Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

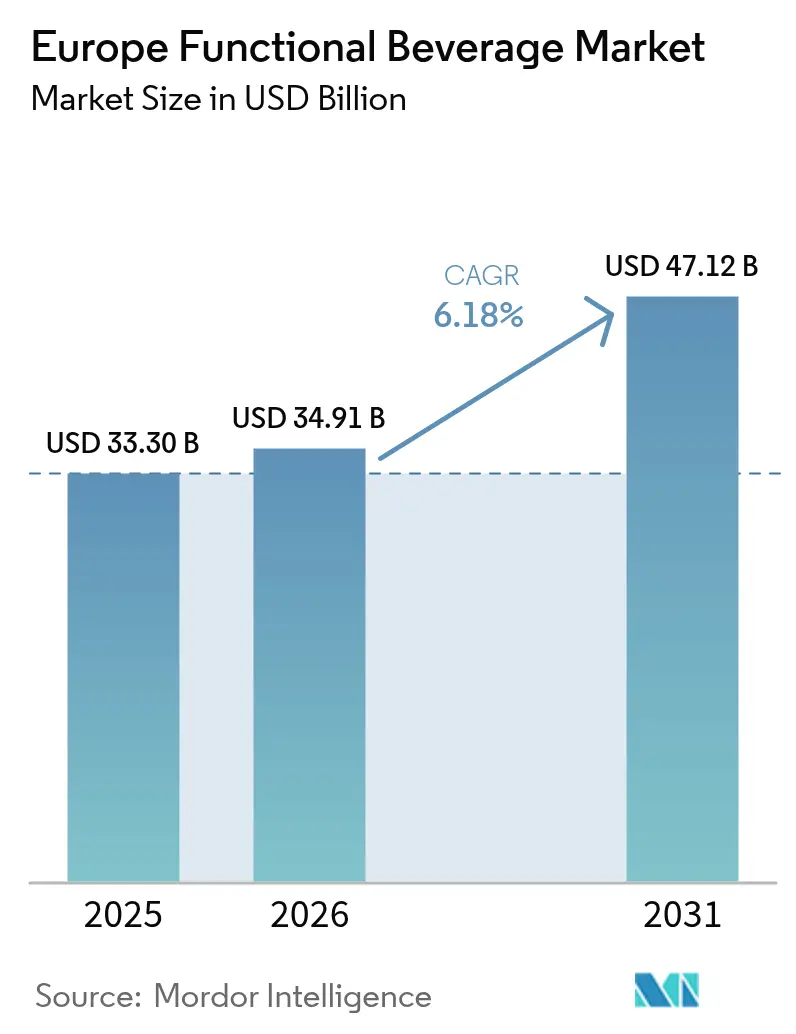

| Base Year Market Size (2025) | USD 33.30 Billion |

| Market Size (2026) | USD 34.91 Billion |

| Market Size (2031) | USD 47.12 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

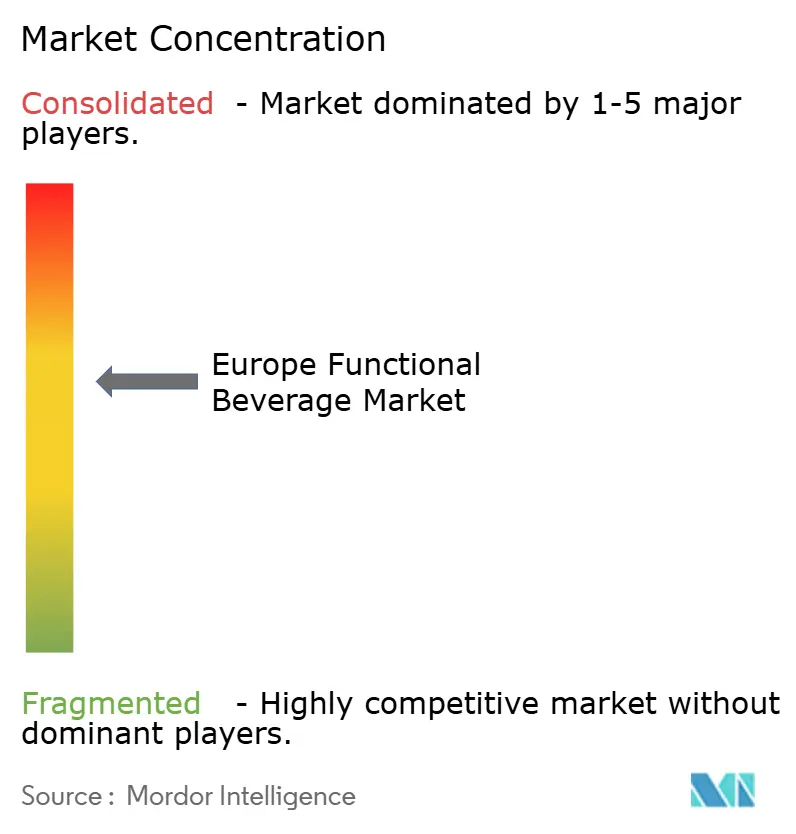

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Functional Beverage Market Analysis by Mordor Intelligence

The Europe functional beverage market size was valued at USD 33.30 billion in 2025 and is estimated to grow from USD 34.91 billion in 2026 to reach USD 47.12 billion by 2031, at a CAGR of 6.18% during the forecast period (2026-2031). Energy-boosting products remain prevalent on retail shelves; however, consumer preferences are shifting toward clinically validated health benefits, clean-label ingredients, and sustainability commitments. Multinational companies are reallocating research budgets toward randomized controlled trials that comply with European Food Safety Authority standards, while retailers are increasing shelf space for plant-based, low-sugar, and gut-health-focused products. The expansion of subscription-based e-commerce is boosting direct-to-consumer brands that prioritize personalization and fresher supply chains. At the same time, rising ingredient and packaging costs are putting pressure on margins, leading manufacturers to streamline product portfolios and invest in vertically integrated sourcing strategies. In this environment, the European functional beverage market is evolving from refreshment-focused offerings to evidence-based nutrition, supporting resilient value growth even as traditional soft drink sales show stagnation.

Key Report Takeaways

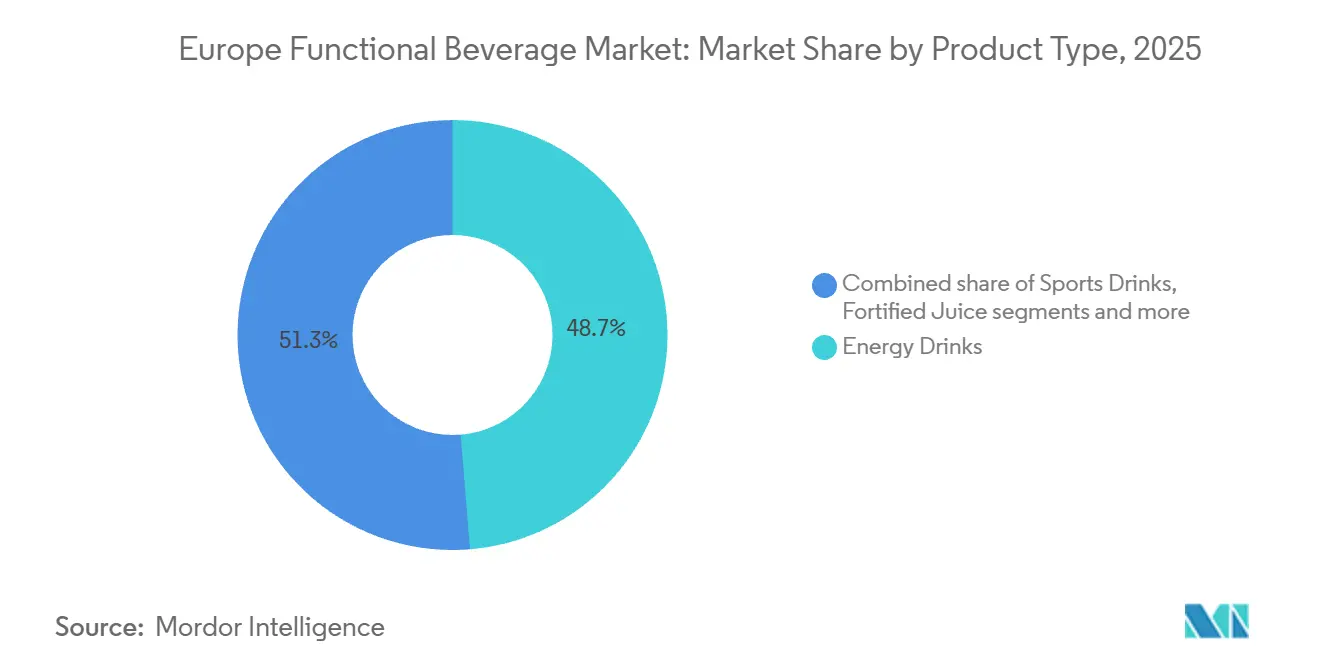

- By product type, Energy Drinks led with 49.21% of the Europe functional beverage market share in 2025, while Sports Drinks are advancing at an 8.23% CAGR through 2031.

- By functionality, Immune Support captured 48.01% of the Europe functional beverage market size in 2025, whereas Digestive Health is projected to expand at an 8.43% CAGR between 2026 and 2031.

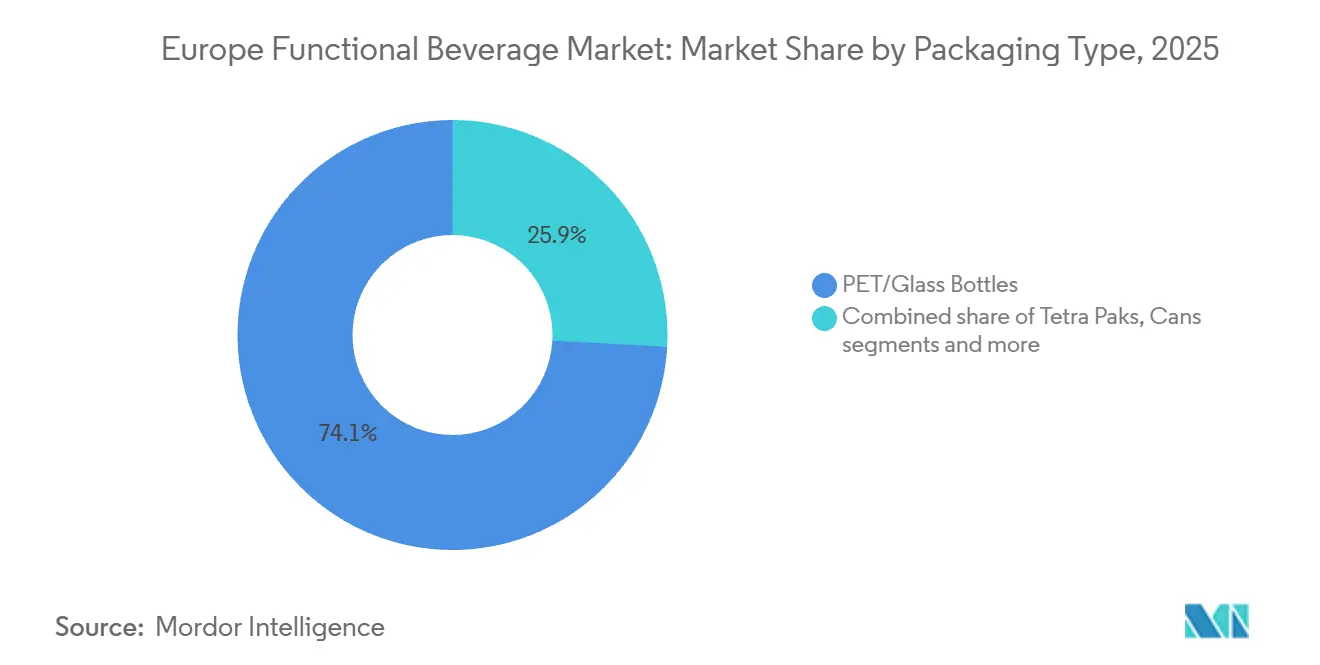

- By packaging, PET and Glass Bottles accounted for 74.12% of 2025 volume; Tetra Paks represent the fastest-growing format at an 8.88% CAGR to 2031.

- By distribution, Supermarkets and Hypermarkets held 41.89% share in 2025, yet Online Retail Stores are forecast to grow at a 7.27% CAGR through 2031.

- By geography, Germany dominated with 34.81% of 2025 value; France is the fastest-growing geography at a 7.81% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Functional Beverage Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising consumer focus on proactive health and wellness maintenance | +1.2% | Germany, United Kingdom, France, Netherlands, Sweden | Medium term (2-4 years) |

| Increasing demand for clean-label beverages with natural ingredients | +0.9% | Germany, France, United Kingdom, Belgium, Netherlands | Short term (≤ 2 years) |

| Growing emphasis on sustainability and ethical sourcing of ingredients | +0.7% | Germany, France, Netherlands, Sweden, Belgium | Long term (≥ 4 years) |

| Shift towards plant-based and organic functional beverages | +1.1% | Germany, France, United Kingdom, Netherlands, Sweden | Medium term (2-4 years) |

| Popularity of energy drinks for quick energy boosts and convenience | +0.8% | Germany, United Kingdom, Poland, Spain, Italy | Short term (≤ 2 years) |

| Aging population driving demand for preventive wellness beverages | +0.6% | Germany, Italy, France, Spain, Belgium | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumer focus on proactive health and wellness maintenance

European consumers are increasingly incorporating functional beverages into their daily routines as preventive health measures rather than using them as reactive remedies. This behavioral shift, which gained momentum during the COVID-19 pandemic, has now become well-established. A recent survey by the International Probiotics Association Europe revealed that over half of European consumers feel inadequately informed about the health benefits of probiotics. However, nearly half of respondents in the United Kingdom reported consuming a functional beverage within the past three months, highlighting latent demand that could be unlocked through education and clinical validation [1]Source: International Probiotics Association Europe, “IPA Europe Manifesto 2024,” IPA Europe, ipaeurope.org. This proactive approach is particularly evident in Germany and the Netherlands, where consumers actively seek products enriched with vitamins D and K2 for bone health, omega-3 fatty acids for cardiovascular support, and adaptogens like ashwagandha for stress management. This trend is influencing product development cycles, with brands increasingly allocating research budgets to randomized controlled trials. These trials aim to meet the European Food Safety Authority's cause-and-effect standards for health claims, enabling the transformation of wellness aspirations into regulatory-compliant marketing strategies.

Increasing demand for clean-label beverages with natural ingredients

The demand for clean-label products has evolved from a marketing trend to an essential product attribute, as European consumers increasingly examine ingredient lists for artificial sweeteners, synthetic colors, and unfamiliar additives. Natural sweeteners like stevia, derived from *Stevia rebaudiana*, and monk fruit, sourced from *Siraitia grosvenorii*, are replacing aspartame and sucralose in product reformulations. However, manufacturers face challenges in masking the taste of these sweeteners, often requiring co-formulation with erythritol or allulose to achieve acceptable palatability. In February 2024, Danone announced an investment in a new Alpro plant-based facility in France, with a production capacity exceeding 300,000 liters per day, highlighting the scale needed to meet clean-label demand while remaining cost-competitive. Additionally, the Union of European Soft Drinks Associations has pledged a 10% reduction in sugar content across member portfolios by 2025. This commitment has accelerated the adoption of natural flavor systems derived from botanicals such as hibiscus, elderflower, and turmeric. This trend is particularly significant in Germany and France, where organic certification and Nutri-Score labeling strongly influence consumer purchasing decisions at the point of sale.

Growing emphasis on sustainability and ethical sourcing of ingredients

Sustainability has shifted from being a secondary corporate social responsibility effort to a key purchasing factor, as European consumers increasingly demand transparency regarding carbon footprint, water usage, and fair labor practices across beverage supply chains. The Coca-Cola Company's "World Without Waste" initiative, which aims for fully recyclable packaging within the next few years and achieving net-zero carbon emissions by the middle of the century, highlights the level of commitment needed to remain relevant among environmentally conscious consumers. Similarly, Danone achieved B Corporation certification for its North American operations several years ago and has expanded regenerative agriculture practices to its European dairy and plant-based ingredient sourcing. This includes partnerships with farmers to restore soil health, sequester carbon, and reduce reliance on synthetic fertilizers. Oatly's recent investment in production facilities in Sweden and the Netherlands integrates renewable energy infrastructure and regenerative oat farming practices, aligning the brand with consumers who closely examine Scope 3 emissions and agricultural methods. The focus on ethical sourcing is particularly strong in Germany, the Netherlands, and Sweden, where consumers are willing to pay premiums of 10% to 15% for products certified by organizations such as Fair Trade, Rainforest Alliance, or B Corporation. Retailers like Albert Heijn and ICA also emphasize partnerships with suppliers that have verified sustainability credentials, reflecting the growing importance of ethical and sustainable practices in these markets.

Shift towards plant-based and organic functional beverages

Plant-based functional beverages are gaining market share from dairy-based alternatives, driven by the prevalence of lactose intolerance, environmental concerns, and the perception that plant proteins offer better digestibility. Analysis by Roland Berger indicates that the European plant-based dairy market has been expanding significantly, with oat milk emerging as the preferred base for functional fortification due to its neutral flavor and creamy texture. Oatly's expansion across Northern Europe, particularly in Sweden and the United Kingdom, has helped normalize plant-based functional beverages in mainstream grocery channels. Additionally, Alpro's announcement in March 2025 to source 100% British oats highlights a localization strategy aimed at reducing carbon footprints and appealing to regional provenance preferences. Organic certification remains a key differentiator in Germany, where the Bio-Siegel label commands price premiums of 15%-20%, and in France, where the Agriculture Biologique (AB) certification is essential for entry into specialty health food retailers such as Naturalia and Biocoop.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent regulatory requirements for health claim labeling | -0.8% | Germany, France, United Kingdom, Netherlands, Belgium | Medium term (2-4 years) |

| Formulation difficulties with natural flavor enhancers | -0.4% | Germany, United Kingdom, France, Italy, Spain | Short term (≤ 2 years) |

| Elevated production costs for innovative ingredients | -0.6% | Germany, France, United Kingdom, Netherlands, Sweden | Medium term (2-4 years) |

| Consumer skepticism regarding unverified health claims | -0.5% | Germany, United Kingdom, France, Italy, Spain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent regulatory requirements for health claim labeling

The European Food Safety Authority (EFSA) enforces rigorous standards for validating health claims, requiring clinical trials that can cost significant amounts per ingredient. These requirements create challenges for small and mid-sized enterprises that lack the necessary research infrastructure. EFSA mandates evidence of cause-and-effect relationships through human randomized controlled trials, a standard that has left thousands of botanical health claims "on hold" for years. This has significantly stifled innovation in the herbal and traditional ingredient categories. European Union Regulation 2024/2105, which rejected health claims for certain probiotic strains and plant extracts, highlights the regulatory conservatism that compels brands to rely on general function claims instead of specific therapeutic messaging [2]Source: EUR-Lex, “EU Regulation 2024/2105 on Health Claims,” Official Journal of the European Union, eur-lex.europa.eu. This approach reduces product differentiation and complicates consumer education. The impact of these restrictions is particularly pronounced in Germany and France, where national authorities strictly adhere to EFSA guidelines with minimal flexibility. In contrast, Italy and Spain have historically adopted more lenient interpretations for traditional Mediterranean botanicals, such as olive leaf extract and pomegranate. For instance, in some cases, the approval rate for health claims in these countries has been higher than in others, exceeding 50% for certain traditional ingredients.

Formulation difficulties with natural flavor enhancers

The shift from artificial to natural flavor systems brings technical challenges that can impact taste profiles, shelf stability, and cost structures, especially when reformulating established products with a loyal customer base. Natural sweeteners such as stevia and monk fruit often have bitter or metallic aftertastes, requiring the addition of complementary ingredients like erythritol, allulose, or natural flavor extracts. This increases formulation complexity and raises raw material costs by 15% to 25% compared to synthetic options. Similarly, natural colors derived from sources like beetroot, turmeric, and spirulina are sensitive to factors such as pH, light, and heat. These sensitivities restrict their use in acidic beverages and transparent packaging formats, where exposure to ultraviolet (UV) light during shelf life can degrade the product. Flavor houses, including Givaudan and Firmenich, are investing in enzymatic modification and fermentation technologies to improve the taste and stability of natural ingredients. However, these innovations are proprietary and expensive, offering competitive advantages to large manufacturers with exclusive supply agreements. The formulation challenges are particularly significant in Energy Drinks and Sports Drinks, where consumers have well-established taste preferences. Reformulating these products risks disrupting customer expectations, potentially leading to a loss of customers to competitors that maintain traditional flavor profiles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Energy Drinks Dominance Meets Sports Drinks Acceleration

Sports Drinks are projected to grow at a compound annual growth rate (CAGR) of 8.23% through 2031, marking the fastest growth among product types. This trend is driven by increasing consumer focus on hydration and electrolyte replenishment, reflecting the rising participation in endurance sports and functional fitness activities across Europe. Energy Drinks accounted for 49.21% of the market in 2025, supported by Red Bull's strong brand presence and Monster's extensive retail partnerships. However, the category faces challenges from age-restriction policies in Eastern Europe and growing concerns about excessive caffeine consumption among adolescents. Fortified Juice is experiencing stagnation as consumers increasingly view traditional orange and apple juice bases as high in sugar. In response, brands are shifting toward cold-pressed, low-glycemic formulations featuring superfruits such as acai, goji, and aronia.

Dairy and Dairy-Alternative Drinks are benefiting from the plant-based trend, with oat and almond bases allowing for fortification with calcium, vitamin D, and omega-3 fatty acids while maintaining vegan-friendly positioning. Functional and Fortified Water is gaining traction among health-conscious urban consumers seeking hydration with added vitamins, minerals, or electrolytes, without the calorie content of traditional sports drinks. In this segment, Vitamin Well has established a strong presence in Sweden and is expanding into Germany and the United Kingdom. The demand for these products is growing as consumers increasingly prioritize health and wellness, with fortified water offering a balance of functionality and low-calorie content.

By Functionality: Immune Support Leadership Yields to Digestive Health Momentum

Digestive Health is projected to be the fastest-growing functionality, with a compound annual growth rate (CAGR) of 8.43% through 2031. This growth is driven by increasing clinical evidence linking gut microbiome diversity to metabolic health, mental well-being, and immune resilience. This shift has elevated probiotics and prebiotics from niche supplements to widely used beverage ingredients. Immune Support accounted for 48.01% of the market in 2025, supported by heightened consumer awareness following the COVID-19 pandemic and the widespread inclusion of vitamin C, zinc, and elderberry in fortified beverages. However, the category faces challenges such as commoditization due to converging efficacy claims and intensifying price competition. Bone and Joint Health, while a smaller segment, is gaining momentum among aging populations in Germany, Italy, and France. Beverages fortified with calcium, vitamin K2 (menaquinone), and collagen peptides are addressing concerns related to osteoporosis and arthritis in these markets. Other Functionalities, including energy, cognitive performance, and beauty-from-within, are diversifying consumer preferences, complicating retail assortment strategies.

The European probiotic market, as reported by the International Probiotics Association Europe, is dominated by fermented dairy drinks such as Danone's Actimel and Yakult [3]Source: International Probiotics Association, “A Holistic Approach to Probiotics in The EU for Informed Consumers And A Sustainable Food Industry,” ipaeurope.org. However, innovation is increasingly focused on next-generation postbiotics and psychobiotics. Postbiotics, which consist of non-viable microbial cells or their metabolites, offer advantages such as eliminating the need for cold-chain logistics and addressing issues related to the viability of live probiotic formulations. These features enable the development of shelf-stable products, reducing distribution costs and creating new market opportunities. Furthermore, significant research is being conducted on the gut-brain axis, with early-stage clinical trials exploring the potential of Lactobacillus and Bifidobacterium strains to influence serotonin production and alleviate anxiety. These advancements could transform the Digestive Health market, positioning it as a mental wellness category rather than being confined to gastrointestinal health.

By Packaging Type: PET and Glass Bottles Face Tetra Pak Sustainability Challenge

Tetra Paks are projected to grow at a compound annual growth rate (CAGR) of 8.88% through 2031, making it the fastest-growing packaging format. This growth is driven by brand commitments to carbon neutrality, the format's superior shelf stability, and consumer perception of carton packaging as more environmentally friendly compared to single-use plastics. PET (Polyethylene Terephthalate) and glass bottles accounted for 74.12% of the market in 2025, supported by consumer familiarity, transparency that highlights product color and clarity, and resealability, which aligns with on-the-go consumption needs. Cans maintain a strong presence in the energy drinks segment, where aluminum's recyclability and rapid chilling properties encourage impulse purchases in convenience stores and vending machines. However, cans face challenges in penetrating the functional water and dairy-alternative categories, where glass and carton packaging are perceived as more premium. Other packaging formats, such as pouches and single-serve sachets, remain niche but are gaining traction in e-commerce channels due to their lightweight nature, which reduces shipping costs and carbon emissions.

Tetra Pak's 2024 sustainability report highlighted progress toward achieving 100% renewable materials and carbon-neutral production by 2030. These milestones resonate strongly with European consumers, who rank environmental impact among their top three purchasing criteria. The company's connected packaging platform, which incorporates QR (Quick Response) codes for supply chain traceability and recycling instructions, is being adopted by companies like Danone and Nestlé to enhance transparency and address greenwashing concerns. In Europe, PET recycling rates reached 60% in 2024. However, the increasing use of colored and opaque bottles complicates mechanical recycling processes. This has prompted brands to shift toward clear PET and invest in chemical recycling partnerships capable of processing mixed-color streams.

By Distribution Channel: Supermarkets Anchor Sales While Online Retail Disrupts

Online retail stores are projected to grow at a compound annual growth rate (CAGR) of 7.27% through 2031, making them the fastest-growing distribution channel. This growth is driven by direct-to-consumer subscription models, which allow brands to achieve higher margins, collect first-party consumer data, and avoid slotting fees and promotional pressures associated with traditional retail. Supermarkets and hypermarkets accounted for 41.89% of the market in 2025, supported by the convenience of one-stop shopping, the impulse-buying behavior encouraged by end-aisle displays, and the cost advantages large-format retailers gain through volume purchasing and private-label offerings.

Convenience stores remain essential for energy drinks and single-serve formats, as their proximity to transportation hubs and suitability for immediate consumption occasions drive foot traffic. However, their limited shelf space restricts product variety and favors established brands with high turnover rates. Specialty stores, including health food retailers such as Holland and Barrett in the United Kingdom and Naturalia in France, cater to a niche demographic of wellness-focused consumers willing to pay premium prices for organic certifications and specialized formulations. The shift toward online retail is further accelerated by Amazon's expansion of its Fresh and Pantry categories, which now feature functional beverages from brands like Innocent, Vitamin Well, and Celsius, alongside subscription services that streamline repeat purchases and offer discounts for bundled orders. Direct-to-consumer brands such as Huel and Athletic Greens have entirely bypassed traditional retail, leveraging social media marketing and influencer partnerships to build brand communities and secure customer lifetime value through subscription models. In Europe, e-commerce penetration for functional beverages reached 12% in 2025, lagging behind the United States by approximately 5%, indicating untapped growth potential as logistics infrastructure improves and consumer confidence in online grocery delivery continues to strengthen.

Geography Analysis

Germany led the European market in 2025, capturing 34.81% of the market share. This leadership is attributed to the country's well-established organic food culture, strict quality standards enforced through the Bio-Siegel certification, and the dominance of major retailers such as Edeka, Rewe, Aldi, and Lidl, which together control over 60% of grocery retail. German consumers are highly willing to invest in functional beverages that offer clinical validation, third-party certifications, and transparent ingredient sourcing. This preference has allowed premium brands like Vitamin Well and Innocent to secure shelf space alongside mainstream options from Coca-Cola and PepsiCo. Additionally, Germany's aging population, with over 21% of residents aged 65 or older, is driving demand for beverages that support bone health, joint care, and cognitive function. Products fortified with calcium, vitamin D, collagen, and omega-3 fatty acids are becoming increasingly common in these categories. The country's regulatory environment, characterized by strict adherence to European Food Safety Authority guidelines and a cultural aversion to exaggerated marketing claims, has strengthened consumer trust and created a stable foundation for sustained growth.

France is the fastest-growing market in Europe, with a compound annual growth rate (CAGR) of 7.81% projected through 2031. This growth is supported by government-backed nutrition initiatives such as the Nutri-Score labeling system, a strong cultural preference for organic and locally sourced ingredients, and the growing adoption of sports nutrition as part of everyday wellness routines. French consumers are increasingly turning to functional beverages as meal replacements or post-workout recovery options, making protein content and amino acid profiles key factors in purchasing decisions. The plant-based dairy market in France is also expanding rapidly, with Danone's Alpro facility serving as a regional manufacturing hub for oat- and almond-based functional beverages distributed across Western Europe. Retailers such as Carrefour, Auchan, and Leclerc are responding to consumer demand by increasing shelf space for functional beverages, while specialty stores like Biocoop and Naturalia are curating selections that emphasize organic certification and fair-trade sourcing.

The United Kingdom, Italy, and Spain represent mature markets where functional beverages compete with traditional coffee, tea, and juice consumption habits, but each market has unique growth drivers. In the United Kingdom, functional beverage penetration reached 49% of consumers in 2024, driven by the availability of kombucha, cold-pressed juices, and plant-based protein drinks in major retailers like Tesco, Sainsbury's, and Waitrose. Direct-to-consumer brands such as Huel have also normalized meal-replacement beverages among time-constrained urban professionals. Italy's functional beverage market is evolving more slowly due to cultural preferences for espresso and traditional Mediterranean diets. However, the aging population and increasing obesity rates are creating opportunities for digestive health and weight management products. In Spain, the sports nutrition segment is outperforming other categories, reflecting the country's active lifestyle and the popularity of activities such as cycling, running, and football. Electrolyte-enhanced beverages are gaining traction in retailers like Mercadona and Carrefour.

Competitive Landscape

The Europe Functional Beverage Market shows moderate concentration, with multinational companies such as PepsiCo, The Coca-Cola Company, Red Bull, Danone, and Nestlé utilizing extensive distribution networks and significant marketing budgets. However, regional specialists and digitally native challengers retain pricing power in premium and niche segments. Strategic trends indicate a division between cost leadership, as demonstrated by Coca-Cola's "World Without Waste" initiative aiming for 100% recyclable packaging by 2025, and differentiation through clinical validation, as seen in Danone's investment in randomized controlled trials for its Actimel probiotic strain. Opportunities are emerging in areas such as postbiotic formulations, psychobiotic beverages targeting mental wellness, and personalized nutrition platforms that use artificial intelligence (AI) to recommend functional beverages based on individual health data and genetic profiles.

Emerging players like Celsius, which has expanded its European distribution through strategic partnerships, and Vitamin Well, which customizes formulations to Nordic taste preferences, are disrupting established companies by targeting underserved demographics and leveraging social media marketing to build brand communities. These companies are effectively addressing gaps in the market while creating strong consumer engagement through innovative approaches.

Technology is becoming a critical competitive factor, with companies investing in connected packaging, blockchain-based supply chain traceability, and direct-to-consumer e-commerce platforms that collect first-party consumer data, enabling dynamic pricing and personalized promotions. Nestlé's Health Science division has filed patents for microencapsulation technologies designed to enhance the bioavailability of vitamins and probiotics. This innovation could support efficacy claims validated through pharmacokinetic studies and meet the European Food Safety Authority's (EFSA) cause-and-effect standards. Additionally, companies are focusing on achieving 100% efficiency in their supply chains to meet sustainability goals and consumer expectations. The adoption of these technologies is expected to drive growth and improve consumer trust in the functional beverage market.

Europe Functional Beverage Industry Leaders

PepsiCo, Inc.

The Coca-Cola Company

Red Bull GmbH

Danone SA

Monster Beverage Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: PepsiCo introduced Pepsi Prebiotic Cola, containing 3 g prebiotic fiber and 5 g cane sugar, following its USD 1.95 billion acquisition of Poppi, marking its first functional soda launch.

- April 2025: Red Bull has expanded its seasonal energy drink range with the introduction of the Summer Edition White Peach flavor. This product is offered in both sugared and sugar-free options, addressing a wider spectrum of consumer preferences.

- March 2025: PepsiCo’s USD 1.95 billion acquisition of Poppi highlights its focus on expanding its presence in the gut-health beverage segment. This move strengthens its portfolio with prebiotic drinks that cater to the growing demand for functional beverages.

- January 2025: Carlsberg has completed the acquisition of Britvic, becoming the largest multi-beverage supplier in the United Kingdom. This acquisition enhances Carlsberg's market position and broadens its product portfolio across multiple beverage categories.

Europe Functional Beverage Market Report Scope

A functional beverage refers to a conventional liquid food that is marketed to emphasize specific ingredients or claimed health benefits. The European functional beverage market is categorized based on Product Type, Functionality, Packaging Type, Distribution Channel, and Geography. By Product Type, the categories include Energy Drinks, Sports Drinks, Fortified Juice, Dairy and Dairy-Alternative Drinks, Functional or Fortified Water, and Other Product Types. By Functionality, the market is segmented into Digestive Health, Immune Support, Bone and Joint Health, and Other Functionalities. By Packaging Type, the options include PET (Polyethylene Terephthalate) or Glass Bottles, Cans, Tetra Paks, and Others. By Distribution Channel, the market is divided into Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Online Retail Stores, and Others. By Geography, the market covers Germany, the United Kingdom, Italy, France, Spain, the Netherlands, Poland, Belgium, Sweden, and the Rest of Europe. The market sizing has been done in value terms in USD and volume in liters for all the abovementioned segments.

By Product Type

| Energy Drinks |

| Sports Drinks |

| Fortified Juice |

| Dairy and Dairy-Alternative Drinks |

| Functional/Fortified Water |

| Other Product Types |

By Functionality

| Digestive Health |

| Immune Support |

| Bone and Joint Health |

| Other Functionalities |

By Packaging Type

| PET/Glass Bottles |

| Cans |

| Tetra Paks |

| Others |

By Distribution Channel

| Supermarkets and Hypermarkets |

| Convenience Stores |

| Speciality Store |

| Online Retail Stores |

| Others |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Energy Drinks |

| Sports Drinks | |

| Fortified Juice | |

| Dairy and Dairy-Alternative Drinks | |

| Functional/Fortified Water | |

| Other Product Types | |

| By Functionality | Digestive Health |

| Immune Support | |

| Bone and Joint Health | |

| Other Functionalities | |

| By Packaging Type | PET/Glass Bottles |

| Cans | |

| Tetra Paks | |

| Others | |

| By Distribution Channel | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Speciality Store | |

| Online Retail Stores | |

| Others | |

| By Geography | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe functional beverage market?

It stands at USD 34.91 billion in 2026 and is projected to reach USD 47.12 billion by 2031.

Which product category is growing fastest in Europe?

Sports Drinks are the fastest, advancing at an 8.23% CAGR through 2031.

Which functionality segment shows the strongest momentum?

Digestive Health leads with an 8.43% CAGR forecast between 2026 and 2031.

How significant is online retail for European functional beverages?

Online channels are forecast to exceed USD 6 billion by 2031, expanding at a 7.27% CAGR.

Which country contributes the largest market share?

Germany held 34.81% of 2025 revenue, driven by strong organic and clinical-validation preferences.

Page last updated on: