Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

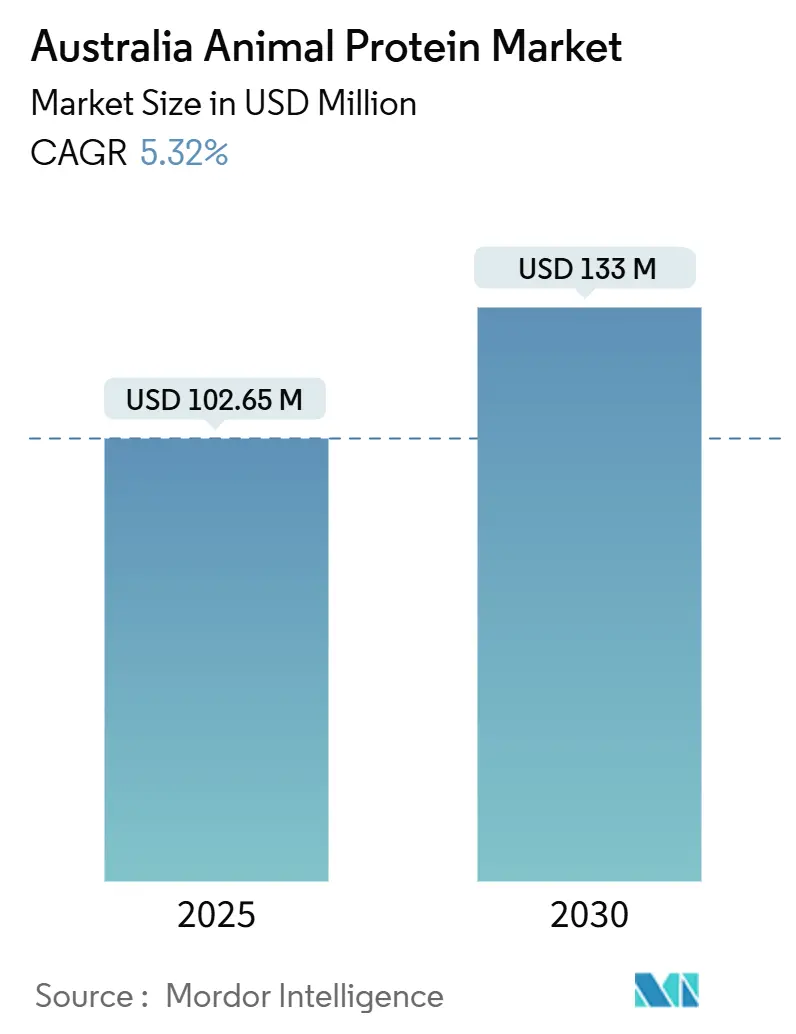

| Market Size (2025) | USD 102.65 Million |

| Market Size (2030) | USD 133 Million |

| Growth Rate (2025 - 2030) | 5.32% CAGR |

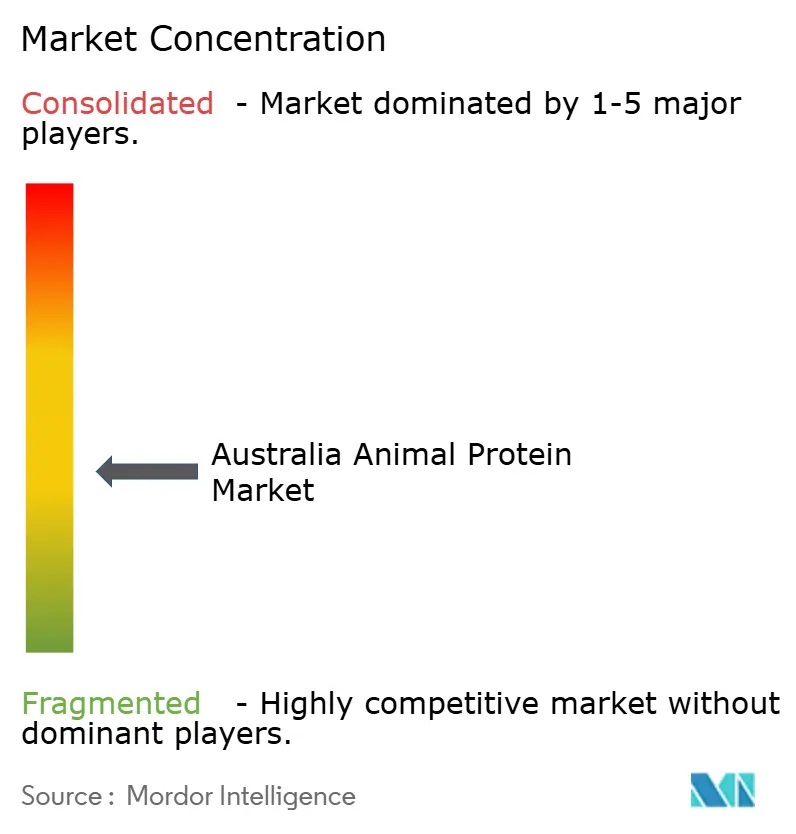

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Australia Animal Protein Market Analysis by Mordor Intelligence

The Australia animal protein market is valued at USD 102.65 million in 2025 and is projected to reach USD 133.0 million by 2030, growing at a CAGR of 5.32% during the forecast period. The market shows sustained growth driven by domestic demand for premium dairy and meat proteins, along with increasing export opportunities to Asia, despite reduced national milk output and limited livestock availability. The decline in average milk production per farm has impacted market dynamics and supply chain operations across the country. Production decreased primarily due to floods and adverse weather conditions that affected farming operations and feed quality, creating operational challenges for farmers and reducing their productivity and profitability. The market is expanding through the adoption of precision fermentation, insect protein, and collagen extraction technologies, establishing new revenue streams beyond conventional segments and reducing reliance on plant-based alternatives. These technologies enhance protein production by offering sustainable options while maintaining the nutritional benefits consumers expect from animal proteins, as the industry responds to changing consumer preferences and environmental standards.

Key Report Takeaways

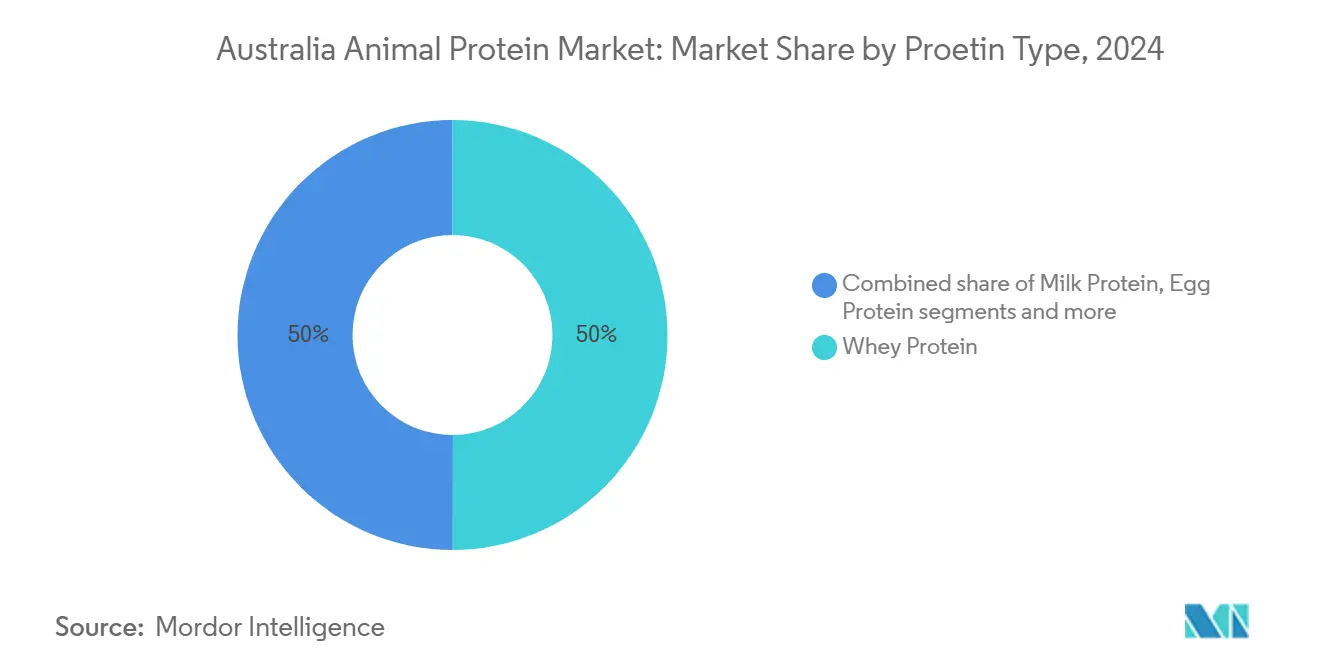

- By protein type, whey protein dominated the market with a 49.98% revenue share in 2024, while the casein and caseinates segment is expected to grow at a 6.24% CAGR through 2030.

- By form, protein concentrates held 34.98% of the Australia animal protein market share in 2024. The hydrolyzed segment is projected to grow at a 6.85% CAGR through 2030.

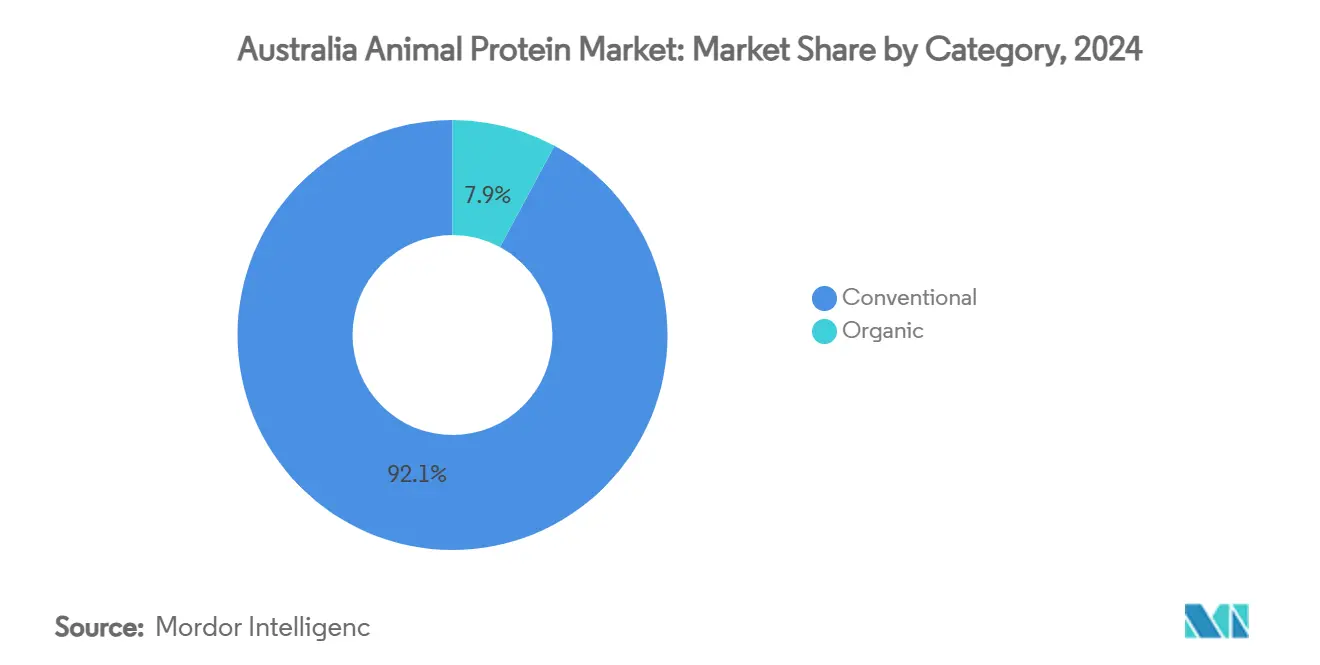

- By category, conventional products commanded 92.14% of the Australia animal protein market size in 2024. The organic segment is anticipated to grow at a 7.18% CAGR through 2030.

- By application, supplements captured 49.94% of revenue share in 2024. The personal care and cosmetics segment is growing at a 6.58% CAGR through 2030.

Australia Animal Protein Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing fitness culture driving protein demand | +1.20% | National, with concentration in urban centers | Medium term (2-4 years) |

| Rising demand for functional dairy proteins in sports nutrition manufacturing | +0.90% | National, with export potential to Asia-Pacific | Medium term (2-4 years) |

| Innovation in insect protein for aquaculture feed reducing reliance on fishmeal | +0.70% | National, with focus on Tasmania and SA aquaculture regions | Long term (≥ 4 years) |

| Premiumization trend in pet food elevating animal protein inclusion rates | +0.80% | National, with premium segments in major cities | Short term (≤ 2 years) |

| Growing popularity of protein-based convenience foods | +0.60% | National, with retail distribution focus | Short term (≤ 2 years) |

| Rising use in functional and fortified food items | +0.50% | National, with focus on health-conscious demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing fitness culture driving protein demand

Australia's fitness industry is experiencing significant growth, with strength training becoming increasingly popular across different age groups, driving the demand for animal-based proteins. According to The Australian Sports Commission (ASC), in the 2023 financial year, 50.2% of Australians aged 18-24 and 48% of those aged 25-35 utilized gyms, fitness clubs, or sports and leisure centers[1] Source: Australian Sports Commission (ASC), "AusPlay survey results July 2022 - June 2023", ausport.gov.au . The active nutrition market encompasses protein powders and performance supplements, including pre-workout formulas, amino acids, creatine, and other sports nutrition products designed for athletic performance and recovery. The market continues to expand through product development. In May 2024, the Commonwealth Scientific and Industrial Research Organisation (CSIRO) launched "Just Meat," a red meat protein powder, in Australia[2]Source: Commonwealth Scientific and Industrial Research Organisation, "Meat you at the gym: A nutritious new protein powder", csiro.au . This product transforms red meat into a nutrient-rich, allergen-free protein supplement suitable for protein balls, shakes, and energy drinks. The powder retains red meat's complete amino acid profile while offering enhanced digestibility and versatility. The product addresses consumer demand for natural, minimally processed protein sources that maintain whole foods' nutritional value. Market growth is further supported by increased protein supplementation among GLP-1 medication users seeking to maintain lean mass during calorie restriction. The Australian sports nutrition market has evolved through product innovation, with manufacturers focusing on clean-label formulations, sustainable sourcing practices, and improved bioavailability to align with consumer preferences.

Rising demand for functional dairy proteins in sports nutrition manufacturing

The demand for functional dairy proteins is increasing as sports nutrition manufacturers emphasize bioavailability and complete amino acid profiles in their formulations. This growth is driven by consumers' enhanced understanding of protein quality and its role in athletic performance and recovery. Fonterra's strategic investments in September 2024, including a new protein plant at Studholme and a USD 150 million cool store expansion at Whareroa, indicate the expected long-term demand for functional dairy ingredients. These investments aim to boost production capacity and meet the increasing global demand for specialized dairy protein ingredients. In July 2024, Fonterra partnered with Nourish Ingredients to develop precision fermentation-based fats for dairy applications. This collaboration focuses on creating sustainable and nutritionally optimized dairy alternatives while maintaining the functional properties of traditional dairy proteins. The rising costs of whey protein isolate have driven innovation in alternative processing methods and hybrid protein formulations that maintain performance characteristics while managing costs. Companies are exploring membrane filtration technologies and enzyme treatments to improve protein yield and functionality. The price variations create opportunities for Australian manufacturers to develop efficient, high-performance protein solutions that compete with imports while supporting local dairy farmers. These manufacturers are investing in research and development to enhance protein extraction processes and create value-added products for domestic and international markets.

Innovation in insect protein for aquaculture feed reducing reliance on fishmeal

Australian companies are advancing insect protein production for aquaculture feed through innovative technologies and strategic partnerships. For instance, in May 2025, Goterra completed its first large-scale insect protein rendering trial, producing insect meal with more than 70% protein and approximately 12% fat, exceeding industry requirements. This achievement follows the company's partnership with Skretting Australia in 2024 to incorporate insect protein meal into aquaculture feed. This collaboration demonstrates the growing potential of insect-based protein solutions in the aquaculture industry. Bardee operates Australia's largest insect breeding facility, using advanced vertical farming systems to convert food waste into certified organic fertilizers and animal protein. The company has achieved a significant milestone by becoming the first industrial insect breeding operation globally to generate carbon credits through food waste diversion, highlighting the environmental benefits of insect farming.

Premiumization trend in pet food elevating animal protein inclusion rates

The increasing consumer preference for premium pet food products is driving higher animal protein content in formulations, as pet owners prioritize nutritional quality and ingredient transparency. This aligns with the broader shift toward enhanced pet nutrition and wellness products. Australia's significant pet ownership contributes to market expansion, with Animal Health Victoria data showing 58% of Victorian adults owned pets in 2023, predominantly dogs[3]Source: Animal Welfare Victoria, "Victorian pet census", agriculture.vic.gov.au. The growing pet population has increased the demand for premium pet food across distribution channels, including specialty pet stores and veterinary clinics. Market consolidation is evident through transactions such as Colgate-Palmolive's acquisition of Prime100 for its Hill's Pet Nutrition division in February 2025. This acquisition focuses on the expanding fresh pet food segment, as Prime100 provides veterinarian-endorsed, premium products that meet the market demand for high-protein, minimally processed formulations. The expanding Australian pet food market and increasing protein content requirements create sustained demand for quality animal proteins in pet food manufacturing. Australian producers utilize their access to premium protein sources and robust quality assurance systems to pursue export opportunities in Asian markets, where pet ownership and related spending continue to grow.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating shift toward plant-based alternatives | -1.4% | National, with higher impact in urban areas | Medium term (2-4 years) |

| Stringent biosecurity and traceability regulations increasing compliance costs | -0.8% | National, with particular impact on exporters | Short term (≤ 2 years) |

| Ethical and environmental concerns over intensive animal farming practices | -0.6% | National, with focus on millennial and Gen Z consumers | Long term (≥ 4 years) |

| Stringent animal welfare regulations | -0.4% | National, with emphasis on livestock and poultry sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating shift toward plant-based alternatives

Plant-based protein alternatives are gaining market share as consumers prioritize environmental sustainability and health considerations in their protein choices. In 2023, four of Australia's six state governments implemented initiatives to strengthen their local alternative protein industries through targeted public investments supporting farmers and food producers. The Western Australian government allocated AUD 5 million to support the construction of a factory producing oat milk enriched with lupin protein from locally-grown crops[4]Source: Good Food Institute, "Public investment in alternative proteins to feed a growing world", gfi.org. While consumer acceptance of flexitarian and plant-based diets is increasing, significant resistance remains toward full adoption of alternative proteins due to concerns about taste, texture, and potential health risks. Additionally, manufacturers continue to develop innovative plant protein products, impacting traditional animal protein market growth. For example, in May 2024, NiHTEK launched NiHPRO, a hydrolyzed protein isolate targeting consumers seeking alternatives to whey protein isolate due to lactose intolerance, demonstrating market demand for dairy-free alternatives that maintain performance characteristics. Animal protein producers face the challenge of addressing consumer concerns regarding processing methods, environmental impact, and ethical sourcing while maintaining competitive pricing against increasingly sophisticated plant-based alternatives.

Stringent biosecurity and traceability regulations increasing compliance costs

Australia's biosecurity framework increases operational costs for animal protein producers through mandatory traceability systems and regulatory compliance requirements. The framework requires extensive documentation, regular audits, and implementation of specialized tracking software. The Australian government's USD 100 million investment in agricultural traceability systems as a part of the National Agricultural Traceability Strategy 2023-2033 imposes compliance requirements on industry participants while improving market access and food safety[5]Source: Department of Agriculture, Fisheries and Forestry, "National traceability", agriculture.gov.au.The strategy encompasses digital tracking systems, enhanced surveillance measures, and stringent reporting protocols. Moreover, the Approved Arrangements Management Product (AAMP) system requires biosecurity industry participants to manage arrangements through self-service platforms, increasing administrative tasks while streamlining processes. The system demands regular updates, detailed record-keeping, and continuous monitoring of compliance status. These regulations benefit larger companies with sufficient capital to manage compliance costs but may create entry barriers for smaller producers and new market participants, particularly in terms of technology investment and staffing requirements.

Segment Analysis

By Protein Type: Whey’s Scale Endures as Casein Accelerates

Whey protein maintains a 49.98% share of the Australia animal protein market, supported by established filtration infrastructure, proven clinical research, and consumer recognition of its rapid absorption properties. Casein and caseinates are expected to grow at a 6.24% CAGR through 2030, driven by increased demand for slow-digesting proteins in night-time recovery products and infant formula. This growth is supported by All G's development of precision-fermented human casein micelles in May 2025. Collagen products derived from beef hides are expanding into gummies, beverages, and topical applications, creating value from processing by-products while enhancing meat processing economics. While insect protein represents a small market volume, it maintains premium pricing and attracts significant attention, positioning it as a long-term diversification opportunity.

Australian manufacturers with multi-protein production capabilities in a single facility protect against market fluctuations and expand their customer reach. The adaptable nature of microfiltration and spray-drying equipment enables efficient transitions between whey, casein, and collagen production, optimizing facility utilization throughout the year. Emerging companies can access established processing facilities through partnerships, reducing initial capital requirements for new protein development. These operational advantages help maintain stable revenue across the Australian animal protein market as consumer preferences shift.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Form: Concentrates Dominate While Hydrolyzed Solutions Surge

Whey protein concentrates maintain a 34.98% market share in 2024 due to their cost-effective processing, sufficient protein purity, and compatibility with bakery, beverage, and confectionery applications. Hydrolyzed whey proteins are expected to grow at a 6.85% CAGR through 2030, driven by their rapid absorption properties that appeal to sports nutrition, clinical nutrition, and senior nutrition manufacturers seeking low-lactose and low-allergen solutions. Whey protein isolates maintain their premium position with protein purity exceeding 90% and the highest unit prices, with growth driven by elite sports nutrition and bariatric care applications.

Enhanced enzymatic hydrolysis techniques improve flavor profiles and solubility, addressing previous challenges with bitterness and expanding market acceptance. The combination of inline chromatography and membrane filtration technology produces higher-quality isolates with improved yields, maintaining profit margins despite increased electricity costs. Processors located in renewable energy zones reduce energy expenses, strengthening their competitive position in the Australian animal protein market.

By Category: Conventional Volume Rules as Organic Premium Rises

Conventional category accounts for 92.14% of market share as of 2024, supported by an extensive feed-grain supply chain, established quality assurance protocols, and widespread retailer acceptance. The conventional segment benefits from decades of infrastructure investment, standardized production processes, and economies of scale that enable competitive pricing. Organic protein is projected to grow at 7.18% CAGR through 2030. This growth is driven by price premiums and consumer confidence in certification labels. Consumer demand for organic products continues to increase due to environmental sustainability awareness, animal welfare concerns, and perceived health benefits.

Suppliers in the Australian animal protein market differentiate their products through multiple certification programs. Animal welfare certifications ensure humane treatment throughout the livestock lifecycle, from breeding to processing. Regenerative grazing practices focus on soil health, biodiversity, and sustainable land management techniques. Carbon-neutral claims demonstrate a commitment to reducing greenhouse gas emissions across operations. These certifications require substantial investments in various areas. Companies must implement comprehensive auditing processes to verify compliance with certification standards. Documentation systems track and maintain detailed records of farming practices, animal treatment protocols, and environmental impact measurements. Supply chain transparency initiatives involve monitoring and reporting mechanisms from farm to retail, enabling suppliers to maintain premium market positions and meet consumer demands for verified sustainability claims.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Supplements Lead, Personal Care Unlocks New Demand

Supplements generate 49.94% of revenue in the Australian animal protein market, driven by established gym culture, e-commerce growth, and medically-recommended nutrition protocols. While sports and performance powders remain dominant, the introduction of ready-to-drink products and collagen chews has expanded market reach across age groups. The personal care and cosmetics segment is expected to grow at 6.58% CAGR, as beauty supplements gain prominence in pharmacies, supported by research demonstrating the benefits of collagen peptides for skin health.

The animal feed segment incorporates Black Soldier Fly meal, poultry by-products, and milk replacer proteins in livestock, aquaculture, and pet food applications to enhance sustainability. Food and beverage manufacturers continue to expand their protein-enriched product lines, including yogurts, breads, and ready meals for convenience-seeking consumers. The infant nutrition sector focuses on fermented human proteins that replicate breast milk properties, targeting premium export markets through traditional formula formats. The elderly nutrition segment utilizes hydrolyzed beef and milk peptides to address muscle loss, establishing consistent supply arrangements with aged-care facilities. These varied market applications provide stable demand for protein suppliers in Australia.

Competitive Landscape

The market structure is moderately fragmented, creating opportunities for both established companies and new entrants to gain market share. Key market players include Fonterra Co-operative Group Limited, Saputo Inc., Groupe Lactalis, Kerry Group plc, and Glanbia PLC. The increasing demand for animal protein, driven by its nutritional value and caloric content, has prompted market players to develop innovative products. Companies are implementing expansion strategies through mergers, acquisitions, and partnerships.

Australian companies are establishing market positions through specialized technologies and distribution strategies. Companies are implementing diverse distribution approaches, including chilled logistics, e-commerce platforms, and veterinary endorsements for insect-protein snacks.

Supplement manufacturers form partnerships with toll spray-dryers to reduce capital expenditure. Companies that demonstrate low-carbon operations and blockchain traceability receive premium pricing from Japanese and Korean retailers. This market environment has established digital traceability systems and renewable energy investments as priorities for Australian animal protein companies.

Australia Animal Protein Industry Leaders

-

Fonterra Co-operative Group Limited

-

Saputo Inc.

-

Groupe Lactalis

-

Kerry Group plc

-

Glanbia PLC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Arla Foods Ingredients and Alchemy Agencies established a distribution partnership to serve the animal proteins for the performance nutrition market in Australia, New Zealand, and the Pacific Islands. The agreement focuses on Australia and New Zealand (ANZ) markets.

- May 2025: Australia-based Goterra had completed its first large-scale insect protein rendering trial, producing insect meal with more than 70% protein and approximately 12% fat, exceeding industry requirements. This achievement is gained by the company's partnership with Skretting Australia in 2024 to incorporate insect protein meal into aquaculture feed.

- March 2025: FrieslandCampina Ingredients introduced Nutri Whey ProHeat, a heat-stable whey protein solution, to the active nutrition segment of the nutraceutical market. The whey protein ingredient, designed for ready-to-drink (RTD) functional beverages, undergoes microparticulation to maintain its consistency when heated.

- February 2024: Cauldron has obtained regulatory approval from the Office of the Gene Technology Regulator (OGTR) to conduct production trials of animal protein ingredients in batches up to 10,000 litres. Under the DIR200 license, Cauldron can utilize its precision fermentation technology and Pichia Pastoris yeast to produce dairy, egg, and spider-silk proteins.

Australia Animal Protein Market Report Scope

Animal protein is extracted from animals or animal products like milk, eggs, and others.

The Australian animal protein market is fragmented by type into casein and caseinates, collagen, egg protein, gelatin, insect protein, milk protein, and whey protein. The market is segmented by application into animal feed, personal care and cosmetics, food and beverages, and supplements.

The market sizing has been done in value terms in USD and volume terms for all the abovementioned segments.

By Protein Type

| Casein and Caseinates |

| Collagen |

| Egg Protein |

| Gelatin |

| Insect Protein |

| Milk Protein |

| Whey Protein |

| Other Animal Protein |

By Form

| Isolates |

| Concentrates |

| Hydrolyzed |

| Marine Based |

| Animal Based |

| Others |

By Category

| Conventional |

| Organic |

By Application

| Animal Feed | |

| Personal Care and Cosmetics | |

| Food and Beverages | Bakery |

| Beverages | |

| Breakfast Cereals | |

| Condiments/Sauces | |

| Confectionery | |

| Dairy and Dairy Alternative Products | |

| RTE/RTC Food Products | |

| Snacks | |

| Supplements | Baby Food and Infant Formula |

| Elderly and Medical Nutrition | |

| Sports/Performance Nutrition |

| By Protein Type | Casein and Caseinates | |

| Collagen | ||

| Egg Protein | ||

| Gelatin | ||

| Insect Protein | ||

| Milk Protein | ||

| Whey Protein | ||

| Other Animal Protein | ||

| By Form | Isolates | |

| Concentrates | ||

| Hydrolyzed | ||

| Marine Based | ||

| Animal Based | ||

| Others | ||

| By Category | Conventional | |

| Organic | ||

| By Application | Animal Feed | |

| Personal Care and Cosmetics | ||

| Food and Beverages | Bakery | |

| Beverages | ||

| Breakfast Cereals | ||

| Condiments/Sauces | ||

| Confectionery | ||

| Dairy and Dairy Alternative Products | ||

| RTE/RTC Food Products | ||

| Snacks | ||

| Supplements | Baby Food and Infant Formula | |

| Elderly and Medical Nutrition | ||

| Sports/Performance Nutrition | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the Australia animal protein market?

The market is worth USD 102.65 million in 2025 and is set to grow to USD 133.0 million by 2030.

Which protein type dominates revenue?

Whey protein leads with 49.98% market share in 2024, supported by extensive manufacturing infrastructure and sports-nutrition demand.

Which segment is expanding the fastest?

Casein and caseinates are projected to grow at 6.24% CAGR through 2030, driven by infant-formula and slow-release applications.

Why are insect proteins gaining traction?

Partnerships such as Goterra-Skretting show insect meal can replace fishmeal, improving sustainability in aquaculture and pet food.

Page last updated on: