Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

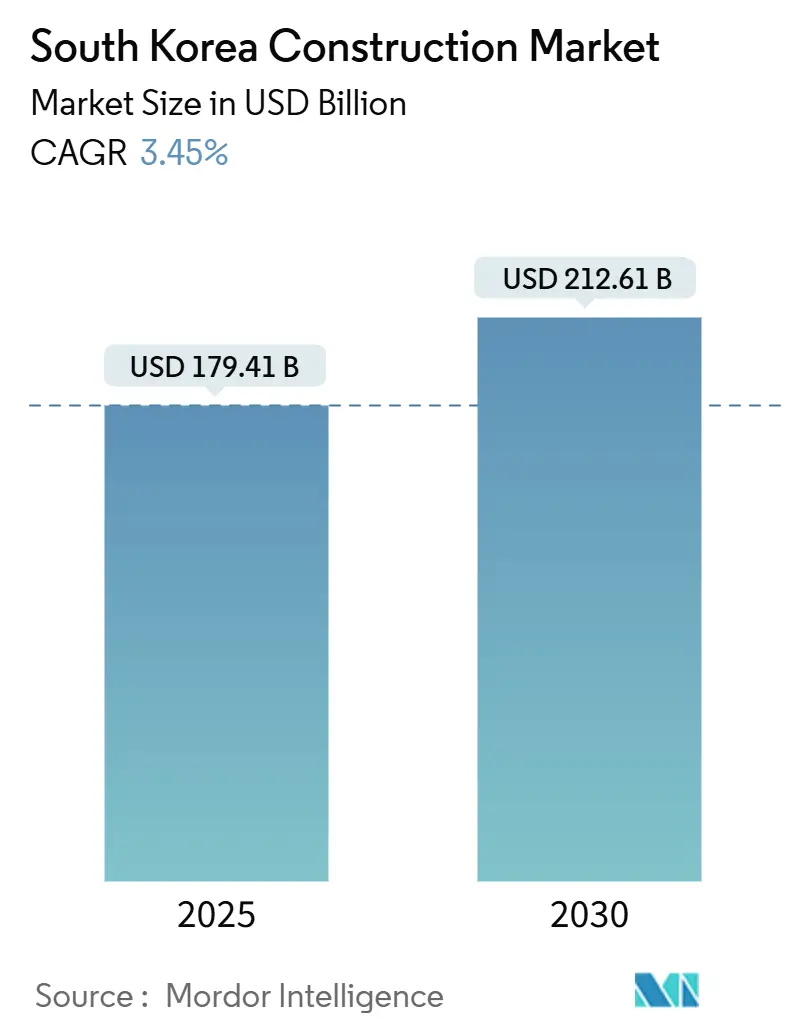

| Market Size (2025) | USD 179.41 Billion |

| Market Size (2030) | USD 212.61 Billion |

| Growth Rate (2025 - 2030) | 3.45% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea Construction Market Analysis by Mordor Intelligence

The South Korea construction market size is valued at USD 179.41 billion in 2025, and is forecast to attain USD 212.61 billion by 2030, advancing at a 3.45% CAGR during 2025-2030. Political uncertainty following the 2025 impeachment of President Yoon Suk Yeol has not derailed spending plans because both the central government and large corporations continue to prioritize transport upgrades, semiconductor fabs, and clean-energy assets. Construction cost inflation and labor shortages are forcing contractors to embrace Building Information Modelling, prefabrication, and modular approaches, which increase speed and mitigate waste. Growing foreign direct investment, record semiconductor outlays, and easier redevelopment rules in Seoul’s older districts are stimulating demand across residential, infrastructure, and industrial segments. Medium-term prospects also benefit from a national pledge to finish all GTX high-speed rail corridors and the USD 44.8 billion 2025 public works budget that accelerates housing delivery and transport modernization.

Key Report Takeaways

- By city, Seoul led with 37.9% of South Korea construction market share in 2024. The South Korea construction market for Incheon is projected to expand at a 4.65% CAGR between 2025-2030.

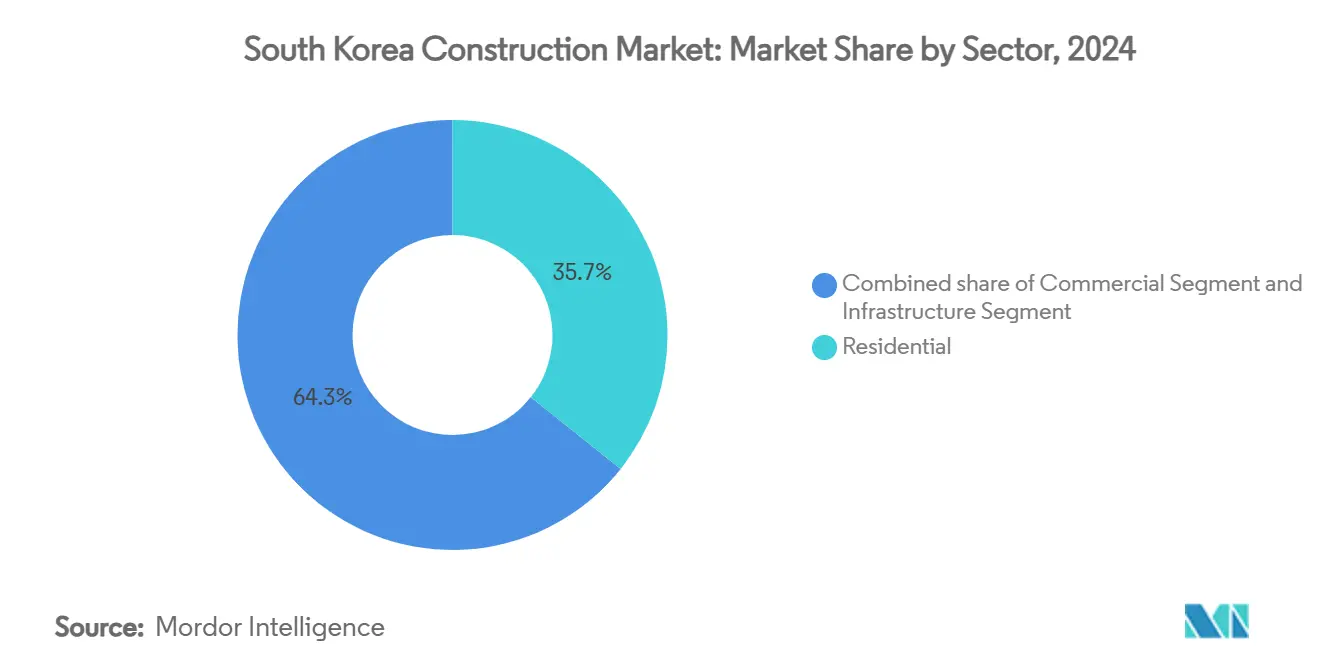

- By sector, the residential segment held 35.7% of South Korea construction market revenue share in 2024. The South Korea construction market for infrastructure is forecast to post the fastest 4.01% CAGR between 2025-2030.

- By construction type, new construction accounted for 73.5% of the South Korea construction market size in 2024. The South Korea construction market for renovation grows at a 4.11% CAGR between 2025-2030.

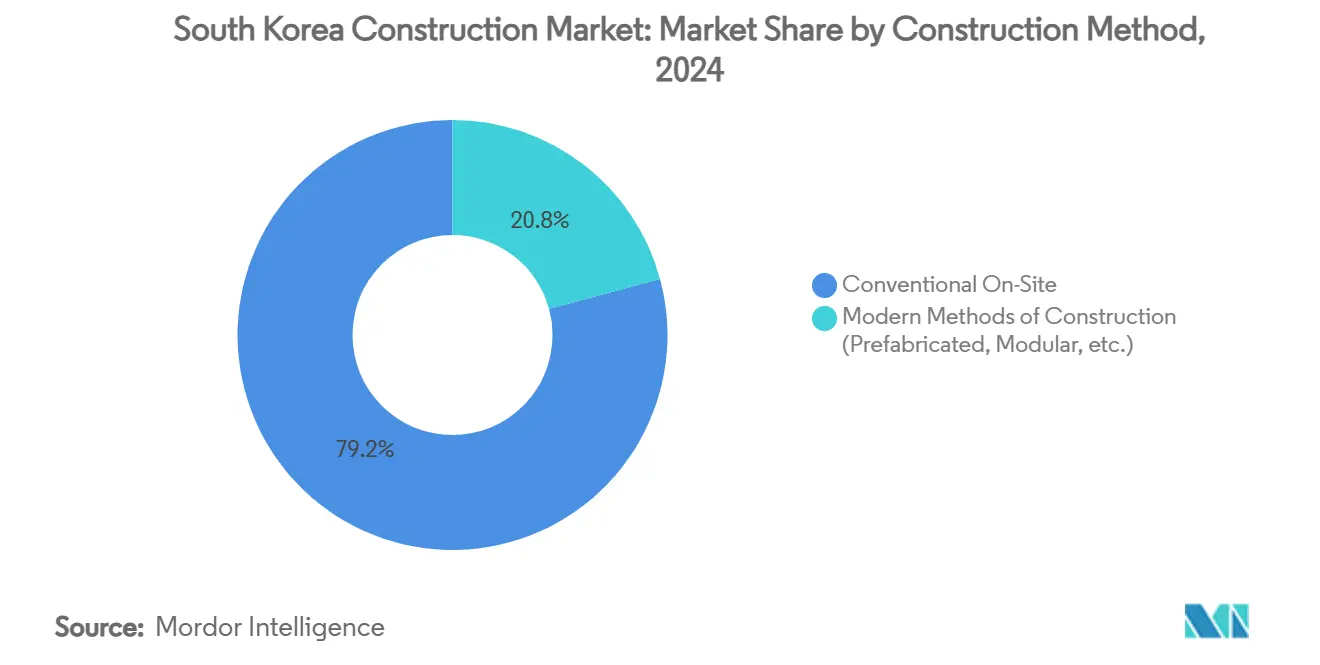

- By construction method, conventional on-site techniques represented 79.2% of South Korea construction market share in 2024. The South Korea construction market for modern modular approaches advance at a 4.91% CAGR between 2025-2030.

- By investment source, private investment commanded a 64.8% share of the South Korea construction market size in 2024. The South Korea construction market for private investment is rising at a 4.21% CAGR between 2025-2030.

South Korea Construction Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industrial and energy projects expanding with demand from tech and power sectors | +0.9% | Gyeonggi Province, Ulsan, and major industrial complexes | Long term (≥ 4 years) |

| Large infrastructure upgrades in rail, ports, and airports | +0.8% | National, with concentration in Seoul metropolitan area and Busan | Medium term (2-4 years) |

| Targeted government funding supporting key infrastructure | +0.7% | National, priority on transport and housing | Medium term (2-4 years) |

| Urban redevelopment boosting activity in Seoul and major cities | +0.6% | Seoul, Busan, Daegu, Incheon metropolitan areas | Medium term (2-4 years) |

| Export-driven industrial base supporting factory and logistics investment | +0.5% | Coastal regions and industrial clusters | Long term (≥ 4 years) |

| Adoption of BIM and modular technology improving speed and efficiency | +0.4% | National, early adoption by major contractors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Large Infrastructure Upgrades Drive Public Construction Momentum

Mega rail, airport, and port programs anchor public spending and multiply activity across the South Korea construction market. GTX-A started passenger service in December 2024 and cut the Paju–Seoul commute in half, demonstrating the network’s city-pair impact. Work on the GTX-B corridor is underway with a USD 5.3 billion budget and a completion target of 2030, signaling continuity despite leadership change at the Blue House. Hyundai E&C is also the sole bidder for the USD 10.5 billion Gadeok Airport, revealing capacity constraints yet underlining long-term project certainty[1]Joon-ho Kim, “GTX-B Line Groundbreaking Ceremony Transcript,” Ministry of Land, Infrastructure and Transport, molit.go.kr. Tunnel breakthroughs, such as the 50 km Yulhyun bore, showcase domestic engineering strengths that can be exported regionally. Together, these undertakings reinforce stable order books for large contractors and suppliers.

Industrial and Energy Projects Expand with Tech Sector Demand

Record chip spending drives unprecedented industrial construction. Samsung’s USD 471 billion cluster in Gyeonggi and SK Hynix’s USD 15 billion Yongin fab demand vast cleanroom, power, and water infrastructure. The 11th Basic Plan pushes nuclear back to 35.2% of the electricity mix by 2038, reviving work on Shin-Hanul Units 3-4. Gas-fired power, typified by the 1.05 GW Yongin plant, supplies interim energy for semiconductor foundries[2]Seon-kyu Hwang, “Shin-Hanul Units 3 & 4 Construction Approval Notice,” Korea Hydro & Nuclear Power, khnp.co.kr. Parallel data-center pipelines, including a 1 GW AI site by SK Group and AWS, require specialist cooling and resilience design. This pipeline compels contractors to upskill in high-specification industrial delivery.

Urban Redevelopment Accelerates in Seoul and Major Cities

Fast-track approvals now allow apartment complexes older than 30 years to sidestep safety audits, which cuts a year from schedules and widens the pool of qualifying estates. Landmark schemes such as Jamsil Jugong 5’s 70-storey towers and Apgujeong’s ultra-luxury rebuilds strengthen the premium residential sub-segment. The KRW 550 billion (USD 0.4 billion) Han River project introduces floating leisure and cultural platforms that stretch contractor capabilities into marine works. Yet Seoul issued only 32% of its 2023 housing permits due to tight financing, a reminder that policy reform must align with liquidity conditions. Nonetheless, redevelopment momentum lifts the South Korea construction market by pivoting volume toward high-value infill projects.

Targeted Government Funding Supports Infrastructure Amid Economic Headwinds

The 2025 transport and housing budget of USD 44.8 billion sustains demand even as GDP growth moderates. Cash subsidies up to 75% and seven-year tax waivers for foreign investors deepen the funding pool for big builds. A USD 13.1 billion semiconductor facility finance package signals long-term policy continuity regardless of cabinet changes[3]Sang-woo Lee, “2025 National Infrastructure & Housing Budget,” Ministry of Land, Infrastructure and Transport, molit.go.kr. Nuclear restart contracts worth USD 2.2 billion have already flowed to domestic suppliers, illustrating fiscal support for mixed energy investment. Such predictable pipelines help contractors plan labor, equipment, and digital upgrades.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor shortages and rising wages delaying projects and raising costs | -0.9% | National, acute in Seoul metropolitan area | Short term (≤ 2 years) |

| Volatile material prices and import disruptions straining budgets | -0.7% | National, higher impact in coastal projects | Medium term (2-4 years) |

| Weakening domestic demand softening new launches | -0.6% | National, chiefly residential and commercial | Short term (≤ 2 years) |

| Lengthy permitting and complex land issues slowing starts | -0.5% | Seoul and other metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Labor Shortages and Rising Wages Delay Projects

Rapid demographic ageing and restricted immigration have squeezed construction labor pools. OECD data show construction vacancies topping historic norms, while average site wages climbed in tandem with a 6.7% jump in ready-mix concrete costs during early 2024. Semiconductor fabs need cleanroom specialists that take months to certify, extending schedules at Yongin and Pyeongtaek. Contractors try to offset gaps with modular production lines, yet this shift demands retraining that small firms defer. Wage premiums and benefit upgrades preserve delivery timetables but compress margins and discourage bid participation on lower-value tenders.

Volatile Material Prices and Import Disruptions Strain Budgets

Project budgets have struggled with 30% construction cost jumps in the third new cities because cement, steel, and concrete prices swung sharply during 2024. A weak KRW, trading near 1,430 per USD, inflated the cost of imported equipment and specialist finishes. Global commodity upheavals forced builders to keep larger inventories, stressing working capital and elevating financing charges. High-profile delays, including Samsung and LG pausing certain US projects, illustrate how volatility bleeds into global strategies and resource allocation. Contract renegotiations and supply-chain audits have become routine, pushing out start dates and raising headline risk on major developments.

Segment Analysis

By Sector: Infrastructure Leads Growth Despite Residential Dominance

Infrastructure’s 4.01% CAGR positions it as the fastest-expanding slice of the South Korea construction market, even though residential still held 35.7% of 2024 revenue. Transport upgrades like the GTX corridors, ongoing motorway widening, and the USD 10.5 billion Gadeok Airport supply a stable pipeline that attracts global engineering partners. Nuclear restarts and renewable capacity expansions further lengthen backlogs for specialist contractors, while public guarantees reduce counterparty risk. Residential momentum now tilts towards high-value rebuilds rather than greenfield sprawl, with tower replacements in Apgujeong and Jamsil setting benchmark premiums. Luxury demand and urban infill bolster contractor margins yet tether exposure to regulatory cycles and mortgage policy adjustments.

The commercial subset remains two-speed. Prime office completions stay limited, lifting occupancy and rents, whereas legacy retail format projects pivot towards mixed-use repositioning. Industrial and logistics construction thrives on semiconductor cluster suppliers and e-commerce consolidation. Collectively, these shifts underline a portfolio effect where infrastructure growth compensates for more cyclical housing swings, giving the South Korea construction market diversified resilience across macro environments.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Construction Type: Renovation Gains Momentum Amid New Construction Dominance

New builds contributed 73.5% of 2024 spending, but renovations’ 4.11% CAGR is the higher trajectory segment. Fast-track rules that waive certain safety inspections for complexes over 30 years can influence 950,000 households by 2027, unlocking a deep pipeline for retrofit specialists. Renovation also faces fewer land acquisition battles, making it attractive in dense districts where plots are scarce and expensive. Developers still battle resident consensus and temporary relocation logistics, yet streamlined approvals shrink overall cycle times and release capital sooner, enticing institutional investors.

South Korea construction market size for renovation is therefore set to rise faster than that for new builds. Nevertheless, greenfield campuses for semiconductors, EVs, and petrochemicals assure large-ticket new-construction awards. The twin track suggests that contractors that bundle engineering, procurement, and refurbishment capabilities can capture a broader opportunity set and hedge portfolio risk as credit conditions shift.

By Construction Method: Modern Methods Accelerate Despite Conventional Leadership

Conventional practice retained a 79.2% share in 2024, yet modern methods are growing at a 4.91% CAGR. Modular plants in Chungcheong province now fabricate up to 80% of structural components under controlled conditions, allowing on-site assembly in weeks rather than months. Studies show 10-20% cost savings and significant waste reduction when BIM drives early clash detection. Government projections indicate the modular sub-sector could triple to USD 1.8 billion by 2024, lifting the modern slice of the South Korea construction market even faster. Initial skepticism about quality is fading thanks to successful pilot towers and factory-finished interior standards. As wage pressures intensify, more tier-two contractors procure modular kits from domestic vendors, broadening adoption beyond the largest conglomerates.

Conventional techniques are unlikely to disappear because heavy civil works, deep foundations, and bespoke high-rise geometries still demand on-site craft. Yet digital tools are penetrating legacy workflows too, making the boundary between the two approaches increasingly porous. The capacity to combine precast cores, BIM coordination, and on-site finishing will distinguish next-generation leaders.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Investment Source: Private Investment Sustains Growth Leadership

Private capital accounted for 64.8% of 2024 funding and is projected to outpace public allocations with a 4.21% CAGR. The USD 471 billion semiconductor super-cluster, wholly financed by corporate balance sheets and global lenders, exemplifies private appetite for long-dated infrastructure. Foreign pledges hit USD 32.7 billion in 2024 as extended tax holidays and cash grants pushed projects over the line. Real estate surveys suggest two-thirds of local corporates will lift construction budgets through 2030, seeking workplace innovations that retain talent and boost productivity. Meanwhile, public-private partnerships such as Gadeok Airport illustrate blended models, with state agencies underwriting planning risk and consortia providing execution capacity.

Public outlays remain critical for social housing and provincial road upgrades, but fiscal headroom is narrowing as debt service rises. Market discipline, therefore, hinges on private capital maintaining confidence in Korea’s rule-of-law framework and political commitment to infrastructure delivery. So far, robust participation rates in project tenders indicate a steadfast belief in long-term fundamentals underpinning the South Korean construction market.

Geography Analysis

Seoul kept 37.9% of 2024 activity, benefiting from marquee redevelopments and steady prime-office leasing, yet its growth trails the national average because land scarcity and stringent permitting slow new launches. The Han River floating park and Jamsil tower rebuilds illustrate high-value niches that elevate revenue per square meter. However, only one-third of the 80,000-unit housing target was permitted in 2023, underscoring implementation friction. Investors prize the city’s transparent rental market and transport links, sustaining stable capitalization rates that support fresh starts when approvals finally materialize.

Incheon is the fastest-expanding urban node with a 4.65% CAGR. The GTX-B line will cut journey times to central Seoul to roughly 30 minutes, catalyzing residential densification around new stations. Industrial spill-overs from the Yongin microchip corridor produce demand for supporting logistics parks, worker dormitories, and auxiliary services. Material cost spikes have stretched budgets by up to one-third, yet developers push ahead due to the strategic value of proximity to both the capital and Incheon International Airport.

Busan, Daegu, and the rest of South Korea together form a diversified demand base. Busan’s USD 10.5 billion Gadeok Airport extends runway capacity and positions the port city as a regional logistics hub. The Oceanix floating city pilot showcases climate-adaptive design, potentially exporting Korean know-how to coastal regions worldwide. North-eastern Chuncheon’s 550,000 m² tech complex demonstrates provincial government efforts to lure bio and AI investors away from congested metro areas. These initiatives reflect the policy intent to balance national growth and distribute construction employment more evenly.

Competitive Landscape

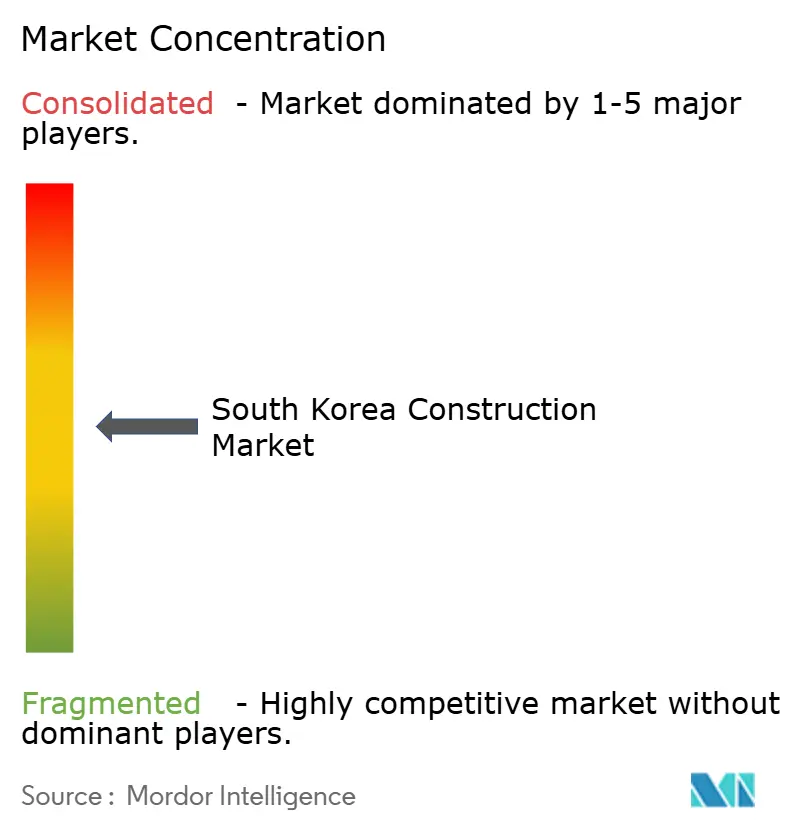

The South Korea construction market is moderately concentrated. Samsung C&T, Hyundai E&C, and GS E&C sustain leadership through integrated engineering divisions, global procurement, and large balance sheets. They also spearhead BIM roll-outs and trial modular high-rise prototypes. Mid-tier specialists such as HanmiGlobal gained global recognition, ranking 8th worldwide in construction management revenues after landing refinery, hospital, and data-center mandates. Technology partnerships are emerging as a competitive lever: Samsung C&T’s renewable venture with LS Electric targets mega-solar and onshore wind farms, while Doosan Enerbility steers nuclear commissioning.

Strategic moves show firms hedging domestic exposure with overseas concessions, such as Samsung-GS winning a USD 7.6 billion Saudi gas-plant EPC contract. M&A is another lever, evidenced by the revised Doosan Robotics-Bobcat merger plan that combines field robots with heavy equipment to automate site logistics. Rising labor and material costs intensify pressure on margins, so companies that digitize workflows, lock in long-term supplier contracts, and expand service offerings will protect profitability. Competition will further sharpen as international consortiums eye Korea’s data-center and clean-energy pipelines.

South Korea Construction Industry Leaders

-

Samsung C&T Corporation

-

Hyundai E&C

-

GS E&C

-

Daewoo E&C

-

DL E&C (Daelim)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: SK Group and AWS confirmed a USD 6.5 billion joint build of Korea’s largest AI data center in Ulsan, slated for February 2029.

- March 2025: Hyundai Motor and Saudi Arabia’s Public Investment Fund agreed to construct a USD 500 million vehicle assembly plant with production from 2026.

- May 2024: POSCO and CNGR broke ground on a joint nickel and battery precursor plant in Pohang, securing critical minerals for Korea’s EV supply chain.

- April 2024: A Samsung-GS consortium secured a USD 7.6 billion contract to build a gas plant in Saudi Arabia, strengthening Korea’s position in Middle East energy EPC markets.

South Korea Construction Market Report Scope

Construction is a general term meaning the art and science of forming objects, systems, or organizations. Construction is an industry that includes the erection, maintenance, and repair of buildings and other immobile structures and the building of roads and service facilities that become integral parts of structures and are essential to their use.

The South Korean construction market is segmented by sector (residential construction, commercial construction, industrial construction, infrastructure (transportation) construction, and energy and utilities construction). The report offers market size and forecasts for the South Korean construction market in value (USD billion) for all the above segments.

By Sector

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy and Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By Key Cities

| Seoul |

| Busan |

| Daegu |

| Incheon |

| Rest of South Korea |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy and Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By Key Cities | Seoul | |

| Busan | ||

| Daegu | ||

| Incheon | ||

| Rest of South Korea | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the South Korea construction market?

The market stands at USD 179.41 billion in 2025 and is projected to grow to USD 212.61 billion by 2030 at a 3.45% CAGR.

Which segment grows fastest within the South Korea construction market?

Infrastructure construction records the quickest expansion, rising at a 4.01% CAGR due to rail, airport, and energy projects.

How significant is private investment to the sector?

Private capital accounts for 64.8% of spending and is increasing at a 4.21% CAGR, supported by semiconductor and data-center megaprojects.

Why is modular construction gaining attention in Korea?

Labor shortages and cost pressures drive adoption; modular methods can shift up to 80% of work off-site and reduce timelines by weeks while saving 10-20% on costs.

Which region outside Seoul shows the highest growth?

Incheon leads regional growth with a 4.65% CAGR owing to the GTX-B rail line and spill-overs from nearby semiconductor facilities.

What are the main restraints on market growth?

Acute labor shortages, volatile material prices, lengthy permitting, and softer domestic demand together trim the sector’s potential CAGR by more than 2 percentage points.

Page last updated on: