Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.05 Billion |

| Market Size (2031) | USD 9.27 Billion |

| Growth Rate (2026 - 2031) | 18.01% CAGR |

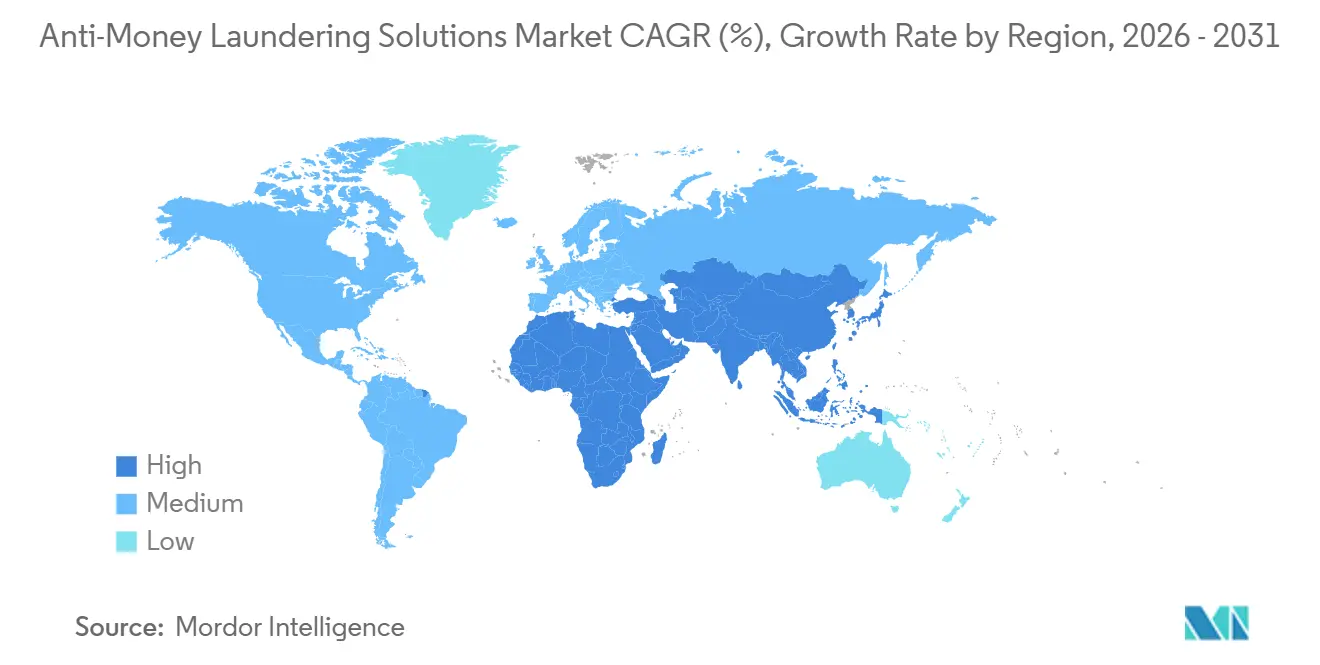

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti-Money Laundering Solutions Market Analysis by Mordor Intelligence

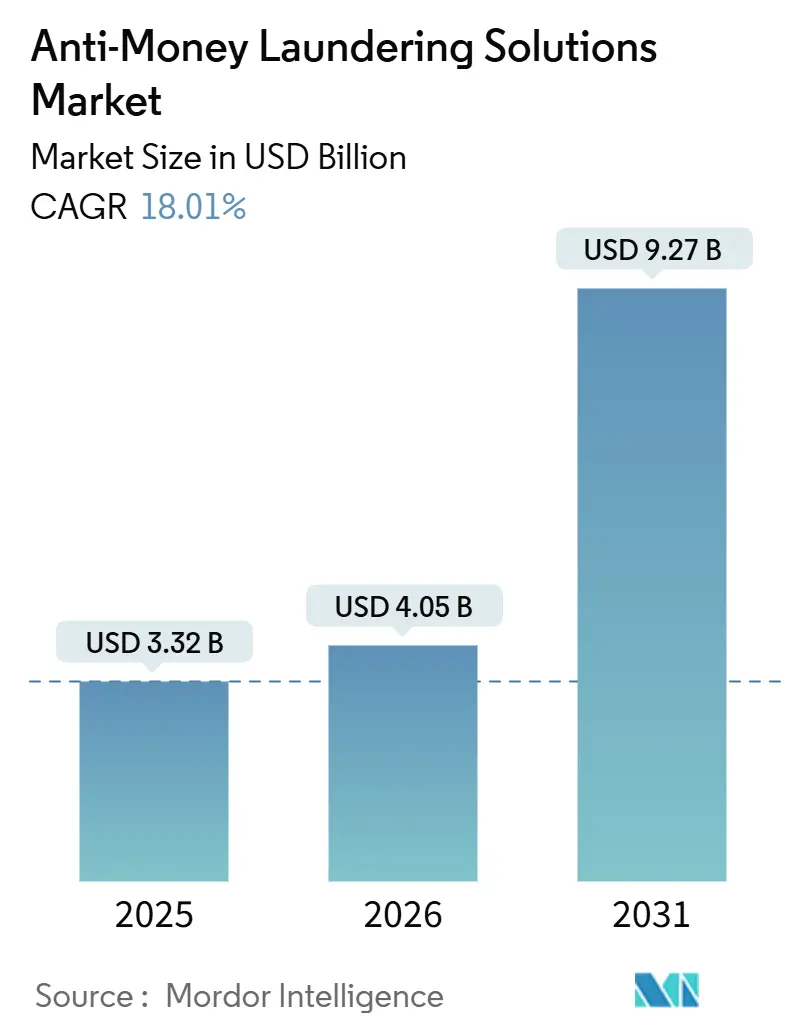

The anti-money laundering solutions market size is expected to grow from USD 3.32 billion in 2025 to USD 4.05 billion in 2026 and is forecast to reach USD 9.27 billion by 2031 at an 18.01% CAGR over 2026-2031. Continued regulatory tightening, rapid adoption of instant-payment rails, and mounting enforcement penalties are pushing compliance teams to replace legacy, batch-based controls with always-on analytics. Cloud-native platforms that pool anonymized data are gaining favour because real-time surveillance needs elastic compute that on-premises installations struggle to provide. Venture capital is flowing to start-ups that embed agentic artificial intelligence in investigative workflows, promising to compress alert handling times without adding headcount. At the same time, financial-crime units are shifting scarce specialists toward proactive typology design while outsourcing high-volume alert triage to managed-service providers. Together, these forces create a demand cycle that keeps the anti-money laundering solutions market on a steep growth trajectory.

Key Report Takeaways

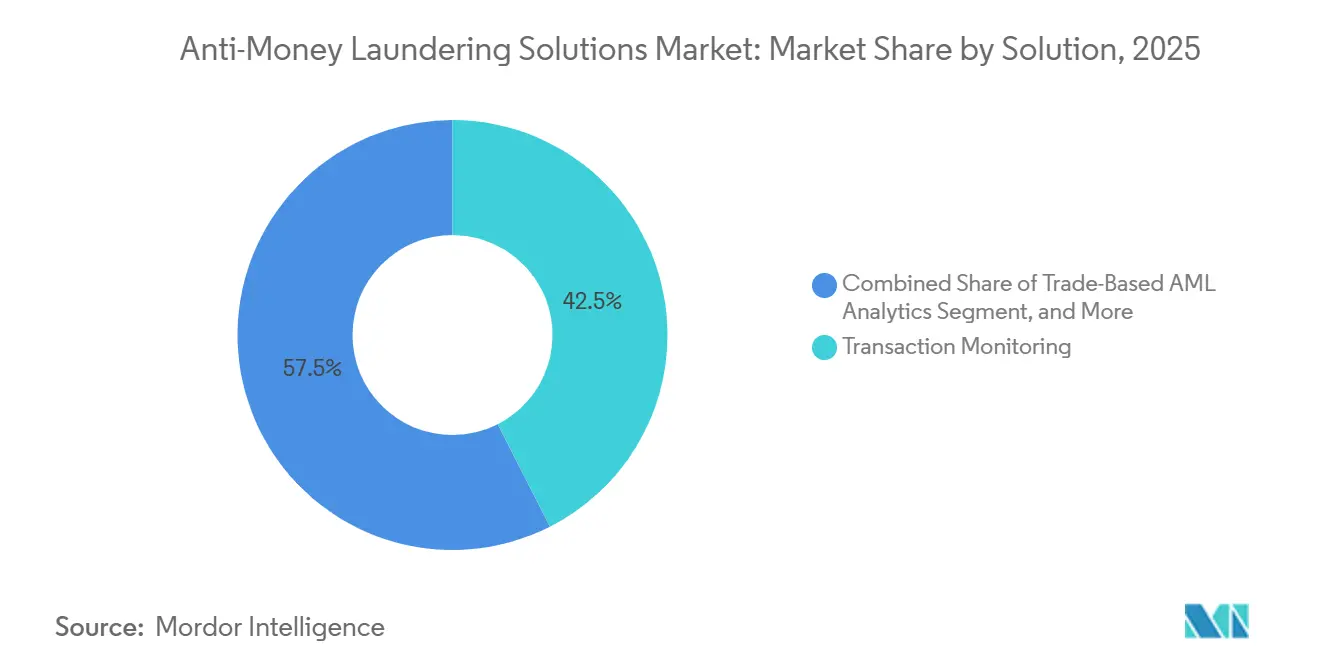

- By solution, transaction monitoring systems led with 42.51% revenue share in 2025, while trade-based analytics is projected to expand at an 18.91% CAGR through 2031.

- By component, software accounted for 63.59% of the anti-money laundering solutions market share in 2025, yet services are forecast to grow at 18.84% through 2031.

- By deployment model, on-premises deployments commanded 58.94% of the anti-money laundering solutions market size in 2025, whereas cloud solutions are advancing at an 18.53% CAGR to 2031.

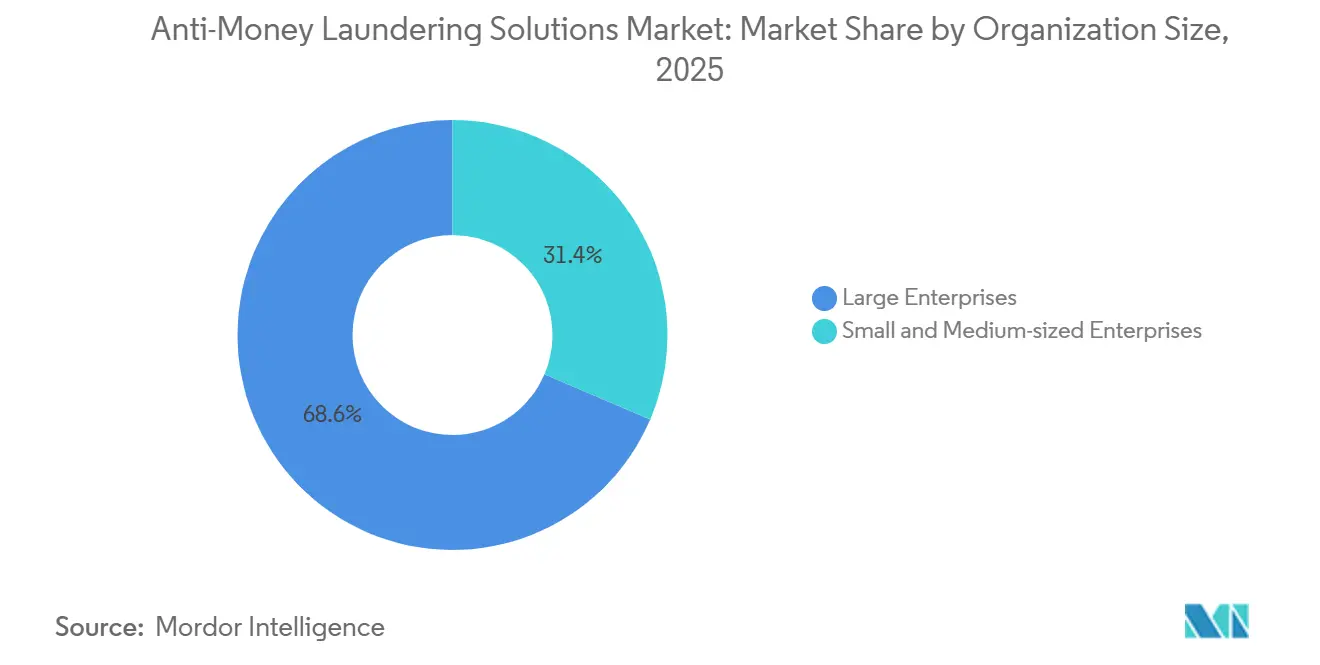

- By organization size, large enterprises held 68.58% of spending in 2025 and small and medium-sized enterprises are set to grow at a 19.05% CAGR through 2031.

- By end-user, banking represented 54.54% of 2025 revenue, and cryptocurrency exchanges are forecast to record the highest CAGR at 19.11% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Anti-Money Laundering Solutions Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Real-Time Compliance Mandates under EU AMLR 2023 | +3.20% | Europe, spillover to UK and Middle East | Medium term (2-4 years) |

| Expansion of Instant Payment Schemes Lifting Monitoring Volumes | +2.80% | Global, led by North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Cryptocurrency Exchange Licensing in Asia-Pacific Fuelling Blockchain-Analytics Spend | +2.50% | Asia-Pacific core, spillover to Middle East | Medium term (2-4 years) |

| FinCEN Rule Extending to SEC-Registered Investment Advisers | +1.90% | North America, primarily United States | Short term (≤ 2 years) |

| FATF Grey-Listing Pressure Accelerating Upgrades in High-Risk Economies | +1.60% | Africa, South America, Southeast Asia | Long term (≥ 4 years) |

| Convergence of Digital Identity and eKYC Platforms with AML Stacks | +1.40% | Global, early adoption in Europe and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Real-Time Compliance Mandates Under EU AMLR 2023

The European Union’s Anti-Money Laundering Regulation, published in 2024, obliges firms to screen transactions before funds leave the institution, replacing overnight batch reviews.[1]“The new EU AML framework: Guide to key changes for financial institutions,” Baker McKenzie, bakermckenzie.com Lowered customer-due-diligence thresholds intensify data-collection demands, and a board-level compliance manager role ensures executive accountability. Because more than 80% of surveyed European banks remain in early preparation, vendors have a multi-year runway to supply real-time analytics, centralized beneficial-ownership checks, and harmonized suspicious-activity-report templates.[2]“Deloitte study: most EU financial institutions are in early preparation stage,” Deloitte, deloitte.com The regulation’s extraterritorial reach forces United Kingdom and Middle East institutions operating in the bloc to adopt identical standards, turning the anti-money laundering solutions market into a compliance technology arms race.

Expansion of Instant Payment Schemes Lifting Monitoring Volumes

FedNow, SEPA Instant, and India’s Unified Payments Interface settle transactions in seconds, compressing alert-decision windows and multiplying monitoring volumes. Banks report alert spikes of up to 40% after onboarding instant rails, exposing rule-based systems that lack latency-optimized scoring. The European Central Bank processed 14.6 billion instant transactions in 2024, forcing adoption of in-memory analytics.[3]“TARGET Instant Payment Settlement,” European Central Bank, ecb.europa.eu Vendors such as NICE Actimize now offer cross-institution intelligence feeds that surface counterparty risk in milliseconds, a capability that accelerates cloud migration and pushes the anti-money laundering solutions market ahead of broader regtech spending.

Cryptocurrency Exchange Licensing in Asia-Pacific Fuelling Blockchain-Analytics Spend

Singapore, Hong Kong, and Japan now license virtual-asset service providers under bank-equivalent standards. Singaporean rules effective December 2024 require suspicious-transaction reports within five working days and enhanced due diligence above SGD 20,000 (USD 15,000). Hong Kong demands blockchain analytics that can trace funds through mixers and privacy coins. Venture funding follows: Sardine raised USD 70 million in 2025 to expand AI agents for automated sanctions monitoring. These mandates push exchanges to deploy enterprise platforms, expanding the addressable anti-money laundering solutions market beyond traditional finance.

FinCEN Rule Extending to SEC-Registered Investment Advisers

Effective January 2026, roughly 15,000 U.S. investment advisers managing USD 110 trillion must adopt risk-based programs, file suspicious-activity reports, and appoint compliance officers. Smaller advisers face per-client compliance costs above USD 1,200, driving outsourcing and boosting services demand. Parallel European rules widen coverage to mortgage intermediaries and crowdfunding platforms, aligning transatlantic obligations. As wealth managers rush to integrate surveillance with portfolio systems, the anti-money laundering solutions market gains a fresh cohort of mid-sized buyers.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High False-Positive Investigation Costs for Tier-2 Banks | -1.80% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Data-Residency Laws in ASEAN Limiting Cloud AML Adoption | -1.30% | Southeast Asia, spillover to South Asia | Medium term (2-4 years) |

| Lack of Explainable-AI Models Hindering Regulator Approval | -0.90% | Global, regulatory scrutiny in Europe and United States | Medium term (2-4 years) |

| Shrinking Correspondent Banking Lines in Africa Curtailing Addressable Market | -0.70% | Africa, limited spillover to Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High False-Positive Investigation Costs for Tier-2 Banks

Alert conversion rates below 5% mean community banks burn budget on investigations that rarely yield suspicious-activity reports. The Office of the Comptroller of the Currency now allows examiners to carry forward satisfactory findings to ease pressure, yet institutions still face USD 500-plus costs per false alert. Managed-service providers offering per-alert pricing appeal to these banks, but regulatory expectations for oversight keep adoption cautious, slowing the anti-money laundering solutions market among smaller depository institutions.

Data-Residency Laws in ASEAN Limiting Cloud AML Adoption

Indonesia, Vietnam, and Thailand demand that customer data remain onshore, complicating single-tenant cloud migrations. Vendors respond with sovereign-cloud regions and in-country key management. Hybrid architectures lift implementation costs and extend project timelines, tempering cloud growth in Southeast Asia even as the anti-money laundering solutions market expands elsewhere.

Segment Analysis

By Solution: Trade Finance Analytics Gains Momentum

Trade-based analytics is forecast to be the fastest-growing slice of the anti-money laundering solutions market, expanding at an 18.91% CAGR through 2031. Traditional monitoring engines held 42.51% of 2025 revenue, yet they lack visibility into invoices, manifests, and commodity pricing. Multinational banks now feed customs data into blockchain-enabled analytics to flag over- and under-invoicing.

The anti-money laundering solutions market size tied to transaction monitoring still dominates, but niche vendors that bridge physical-goods data with payment flows are capturing new budgets. Continuous know-your-customer screening blurs with monitoring as vendors trigger re-verification when adverse media or sanctions hits appear. Case-management systems add agentic AI that drafts narratives, shrinking investigation times. Market entrants that package trade-risk models into modular APIs stand to influence the anti-money laundering solutions market share as mid-tier banks join global supply chains.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Component: Services Outpace Software

Software represented 63.59% of revenue in 2025, reflecting decades of rules-based engines deployed on-premises. Services, however, are projected to grow 18.84% per year, making them the fastest-expanding component of the anti-money laundering solutions industry. Enforcement actions signal regulators tolerate outsourcing if governance is tight, pushing institutions to contract 24/7 alert triage, sanctions screening, and suspicious-activity report drafting.

The anti-money laundering solutions market size related to professional services rises as vendors bundle model tuning and explainability documentation. Managed-service providers differentiate through typology depth: some target crypto-mixing, others trade finance or gaming patterns. This specialization shifts fixed cost into pay-per-transaction models, allowing small firms to access enterprise-grade protection.

By Deployment Model: Cloud Adoption Accelerates

On-premises installations still held 58.94% market share in 2025, but cloud deployments are advancing at an 18.53% CAGR. Elastic scaling is indispensable for real-time screening of instant payments and for model retraining that produces explainable AI artifacts demanded by supervisors. Hybrid models proliferate where data-localization rules apply, with primary screening engines running on-premises while sanctions tables, name-matching algorithms, and negative-media scans execute in vendor clouds.

Oracle’s sovereign-cloud regions let banks keep encryption keys domestically, easing Southeast Asian concerns over data flow. Over time, cloud newcomers could narrow the anti-money laundering solutions market share gap, especially as cross-institution intelligence networks require pooled data that single-tenant servers cannot provide.

By Organization Size: SMEs Enter the Fold

Large enterprises generated 68.58% of spending in 2025, but growth momentum lies with small and medium-sized enterprises. New rules rope securities advisers, crowdfunding portals, and professional football clubs into anti-money laundering surveillance. Per-user SaaS pricing lets a 30-person wealth manager deploy baseline monitoring for thousands monthly, rather than hiring full-time analysts.

Vendors pre-configure rule sets that map to niche risk typologies, lowering entry hurdles. As SME adoption widens, the anti-money laundering solutions market size gains breadth, diversifying away from its traditional dependence on global banks.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Crypto Exchanges Surge

Banking supplied 54.54% of 2025 revenue, anchored by mature regulatory frameworks and high transaction volumes. Yet cryptocurrency exchanges and virtual-asset service providers are the fastest-growing customer set, projected at a 19.11% CAGR. Asia-Pacific licensing standards now mirror bank obligations, compelling exchanges to integrate blockchain analytics with traditional KYC onboarding.

Payment service providers also accelerate spending as instant-payment volumes balloon. Gaming operators adopt pattern detection to flag rapid bet-and-cash-out behaviour. Government agencies deploy investigative platforms to spot procurement fraud. Together, these non-bank sectors expand the total addressable anti-money laundering solutions market.

Geography Analysis

North America generated 43.09% of revenue in 2025 on the back of stringent enforcement and high per-institution budgets. FinCEN’s USD 1.3 billion penalty against TD Bank reinforced the expectation that underinvestment in technology will be punished, prompting multi-year platform replacement programs.

Europe follows closely, with direct supervision by the new European Anti-Money Laundering Authority starting 2028 driving real-time system upgrades. Asia-Pacific, however, is the growth engine, forecast to advance at 19.31% through 2031. Licensing of virtual-asset providers, rapid instant-payment adoption, and Financial Action Task Force grey-listing pressures create an urgent need for modern surveillance across banks, fintechs, and public agencies.

South America and Africa remain smaller but strategically important, as correspondent banking retrenchment forces local institutions to modernize controls or lose access to dollar clearing. The Middle East leverages anti-money laundering modernization to attract fintech sandboxes and cross-border payment corridors, adding incremental demand for the anti-money laundering solutions market.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The anti-money laundering solutions market sits at moderate concentration, with legacy platform providers SAS, NICE Actimize and Oracle defending installed bases against niche AI specialists such as Hawk AI and Lucinity. Incumbents are infusing platforms with generative-AI investigation assistants that draft narrative reports and accelerate disposition cycles. Disruptors differentiate through lightweight SaaS footprints and transparent model architectures that satisfy the rising bar for explainability.

Strategic alliances multiply as vendors pair software with curated data feeds, managed-service operators and cloud-infrastructure majors. Mastercard’s Asia-Pacific TRACE launch underscores the value of payment-rail adjacency in winning regional share. Funding momentum is strong: Napier AI’s growth-equity infusion from Marlin Equity is earmarked for global channel build-out and R&D on explainable ML.

Price competition centers on total-cost-of-ownership rather than license rates alone, with buyers valuing platform extensibility, managed-service bundles and pay-per-throughput models. Vendor roadmaps converge on self-configuring risk scenarios that learn from investigator feedback loops—an arms race that places data-science talent at a premium.

Anti-Money Laundering Solutions Industry Leaders

SAS Institute, Inc.

NICE Actimize (Nice Ltd)

LexisNexis Risk Solutions

Fair Isaac Corporation (FICO)

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2026: NICE Actimize launched the Insights Network, delivering millisecond counterparty-risk scores for instant payments.

- December 2025: Socure acquired Qlarifi to build unified identity, anti-fraud, and buy-now-pay-later credit infrastructure.

- April 2025: CSI and Dataseers launched a joint AI-powered AML platform aimed at reducing alert backlogs for mid-sized U.S. banks, underscoring the appeal of collaborative go-to-market models.

- March 2025: Oracle upgraded its Investigation Hub Cloud Service with generative-AI agents that synthesize alert histories and draft SAR narratives, improving investigator productivity.

Global Anti-Money Laundering Solutions Market Report Scope

The Anti-Money Laundering Solutions Market Report is Segmented by Solution (Transaction Monitoring Systems, Know-Your-Customer and Customer Due Diligence, Sanctions and PEP Screening, Case and Alert Management, Currency Transaction and Regulatory Reporting, Trade-Based AML Analytics), Component (Software, Services), Deployment Model (On-Premise, Cloud, Hybrid), Organization Size (Large Enterprises, Small and Medium-sized Enterprises), End-User Industry (Banking, Insurance, FinTech and Payment Service Providers, Wealth and Asset Management, Gaming and Gambling Operators, Cryptocurrency Exchanges and Virtual-Asset Service Providers, Government and Public Sector), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Solution

| Transaction Monitoring Systems |

| Know-Your-Customer / Customer Due Diligence (KYC/CDD) |

| Sanctions and PEP Screening |

| Case and Alert Management |

| Currency Transaction and Regulatory Reporting |

| Trade-Based AML Analytics |

By Component

| Software |

| Services (Managed, Professional) |

By Deployment Model

| On-Premise |

| Cloud |

| Hybrid |

By Organization Size

| Large Enterprises |

| Small and Medium-sized Enterprises |

By End-User Industry

| Banking |

| Insurance |

| FinTech and Payment Service Providers |

| Wealth and Asset Management / Investment Advisers |

| Gaming and Gambling Operators |

| Cryptocurrency Exchanges and Virtual-Asset Service Providers |

| Government and Public Sector |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Nordics | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Southeast Asia | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | GCC Countries |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Solution | Transaction Monitoring Systems | |

| Know-Your-Customer / Customer Due Diligence (KYC/CDD) | ||

| Sanctions and PEP Screening | ||

| Case and Alert Management | ||

| Currency Transaction and Regulatory Reporting | ||

| Trade-Based AML Analytics | ||

| By Component | Software | |

| Services (Managed, Professional) | ||

| By Deployment Model | On-Premise | |

| Cloud | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-sized Enterprises | ||

| By End-User Industry | Banking | |

| Insurance | ||

| FinTech and Payment Service Providers | ||

| Wealth and Asset Management / Investment Advisers | ||

| Gaming and Gambling Operators | ||

| Cryptocurrency Exchanges and Virtual-Asset Service Providers | ||

| Government and Public Sector | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Southeast Asia | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | GCC Countries | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the anti-money laundering solutions market in 2026?

The anti-money laundering solutions market size is estimated at USD 4.05 billion in 2026.

What is the projected CAGR for anti-money laundering solutions from 2026 to 2031?

The market is forecast to register an 18.01% CAGR during the 2026-2031 period.

Which solution segment will grow the fastest through 2031?

Trade-based analytics is projected to expand at an 18.91% CAGR, outpacing all other solution segments.

Why are small and medium-sized enterprises adopting anti-money laundering platforms?

New regulations now compel advisers, crowdfunding portals, and similar SMEs to monitor transactions, and SaaS pricing lets them comply without large in-house teams.

Which region will see the highest growth in anti-money laundering spending?

Asia-Pacific is forecast to grow at 19.31% through 2031, propelled by virtual-asset licensing and instant-payment adoption.

How are vendors using artificial intelligence in anti-money laundering systems?

Providers embed agentic AI that drafts investigation narratives, surfaces cross-bank risk signals, and retrains models continuously to cut false positives and investigation times.