Zeolite Molecular Sieves Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.98 Billion |

| Market Size (2031) | USD 5.14 Billion |

| Growth Rate (2026 - 2031) | 5.28% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

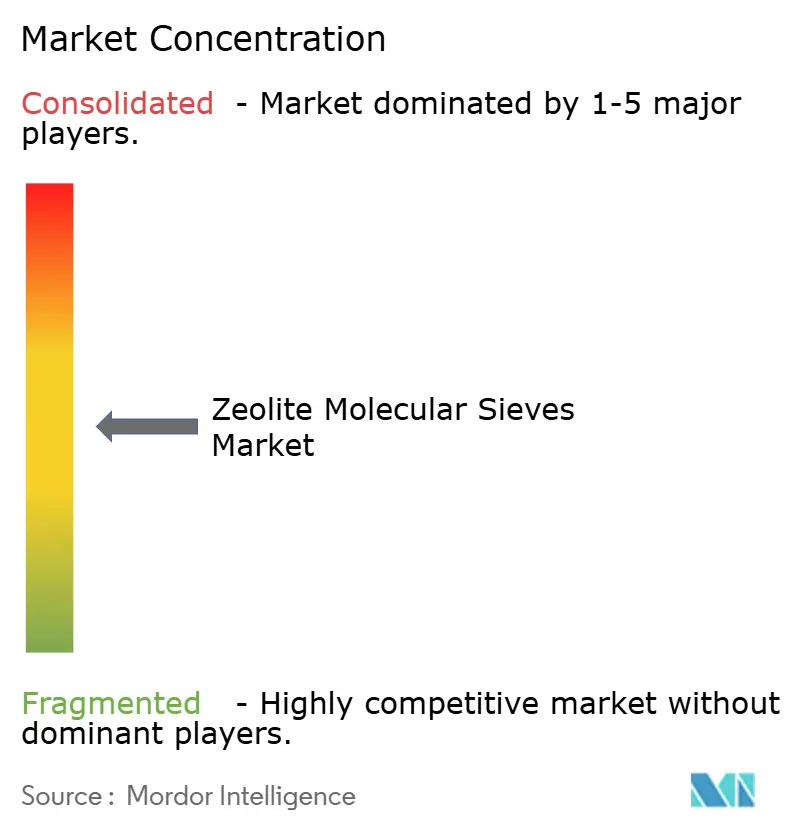

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Zeolite Molecular Sieves Market Analysis by Mordor Intelligence

Zeolite Molecular Sieves Market size in 2026 is estimated at USD 3.98 billion, growing from 2025 value of USD 3.78 billion with 2031 projections showing USD 5.14 billion, growing at 5.28% CAGR over 2026-2031. Demand growth is anchored in four structural forces: tightening environmental regulations that substitute phosphates in detergents, capacity additions across global petrochemical complexes, rapid urbanization in emerging economies that drives hygiene product uptake, and the accelerated pursuit of low-carbon industrial processes that favor zeolite-based adsorption and catalysis. Competitive differentiation rests on proprietary synthesis know-how that tailors pore size, silica-to-alumina ratio, and crystal morphology to specific separation or catalytic duties. Cost volatility in alumina and high-purity silica feedstocks poses a margin challenge, but circular feedstock strategies, especially the conversion of coal fly ash and other industrial residues, are mitigating raw-material risk while supporting corporate sustainability goals. Breakthrough deployments in carbon-capture and PFAS remediation are expanding the commercial frontier, positioning advanced zeolite formulations as viable alternatives to activated carbon and amine solvents in next-generation environmental systems

Key Report Takeaways

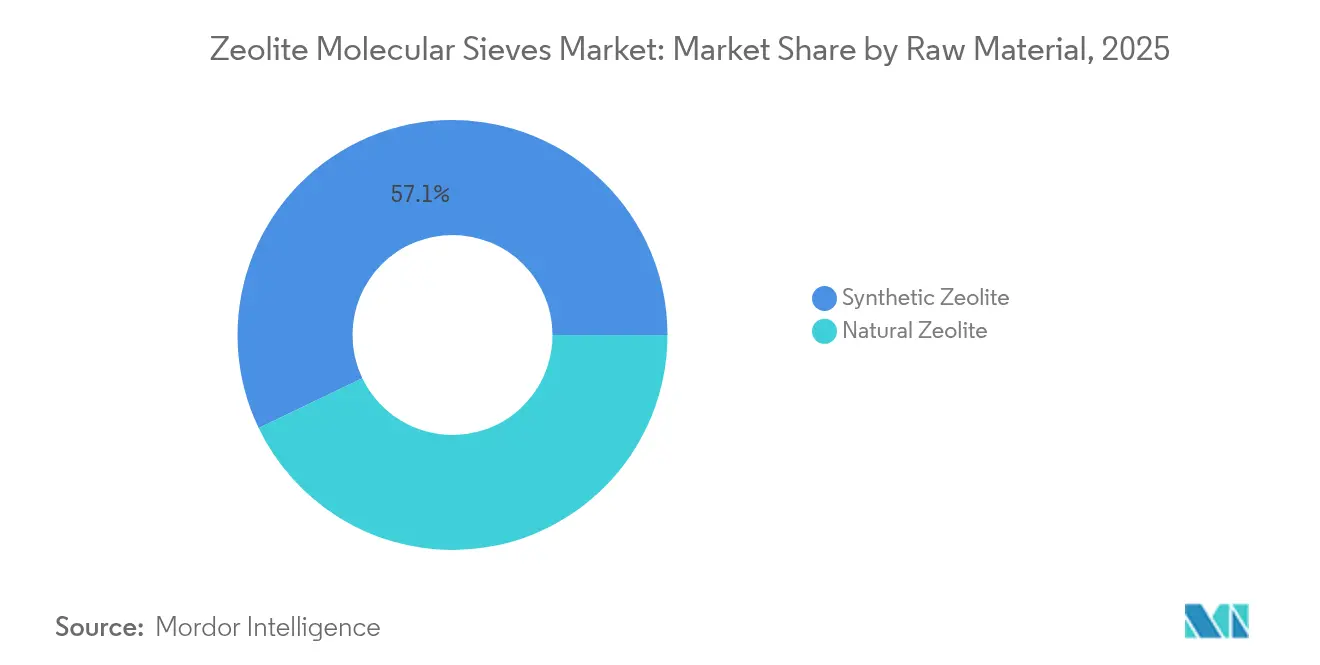

- By raw material, synthetic zeolite A held 57.12% of the zeolite molecular sieve market share in 2025; natural zeolites are projected to expand at a 5.84% CAGR through 2031.

- By end-user industry, detergents commanded 65.02% share of the zeolite molecular sieve market size in 2025; waste and water treatment is the fastest-growing end-use at 5.72% CAGR to 2031.

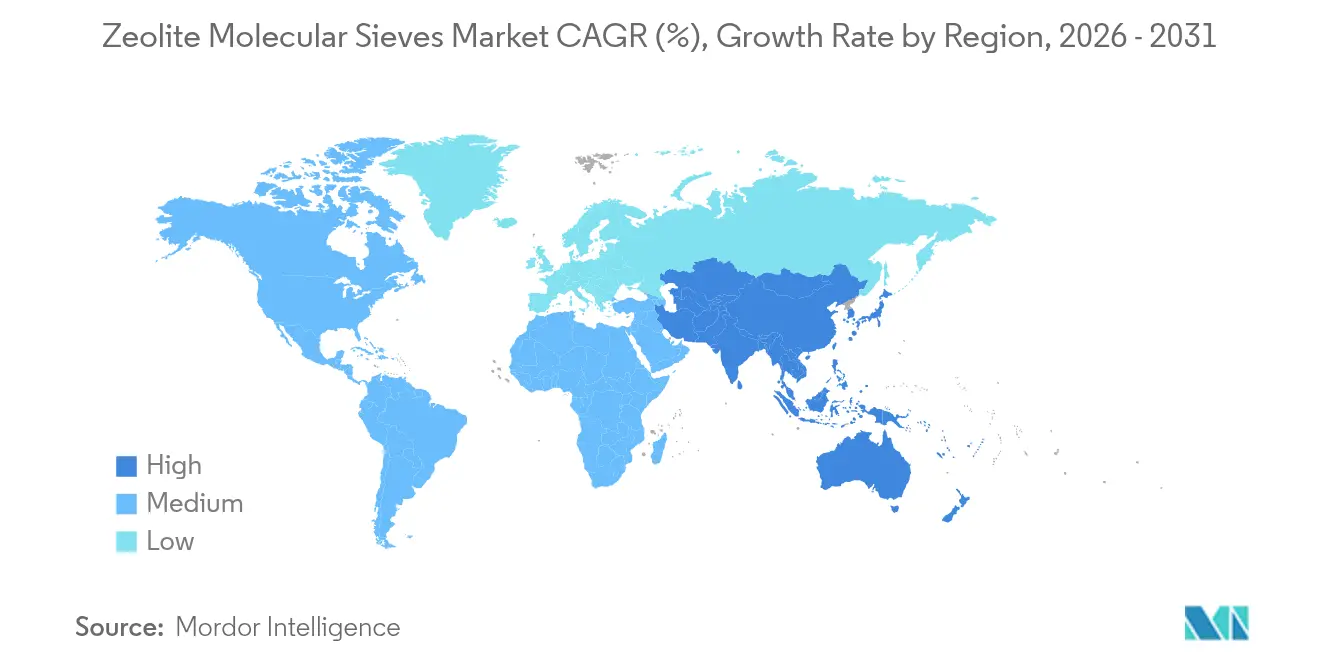

- By geography, Asia Pacific accounted for 37.12% revenue share in 2025 and is advancing at a 6.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Zeolite Molecular Sieves Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Phosphate bans in detergents shifting builders to zeolites | +1.2% | Global, early adoption in EU and North America | Medium term (2-4 years) |

| Petrochemical dehydration and gas-purification boom | +1.8% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Stringent wastewater discharge norms | +1.1% | Global, stringent in developed markets | Short term (≤ 2 years) |

| Hygiene-driven detergent demand in emerging economies | +0.9% | APAC, Latin America, Africa | Medium term (2-4 years) |

| Bio-refinery shift demanding shape-selective catalysts | +0.6% | North America and EU leading | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Phosphate Bans in Detergents Shifting Builders to Zeolites

Global detergent regulations prohibit phosphates because of eutrophication risks, redirecting builder demand toward zeolite 4A. The European Union’s 2017 ban eliminated 2.5 million tons of phosphate consumption annually, and zeolites now replace roughly 60% of that volume in both powder and liquid formulations[1]Nicholas Stockreiter, “Environment,” EUZEPA, euzepa.eu. Similar mandates in North America, along with phased restrictions in India and Brazil, sustain predictable volume growth. Performance advantages compound the regulatory pull: zeolite 4A exhibits higher calcium-binding capacity than carbonates, securing wash performance in hard-water regions. Multinational detergent brands have embedded zeolite builders across their global portfolios, making a reversal technically and commercially unlikely. Emerging economies are poised to expand phosphate-free regulations through 2027, reinforcing the long-run demand trajectory for the zeolite molecular sieve market.

Petrochemical Dehydration and Gas-Purification Boom

Investment exceeding USD 50 billion in new ethylene and propylene complexes across China, India, and Saudi Arabia is elevating demand for 3A and 4A molecular sieves that dehydrate cracked gas and strip CO₂ to parts-per-million levels. A single world-scale ethylene cracker consumes 500–800 tons of sieves in initial charging and annual top-ups. Shale-gas growth in North America accelerates the trend, because unconventional feedstocks carry higher moisture and acid-gas loads. Recent synthesis advances have produced larger zeolite crystals with enhanced mass-transfer characteristics, cutting regeneration energy by 25% and reducing lifecycle cost for petrochemical operators. Consequently, the zeolite molecular sieve market is poised to capture incremental offtake from greenfield projects and from revamps that target higher purity specifications.

Stringent Wastewater Discharge Norms

The U.S. EPA’s 2024 effluent guideline revisions and China’s National Sword policy mandate lower ammonia-nitrogen and heavy-metal limits that conventional treatments struggle to meet cost-effectively. Coal fly-ash derived zeolites remove more than 90% of ammonia-nitrogen and can be regenerated multiple cycles, driving total cost of ownership down for municipal and industrial plants. EU facilities that upgraded to zeolite-based tertiary processes report 80–95% phosphorus removal, while zeolite–carbon composites achieve 90% plus antibiotics elimination in just two-minute contact times. Tighter discharge norms, therefore, redirect capital budgets toward zeolite systems, lifting the zeolite molecular sieve market outlook in environmental segments.

Hygiene-Driven Detergent Demand in Emerging Economies

Urbanization and rising disposable incomes are pushing per-capita detergent use in India and Southeast Asia upward at double-digit rates. Washing-machine penetration across South Asia remains below 25%, leaving ample runway for appliance adoption that favors zeolite-built detergents owing to hard-water prevalence. Local producers are expanding zeolite capacity in India, Thailand, and Brazil to shorten supply chains and hedge currency volatility, reinforcing regional demand pull for the zeolite molecular sieve market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enzyme and chemical substitutes in laundry formulations | -0.8% | Global, particularly in premium detergent segments | Medium term (2-4 years) |

| Volatile alumina/silica feedstock pricing | -1.1% | Global, with acute impact on cost-sensitive applications | Short term (≤ 2 years) |

| High energy footprint questioned by ESG investors | -0.7% | North America and EU leading, APAC following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Enzyme and Chemical Substitutes in Laundry Formulations

Premium detergent brands increasingly favor protease and lipase enzymes that deliver comparable soil removal at lower builder dosage, cutting zeolite content by up to 20% in liquid formats. Polycarboxylate and phosphonate builders disperse easily in concentrated liquids, where zeolite’s insolubility complicates processing and packaging. As liquid detergents represent the fastest-growing category in developed markets, zeolite volumes risk erosion in the top-tier segment. Yet powder detergents and value-priced products, particularly in emerging economies, still depend on zeolite 4A for hardness control, mitigating the overall impact on the zeolite molecular sieve market.

Volatile Alumina/Silica Feedstock Pricing

Alumina prices increased in 2024 amid energy cost spikes, while Hurricane Helene disrupted North Carolina quartz supply that feeds specialty zeolite production. Small and mid-tier producers lacking vertical integration face margin compression when raw-material spikes coincide with fixed-price supply contracts. In response, several firms are commercializing fly-ash and red-mud derived zeolites that slash raw-material costs by up to 50% and qualify under circular-economy procurement policies. These innovations buffer, but do not eliminate, pricing risk in the zeolite molecular sieve market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Synthetic Dominance Faces Natural Revival

Synthetic zeolite A captured 57.12% of global volume in 2025 thanks to precise Si/Al control that engineers pore size for petrochemical dehydration and separation tasks. Cost-optimized hydrothermal, microwave-assisted, and template-free syntheses continue to elevate product purity while trimming energy consumption by 35%. In contrast, natural clinoptilolite and mordenite grades are growing at 5.84% CAGR, primarily in agriculture, odor control, and low-pressure water treatment applications where the performance-to-price ratio outranks crystal perfection. Natural deposits in Turkey and Bulgaria deliver ore that requires minimal ion-exchange to reach specification, offering a 30–40% cost edge. Regulatory drivers such as the EU’s Green Deal favor non-synthetic minerals, further stimulating adoption. Looking forward, synthetic grades maintain their hold in high-pressure dehydration and catalysis, but natural zeolites increasingly claim environmental and agricultural niches, carving a complementary growth lane within the zeolite molecular sieve market.

By End-user Industry: Detergents Lead While Water Treatment Surges

Detergents accounted for 65.02% of global revenue in 2025, supported by zeolite 4A’s entrenched role as the dominant phosphate substitute. Product-development efforts target sub-5 micron particle sizes and silicate coatings to enhance suspension in liquid blends and to curb caking in powder formats. Petrochemical and refining uses rank second, capitalizing on rising ethylene and propylene capacities in Asia and the Middle-East that need robust dehydration performance under high partial-pressure hydrocarbon streams. Waste and water treatment, advancing at a 5.72% CAGR, is the fastest-growing end-use on tightening discharge norms. Iron-modified zeolites achieve 75–98% lead removal, while specialty sieves capture uranium in mining effluents, underscoring their versatility. Air-purification, industrial gas, and agricultural applications round out demand, each leveraging zeolite selectivity to cut energy or nutrient losses. These cross-sector dynamics cement diversified resilience for the zeolite molecular sieve market size over the forecast horizon.

Geography Analysis

Asia Pacific generated 37.12% of global sales in 2025 and is set to grow at a 6.02% CAGR. China spearheads investment in ethylene crackers and coal-to-chemicals complexes, each requiring hundreds of tons of molecular sieves for dehydration duty. Asia Pacific’s convergence of production scale, tightening environmental norms, and large consumer bases drives the region’s leadership. China’s Zhejiang and Guangdong ethylene projects require molecular-sieve dehydration units that remove moisture to below 1 ppm, while local wastewater standards enforce ammonia limits that spur zeolite tertiary systems.

North America exhibits mature but technology-rich demand. Shale-gas processing plants in Texas deploy 3A molecular sieves to strip moisture before cryogenic NGL recovery, seeking higher efficiency and longer bed life. EPA PFAS discharge proposals accelerate trials of high-silica zeolites that capture perfluoro-alkyl compounds at parts-per-trillion levels, an emerging revenue stream for specialty producers.

Europe prioritizes sustainability and circularity. Plants in Germany and the Netherlands validate fly-ash-derived zeolites at commercial scale, delivering 40% embodied-carbon reduction relative to virgin mineral routes. Middle-East and Africa capitalize on petrochemical diversification and water scarcity.

Saudi Arabia’s Vision 2030 resin capacities rely on large-format molecular-sieve towers for feedstock preparation. South Africa’s mining sector adopts clinoptilolite for acid-mine drainage remediation, benefitting from domestic natural deposits that eliminate import costs.

Collectively, these regional developments underscore the expanding geographic canvas for the zeolite molecular sieve market.

Value Chain Analysis

The value chain starts with aluminosilicate inputs such as bauxite-derived alumina, sodium silicate, and sodium hydroxide, along with binders and cation-exchange media used to tune performance (for example, 3A/4A/5A and X/LSX families). Synthetic production centers on gel preparation and controlled crystallization, followed by filtration, drying, calcination, and forming into beads, pellets, or granules, then activation and packaging. Natural zeolite routes add mining, beneficiation, and ion-exchange steps, with USGS reporting 81,000 tons of US natural zeolite production in 2024 for applications including animal feed, odor control, and water purification.

Downstream, sieve suppliers sell through two main channels: direct, application-engineering-led supply to large petrochemical, refining, industrial gas, and LNG customers (where bed design, loading, and regeneration support are part of the offer), and distributor-led supply to mid-sized users in detergents, HVAC, and general drying. Key participants span integrated chemical and catalyst players and specialist sieve producers (for example, BASF, Clariant, Honeywell UOP, W. R. Grace, Zeochem, and Zeolyst International). Differentiation increasingly rests on formulation know-how (attrition resistance, cycle stability, and selectivity) and on lower-carbon feedstock strategies, including converting coal fly ash and other industrial residues into zeolite precursors to reduce raw-material and logistics exposure.

Competitive Landscape

The zeolite molecular sieves market is moderately fragmented. Barriers to entry include capital-intensive hydrothermal reactors, stringent ISO quality requirements for food and pharma grades, and long qualification cycles in petrochemical plants. However, newer entrants from China and India exploit waste-to-zeolite routes that slash raw-material cost and align with ESG procurement mandates, challenging incumbents on price in commodity segments. Strategic moves emphasize capacity expansion, product customization, and sustainability.

Zeolite Molecular Sieves Industry Leaders

BASF

CLARIANT

Honeywell International Inc.

Tosoh Corporation

W. R. Grace & Co.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is expanding as zeolite molecular sieves move beyond commodity drying into higher-value catalytic and environmental duties that require engineered pore architectures and tighter performance specifications. In 2026, Zeopore publicized a mesoporous zeolite approach that upgrades low-cost NaY-zeolite precursors for hydrocracking. In July 2026, INERATEC and Zeopore announced collaboration to integrate that catalyst technology into hydrocracking routes for CO2-neutral fuels and chemicals, pointing to commercial pull for advanced frameworks in refining and circular fuels value chains. R&D activity is also shifting toward data-driven adsorbent design, with 2026 academic work demonstrating machine-learning-guided development of Sr-LSX oxygen adsorbents, which reinforces opportunity in air separation and on-site oxygen supply where adsorption selectivity and stability are monetized.

On the supply side, buyers in petrochemicals, LNG, and industrial gas are placing more emphasis on secure, regionalized sourcing, along with technical service for unit start-ups and bed life optimization. That focus creates whitespace for suppliers that can shorten qualification cycles and localize manufacturing. Capacity additions remain a visible lever, illustrated by Jalon Zeolite stating completion of 2026 expansion projects that doubled its total molecular sieve production capacity. This supports a competitive push toward shorter lead times and broader grade portfolios for dehydration, purification, and emerging water-treatment use cases under tightening discharge norms.

Recent Industry Developments

- July 2026: INERATEC and Zeopore announced a collaboration to integrate Zeopore's meso-zeolite catalyst technology into INERATEC's hydrocracking processes for CO2-neutral fuels and chemicals. The tie-up links an engineered zeolite architecture with a commercial process platform, reinforcing momentum for specialty molecular-sieve catalysts in low-carbon fuel pathways.

- March 2026: Clariant announced a strategic collaboration with Vertimass LLC to scale up advanced zeolite catalysts for the catalytic conversion of biobased alcohols via the CADO process. The partnership targets a scalable catalyst route for sustainable fuels and chemicals, supporting higher-value demand beyond traditional drying and purification grades.

- January 2024: Zeochem acquired Sorbead India and Swambe Chemicals, expanding its footprint in molecular sieves and chromatography gels for pharmaceutical packaging. The acquisition broadened manufacturing and customer reach in adsorbents, strengthening competitive positioning in specialty and regulated end markets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the zeolite molecular sieves market is defined as revenues from natural and synthetic zeolite-based sieve materials used mainly for adsorption, drying, separation, and catalytic functions across industrial and environmental end uses.

Scope exclusions: We exclude non-zeolite molecular sieve families and general adsorbents that do not use a zeolite framework, even if they address similar separation needs.

Segmentation Overview

- By Raw Material

- Natural Zeolite

- Synthetic Zeolite

- By End-user Industry

- Detergents

- Petrochemical and Refining

- Industrial Gas Production

- Waste and Water Treatment

- Air Purification and HVAC

- Agriculture and Animal Feed

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clean fact base around demand pools, manufacturing activity, and end-use trends that pull zeolite molecular sieves. We typically rely on public sources such as USGS mineral statistics, UN Comtrade trade tables, International Energy Agency releases, US EPA technical and regulatory updates, and peer-reviewed separation and catalysis journals to understand volumes, applications, and policy direction.

To translate these signals into sizing inputs, we also review company annual reports and investor presentations, association websites, and trusted business press to map capacity additions, product positioning, and pricing direction. Where needed, we supplement with paid subscription data for company financials and intelligence, patent search, and shipment-level import-export checks to confirm trade flows and unit values. These sources are illustrative only, and many other references were used to collect, validate, and clarify the data.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk assumptions and to fill the gaps on mix, pricing, and adoption in key applications, including detergents, industrial gas production, refining, water treatment, and air purification. We speak with manufacturers, distributors, and end users across major regions so the model reflects how demand is contracted, shipped, and consumed, and then we re-check the final assumptions when input ranges drift from what respondents report in the field.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 12% | APAC: 53% |

| Mid tier: 53% | Functional/Unit leaders: 38% | EMEA: 29% |

| Smaller Players: 14% | Managers: 50% | Americas: 18% |

Market-Sizing & Forecasting

Sizing is built using a top-down and bottom-up approach, with the main structure starting from end-use demand pools and then being reconstructed from production activity and trade movements that connect to zeolite sieve consumption. For example, demand is built by linking application-level indicators like detergent output and formulation intensity, refining and petrochemical activity, industrial gas capacity and utilization, and water and air treatment spending. We then convert these to implied sieve consumption using usage rates validated in interviews.

To keep totals realistic, we corroborate the outputs with selective bottom-up checks such as sampled supplier revenues, channel checks on regional shipment patterns, and ASP-by-form estimates (pellets, beads, powders) multiplied by plausible volumes. When company data is missing or reported at a higher level, gaps are handled with peer benchmarking and conservative allocation rules that we confirm through follow-up calls.

Forecasts are produced using scenario analysis, since end-market swings can be driven by energy cycles, environmental compliance spending, and new capacity ramp-ups. The scenarios are anchored on variables like refinery throughput outlook, industrial gas additions, detergent demand trends, zeolite raw material cost movement, and typical price reset timing, and then reconciled back to what primary respondents expect for the next few years.

Data Validation & Update Cycle

Outputs are cross-checked against independent signals such as trade value trends, capacity announcements, and demand movements in major consuming industries, and then variances are investigated before numbers are finalized. If a region or application shows a step-change that is not supported by the supporting indicators, we re-open the assumptions, revisit conversion factors, and re-contact respondents to confirm whether it is a real shift or a modeling artifact.

A multi-step analyst review is followed so definitions, units, and currency conversions remain consistent across the entire model. The report is refreshed annually, and interim updates are made when material events occur, such as large plant start-ups, major regulation changes, or sharp feedstock price moves. Before delivery, a final pass is completed to ensure clients receive the latest aligned view.

Mordor Intelligence's Zeolite Molecular Sieves Market Size Versus Other Published Estimates

Published market sizes for zeolite molecular sieves can differ even when the topic label looks the same, because the boundary of what counts as a zeolite sieve and how end uses are converted into demand is not uniform. Differences also show up when one study uses a different base year, a different currency timing, or a faster price-escalation assumption.

By tracking application-level demand drivers and refresh timing across end uses, Mordor Intelligence keeps the 2026 value tied to detergents, refining, industrial gas production, water treatment, and air purification, instead of folding in broader non-zeolite adsorbents or loosely related catalyst revenues.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.98 B (2026) | |

| Market Research Publisher A | USD 4.10 B (2024) | Uses an earlier base year and a broader table structure by application that can blend adjacent adsorption and catalyst value pools, which lifts the starting value when compared on a like-for-like year. |

| Industry Forecast Outlet B | USD 4.23 B (2024) | Anchors on a 2024 valuation and applies a higher near-term growth and price progression assumption, which can overstate the bridge into 2026 if end-use utilization is modeled aggressively. |

The spread in the table is mainly explained by base-year choice and how tightly the scope is kept to zeolite-framework sieve materials used in defined end uses. When the demand pool is constructed from observable end-market indicators and checked with channel and pricing inputs, the output stays easier to reproduce and to update as new capacity and consumption signals emerge.

Key Questions Answered in the Report

What is the 2026 revenue value for the zeolite molecular sieve market?

It stands at USD 3.98 billion with a forecast CAGR of 5.28% to 2031.

Which raw material type leads global demand?

Synthetic zeolite A dominates with 57.12% volume share in 2025.

Which application segment is growing fastest?

Waste and water treatment is expanding at a 5.72% CAGR through 2031.

Why is Asia Pacific the largest regional market?

The region hosts 37.12% share due to extensive petrochemical investments and stricter environmental policies.

How are manufacturers mitigating feedstock price volatility?

They are adopting waste-derived aluminosilicate sources such as coal fly ash to cut raw-material costs by up to 50%.

Page last updated on: