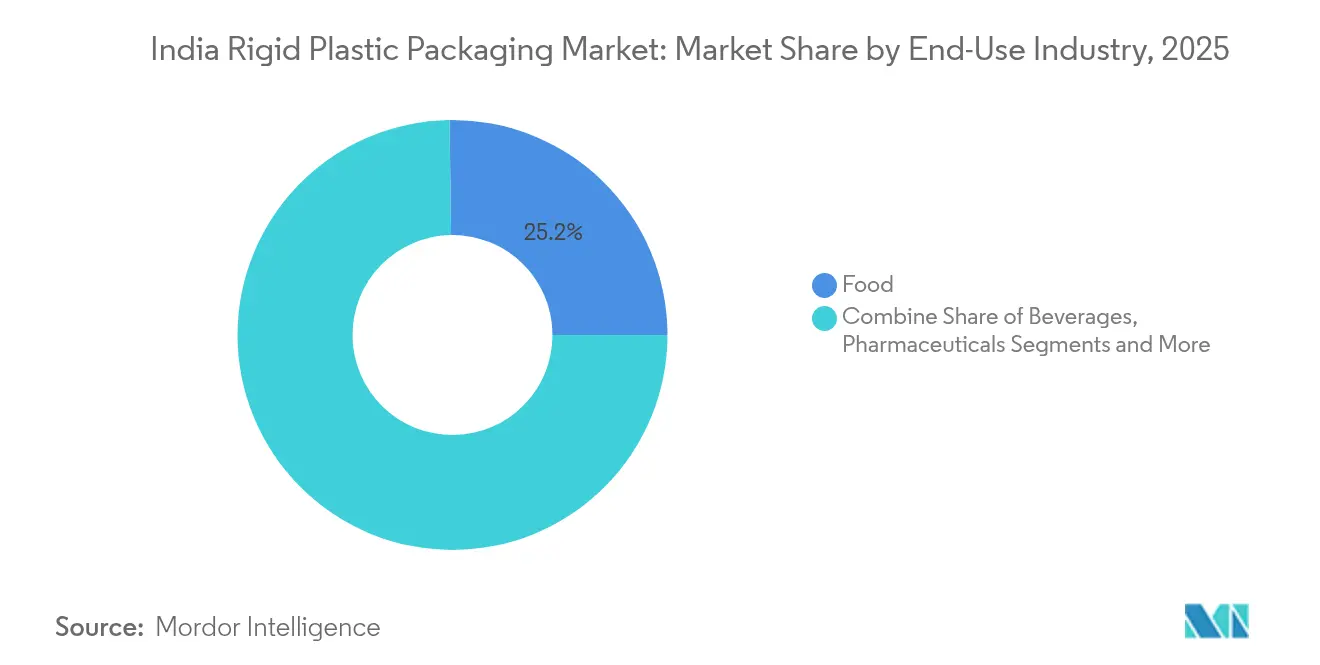

- By end-use industry, the Food segment retained 25.22% share of the India rigid plastic packaging market size in 2025, while Pharmaceuticals are forecast to grow fastest at 8.12% CAGR.

- By production process, Extrusion dominated with 68.34% share in 2025; Injection Molding shows the highest projected CAGR of 5.65% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Rigid Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive Growth of Packaged Dairy in Tier-II and Semi-Urban India | +1.2% | Tier-II cities, semi-urban regions with focus on Uttar Pradesh, Rajasthan, Madhya Pradesh | Medium term (2-4 years) |

| Government Push for Ethanol-Blended Fuel Boosting HDPE Jerrycan Demand | +0.8% | National, with concentration in fuel distribution networks | Short term (≤ 2 years) |

| Rising Adoption of PCR-Content Mandates by Top FMCG Brands Accelerating rPET Bottle Penetration | +1.5% | National, with early adoption in metropolitan markets | Medium term (2-4 years) |

| Surge in Organized Food-service Chains Driving Clamshell and Tray Volumes | +0.9% | Urban centers, expanding to Tier-II cities | Short term (≤ 2 years) |

| Cold-Chain Expansion Enabling PET Preform Demand for Beverage and Pharma Vials | +1.1% | National, with infrastructure concentration in industrial corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth of Packaged Dairy in Tier-II and Semi-Urban India

Fluid milk consumption is set to touch 91 million tonnes in 2025, a 2.2% rise from 2024, converting into consistent bottle and jar demand inside the India rigid plastic packaging market. Packaged fresh milk alone pursues a USD 20 billion opportunity by 2026 as semi-urban consumers shift from loose to branded supply. The INR 15,000 crore Animal Husbandry Infrastructure Fund is financing processing units that specify multilayer HDPE bottles for improved shelf life. Direct-to-consumer brands such as Country Delight, backed by USD 20 million of fresh capital in 2025, adopt tamper-evident PET designs to guarantee delivery within 36 hours. Together these forces embed long-run volume visibility for converters operating in the India rigid plastic packaging market.

Government Push for Ethanol-Blended Fuel Boosting HDPE Jerrycan Demand

India averaged an 11.5% ethanol blend in 2024 and eyes 20% by 2025, triggering downstream demand for chemically resistant HDPE storage drums. [1]Ministry of Petroleum & Natural Gas, “India's Ethanol Push: A Path to Energy Security,” pib.gov.in Production capacity reached 6.35 billion liters in 2024 and continues to climb under the modified Pradhan Mantri JI-VAN Yojana. [2]U.S. Department of Agriculture, “Biofuels Annual: India,” apps.fas.usda.gov As new distilleries open away from cane belts, distributed jerrycan demand follows, widening geographic spread within the India rigid plastic packaging market. Premium grade HDPE that withstands ethanol corrosion commands higher margins, rewarding processors with compounding expertise.

Rising Adoption of PCR-Content Mandates by Top FMCG Brands Accelerating rPET Bottle Penetration

A 30% minimum recycled-content rule effective April 2025 forces beverage and personal-care brands toward bottle-to-bottle loops. Only 5 of 18 food-grade rPET units have FSSAI licences, constraining supply and inflating bottling costs by 30%. Capacity additions by Ganesha Ecopet and an Indorama Ventures JV add 142 kilotons by 2026, narrowing the gap. As infrastructure scales, rPET becomes a branding tool rather than a compliance cost inside the India rigid plastic packaging market.

Cold-Chain Expansion Enabling PET Preform Demand for Beverage and Pharma Vials

Cold-chain investment is targeted to hit Rs 5 lakh crore by 2032 under the PM Gati Shakti plan. Improved temperature logistics favor PET preforms for dairy, juice and injectables requiring tight oxygen and moisture barriers. Converters that can certify vial grades for export win share in the India rigid plastic packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Draft BIS Standards Limiting Phthalate Levels Raising Compliance Costs | -0.7% | National, with higher impact on food-contact applications | Short term (≤ 2 years) |

| State-Level Single-Use Plastic Bans Shifting Volume to Paper Cartons | -0.9% | State-specific, with varying enforcement levels | Medium term (2-4 years) |

| Volatile Propylene Prices Squeezing PP Margins for SME Converters | -0.6% | National, with higher impact on cost-sensitive segments | Short term (≤ 2 years) |

| E-commerce Preference for Flexible Mailers Reducing Small-Parcel Rigid Use | -0.4% | Urban centers with high e-commerce penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Draft BIS Standards Limiting Phthalate Levels Raising Compliance Costs

Revised BIS norms for LDPE, LLDPE and HDPE effective January 2024 impose certification hurdles that smaller converters struggle to finance. Parallel Food Safety Authority rules demand migration testing for recycled PET, adding laboratory overheads. The expense tilts bargaining power toward larger players inside the India rigid plastic packaging market that operate accredited labs and can amortize compliance over scale.

State-Level Single-Use Plastic Bans Shifting Volume to Paper Cartons

Nineteen categories of single-use plastics were banned nationally in July 2022, yet enforcement varies widely by state. Some jurisdictions extend restrictions to trays and cutlery, nudging retailers toward coated paperboard. The Central Pollution Control Board’s monitoring reveals patchy compliance, creating uncertainty for suppliers. Inconsistent rules complicate inventory planning across the India rigid plastic packaging market and limit long-horizon capital spending on affected SKUs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: PET Leadership With Accelerating PP Gains

The segment generated the largest slice of the India rigid plastic packaging market size, as PET secured 33.02% share in 2025 on the strength of beverage and pharma demand. PP, while smaller, is projected to clock a 7.42% CAGR to 2031 supported by microwave-safe food tubs and automotive components. Regulatory pushes for higher recycled content favor rPET investments, whereas polypropylene volatility, with prices at USD 970-990 per tonne CFR in early 2025, stresses SME cash flows. Bioplastic PLA capacity of 75,000 tonnes coming onstream by 2026 introduces fresh competition, yet cost parity is some years away.

Continued dairy bottling and pharmaceutical vial adoption anchor PET volume, while the circular-economy narrative lifts brand acceptance of recycled grades. PP’s heat-resistance profile secures growth in hot-fill applications even as resin price uncertainty leads converters to hedge procurement. Collectively, resin choice trends will recalibrate margins across the India rigid plastic packaging market.

By Product Type: Bottles & Jars Dominate While Trays Accelerate

Bottles & Jars contributed 35.31% of the India rigid plastic packaging market share in 2025 due to universal use in milk, water and OTC medicine. Rice, snack and ready-to-eat portfolios rely on barrier trays that extend shelf life under humid conditions. Intermediate bulk containers maintain a stable niche in chemicals, amplified by the ethanol program that lifts 20-liter drum procurement. Product innovation centers on lightweight neck finishes that drop resin usage per unit, a vital lever to sustain profitability inside the India rigid plastic packaging market.

By End-Use Industry: Food Steady, Pharmaceuticals Fastest

Food applications accounted for 25.22% of the India rigid plastic packaging market size in 2025, anchored by dairy, edible oils and snacks. Pharmaceutical demand, expanding at 8.12% CAGR, gains from India’s role as the leading global supplier of generics and vaccines.

Regulations mandate child-resistant closures and traceability features on export vials, pushing converters to invest in vision inspection and clean-room molding. Cosmetics and personal care segments ride income growth but remain comparatively smaller. Overall, end-use diversification tempers cyclical swings in the India rigid plastic packaging market.

By Production Process: Extrusion Scale, Injection Precision

Extrusion held 68.34% revenue in 2025, underlying the cost-effective production of water and milk bottles. Injection molding, poised for a 5.65% CAGR, captures closures, pharma components and intricate personal-care jars where dimensional accuracy is critical.

Automation drives both lines, yet injection projects focus on multi-cavity hot-runner tools to cut cycle time. Blow molding retains relevance for HDPE jerrycans demanded by the ethanol blend program. Thermoforming gains in bakery clamshells, aided by polypropylene’s rigidity-to-weight advantage. Collectively, evolving process mix underpins productivity gains across the India rigid plastic packaging market.

Geography Analysis

Western India leads consumption with 46.72% of national plastic demand as FMCG and petrochemical clusters co-locate in Gujarat and Maharashtra. Northern states deploy automotive and packaging hubs around Delhi-NCR, while southern Tamil Nadu leverages port access for processed-food exports. Government-approved plastic parks—10 to date—provide shared utilities that cut conversion costs and support exports that the industry targets to double to USD 25 billion by 2025.

Inland logistics improves under the Unified Logistics Interface Platform, reducing transit damage to rigid packs bound for tier-II cities. Cold-chain corridors linking dairy catchments to consumption centers further widen addressable demand in the India rigid plastic packaging market. Export-oriented units around special economic zones win pharma and food assignments from Western buyers who value India’s BIS and ISO certifications.

Collectively, geography shapes resin selection, pack formats and compliance investments, making location strategy a critical determinant of competitiveness inside the India rigid plastic packaging market.

Competitive Landscape

The market remains fragmented. PAG’s USD 1 billion purchase of Manjushree Technopack and USD 200 million follow-on deal for Pravesha Industries provide scale and pharma exposure. UFlex allocates USD 200 million to backward integration in Egypt, insulating resin inputs for its Indian plants.

Amcor’s Lift-Off program commits USD 3 million annually to start-ups solving recyclability and AI-based design, aiming to speed sustainable innovations. Ganesha Ecopet’s tie-up with Sorema lifts bottle-to-bottle recycling to 42,000 tonnes a year, addressing supply gaps ahead of the 2025 mandate.

Mold-Tek commissions three plants focused on pharma tubs, courting a Rs 6,000 crore opportunity with tamper-evident IML pails. Resin price swings and tightening BIS norms are squeezing sub-scale players, accelerating M&A and joint-venture activity within the India rigid plastic packaging market.

India Rigid Plastic Packaging Industry Leaders

Essel Propack (EPL Ltd)

Manjushree Technopack Ltd

Mold-Tek Packaging Ltd

Pyramid Technoplast Pvt Ltd

Chemco Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Deluxe Recycling opened India’s largest multi-layered plastic (MLP) recycling facility in Gujarat, doubling capacity to 27,400 tpa and supplying rigid auto components made from recovered plastics.

- April 2025: Loop Industries and Ester Industries confirmed the Infinite Loop India plant in Gujarat will break ground in Q2 2025, aiming to supply 100% recycled PET resin and polyester fiber from 2027.

- February 2025: Ganesha Ecopet commissioned two additional Starlinger lines, lifting bottle-to-bottle rPET capacity to 42,000 t per year and targeting 25% of India’s used PET bottle stream by 2026.

- January 2025: PAG acquired packaging firm Pravesha Industries at an enterprise value of Rs 1,700 crore (USD 200 million), broadening its pharma-grade rigid container portfolio.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the India rigid plastic packaging market as all primary, reusable, and returnable articles, bottles, jars, trays, drums, IBCs, caps, and closures, manufactured from PET, PE, PP, PVC, PS / EPS, and emerging bio-resins that retain shape during handling and storage. According to Mordor Intelligence, volumes are tracked in metric tons and then converted to revenue using weighted average selling prices observed at converter level.

Scope exclusion: Disposable flexible pouches, multilayer laminates, paper or metal rigid packs, and thermoform inserts made from recycled board are not part of this assessment.

Segmentation Overview

- By Resin Type

- Polyethylene (PE)

- Low-Density Polyethylene (LDPE)

- Linear Low-Density Polyethylene (LLDPE)

- High-Density Polyethylene (HDPE)

- Polyethylene Terephthalate (PET)

- Polypropylene (PP)

- Polystyrene (PS) and Expanded PS (EPS)

- Polyvinyl Chloride (PVC)

- Other Resin Type

- Polyethylene (PE)

- By Product Type

- Bottles and Jars

- Trays and Containers

- Intermediate Bulk Containers (IBCs)

- Drums and Jerrycans

- Other Product Type

- By End-Use Industry

- Food

- Snacks and Confectionery

- Fresh Produce

- Dairy Based Products

- Dry Foods and Cereals

- Pet Food

- Other Food Products

- Beverage

- Bottled Water

- Juices and Nectars

- Dairy Based Beverages

- Carbonated Soft Drinks

- Other Beverages

- Food-service

- Pharmaceuticals

- Cosmetics and Personal Care

- Industrial

- Other End-Use Industry

- Food

- By Production Process

- Blow Molding

- Injection Molding

- Extrusion

- Thermoforming

Detailed Research Methodology and Data Validation

Primary Research

Analysts spoke with resin suppliers, blow-molders, dairy brands, pharma fillers, and large e-commerce shippers across West, North, and South India. Interviews validated run-rate utilization, average container weights, post-consumer resin uptake, and near-term demand signals, filling gaps left by public data and anchoring key assumptions.

Desk Research

We began with open datasets from the Department of Chemicals & Petro-Chemicals, Directorate General of Commercial Intelligence & Statistics customs logs, and the Ministry of Food Processing Industries, which together clarify domestic resin supply and packaged-food output. Trade association briefs from the All-India Plastics Manufacturers Association, Indian Institute of Packaging, and Plastindia Foundation offered converter capacity maps and recycling rate updates. Company 10-Ks, investor decks, and reputable press traced new blow-molding lines and M&A moves. D&B Hoovers and Dow Jones Factiva helped size private converter revenues. This list is illustrative; many additional sources fed baseline checks and context building.

Market-Sizing & Forecasting

A top-down construct starts with polymer production plus net imports, deducts export of finished packs, and applies conversion yields to derive container tonnage, which is then multiplied by segment-specific ASPs. Results are stress-tested against a bottom-up sample of converter sales and channel checks. Variables such as FMCG output index, per-capita milk consumption, organized retail floor space, PET scrap collection rate, resin price spread, and capacity additions feed a multivariate regression that projects demand through 2030. Scenario analysis adjusts for EPR compliance pace.

Data Validation & Update Cycle

Mordor analysts triangulate model outputs with shipment records and periodic converter audits. Variance beyond set thresholds triggers re-contact of sources before sign-off. Reports refresh yearly, with interim updates whenever duty changes, major capacity closures, or policy shifts materially alter the outlook.

Why Our India Rigid Plastic Packaging Baseline Commands Reliability

Published estimates often diverge because firms adopt different fiscal calendars, resin baskets, or assume uniform price inflation.

By aligning scope with on-ground converter reality and refreshing inputs every twelve months, Mordor delivers a decision-ready number buyers can track over time.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 14.28 Bn (2025) | Mordor Intelligence | - |

| USD 11.76 Bn (2025) | Global Consultancy A | Excludes drums and IBCs; relies only on converter sales surveys |

| USD 10.57 Bn (2024) | Research Publisher B | Counts PET and HDPE only; applies single high ASP across SKUs |

| USD 12.89 Bn (FY 2025) | Regional Firm C | Uses fiscal year base and generic plastics price index with limited primary checks |

The comparison shows that scope breadth, price stratification, and refresh cadence are the chief drivers of variance. By integrating verified resin flows with live market interviews, Mordor Intelligence offers the most balanced, transparent baseline for planners seeking dependable numbers.

Key Questions Answered in the Report

What is the current value of the India rigid plastic packaging market?

The market is worth USD 15.17 billion in 2026 and is projected to reach USD 20.53 billion by 2031.

Which resin holds the largest share in the India rigid plastic packaging market?

Polyethylene Terephthalate leads with 33.02% share in 2025.

Why are HDPE jerrycans in higher demand?

Government targets for 20% ethanol-blended fuel by 2025 require chemically resistant HDPE containers across fuel supply chains.

How will recycled-content mandates affect packaging suppliers?

A 30% rPET requirement from April 2025 is driving investments in bottle-to-bottle recycling and raising costs for brands without secure recycled resin supply.

Which end-use sector is growing fastest?

Pharmaceutical applications show the highest 8.12% CAGR thanks to India’s expanding generic drug and vaccine production.

What is the main restraint confronting the industry?

State-level single-use plastic bans and new BIS standards raise compliance expenditures and push some volume to alternative materials.

Page last updated on: