Zinc Methionine Chelates Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

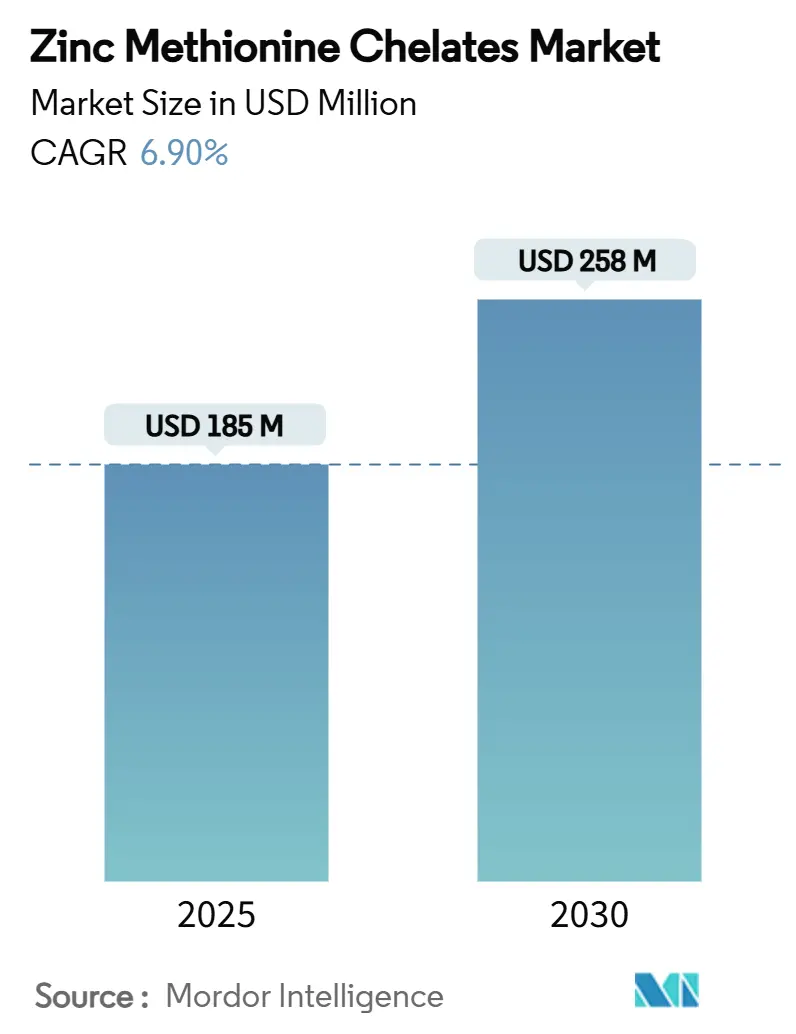

| Market Size (2025) | USD 185 Million |

| Market Size (2030) | USD 258 Million |

| Growth Rate (2025 - 2030) | 6.90% CAGR |

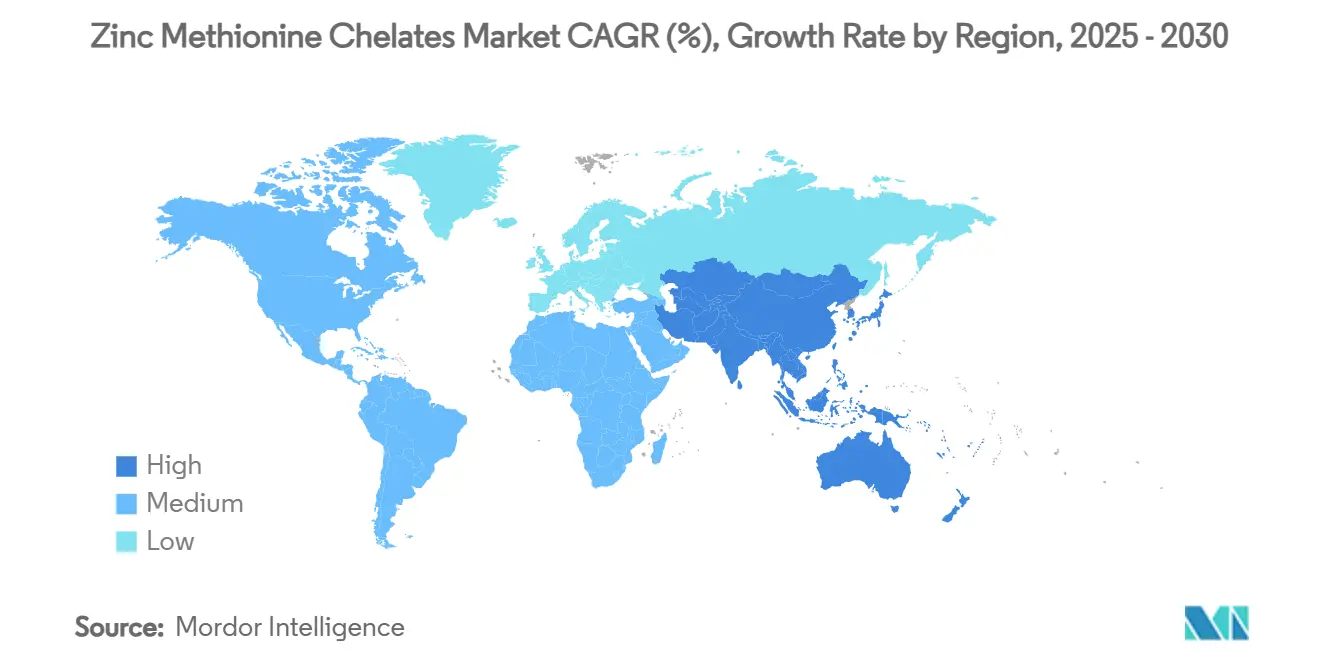

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Zinc Methionine Chelates Market Analysis by Mordor Intelligence

Zinc methionine chelates market size stood at USD 185 million in 2025 and is forecast to reach USD 258 million by 2030, advancing at a 6.9% CAGR. This expansion reflects a decisive shift from inorganic zinc salts toward highly bioavailable organic complexes that boost animal performance, curb fecal mineral losses, and align with tightening sustainability norms. Uptake is accelerating as regulators restrict antibiotic growth promoters, producers seek feed efficiencies that withstand climate stress, and aquaculture integrators demand nutrient-dense formulas that minimize water contamination. Competitive differentiation now centers on chelation chemistry, delivery format innovation, and application support that proves return on investment in diverse production systems. Investment in localized premix manufacturing and strategic alliances among mineral specialists underlines the market’s long-term growth runway.

Key Report Takeaways

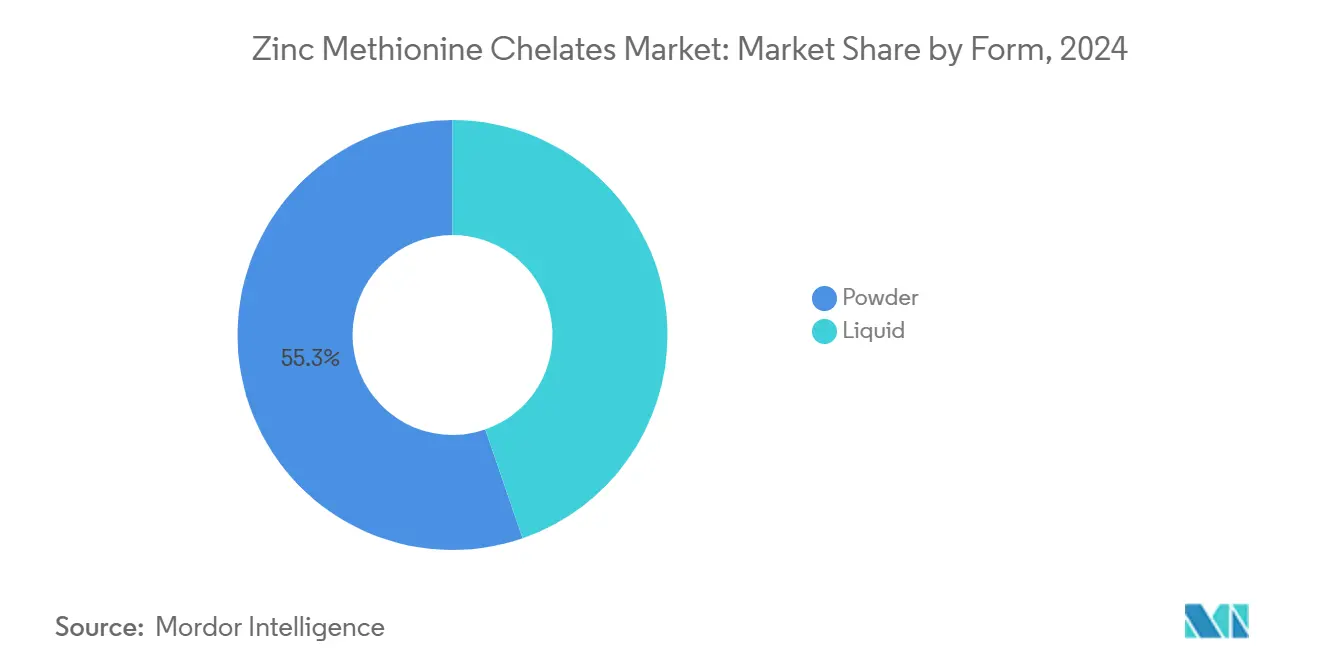

- By form, powder products held 55.3% revenue share in 2024, whereas liquid offerings are projected to record the fastest 8.9% CAGR to 2030, underscoring demand for easy-to-dose solutions in aqua and water-soluble applications.

- By livestock type, poultry commanded 34.8% of the zinc methionine chelates market share in 2024, while aquaculture is forecast to grow at a 10.7% CAGR through 2030 on the back of intensive shrimp and salmon farming.

- By chelation strength, moderate 2:1 complexes captured 48.0% of sales in 2024, strong greater than 2:1 products are poised to expand at a 9.5% CAGR as premium users target maximal mineral retention.

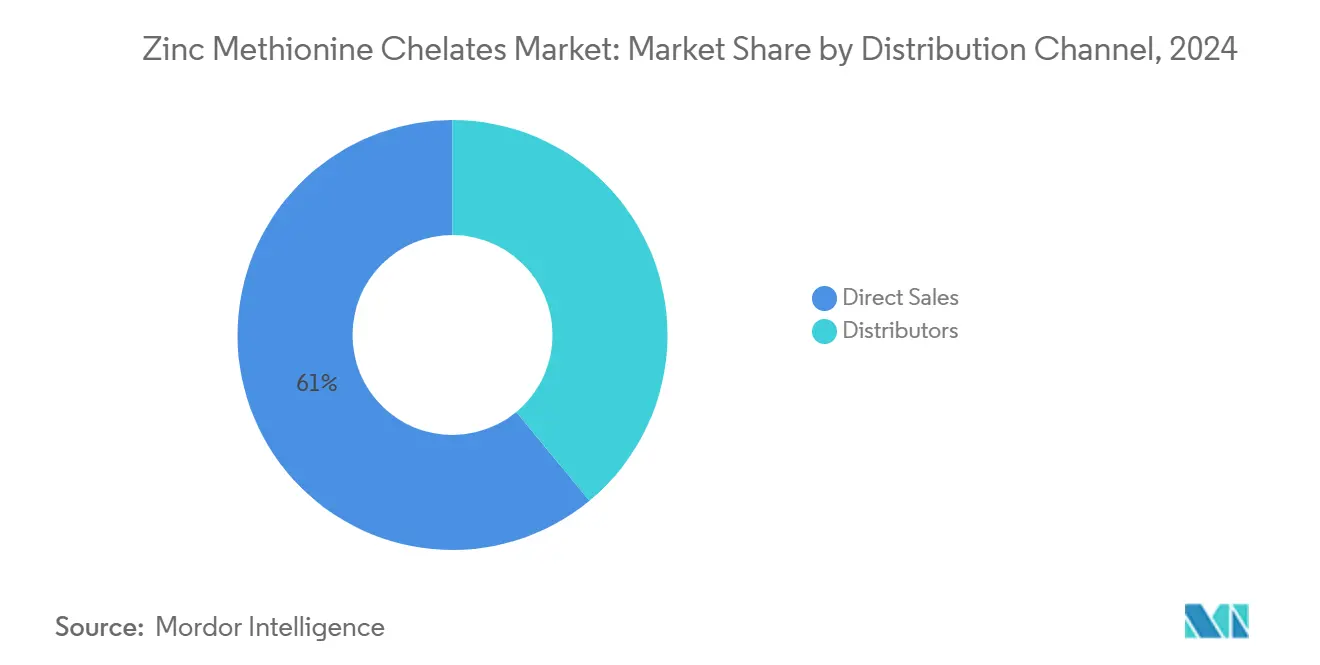

- By distribution channel, direct sales accounted for 61.0% of value in 2024 in the zinc methionine chelates market size, yet distributor channels are likely to post a 7.8% CAGR as emerging regions lean on local inventory and technical outreach.

- By geography, North America led global revenues accounting for 35% of the market in 2024, whereas Asia-Pacific is projected to deliver the fastest 8.2% CAGR, driven by aquaculture scale-up and intensifying livestock densities.

- The top five suppliers control 62% of the zinc methionine chelates market share in 2024, signaling a moderately concentrated zinc methionine chelates market

Global Zinc Methionine Chelates Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory pressure to curb antibiotic growth promoters in animal feed | +1.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Rising demand for chelated trace minerals in climate-resilient poultry production | +1.2% | Global, highest impact in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Expansion of premix production capacity among integrators in South America | +0.9% | South America, spillover to North America | Short term (≤ 2 years) |

| Cost-saving formulation shifts from inorganic to organic trace minerals in aqua feed | +1.1% | Asia-Pacific core, expansion to global markets | Medium term (2-4 years) |

| Intensifying sustainability audits in European dairy supply chains | +0.7% | Europe, extending to North America | Long term (≥ 4 years) |

| Growth of functional pet food segment using bioavailable zinc sources | +0.6% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Pressure to Curb Antibiotic Growth Promoters in Animal Feed

Global bans on routine antibiotic growth promoters are redirecting a USD 2.3 billion additive spend toward nutritional substitutes that protect gut health without pharmacological residues. European Union prohibitions and parallel U.S. FDA actions have legitimized chelated minerals as trustworthy immune modulators [1]Source: U.S. Food and Drug Administration, “Food Additive Petition 031559,” fda.gov. Trials in broilers reveal feed conversion improvements when zinc methionine partly replaces antibiotic regimens, which substantiates the zinc methionine chelates market narrative in both poultry and swine operations. As integrators standardize antibiotic-free labels, feed mills invest in precision mineral programs that guarantee efficiency yet satisfy regulatory screeners. The resulting compliance momentum cements long-term demand for proven, bioavailable zinc sources.

Rising Demand for Chelated Trace Minerals in Climate-Resilient Poultry Production

Heat stress erodes USD 5.8 billion of global poultry output annually, elevating interest in nutritional countermeasures that stabilize antioxidant defenses [2]Source: Journal of Animal Science, “Heat Stress Mitigation via Chelated Minerals,” asas.org. Controlled studies show amino acid–chelated zinc mitigating heat shock protein expression and reinforcing gut barrier integrity in broilers under 34 °C test conditions. Integrators in the Persian Gulf and tropical Asia now integrate chelated minerals at breeder and grow-out stages to maintain uniform carcass yields in summer cycles. Progressive formulation strategies align with the National Poultry Technology Center guidelines, which prioritize mineral bioavailability when ambient temperatures exceed physiological comfort. Wide adoption supports the zinc methionine chelates market as producers pre-empt productivity dips linked to climate volatility.

Cost-Saving Formulation Shift from Inorganic to Organic Trace Minerals in Aqua Feed

Shrimp and fin-fish nutritionists report that chelated zinc delivery at 40% of previous inorganic levels preserves growth and survivability, yielding tangible cost offsets in feeds that constitute up to 70% of operating expenses[3]Source: Frontiers in Veterinary Science, “Organic Trace Minerals in Shrimp Nutrition,” frontiersin.org. Research on Litopenaeus vannamei documented superior intestinal antioxidant status and reduced cholesterol when zinc methionine replaced zinc sulfate. Such evidence drives Asia-Pacific formulators to retrofit pellet lines for liquid and fine powder chelates that disperse evenly in water-stable rations. Procurement teams translate lower inclusion into working-capital relief, therefore accelerating the zinc methionine chelates market adoption in high-density ponds and recirculating aquaculture systems.

Growth of Functional Pet Food Segment Using Bioavailable Zinc Sources

North American pet-food formulators capitalize on consumer readiness to pay premiums for formulations touting coat sheen and immune vitality. A double-blind study on senior dogs recorded faster hair regrowth and lower shedding with amino acid–complexed zinc versus zinc oxide. AAFCO guidance now highlights chelation as a viable strategy for minimizing mineral toxicity in sensitive breeds. Niche brands market condition-specific recipes—mobility, skin, and gastrointestinal health—that rely on zinc methionine to substantiate claims. The retail traction broadens the zinc methionine chelates industry footprint beyond traditional livestock verticals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of methionine and zinc raw materials | -1.4% | Global, highest impact in cost-sensitive markets | Short term (≤ 2 years) |

| Limited awareness among smallholder farmers in Africa | -0.8% | Africa, extending to rural Asia-Pacific | Long term (≥ 4 years) |

| Strict maximum inclusion limits of zinc in EU feed regulations | -0.9% | Europe, potential spillover to other regions | Medium term (2-4 years) |

| Availability of cheaper inorganic zinc sulfate alternatives | -1.1% | Global, strongest in price-sensitive segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Methionine and Zinc Raw Materials

Global methionine spot prices spiked following a U.S. Department of Commerce ruling that set a 9.24% dumping margin on Spanish exports, magnifying uncertainty for chelate producers [4]Source: Federal Register, “Methionine From Spain: Final Results of Antidumping Duty Review,” federalregister.gov. Parallel zinc concentrates shortages tied to Peruvian mine curtailments inflated smelter premia. Manufacturers hedge with multi-year contracts yet smaller formulators face margin squeeze, prompting temporary reversion to inorganic salts. Fluctuating input costs therefore temper the zinc methionine chelates market expansion where tight feed budgets dominate procurement choices.

Availability of Cheaper Inorganic Zinc Sulfate Alternatives

Benchmark FOB Qingdao prices for zinc sulfate heptahydrate hover 65% below comparable chelated zinc equivalents, rendering cost-benefit debates difficult in commodity swine and layer rations. Meta-analyses confirm inorganic zinc can sustain baseline growth when provided at elevated inclusion, narrowing immediate performance differences. Feed formulators balancing penny-per-pound targets may downgrade to sulfates during price spikes or liquidity constraints, which periodically dents the chelated zinc methionine market momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Dominance Driven by Handling Convenience

Powder variants generated 55.3% of the zinc methionine chelates market share as premix plants favor dry flowability, extended shelf stability, and compatibility with automated micro-dosing equipment. The zinc methionine chelates market size for powder products is set to rise steadily as global feed mills retrofit higher-speed ribbon blenders that rely on uniform bulk density. Direct inclusion into pelleted and mash feeds limits nutrient segregation, boosting formulation predictability and reinforcing end-user confidence.

Liquid formats exhibit the highest 8.9% CAGR. Ready-to-use suspensions dissolve swiftly in recirculating aquaculture systems and drinking-water lines, supporting rapid therapeutic interventions during health challenges. Manufacturers refine viscosity profiles and preservative systems that safeguard shelf life at tropical storage temperatures. These functional gains justify price premiums in hatchery, nursery, and pet-food wet-mix settings, positioning liquids as a core innovation pathway within the broader zinc methionine chelates market.

By Livestock Type: Aquaculture Emerges as Growth Engine

Poultry retained a 34.8% revenue lead in 2024 due to the sector’s early adoption of chelates for heat-stress mitigation and antibiotic-free programs. The zinc methionine chelates market size tied to broiler and layer rations is forecast to climb steadily as integrators expand cage-free facilities that intensify stress loads. Field trials demonstrate up to 3-point improvements in feed conversion when replacing 50% of zinc oxide with zinc methionine in finisher diets.

Aquaculture delivers the strongest 10.7% CAGR, driven by shrimp, tilapia, and Atlantic salmon intensification. Formulators cite lower leaching losses and improved gill health as decisive benefits over sulfate counterparts, aligning with stricter water-quality discharge limits in Southeast Asia. The zinc methionine chelates market share in aqua feeds is therefore set to widen as governments incentivize high-density systems that demand ultra-available micronutrients to safeguard survival rates.

By Chelation Strength: Moderate Chelates Balance Performance and Cost

Moderate 2:1 chelates controlled 48.0% of the zinc methionine chelates market size by offering adequate protection against antagonistic minerals while maintaining competitive pricing. Nutritionists value their validated bioavailability across multiple species, ensuring predictable blood zinc levels without excessive fortification. The zinc methionine chelates market size associated with moderate complexes remains anchored in mainstream broiler, swine grow-finish, and dairy concentrate applications where cost discipline prevails.

Strong greater than 2:1 chelates expand at a 9.5% CAGR as premium dairy herds, companion animals, and salmon sectors seek maximal uptake. Enhanced molecular stability shields zinc from phytate binding and alkalinity shifts along the gastrointestinal tract, fostering high tissue deposition. Producers leverage the incremental margin by lowering supplementation rates yet achieving equal or superior zootechnical outcomes, thus carving a high-value niche within the zinc methionine chelates market.

By Distribution Channel: Direct Sales Reflect Technical Complexity

Direct channels captured 61.0% of global revenue in 2024 because premix integrators rely on manufacturer agronomists to optimize inclusion curves and troubleshoot antagonisms with calcium, phytate, or fiber. Long-term supply contracts mitigate the risk of counterfeit chelates and ensure traceability, which downstream packers demand for audit readiness. This collaboration deepens producer trust and sustains repeat orders, reinforcing direct sales dominance in the zinc methionine chelates market.

Distributor networks grow at 7.8% CAGR as smaller farms in South America, Southeast Asia, and Eastern Europe seek flexible pack sizes and localized after-sales support. Regional warehouse hubs shorten lead-times and buffer exchange-rate exposure for buyers. As awareness campaigns widen, distributors will play a pivotal role in introducing zinc methionine chelates market solutions to frontier geographies where manufacturer footprints are still emerging.

Geography Analysis

North America retained the largest zinc methionine chelates market share of 35% revenue in 2024 on the strength of vertically integrated poultry and swine systems that prioritize antibiotic-free credentials and measurable feed efficiency. Zinpro and Balchem reinforce market penetration by coupling product supply with on-farm diagnostics that quantify tissue mineralization gains. Research consortia with universities bolster evidence that supports further inclusion in phase-feeding strategies, extending the region’s demand base. Enhanced water-soluble offerings for stress periods illustrate continuous product evolution tailored to U.S. and Canadian husbandry models.

Asia-Pacific records the fastest 8.20% CAGR through 2030. China’s push for professionalized shrimp culture and India’s duty reduction on key feed inputs catalyze widespread chelate adoption in aqua diets. Feed conglomerates in Vietnam and Indonesia integrate local chelate manufacturing under joint ventures to circumvent import tariffs and guarantee consistent quality. Extension programs led by FAO train smallholders on mineral optimization under changing monsoon patterns, indirectly mainstreaming zinc methionine chelates market practices across emerging clusters.

Europe represents a mature yet opportunity-rich landscape where environmental audits and consumer scrutiny align in favor of chelated complexes. Cooperatives in Denmark and the Netherlands pilot precision supplementation that trims manure zinc output without compromising daily milk solids, meeting progressive retailer scorecards. Despite regulatory inclusion ceilings, the zinc methionine chelates market continues to expand via value-added niches such as organic labeled layers and specialty calf milk replacers.

Competitive Landscape

The top five suppliers control 62% of global revenue, signaling a moderately concentrated zinc methionine chelates market. Zinpro commands the major share by leveraging proprietary Availa and TruCare platforms protected by robust patent portfolios. Balchem, through its encapsulation expertise and multi-species technical service teams, holds its position in the market. DSM-Firmenich, ADM, and Novus International round out the leadership cohort, each wielding integrated supply chains and regional production footprints that support localized customer service. Scale confers advantages in raw-material procurement, regulatory dossier maintenance, and sustained R&D spend aimed at refining chelation efficiency and delivery formats.

Mid-tier competitors pursue differentiation via species-targeted blends or partnerships with premix specialists that need private-label chelate sources. For instance, Anpario’s acquisition of Bio-Vet expands its probiotic pairing portfolio, enabling combination packs that address immunity and mineral nutrition concurrently. Innovation trajectories include micro-encapsulated liquids that resist oxidation, synergistic blends with yeast metabolites, and digitally aided dosing systems that align mineral release with digestive pH shifts.

Sustainability pressures and evolving antibiotic-free standards drive ongoing strategic maneuvers. DSM-Firmenich’s decision to spin off its animal nutrition unit, valued at EUR 3 billion (USD 3.3 billion), may prompt portfolio realignments or invite new capital flows that reshape competitive intensity. Joint ventures between mineral suppliers and microbiome startups indicate a widening frontier where chelation expertise converges with gut-health science, potentially redefining value propositions within the zinc methionine chelates market.

Zinc Methionine Chelates Industry Leaders

Novus International, Inc.

Zinpro Corporation

Balchem Corporation

ADM (Archer Daniels Midland Company)

Alltech Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Food and Drug Administration (FDA) approved zinc L-selenomet hionine for broiler diets, validating chelated mineral efficacy and safety claims.

- January 2025: Novus International partnered with Resilient Biotics on a three-year program to identify microbial strains that enhance swine respiratory health, complementing trace mineral strategies.

- October 2024: DSM-Firmenich has opened a 100,000 metric tons animal nutrition plant in Sete Lagoas, Brazil, boosting local production of mineral premixes for beef and dairy cattle. The facility enhances regional access to trace minerals like zinc methionine chelates, supporting demand for more bioavailable and sustainable feed solutions in one of the world’s largest livestock markets.

- July 2024: ADM unveiled its new nutrient plant in Apucarana, Paraná, increasing its Brazilian premix capacity by 40%. The expansion supports rising demand for advanced trace minerals like zinc methionine chelates, enhancing local access to high-bioavailability feed ingredients for Brazil’s growing livestock sector.

Global Zinc Methionine Chelates Market Report Scope

| Powder |

| Liquid |

| Poultry |

| Swine |

| Ruminant |

| Aquaculture |

| Companion Animals |

| Weak (1:1) |

| Moderate (2:1) |

| Strong (greater than 2:1) |

| Direct Sales |

| Distributors |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| Netherlands | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Form | Powder | |

| Liquid | ||

| By Livestock Type | Poultry | |

| Swine | ||

| Ruminant | ||

| Aquaculture | ||

| Companion Animals | ||

| By Chelation Strength | Weak (1:1) | |

| Moderate (2:1) | ||

| Strong (greater than 2:1) | ||

| By Distribution Channel | Direct Sales | |

| Distributors | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| Netherlands | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the chelated zinc methionine market?

The sector generated USD 185 million in 2025 and is projected to reach USD 258 million by 2030.

Which region is expected to grow the fastest?

Asia-Pacific is forecast to post an 8.20% CAGR through 2030, led by aquaculture feed demand.

Why are chelated forms preferred over zinc sulfate?

Chelated zinc offers higher bioavailability at lower inclusion, improves immunity, and lowers fecal mineral losses, which supports sustainability goals.

How concentrated is the supplier landscape?

The top five players control roughly 62% of global revenue, indicating moderate consolidation

What livestock segment will expand most rapidly?

Aquaculture applications are set to grow at a 10.7% CAGR as shrimp and salmon farmers adopt chelated minerals for water-stable, high-efficiency feeds.

Are liquid or powder chelated products growing faster?

Liquid formulations lead growth with an 8.9% CAGR thanks to ease of dosing in water-based delivery systems and aqua feed lines.

Page last updated on: