Wireless Healthcare Asset Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 74.96 Billion |

| Market Size (2031) | USD 213.88 Billion |

| Growth Rate (2026 - 2031) | 23.35% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Wireless Healthcare Asset Management Market Analysis by Mordor Intelligence

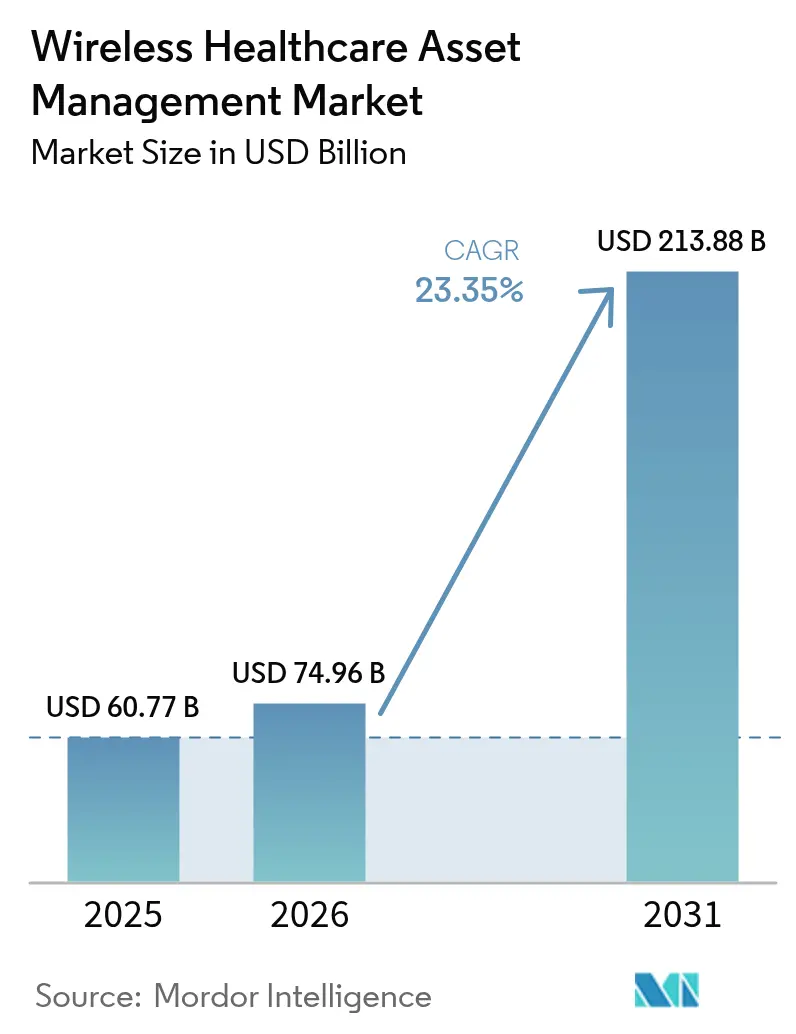

The wireless healthcare asset management market size is expected to grow from USD 60.77 billion in 2025 to USD 74.96 billion in 2026 and is forecast to reach USD 213.88 billion by 2031 at 23.35% CAGR over 2026-2031. Growth is underpinned by hospitals shifting capital from manual inventory audits to real-time location systems that slash equipment search time, automate regulatory documentation, and support predictive maintenance. The convergence of RFID, Bluetooth Low Energy (BLE), and Ultra-Wideband (UWB) with edge-based AI is reshaping utilization economics, as reimbursement regimes penalize avoidable delays and regulators tighten traceability rules.[1]U.S. Food and Drug Administration, “RFID Tags on Medical Devices—Guidance for Industry,” fda.gov Platform vendors are embedding location analytics directly within electronic health record (EHR) workflows, shortening payback cycles and opening up new subscription revenue opportunities. At the same time, cybersecurity mandates such as the forthcoming HIPAA Security Rule updates are influencing technology choices and vendor selection, favoring suppliers who can demonstrate AES-256 encryption and software bill-of-materials transparency.

Key Report Takeaways

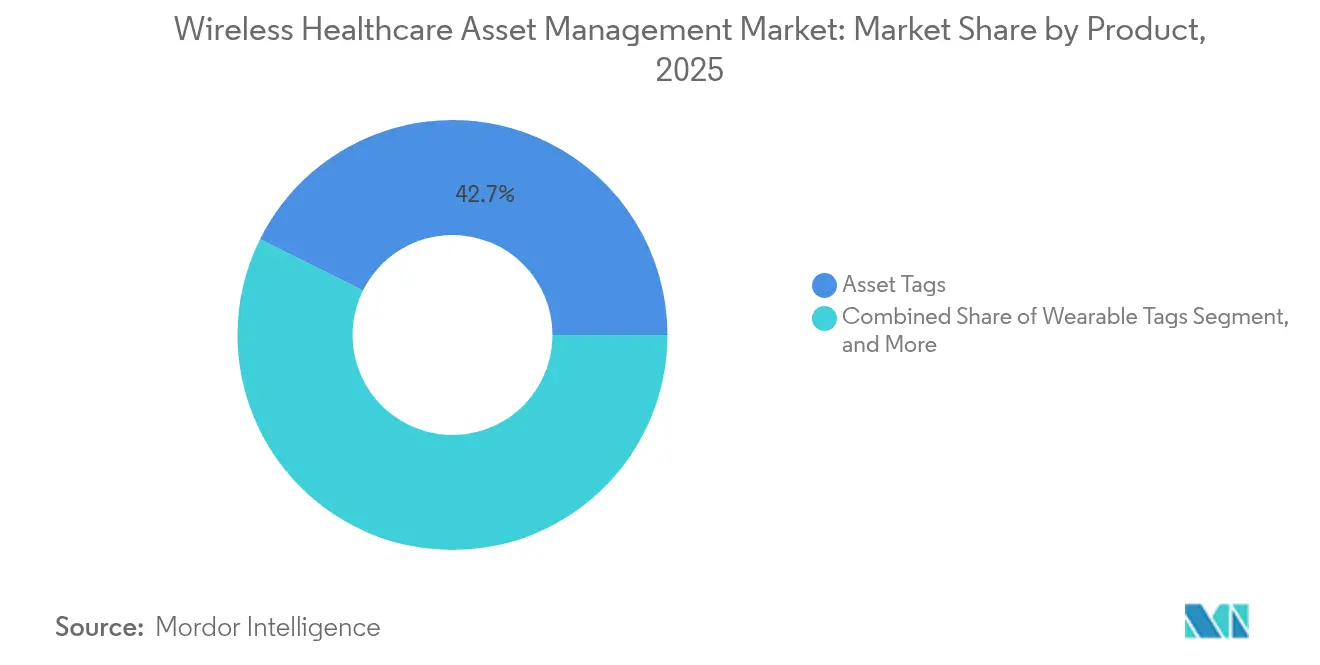

- By product, Asset Tags captured 42.65% of the wireless healthcare asset management market share in 2025, while Software Platforms are projected to achieve a 25.95% CAGR through 2031.

- By technology, RFID held 55.10% revenue share of the wireless healthcare asset management market in 2025; Ultra-Wideband is forecast to expand at 26.05% CAGR through 2031.

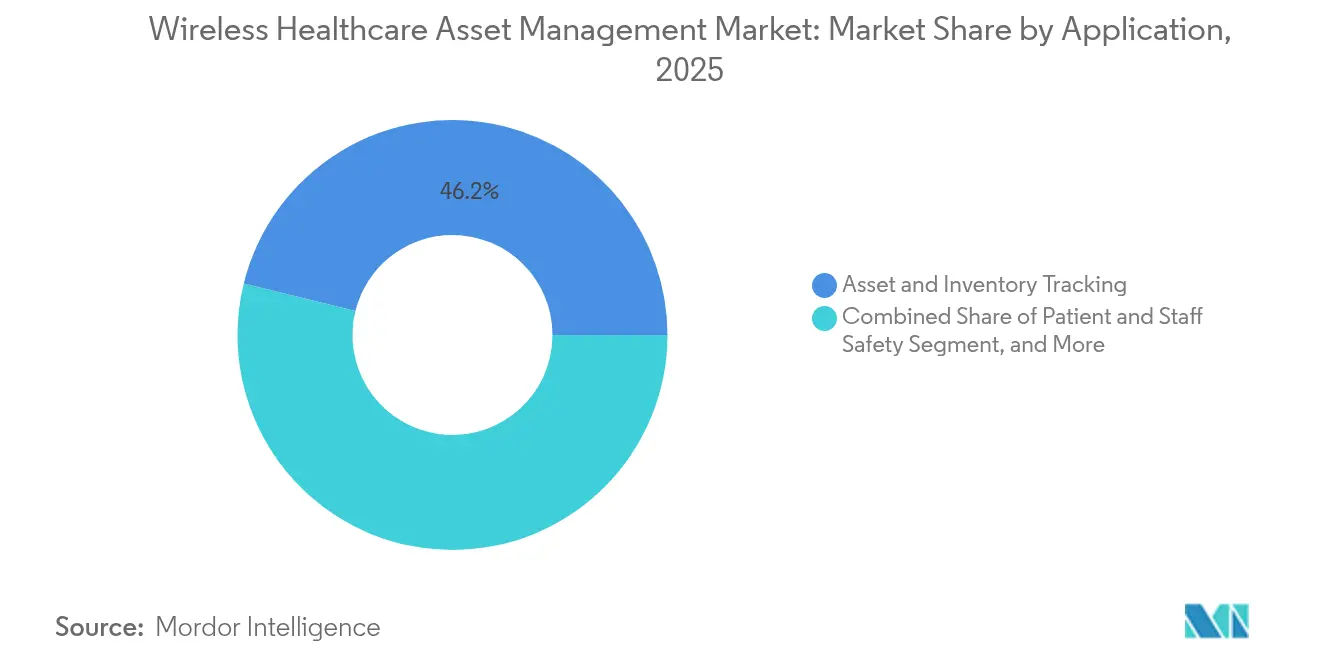

- By application, Asset and Inventory Tracking commanded 46.15% of the wireless healthcare asset management market size in 2025, while Environmental and Condition Monitoring is growing at a rate of 26.2%.

- By end user, Hospitals and Integrated Delivery Networks led the wireless healthcare asset management market with a 53.10% share in 2025, whereas Long-Term Care and Senior Living Facilities are advancing at a 26.4% CAGR.

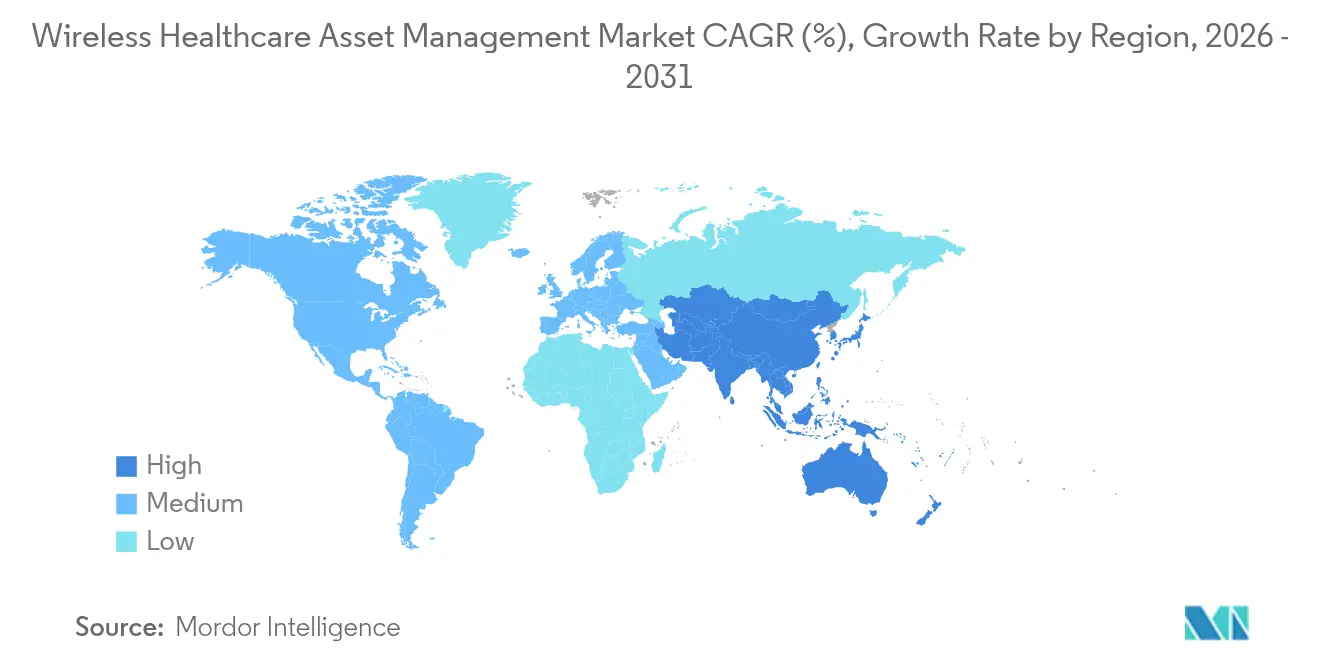

- By geography, North America accounted for 37.45% revenue of the wireless healthcare asset management market in 2025; Asia-Pacific is set to rise at 25.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wireless Healthcare Asset Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of RFID-based asset tagging | +5.2% | North America, Europe, Asia Pacific leading deployments | Medium term (2-4 years) |

| Need for real-time asset visibility | +4.8% | Global, acute in North America and Asia Pacific tier-1 hospitals | Short term (≤ 2 years) |

| Rising investment in smart hospital infra | +4.5% | Asia Pacific core, spillover to Middle East | Long term (≥ 4 years) |

| Edge-AI predictive maintenance | +3.9% | North America, Europe, early pilots in China and India | Medium term (2-4 years) |

| ESG targets driving low-power BLE and UWB | +2.8% | Europe and North America, emerging in Middle East | Long term (≥ 4 years) |

| Shift to RTLS-as-a-Service models | +2.6% | Global, fastest in North America ambulatory surgery centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of RFID-Based Asset Tagging

Hospitals are embedding passive RFID tags into infusion pumps, ventilators, and wheelchairs because the technology provides read ranges of 3 m–10 m without requiring batteries, a critical benefit in settings where biomedical staff turnover exceeds 20% annually. Impinj’s M800 reader, launched in 2024, improves tag-read density by 40%, allowing one fixed reader to monitor 200 assets in busy corridors. FDA guidance issued the same year confirmed that RFID labels attached to Class II devices need no separate 510(k) filing, removing a key regulatory hurdle. A peer-reviewed study demonstrated that RFID tracking reduced search time by 68% in a 300-bed hospital and enabled 4.2 additional monthly procedures per operating room. Ambulatory surgery centers, where manual audits consume up to 90 minutes per shift, are consequently accelerating rollouts.

Need for Real-Time Asset Visibility to Cut Equipment Search Time

Clinical teams in U.S. hospitals lose 21 minutes per shift searching for devices, a drain exacerbated by value-based payment models that penalize extended lengths of stay. Real-time location systems, which refresh every 5–10 seconds, route the nearest available pump or ECG unit to the requesting ward, reducing response time from 12 minutes to under 3 minutes. A 2024 integrated delivery network saved USD 1.8 million a year on rentals after achieving 95% visibility via Wi-Fi triangulation. Zebra Technologies reports customers trimmed capital expenditure by 18% by redeploying idle assets surfaced through its MotionWorks analytics.[2]Zebra Technologies, “Annual Report 2024,” zebra.com

Rising Investment in Smart Hospital Infrastructure

China earmarked CNY 50 billion (USD 7 billion) in 2024 to build smart tertiary hospitals with mandatory real-time location capability under Healthy China 2030. India’s Ayushman Bharat Digital Mission plugged asset-tracking modules into its national health stack that same year, covering 12,000 public facilities. Saudi Arabia’s Vision 2030 program mandates the use of UWB or BLE infrastructure in new medical centers, compressing vendor sales cycles to under 12 months. Cisco notes 38% of its healthcare pipeline now bundles location services, up from 14% in 2022.

Edge-AI Predictive Maintenance Reducing Device Downtime

Embedding analytics at the network edge enables platforms to predict infusion-pump failure 72 hours in advance by analyzing vibration and temperature signatures. GE Healthcare’s Edison module analyzes telemetry from 15,000 imaging devices worldwide and lowered service costs 22% in 2024. Siemens integrated similar algorithms into its Teamplay suite, cutting unplanned downtime by 28%. Early adopters extend the mean time between failures of ventilators by 30%–40%, thereby preserving scarce capital.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront hardware and integration costs | -3.2% | Global, acute in emerging markets and rural North America | Short term (≤ 2 years) |

| Data-privacy and cybersecurity compliance hurdles | -2.9% | North America and Europe, tightening in Asia Pacific | Medium term (2-4 years) |

| Shortage of RTLS-skilled biomedical engineers | -2.1% | Global, severe in rural integrated delivery networks | Long term (≥ 4 years) |

| RF interference from 5G and Wi-Fi-6E in legacy hospital buildings | -1.8% | North America and Europe, emerging in Asia Pacific urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Hardware and Integration Costs

A 300-bed deployment typically requires 150–200 infrastructure nodes, along with 3,000 tags, resulting in a capital outlay of USD 400,000–600,000 before accounting for software and labor costs.[3]American Hospital Association, “Rural Hospital Technology Adoption Survey 2024,” aha.org Ambulatory surgery centers operating on 3%–5% margins struggle to fund such investments despite 24-month payback models. Linking platforms to EHRs like Epic can add 6–9 months of custom interface work priced at USD 150–250 per hour. RTLS-as-a-Service, where vendors retain hardware ownership and bill monthly per-tag fees, is easing friction but remains nascent outside North America.

Data-Privacy and Cybersecurity Compliance Hurdles

HIPAA Security Rule revisions proposed in 2024 require multifactor authentication and AES-256 encryption for connected tags, forcing upgrades to legacy RFID and BLE devices. The EU Medical Device Regulation classifies RTLS software influencing care workflows as Class IIa, adding 12–18 months of conformity assessment. Hospitals now demand a software bill of materials and annual penetration tests, obligations smaller suppliers find hard to satisfy. CISA reported a 34% rise in ransomware attacks on healthcare IoT endpoints in 2024, elevating cybersecurity to a board-level issue.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Analytics-Driven Platforms Overtake Hardware

Software Platforms are expanding at a rate of 25.95% annually, outpacing the overall wireless healthcare asset management market. Hospitals recognize that raw location data has limited value without predictive analytics, EHR integration, and automated audit trails. Asset Tags retained a 42.65% share in 2025, reflecting a legacy RFID and BLE installed base, yet revenue is migrating to recurring software fees. Wearable Tags for duress and elopement prevention are gaining steam in behavioral health units. Wireless Sensor monitoring of temperature and humidity surged following the updated USP 797 sterility rules. Hardware margins are being compressed as semiconductor firms integrate UWB into general-purpose Wi-Fi chipsets, underscoring the shift toward platform economics.

Software-centric vendors tend to capture higher valuation multiples; Zebra’s 2024 filing showed that software and services rose 31% year-over-year, compared to 12% for hardware. As a result, the wireless healthcare asset management market is tilting toward end-to-end subscriptions that roll infrastructure, tags, analytics, and compliance reporting into predictable OPEX.

By Technology: Ultra-Wideband Races Ahead for Sub-Meter Precision

RFID held a 55.10% share in 2025, thanks to the adoption of battery-free passive tags and the increasing ubiquity of readers. However, UWB is growing 26.05% a year as surgical theaters, catheter labs, and neonatal ICUs demand <30 cm accuracy, unattainable with Wi-Fi triangulation or BLE beacons. Wi-Fi solutions leverage existing access points but deliver errors of 3 m–5 m in metal-dense environments. BLE balances cost and performance, making it the preferred option for long-term care facilities. ZigBee and infrared remain niche. Qorvo shipped 12 million UWB chips in 2024, a 47% increase, driven by the demand for surgical instrument tracking.

Hospitals now operate dual-tier architectures, utilizing RFID or BLE for wheelchairs and pumps, and UWB for high-value instruments. Vendors that can orchestrate both layers within a single dashboard are winning multi-year contracts across integrated delivery networks.

By Application: Environmental Monitoring Posts Fastest Gains

Asset and Inventory Tracking accounted for 46.15% of revenue in 2025; however, Environmental and Condition Monitoring is advancing by 26.2% due to stricter cold-chain and pharmacy sterility mandates. United States hospital pharmacies adopting automated temperature sensors cut vaccine wastage by 81% and saved USD 340,000 per site in 2024. Patient and Staff Safety solutions, including duress badges and wander-management wristbands, are expanding in skilled nursing as staffing constraints worsen. Workflow and Capacity Optimization modules that map patient flow across emergency departments and operating rooms help hospitals hit throughput goals without adding beds. Compliance and Audit Management tools, which were once optional, are now typically bundled in most RFPs.

The wireless healthcare asset management market size for environmental monitoring is projected to widen its share as hospitals converge asset location and telemetry to enable contextual intelligence that anticipates failure and automates documentation.

By End User: Long-Term Care Accelerates Amid Labor Shortages

Hospitals and Integrated Delivery Networks held 53.10% of the wireless healthcare asset management market in 2025, leveraging scale to deploy enterprise RTLS. Yet, Long-Term Care and Senior Living Facilities are experiencing a 26.4% annual increase, driven by a 14% vacancy rate for certified nursing assistants that pressures operators to automate rounding and enhance resident safety. Ambulatory Surgery Centers, which perform 60% of U.S. outpatient procedures, are integrating RTLS to reduce turnover times and avoid rentals. Diagnostic Laboratories tracks mobile X-ray and specimen carriers to hit turnaround benchmarks. Other institutions, such as dialysis centers and rehabilitation hospitals, remain in the early stages but offer green-field growth opportunities.

Demonstrable ROI, regulatory reporting, and workforce augmentation form the core purchasing rationale across all end-user categories, anchoring long-term demand for wireless healthcare asset management.

Geography Analysis

North America accounted for 37.45% of the revenue in 2025, as integrated delivery networks, such as HCA Healthcare, standardized asset visibility across hundreds of sites. High EHR penetration: Epic and Oracle Cerner cover 70% of U.S. beds, facilitating rapid data integration. Canada accelerated provincial deployments; Ontario Health invested CAD 85 million (USD 63 million) in 2024 to outfit 42 hospitals. Mexico’s IMSS pilot aimed to achieve a 25% reduction in rental costs across 18 hospitals. CMS has proposed tying payments to utilization metrics, a policy that could expand the wireless healthcare asset management market if adopted.

The Asia Pacific is the fastest-growing region, with a 25.9% CAGR. China mandated RTLS in all new tertiary hospitals larger than 500 beds, directing CNY 30 billion (USD 4.2 billion) toward deployments. India has embedded asset-tracking in the Ayushman Bharat Digital Mission, which spans 12,000 hospitals. Japan subsidizes up to 50% of elder-care RTLS projects to mitigate a projected 370,000-worker shortfall by 2025. South Korea offers certification incentives, and Australia clarified a lighter regulatory path for non-diagnostic RTLS software. Rapid urbanization, as forecasted by the WHO, is expected to add 400 million new city residents by 2030, driving the need for new hospital construction pre-wired for RTLS.

Europe, the Middle East, and Africa display mixed adoption. Germany, the United Kingdom, France, and Spain are deploying RTLS to meet the Medical Device Regulation's traceability rules. GDPR requires anonymization and local data hosting, benefiting vendors with regional cloud services. Saudi Arabia invested SAR 12 billion (USD 3.2 billion) in 2024 for Vision 2030 hospitals with built-in RTLS. The UAE requires RTLS in all new facilities as part of its ambitious goal to become one of the top 100 global healthcare providers. Africa and South America remain nascent, though private chains in Brazil, South Africa, and Nigeria are piloting deployments to attract medical tourists.

Competitive Landscape

The wireless healthcare asset management market exhibits moderate concentration at the platform layer, where Zebra Technologies, CenTrak, Stanley Healthcare, and Impinj dominate EHR interoperability. Yet the tag and sensor tier is fragmented, with dozens of regional suppliers competing on battery life and form factor. Pure-play RTLS specialists face encroachment from enterprise Wi-Fi incumbents, as Cisco and Aruba bundle location services into access points, and semiconductor firms such as Qorvo and NXP embed UWB in commodity tags. The strategy centers on vertical integration into analytics, geographic expansion in the Asia Pacific through greenfield builds, and technology migration toward UWB for sub-meter accuracy.

Vendors are transitioning from one-time hardware sales to multiyear RTLS-as-a-Service contracts. Zebra’s 2024 report noted 31% growth in software and services driven by per-bed subscriptions. CenTrak partnered with Epic and Oracle Cerner to embed location data natively in EHR workflows, shortening time-to-value. Stanley Healthcare merged with AeroScout to consolidate its portfolios for infant security, staff duress, and asset tracking. Honeywell earned ISO 27001 in 2024, signaling security leadership that resonates with procurement teams obliged to follow CISA guidance.

Patent activity is brisk. The USPTO granted 127 healthcare location patents in 2024, representing a 38% year-over-year increase, with a focus on interference mitigation, battery optimization, and privacy-preserving algorithms.[4]United States Patent and Trademark Office, “Healthcare Location Technology Patent Grants 2024,” uspto.gov Vendors demonstrating compliance readiness, predictive analytics, and flexible commercial models are best positioned to capture the expanding wireless healthcare asset management market.

Wireless Healthcare Asset Management Industry Leaders

-

AiRISTA Flow, Inc.

-

Aruba Networks (Hewlett Packard Enterprise Development LP)

-

Ascom Holding AG

-

Awarepoint Corporation

-

CenTrak, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Impinj expanded its RAIN RFID healthcare portfolio with the M900 Speedway reader, which features enhanced interference mitigation for 5G and Wi-Fi 6E environments, helping hospitals achieve 98% tag-read accuracy in high-density wireless zones. Early adopters in the United States, who integrated delivery networks, reduced false-negative reads by 43% compared to older hardware, addressing a critical pain point in operating rooms and emergency departments where spectrum congestion had degraded location precision.

- September 2025: Zebra Technologies completed a USD 180 million acquisition of a European real-time location system software provider to accelerate expansion into the EU market and strengthen Medical Device Regulation traceability compliance. The transaction added 240 hospital customers across Germany, France, and the United Kingdom to Zebra's installed base and brought engineering talent specializing in GDPR-compliant patient proximity tracking, a capability that differentiates the combined entity in privacy-sensitive European procurement processes.

- August 2025: Siemens Healthineers partnered with Microsoft to integrate its Teamplay digital health platform with Azure AI services, enabling predictive maintenance algorithms that analyze equipment telemetry from real-time location system tags to forecast device failures 96 hours in advance. Initial rollouts across 15 academic medical centers in North America and Europe delivered a 31% reduction in unplanned imaging equipment downtime and a 19% improvement in mean time between failures for MRI and CT scanners.

- July 2025: CenTrak secured a USD 52 million contract with a Middle Eastern health authority to deploy UWB real-time location systems across 28 hospitals in Saudi Arabia and the UAE as part of Vision 2030 smart hospital initiatives. The multi-year engagement includes 85,000 asset tags, 12,000 infrastructure anchors, and cloud-based analytics platforms, with implementation scheduled through 2027 to support asset tracking, environmental monitoring, and staff duress applications in facilities ranging from 150 to 800 beds.

- June 2025: Cisco Systems launched DNA Spaces Healthcare 3.0, incorporating UWB support and edge-based AI inference to deliver sub-30 cm location accuracy for surgical instruments and high-value mobile equipment. The platform integrates with Epic and Oracle Cerner EHR systems through pre-built APIs, compressing implementation timelines from 9–12 months down to 4–6 months and enabling hospitals to correlate asset location with patient flow and bed management workflows.

- May 2025: GE Healthcare announced the commercial availability of its Edison Asset Intelligence module, which ingests telemetry from connected imaging devices and flags maintenance needs before they lead to unplanned downtime. The company disclosed that 220 hospitals globally had deployed the platform by mid-2025, collectively achieving a 24% reduction in service costs and a 16 percentage point improvement in equipment uptime, with particularly strong adoption in integrated delivery networks seeking to maximize return on capital-intensive diagnostic equipment.

Global Wireless Healthcare Asset Management Market Report Scope

Wireless Healthcare Asset Management primarily involves using various wireless devices and sensors to track, monitor, and manage the assets used in the healthcare industry, especially hospitals. These devices include asset tags, wearable tags, and wireless sensors. Various technologies in these products make them a suitable solution, including Wi-Fi, RFID, and ZigBee.

Wireless Healthcare Asset Management Market is segmented by Products (asset tags, wearable tags, wireless sensors), by technology (RFID, Wi-Fi, zigBee), and by geography (North America, Europe, Asia-Pacific, and the Rest of the World). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Asset Tags |

| Wearable Tags |

| Wireless Sensors |

| Software Platforms |

| Other Products |

| RFID |

| Wi-Fi |

| Bluetooth Low Energy |

| Ultra-Wideband |

| ZigBee and Other Technologies |

| Asset and Inventory Tracking |

| Patient and Staff Safety |

| Environmental and Condition Monitoring |

| Workflow and Capacity Optimization |

| Compliance and Audit Trail Management |

| Hospitals and Integrated Delivery Networks |

| Ambulatory Surgery Centers |

| Long-Term Care and Senior Living Facilities |

| Diagnostic Laboratories and Imaging Centers |

| Other Healthcare Institutions |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Product | Asset Tags | ||

| Wearable Tags | |||

| Wireless Sensors | |||

| Software Platforms | |||

| Other Products | |||

| By Technology | RFID | ||

| Wi-Fi | |||

| Bluetooth Low Energy | |||

| Ultra-Wideband | |||

| ZigBee and Other Technologies | |||

| By Application | Asset and Inventory Tracking | ||

| Patient and Staff Safety | |||

| Environmental and Condition Monitoring | |||

| Workflow and Capacity Optimization | |||

| Compliance and Audit Trail Management | |||

| By End User | Hospitals and Integrated Delivery Networks | ||

| Ambulatory Surgery Centers | |||

| Long-Term Care and Senior Living Facilities | |||

| Diagnostic Laboratories and Imaging Centers | |||

| Other Healthcare Institutions | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the wireless healthcare asset management market?

The market was valued at USD 74.96 billion in 2026 and is forecast to reach USD 213.88 billion by 2031.

Which product category is growing fastest?

Software Platforms are expanding at 25.95% CAGR as hospitals favor analytics-driven subscriptions.

Why is Ultra-Wideband gaining traction in hospitals?

UWB delivers sub-meter accuracy needed in surgical suites and catheter labs, driving a 26.05% CAGR through 2031.

Which region offers the highest growth opportunity?

Asia-Pacific is advancing at 25.9% CAGR due to government-mandated smart hospital programs in China and India.

How are vendors addressing high upfront costs?

Many suppliers now offer RTLS-as-a-Service models that convert capital expenditure into monthly per-tag fees, easing adoption for cost-sensitive facilities.

Page last updated on: