Saudi Arabia Agriculture Market Analysis by Mordor Intelligence

The Saudi Arabia Agriculture Market size is estimated at USD 15.20 billion in 2026 and is anticipated to reach USD 20.30 billion by 2031, at a CAGR of 5.96% during the forecast period. Continued investment in desalination-fed irrigation, controlled-environment agriculture, and salt-tolerant crop genetics is reshaping production economics, supporting steady gains in domestic fruit, vegetable, dairy, and poultry output. Vision 2030 subsidies covering up to 60% of capital costs have triggered rapid greenhouse expansion, while agrivoltaic pilots deliver dual revenue streams that improve farm cash flow and water-use efficiency. Import costs for cereals and off-season produce still create exposure to Red Sea and Black Sea disruptions, yet treated-wastewater mandates and feed-in tariffs for on-farm solar power strengthen resilience. Private and sovereign capital is shifting toward vertically integrated agritech parks in Tabuk and Al-Jouf, giving the Saudi Arabian agricultural commodity market clear momentum toward food-sovereignty targets.

Key Report Takeaways

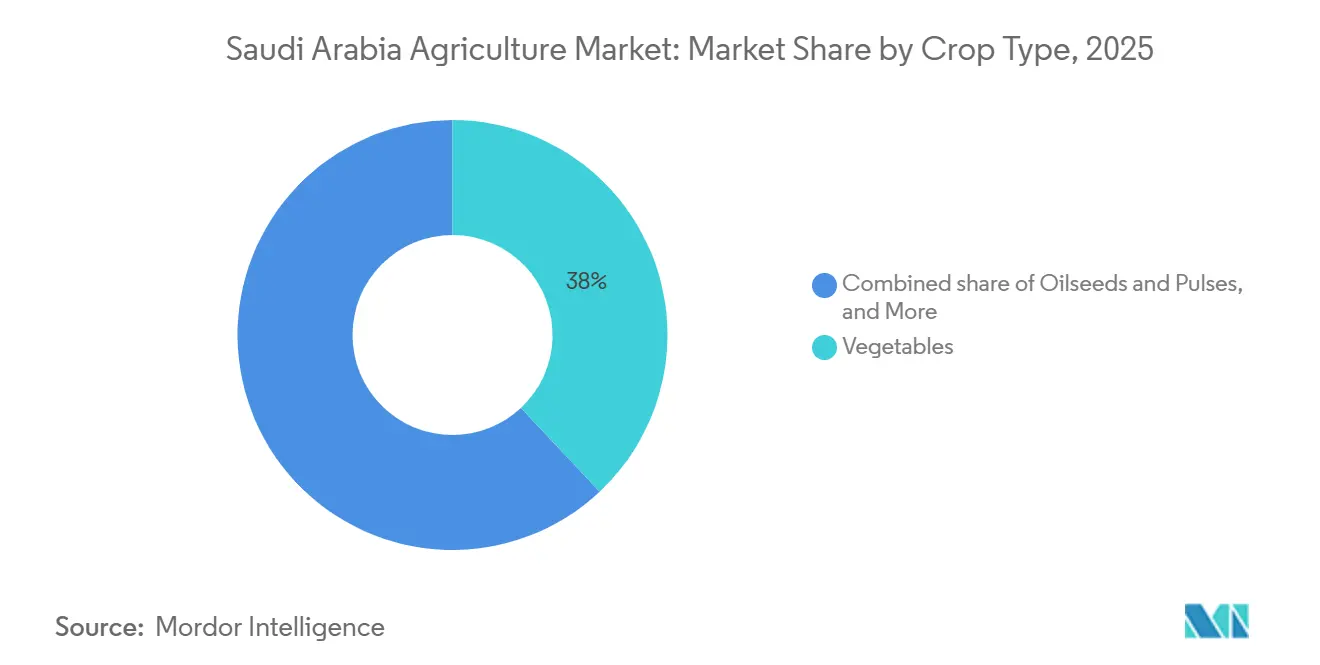

- By crop type, vegetables led with 38% of Saudi Arabia's agriculture market share in 2025, while oilseeds and pulses segment emerges as the fastest-growing crop category with a 10.2% CAGR forecast through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Agriculture Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Vision-2030 subsidies and grants | +1.8% | National, with concentration in Al-Jouf, Tabuk, Hail provinces | Medium term (2-4 years) |

| Food-security imperative amid import dependence | +1.5% | National, with strategic focus on major consumption centers | Long term (≥ 4 years) |

| Precision and greenhouse tech adoption | +1.2% | National, with early adoption in Northern provinces | Medium term (2-4 years) |

| National water-efficiency programs | +0.9% | National, with priority in water-stressed regions | Long term (≥ 4 years) |

| Solar-powered agrivoltaics in desert farms | +0.4% | Regional, focused on high solar irradiance areas | Long term (≥ 4 years) |

| Salt-tolerant date-palm breeding success | +0.2% | Regional, concentrated in traditional date-growing oases | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Vision-2030 Subsidies and Grants

Vision 2030's agricultural financing programs are reshaping capital allocation patterns across the Kingdom's farming sector through unprecedented government support mechanisms. The Agricultural Development Fund provides up to 75% financing for greenhouse projects and modern irrigation systems, with tax holidays extending up to 10 years for qualifying agritech investments [1]Source: Saudi Vision 2030, “Vision 2030 Programs,” Vision2030.gov.sa . This financial backing has catalyzed a surge in controlled-environment agriculture, with companies like Topian (NEOM subsidiary) opening a 4-hectare climate-resilient greenhouse facility in Oxagon during 2025, marking the Kingdom's largest single investment in precision horticulture to date. The subsidy structure particularly favors water-efficient technologies, creating market incentives that align private sector returns with national water conservation objectives.

Food-Security Imperative Amid Import Dependence

Saudi Arabia's strategic push to reduce food import dependency has intensified following supply chain disruptions during the COVID-19 pandemic and geopolitical tensions affecting global trade routes. The Kingdom currently imports approximately 90-95% of its edible oil requirements and significant portions of its fresh produce, creating vulnerability to external price shocks and supply disruptions. Government mandates now require major food companies to demonstrate domestic sourcing capabilities, with SALIC launching National Grain Supply Company (SABIL) in April 2025 to manage strategic grain storage and procurement operations across 14 silo branches with combined capacity exceeding 2.7 million metric tons. This policy framework is driving vertical integration strategies among agricultural companies, as domestic production capacity becomes a competitive differentiator in government contract bidding processes.

Precision and Greenhouse Tech Adoption

Internet of Things sensors and automated climate control systems are transforming agricultural productivity metrics across Saudi Arabia's controlled-environment facilities. Research partnerships between domestic companies and South Korean technology providers have resulted in smart agriculture systems that integrate soil moisture sensors, weather monitoring, and automated irrigation controls to optimize resource utilization. Companies like FarmERP expanded into Saudi Arabia through partnerships with local technology integrator Seiyaj Tech in August 2024, providing cloud-based farm management platforms that enable real-time monitoring of crop health, irrigation schedules, and harvest timing across multiple cultivation sites.

National Water-Efficiency Programs

The National Water Strategy's emphasis on agricultural water conservation is driving systematic adoption of drip irrigation and micro-sprinkler systems that reduce water consumption by up to 40% compared to traditional flood irrigation methods. Government-funded infrastructure projects include the construction of advanced desalination facilities specifically designed for agricultural use, with King Abdullah University of Science and Technology (KAUST) researchers developing custom desalination technologies that produce irrigation-quality water at lower energy costs than conventional seawater treatment plants. The program's impact extends beyond water savings to soil health improvement, as precision irrigation reduces salt accumulation in agricultural soils and enables cultivation in previously marginal lands.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extreme aridity and groundwater depletion | -1.1% | National, with severe impact in central and eastern regions | Long term (≥ 4 years) |

| High capex for modern farming systems | -0.8% | National, with disproportionate impact on SME (Saudi Small and Medium-sized Enterprises) farmers | Medium term (2-4 years) |

| Soil-salinity spikes from brine return flows | -0.5% | Regional, concentrated near desalination facilities | Medium term (2-4 years) |

| Cold-chain and remote-logistics gaps | -0.4% | National, with acute challenges in rural production areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Extreme Aridity and Groundwater Depletion

Saudi Arabia's agricultural expansion faces fundamental water resource constraints as fossil aquifers decline at accelerating rates across major production regions. The Kingdom's non-renewable groundwater reserves are dropping by an average of 0.6 meters annually, with some agricultural areas experiencing depletion rates exceeding 1 meter per year [2]Source: World Bank, “Saudi Arabia Water Data,” worldbank.org. This hydrological challenge forces agricultural operators to invest in increasingly expensive water extraction equipment and deeper well drilling, driving up operational costs and threatening the economic viability of water-intensive crops. The situation is particularly acute in the Eastern Province and central regions, where traditional agricultural areas are experiencing well failures and declining water quality as aquifer levels drop below economically extractable depths.

High Capex for Modern Farming Systems

Greenhouse construction costs in Saudi Arabia exceed USD 1.2 million per hectare for advanced climate-controlled facilities, creating significant barriers to entry for small and medium-scale agricultural enterprises. The capital intensity of modern farming systems reflects the specialized equipment requirements for desert agriculture, including advanced cooling systems, automated irrigation networks, and soil-less growing media that can withstand extreme temperature variations. The high upfront investment requirements are concentrating market participation among well-capitalized corporate entities and government-backed development companies.

Segment Analysis

By Crop Type: Oilseeds Drive Import Substitution Strategy

Vegetables maintain the largest market share at 38% in 2025, driven by controlled-environment agriculture that enables year-round production of tomatoes, cucumbers, and peppers despite extreme seasonal temperature variations. Growing vegetable output shortens import lines, trimming freight-driven carbon footprints in the Saudi Arabia agriculture market. Controlled environments stabilize supply in Ramadan and Hajj seasons when demand spikes.

The oilseeds and pulses segment emerges as the fastest-growing crop category with a 10.2% CAGR forecast through 2031, reflecting Saudi Arabia's strategic imperative to reduce import dependency for protein-rich crops and cooking oils that currently account for over 90% of domestic consumption. Government incentives specifically target oilseed cultivation through subsidized land allocation and water access programs, with the Ministry of Environment, Water, and Agriculture prioritizing sunflower and soybean production in northern provinces where climate conditions support these temperate crops.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Saudi Arabia's agricultural market concentrates in the northern provinces of Al-Jouf, Tabuk, and Hail, which collectively account for the majority of the Kingdom's fresh produce output due to their relatively moderate climate conditions and groundwater availability. Al-Jouf Province has emerged as the primary agricultural hub, hosting major processing facilities, including Al-Jouf Agricultural Development Company's French-fries processing plant that opened in May 2024 with the capacity to serve both domestic and export markets [3]Source: Al-Jouf Agricultural Development Company, “New Processing Plant Launch,” .

The Eastern Province plays a strategic role in agricultural logistics and processing, with major companies like ARASCO (Arabian Agricultural Services Company) operating feed production facilities and Almarai maintaining large-scale dairy operations that support the livestock sector. The NEOM region in the northwest is developing into a showcase for advanced agricultural technologies, with Topian's 4-hectare climate-resilient greenhouse facility representing the largest single investment in precision horticulture within the Kingdom.

Central and southern regions face greater agricultural challenges due to extreme aridity and limited groundwater resources, though specialized crops like dates continue to thrive in traditional oasis systems. The government's National Water Strategy prioritizes these regions for advanced desalination infrastructure and water-efficient irrigation technologies that could unlock additional agricultural potential. Recent investments in cold-chain logistics infrastructure, including the development of 59 logistics centers by 2030 under the Saudi logistics master plan, are improving market access for producers in remote areas and reducing post-harvest losses that previously constrained profitability in marginal production zones.

Competitive Landscape

The Saudi Arabian agricultural commodity market features moderate fragmentation, the top five firms held sigificant share of 2025 revenue. Almarai leads dairy and poultry through full vertical integration that spans fodder farms in Argentina and 58,000 retail outlets across the Gulf, driving scale efficiencies and brand reach. Nadec follows with diversified dairy and produce lines supplied by thousands of head of cattle and several hectares of crops. Tabuk Agricultural Development Company leverages 22,000 hectares of irrigated land to export potatoes, onions, and greenhouse vegetables, maintaining stable cash flow even after the wheat ban.

Disruptive entrants include Pure Harvest Smart Farms, which deployed AI-driven climate algorithms that cut energy 19% and achieved 95% delivery accuracy. Red Sea Farms introduced seawater-cooled greenhouses that slash freshwater use 90%, broadening technology options for arid-zone horticulture. Patent filings in gene editing surged to 142 in 2024, with King Abdulaziz City for Science and Technology and King Abdullah University of Science and Technology leading breakthroughs in salt tolerance. These innovations pressure incumbents to accelerate R&D or partner with startups.

Investment momentum favors large-scale, desert-adjacent greenhouse estates that pair solar power with desalination. Public Investment Fund backing lowers cost of capital and unlocks globally competitive produce pricing. Smallholders gain by joining cooperatives that aggregate demand for inputs and market output, but high technology entry costs keep them reliant on subsidies. Overall, the Saudi Arabian agricultural commodity market exhibits a blend of state intervention and private entrepreneurship that promotes consolidation and modernization simultaneously.

Recent Industry Developments

- May 2025: The Saudi-Chinese Forum signed 57 agreements worth USD 3.7 billion (SAR 14 billion) covering water recycling, agri-tech, and a dedicated smart-food-security city. The scope and volume of agreements reaffirm China’s status as Saudi Arabia’s largest trading partner, accounting for 18 percent of the Kingdom’s foreign trade, and align directly with Saudi Arabia’s Vision 2030 and China’s Belt and Road Initiative (BRI).

- April 2025: Brasil Foods S.A. committed USD 160 million to a Jeddah poultry plant in partnership with Halal Products Development Company, targeting 40,000 metric tons annual capacity. The facility will have an annual capacity of approximately 40,000 metric tons and is anticipated to begin operations in mid-2026, initially serving the Saudi market but with potential for regional exports.

- March 2025: Hilton Foods and NADEC (National Agricultural Development Company) formed a joint venture to expand value-added protein offerings. The partnership, initially a 10-year collaboration, combines Hilton Foods' expertise in processing and packaging with NADEC's local cattle operations, with NADEC holding a 51% stake and Hilton Foods a 49% stake.

- July 2024: FarmERP partnered with Seiyaj Tech to deliver ERP systems to Saudi farms, improving traceability and cost control. This collaboration leverages Seiyaj Tech's local market expertise and FarmERP's advanced, AI-powered platform to address the specific challenges of agriculture in Saudi Arabia, such as water scarcity and extreme weather.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Saudi Arabian agriculture market as the total annual farm-gate value of field-grown and protected crops, including cereals, fruits, vegetables, oilseeds, and pulses, harvested within the Kingdom's borders. Value is expressed in constant 2024 US dollars after converting Saudi riyal receipts at the average central-bank rate.

Scope exclusion: Livestock, aquaculture, forestry products, agro-inputs, and post-farm processing activities are excluded.

Segmentation Overview

- By Crop Type

- Cereals and Grains

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Fruits

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Vegetables

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Oilseeds and Pulses

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Cereals and Grains

Detailed Research Methodology and Data Validation

Primary Research

Multiple touchpoints with growers, hydroponic solution integrators, export inspectors, and cooperative officials across Riyadh, Al-Qassim, and Tabuk let us validate harvested volumes, typical farm-gate prices, water-tariff impacts, and technology adoption rates that secondary sources only hint at.

Desk Research

Mordor analysts first map the production base using publicly available tier-1 datasets such as FAOSTAT, the Ministry of Environment Water & Agriculture statistical yearbooks, GaStat crop surveys, UN Comtrade shipment data, and International Grains Council acreage reports. Company filings, local press releases, and parliament briefing papers help us trace subsidy flows and private greenhouse capacity. Paid repositories, chiefly D&B Hoovers for grower revenues and Dow Jones Factiva for deal tracking, add firm-level depth. These are illustrative rather than exhaustive; many other authoritative sources are tapped during data collection and cross-checks.

Market-Sizing & Forecasting

We begin with a top-down reconstruction. Official production in metric tons is multiplied by region-specific farm-gate averages, imports and carry-over stocks are netted, and the resulting pool is valued to establish 2024 baseline demand. Selective bottom-up roll-ups, sampled greenhouse hectares multiplied by yield norms and channel checks on key traders, act as a reasonableness filter before final calibration. Variables tracked include irrigated acreage, desalinated-water allocation, protected-farm footprint, average tomato and date yields, consumer per-capita produce intake, and subsidy intensity. Future values are projected through multivariate regression blended with ARIMA to capture both structural drivers, such as Vision 2030 investments, and seasonal shocks, with scenario ranges refined in expert workshops.

Data Validation & Update Cycle

Outputs pass anomaly and variance screens, peer review, and a senior analyst sign-off. We refresh the model every twelve months, re-opening it sooner if drought events, tariff shifts, or major subsidy announcements move the market.

Credibility Anchor: Why Mordor's Saudi Arabia Agriculture Baseline Stands Up to Scrutiny

Published figures often diverge because studies follow different scopes, price points, and refresh cadences.

Key gap drivers include whether livestock and agro-inputs are bundled, the choice of retail versus farm-gate valuation, reliance on legacy FAO averages without local surveys, and currency conversion timing.

By focusing strictly on harvested crop value and reconciling top-down statistics with bottom-up grower evidence each year, Mordor Intelligence supplies a balanced, decision-ready baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 15.20 B (2025) | Mordor Intelligence | - |

| USD 130 B (2024) | Global Consultancy A | Bundles livestock, forestry, and fertilizer sales; GDP ratio method, no farm-gate price testing |

| USD 14.8 B (2024) | International Publisher B | Uses historic FAO yield tables only; limited 2024 field survey; no import-export reconciliation |

| USD 18.77 B (2025) | Regional Consultancy C | Values retail turnover and processing output; excludes on-farm waste adjustments |

Taken together, the comparison shows that our disciplined scope selection, annual primary validation, and dual-pass modeling give decision-makers a transparent, reproducible baseline they can trust.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large will Saudi Arabia agriculture sector be by 2030?

The Saudi Arabia agriculture market size is forecast to hit USD 20.30 billion by 2031, up from USD 15.20 billion in 2026.

Which crop dominates fresh-produce output?

Vegetables hold the largest share at 38% of 2025 value owing to high-yield greenhouse tomatoes and expanding leafy-green production.

How is Vision 2030 influencing farm investment?

Vision 2030 provides up to 75% project financing and 10-year tax holidays for water-efficient greenhouses, accelerating tech adoption.

Which regions produce most of Saudi Arabia fresh produce?

Al-Jouf, Tabuk, and Hail provinces supply about 65% of national output due to favorable microclimates and targeted infrastructure upgrades.