Wellhead Component Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.03 Billion |

| Market Size (2031) | USD 8.90 Billion |

| Growth Rate (2026 - 2031) | 4.84% CAGR |

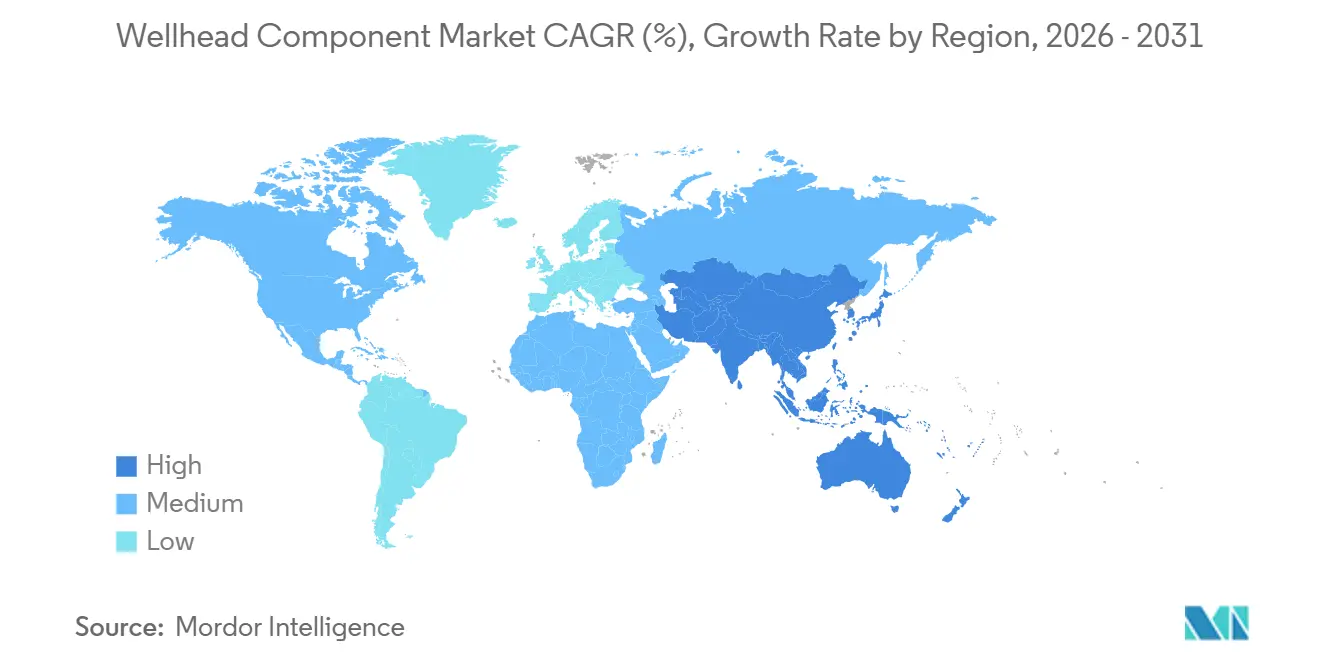

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

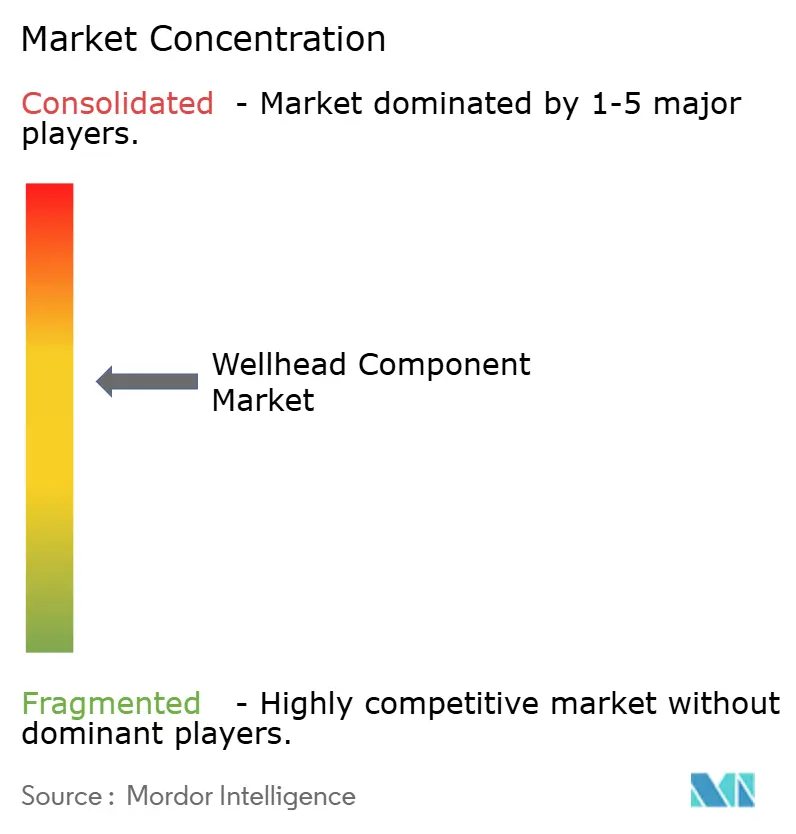

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wellhead Component Market Analysis by Mordor Intelligence

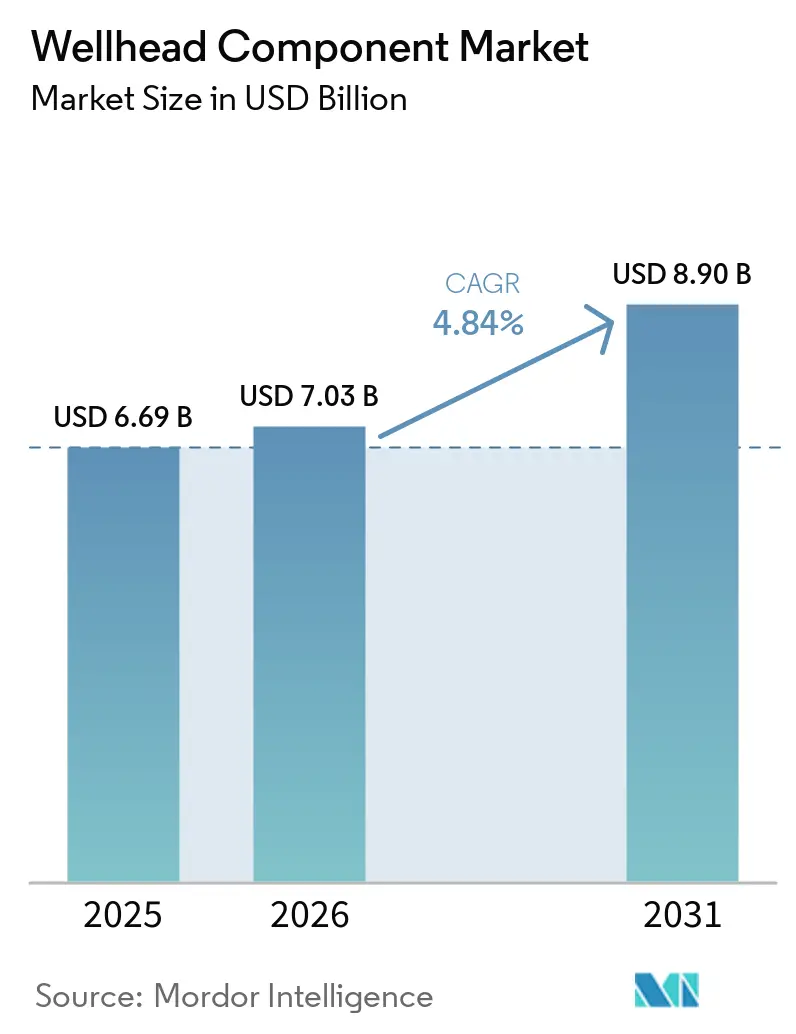

The Wellhead Component Market size is projected to be USD 6.69 billion in 2025, USD 7.03 billion in 2026, and reach USD 8.90 billion by 2031, growing at a CAGR of 4.84% from 2026 to 2031. Capital discipline, deep- and ultra-deepwater project sanctions, and the adoption of predictive-maintenance software shape this measured growth path, replacing the pre-2025 volume-driven expansion cycle. Operators now favor high-integrity, modular wellhead systems that shorten installation schedules, support sour-gas service, and satisfy tighter methane-leak rules issued in 2025 by the U.S. EPA and counterpart agencies in the European Union [1]U.S. Environmental Protection Agency, “Oil and Natural Gas Sector Climate Review Final Rules,” epa.gov. Sustained Brent prices above USD 75 per barrel continue to underpin project economics, yet wellhead spending increasingly follows project breakevens rather than rig counts, a trend underscored by Chevron’s 2026 budget that allocates 60% of upstream capital to Permian and Tengiz sour-service wells requiring specialized 15 000-psi heads [2]Chevron Corp., “2026 Capital and Exploratory Expenditure Guidance,” chevron.com. Ultra-high-pressure subsea platforms, metal-to-metal seal conversions, and turnkey equipment-plus-software bundles from vertically integrated suppliers are the principal avenues for value creation through 2031.

Key Report Takeaways

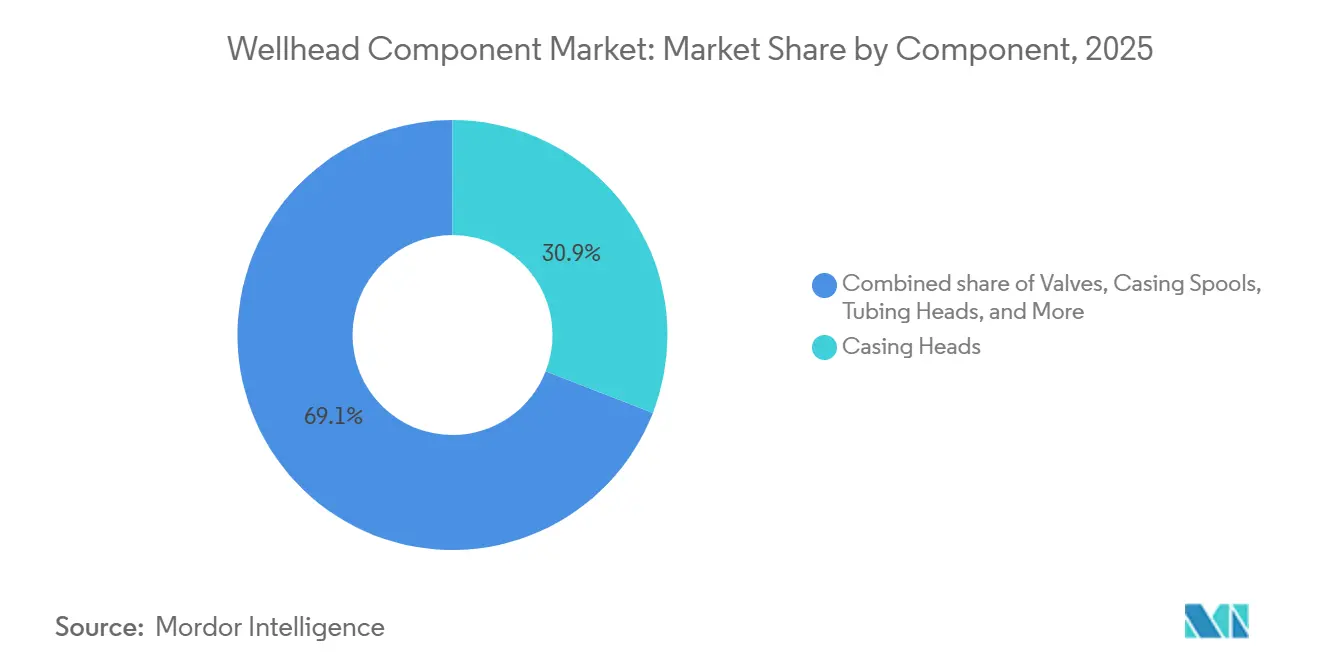

- By component, casing heads accounted for 30.9% of the 2025 wellhead components market share, while valve assemblies are forecast to expand at a 7.5% CAGR through 2031.

- By pressure rating, systems up to 3 000 psi led with 41.5% of the 2025 wellhead components market size, yet equipment rated above 5 000 psi is projected to advance at a 7.9% CAGR over 2026-2031.

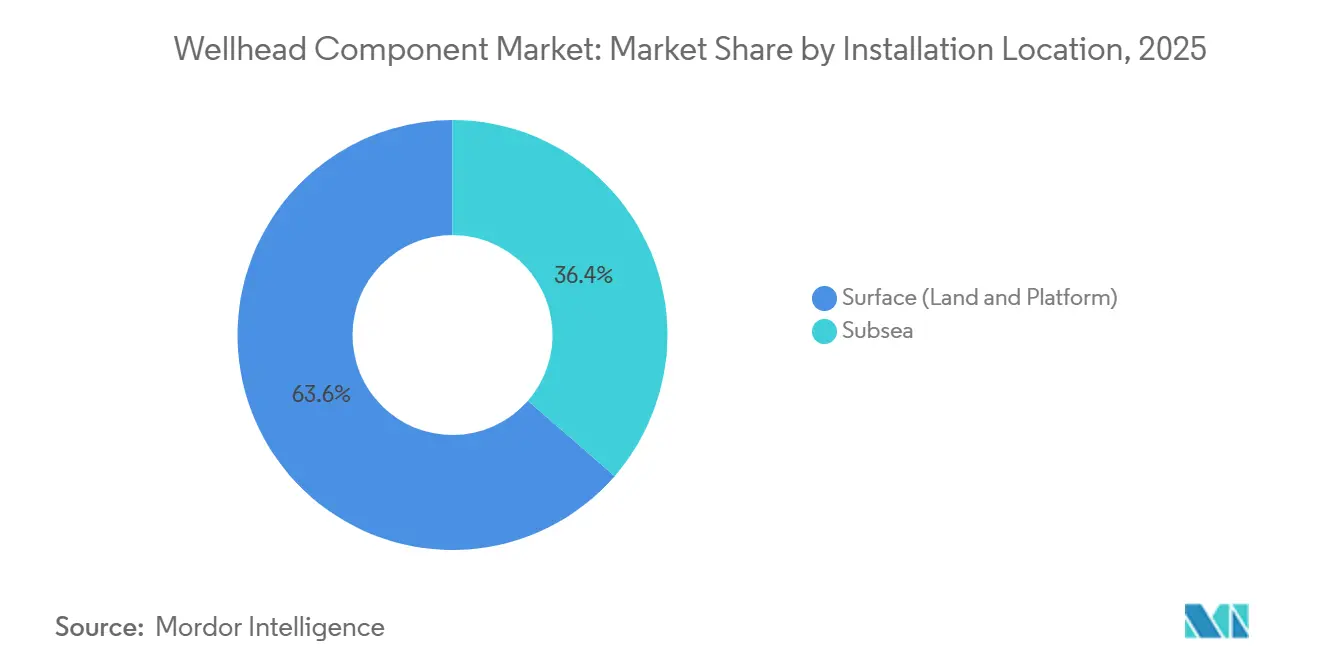

- By installation location, surface wellheads dominated with 63.6% revenue share in 2025, whereas subsea systems are poised for the fastest 8.6% CAGR to 2031.

- By application, onshore drilling captured 78.3% of 2025 demand, but offshore deep and ultra-deep wells are set to register an 8.3% CAGR to 2031.

- By geography, North America held a 40.1% share in 2025, while Asia-Pacific is projected to be the fastest-growing region at a 7.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wellhead Component Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing global E&P activity | +1.2% | Global, strongest in North America & Middle East | Medium term (2-4 years) |

| Higher investment in unconventional shale & tight plays | +1.8% | Primarily North America, expanding to Argentina & Australia | Long term (≥4 years) |

| Deep- & ultra-deepwater project sanctions | +0.9% | Brazil, Gulf of Mexico, West Africa | Long term (≥4 years) |

| Digital-twin predictive maintenance adoption | +0.8% | North America & Europe first movers | Medium term (2-4 years) |

| Modular compact wellhead systems for small LNG tie-backs | +0.6% | Asia-Pacific & Africa | Medium term (2-4 years) |

| CCS well conversions needing retrofit wellheads | +0.4% | North America & Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Global E&P Activity

Selective rebounding of exploration and production budgets in 2025-2026 focused on high-margin resources instead of broad drilling campaigns. Chevron’s USD 18-19 billion 2026 program earmarks 60% for Permian and Tengiz wells that require hydrogen-sulfide-resistant, 15 000-psi heads. Saudi Arabia’s USD 100 billion Jafurah unconventional-gas project targets 2 billion cubic feet per day by 2030 and specifies metal-seal 15 000-psi systems to curb fugitive emissions [3]Saudi Aramco, “Jafurah Gas Field Development Update 2025,” saudiaramco.com. As a result, wellhead demand now follows project breakevens under USD 50 per barrel rather than absolute rig counts, decoupling equipment orders from traditional activity indicators.

Higher Investment in Unconventional Shale & Tight Plays

Efficiency gains of 20-30% in U.S. shale basins during 2025-2026, enabled by longer laterals and dense pad layouts, raised wellhead component consumption per acre. The USD 58 billion Devon-Coterra merger consolidated Permian acreage, optimizing eight-to-12-well pads that place heavier cyclic-pressure loads on casing heads and hangers. Argentina’s Vaca Muerta attracted USD 5 billion of 2025 foreign investment; local-content rules oblige suppliers to partner with Argentine forges, widening lead times and fragmenting the supply chain. China’s Sichuan tight-gas push mandates duplex-stainless heads to manage 15% hydrogen-sulfide streams, creating openings for imported premium-connection technology.

Deep- & Ultra-Deepwater Project Sanctions

A wave of deepwater final investment decisions in 2025-2026 revived demand for 20 000-psi subsea heads. BP sanctioned the USD 5 billion Kaskida field (5 800 ft water, 20 000 psi reservoir), ordering HMH 20 000-psi systems [4]bp PLC, “Kaskida Field Development Plan,” bp.com. Nigeria’s USD 20 billion Bonga North will install more than 200 subsea trees rated at 15 000 psi. Integrated subsea production packages, factory-assembled head-tree-manifold clusters, compress installation schedules by 30-40%, and are now preferred over field-welded configurations. Qatar’s North Field expansion, which reached first gas in mid-2026, validates mega-scale subsea infrastructure with eight platforms and 80-plus completions.

Digital-Twin Predictive Maintenance Adoption

Digital twins migrated from pipelines to wellheads in 2024-2026, letting operators forecast seal wear 6-12 months ahead and cut unplanned shutdowns. Precision Drilling’s 2025 rollout across its North American rigs reduced non-productive time by 18% and lengthened service intervals from three to five years. WellsX’s subscription platform lowered North Sea intervention costs by 25% in early-2026 trials. With an API 6A-Digital interoperability standard due in 2027, competition is shifting from hardware to analytics algorithms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-oil price volatility | -1.1% | Global, acute impact in marginal offshore basins and high-cost shale plays | Short term (≤ 2 years) |

| Stringent environmental & methane-leak regulations | -0.7% | North America (EPA jurisdiction), European Union (Methane Regulation), select Asia-Pacific markets | Medium term (2-4 years) |

| Supply-chain bottlenecks for high-spec alloy forgings | -0.4% | Global, most severe for HPHT and sour-service applications | Short term (≤ 2 years) |

| Cyber-security risks in smart wellhead controls | -0.2% | Global, concentrated in digitally advanced markets (North America, Europe, Middle East) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Oil Price Volatility

Brent fluctuations between USD 55 and USD 85 per barrel through 2025-2026 triggered 15-20% project deferrals in West Africa and Southeast Asia when prices dipped below USD 60. Consolidation, such as the Devon-Coterra deal, concentrates buying power with fewer integrated players, pressuring suppliers to accept lower margins. Standardized, pre-engineered platforms like TechnipFMC’s JXT-3 5 000-psi tree now enable projects to proceed economically even at USD 60 oil.

Stringent Environmental & Methane-Leak Regulations

U.S. EPA Subpart W amendments and NSPS OOOOb rules finalized in 2025 impose quarterly leak detection and <500 ppm thresholds, pushing operators toward zero-leak metal seals. Colorado’s 2025 rule requires packoff replacement by 2028, spawning a 40 000-well retrofit market. Plexus’s POS-GRIP seal won a 2025 North Sea framework because its maintenance-free design satisfies new limits. The EU Methane Regulation, effective in 2026, extends similar standards to LNG imports, globalizing North American compliance norms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Valve Assemblies Lead Innovation Race

Valve assemblies represented the fastest-growing slice of the wellhead components market, forecast to advance at 7.5% CAGR over 2026-2031. Expro’s Solus single-valve shear-and-seal system, API 17G-qualified in 2026, halves installation time and fits smaller BOP stacks, reducing logistics costs by 20-30%. Casing heads accounted for 30.9% of the wellhead components market share in 2025, driven by their essential role in pressure control and maintaining well integrity. However, refurbishment programs and the adoption of digital monitoring technologies are extending their service life, thereby reducing replacement demand. Tubing heads, spools, and hangers are experiencing strong demand due to increased U.S. shale pad drilling activity and the transition to metal-seal interfaces to comply with methane-emission regulations. Adapter spools are also seeing increased adoption as operators upgrade legacy wells to ensure compatibility with advanced tree systems. Additionally, suppliers offering integrated packages that combine valves, seals, and sensing modules are enhancing their competitive position in the wellhead components market.

The push toward integrated component suites is strongest in deepwater tie-backs, where operators prefer single-source warranties. Plexus’s 2025 licensing of POS-GRIP to Schlumberger and TechnipFMC expands metal-seal availability and positions the technology for 15-20% of U.S. retrofit demand by 2028. Meanwhile, Cactus Wellhead’s 2026 purchase of 65% of Baker Hughes’ surface pressure-control line boosts its ability to supply turnkey head-plus-valve kits throughout the Middle East and Latin America. As digital twins become standard, hardware differentiation will hinge on embedded sensor arrays that can feed predictive-maintenance platforms over a 20-year field life.

By Pressure Rating: Ultra-High Systems Capture Deepwater Premium

Ultra-high-pressure equipment (above 5 000 psi) is projected to grow at 7.9% CAGR, fueled by 20 000-psi Gulf of Mexico, Brazil pre-salt, and Nigeria deepwater fields. Chevron’s Anchor pilot, which came onstream in 2024 using 20 000-psi heads, proved the technology’s reliability at 7 000 ft water depth. Dril-Quip’s BigBore II 20 000-psi mudline design subsequently secured 2025-award slots in West Africa. Low-pressure heads (≤3,000 psi) are projected to account for 41.5% of the wellhead components market size in 2025. This is attributed to their extensive use in mature onshore fields. However, growth is slowing as basin development nears saturation in several established production regions.

Mid-range 3 001-5 000 psi systems demand remains standard for Southeast Asian and Middle Eastern shelf gas, where water depth is 100-400 ft, and costs matter. TechnipFMC’s JXT-3 tree, 5 000 psi-rated yet 40% lighter than conventional designs, secured Malaysia BIGST and Indonesia Mako gas awards in 2025. The Gulf of Mexico, Brazil, and Nigeria specify 15 000-20 000 psi heads, while onshore Middle East and North America continue to reorder ≤3 000 psi designs for infill wells.

By Installation Location: Subsea Systems Redefine Tie-Back Economics

Subsea wellheads are expected to post the segment-leading 8.6% CAGR as operators convert offshore finds into unmanned tie-backs and avoid USD 500 million-plus fixed platforms. Qatar’s North Field added 80 subsea completions by mid-2026, underscoring this pivot. Surface heads accounted for 63.6% of the projected 2025 revenue, driven by widespread use in conventional and shale drilling operations. However, growth is slowing as major shale programs reach maturity.

Modular compact heads now enable 6-9 month subsea schedules versus 12-18 months earlier. Equinor’s Verdande tie-back, onstream in 2026 after a NOK 6 billion outlay, sourced local Norwegian fabrication and achieved a 12-month equipment cycle. Baker Hughes and Tecnimont’s 2026 MoU couples NMBL LNG modules with 5 000-10 000 psi plug-and-play subsea systems, opening a new front for cost-effective small-scale gas monetization.

By Application: Offshore-Deep Segment Rides Mega-Project Wave

Onshore drilling accounted for 78.3% of the projected demand in 2025, driven by extensive development programs in the Permian, Jafurah, and Sichuan basins. However, growth in onshore drilling is gradually slowing as mature regions prioritize efficiency improvements and refurbishment strategies. In comparison, offshore deepwater and ultra-deepwater activities are expanding, supported by significant projects such as BP’s Kaskida-Tiber hub, Petrobras’ Búzios 9 and Mero 4 FPSOs, and Vietnam’s Lac Da Vang development.

Deepwater heads sell for USD 4-6 million each versus USD 200 000-500 000 for surface units, giving the segment an outsized share of incremental revenue. CCS conversions add a niche but fast-growing outlet: Talos Energy’s Bayou Bend began retrofitting legacy wells with CO₂-rated, corrosion-resistant heads in 2026. Offshore deepwater developments and CCS retrofit projects are anticipated to be significant drivers of growth in the wellhead components market value through 2031.

Geography Analysis

North America controlled 40.1% of 2025 revenue, anchored by 4 500 Permian spuds and resurging Gulf of Mexico deepwater sanctions. Yet, regional growth is slowing due to the depletion of tier-1 shale inventory and a growing focus on capital investment in deepwater projects in Brazil and West Africa. Canada’s Bay du Nord (first oil 2028) will add niche demand for cold-water-rated heads, whereas Mexico’s shallow-water tenders languish under tight fiscal terms.

Asia-Pacific is the fastest-growing territory at a 7.3% CAGR thanks to Indonesia’s Northern Hub (6.6 tcf), Malaysia’s BIGST (800 MMcfd), and Vietnam’s deepwater campaign that logged first oil at Lac Da Vang in Q4 2026. Papua LNG, Scarborough LNG, and China’s South China Sea blocks collectively require 150-plus subsea heads by 2028, but local-content and alloy-forging gaps extend lead times to 18-24 months.

In Europe. Norway’s Johan Sverdrup Phase 3 (FID 2025) and the U.K.’s Rosebank (first oil 2026) keep a residual flow of high-spec orders, while Plexus’s 2025 North Sea framework exploits plug-and-abandonment demand.

In the Middle East and Africa, Saudi Aramco’s Jafurah program alone necessitates thousands of 15 000-psi heads through 2030, and ADNOC’s Hail & Ghasha sour-gas project, financed in 2025, requires corrosion-resistant alloy heads rated at 15 000 psi. Nigeria’s Bonga North and Angola’s new pre-salt probes add deepwater growth, although political and local-content hurdles stretch schedules. The

South America market is rising on the strength of Brazil’s pre-salt complex, which delivered Búzios 9 and Mero 4 FPSOs in 2026, each tied to 8-12 subsea wells equipped with 15 000-psi systems. Argentina’s YPF-Petronas LNG joint venture, targeting FID 2025, underpins 20 000 new shale wellheads by 2030, provided macro-economic stability holds.

Competitive Landscape

The Wellhead Component Market is semi-consolidated. Cactus Wellhead’s January 2026 acquisition of 65% of Baker Hughes’ surface pressure-control business for USD 344.5 million widens its turnkey offering and reinforces Middle Eastern and Latin American reach. Integrated service providers increasingly acquire niche technologists to fuse hardware with software, shifting competition toward lifecycle contracts that guarantee uptime rather than one-time equipment margins.

Plexus’s POS-GRIP metal-seal technology, licensed to Schlumberger and TechnipFMC in 2025, delivers zero-maintenance performance aligning with EPA methane rules and could secure 15-20% of North American retrofit activity by 2028. Expro’s 2026 Solus single-valve system shortens subsea installations by up to 50% and allows operators to charter smaller intervention vessels, a logistics saving particularly valuable in the North Sea. Digital-twin platforms from WellsX and Precision Drilling are carving out 10-15% subscription revenue streams as API readies its 6A-Digital sensor standard for 2027.

Forum Energy Technologies, which generated USD 196 million revenue in Q3 2025 with a 1.12 book-to-bill, competes on nine- to 12-month lead times and flexible pricing, resonating with independent E&Ps. High-nickel alloy forging shortages remain a bottleneck, stretching deliveries of NACE MR0175-compliant heads to 12-16 months and favoring suppliers with captive mill capacity. Carbon-capture retrofits, such as Talos Energy’s Bayou Bend CCS (1.35 Mt CO₂ per year, start-up 2026), represent an emerging niche that large incumbents have yet to address at scale.

Wellhead Component Industry Leaders

Schlumberger

Halliburton

Baker Hughes

TechnipFMC

NOV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: SLB announced that it had clinched two five-year contracts with Petroleum Development Oman (PDO) for the supply of wellheads and artificial lift systems for Block 6. As per the contract terms, SLB is set to provide a range of products, including low-pressure, high-pressure, and thermal wellheads, alongside electric submersible pumps and progressive cavity pumps.

- July 2025: CNOOC announced the commencement of production at the Kenli 10-2 offshore oilfield. The development includes multiple wellhead platforms and 79 planned wells. This project is significant as it represents one of China’s largest offshore heavy oil developments and incorporates advanced thermal recovery systems integrated with wellhead infrastructure. Production is anticipated to peak in 2026, driving demand for offshore wellhead components.

- June 2025: Baker Hughes announced the sale of a 65% stake in its Surface Pressure Control (SPC) business to a unit of Cactus Inc. The SPC unit encompasses wellhead systems and production tree equipment, which are essential components of wellhead operations. A joint venture was established, with Baker Hughes retaining a 35% ownership stake. This transaction aims to streamline Baker Hughes' portfolio and expand Cactus' international wellhead presence, particularly in the Middle East. The deal underscores industry trends toward consolidation and specialization in wellhead technologies.

- February 2025: Baker Hughes landed multi-service awards from Petrobras for pre-salt developments, including well construction, workover support, and flexible pipe supply through 2029.

Global Wellhead Component Market Report Scope

Wellhead components play a critical role in ensuring safe and efficient well operations by providing structural integrity, pressure containment, and flow control. These components are essential during the drilling, completion, and production phases of oil and gas wells.

The global wellhead component market is segmented by component, pressure rating, installation location, application, and geography. By component, the market is segmented into casing heads, casing spools, tubing heads, hangers, valves, seals and gaskets, and adapter spools. By pressure rating, the market is segmented into up to 3,000 psi, 3,001 to 5,000 psi, and above 5,000 psi. By installation location, the market is segmented into surface and subsea. By application, the market is segmented into onshore, offshore-shallow, and offshore-deep/ultra-deep. The report also covers the market sizes and forecasts for the global wellhead component market across major countries across key regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been provided on the basis of value (USD).

| Casing Heads |

| Casing Spools |

| Tubing Heads |

| Hangers |

| Valves |

| Seals and Gaskets |

| Adapter Spools |

| Up to 3,000 psi |

| 3,001 to 5,000 psi |

| Above 5,000 psi |

| Surface (Land and Platform) |

| Subsea |

| Onshore |

| Offshore - Shallow |

| Offshore - Deep/Ultra-deep |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Component | Casing Heads | |

| Casing Spools | ||

| Tubing Heads | ||

| Hangers | ||

| Valves | ||

| Seals and Gaskets | ||

| Adapter Spools | ||

| By Pressure Rating | Up to 3,000 psi | |

| 3,001 to 5,000 psi | ||

| Above 5,000 psi | ||

| By Installation Location | Surface (Land and Platform) | |

| Subsea | ||

| By Application | Onshore | |

| Offshore - Shallow | ||

| Offshore - Deep/Ultra-deep | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the wellhead components market by 2031?

The market is forecast to reach USD 8.90 billion by 2031 at a 4.84% CAGR.

Which component category is expected to grow the fastest?

Valve assemblies are projected to record the highest 7.5% CAGR through 2031.

Which pressure-rating segment will lead revenue growth?

Ultra-high-pressure heads rated above 5 000 psi will grow the quickest at a 7.9% CAGR.

Why are subsea wellhead systems gaining momentum?

Subsea heads enable unmanned tie-backs that avoid platform costs and are expected to expand at an 8.6% CAGR through 2031.

Which region offers the strongest growth outlook?

Asia-Pacific is forecast to grow at a 7.3% CAGR, outpacing all other regions through 2031.

How will environmental regulations influence product design?

Stricter methane-leak limits in the U.S. and EU are accelerating the shift to metal-to-metal seals and digital leak-detection sensors.

Page last updated on: