Voice Biometrics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

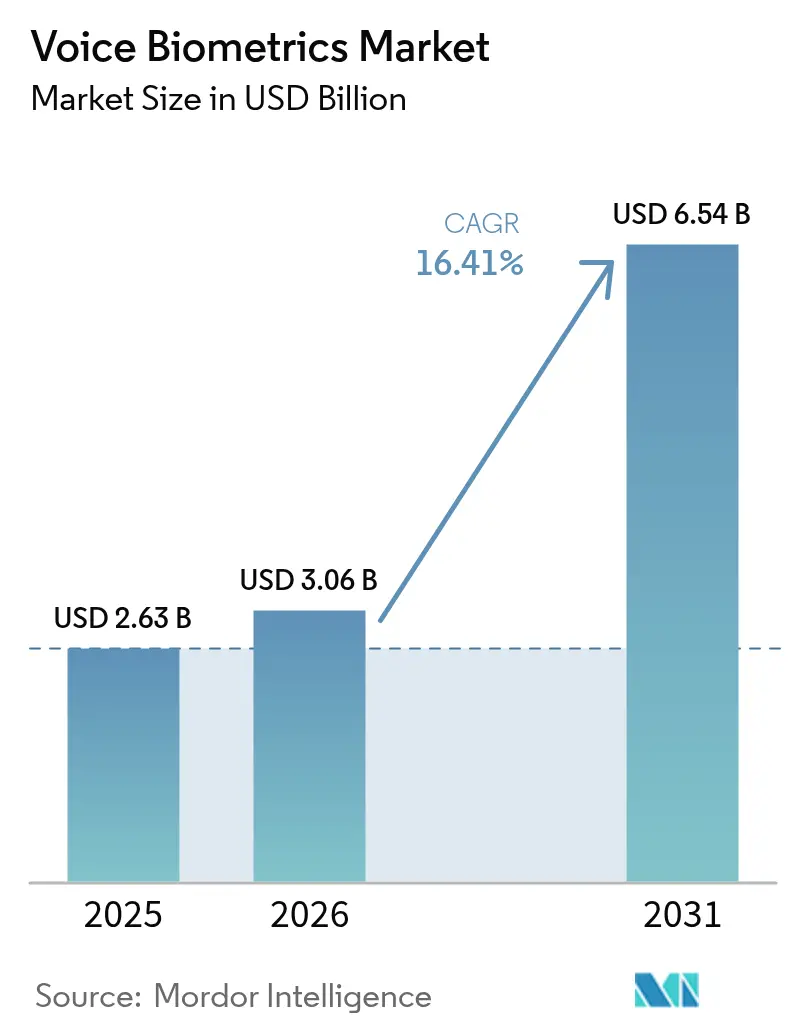

| Market Size (2026) | USD 3.06 Billion |

| Market Size (2031) | USD 6.54 Billion |

| Growth Rate (2026 - 2031) | 16.41% CAGR |

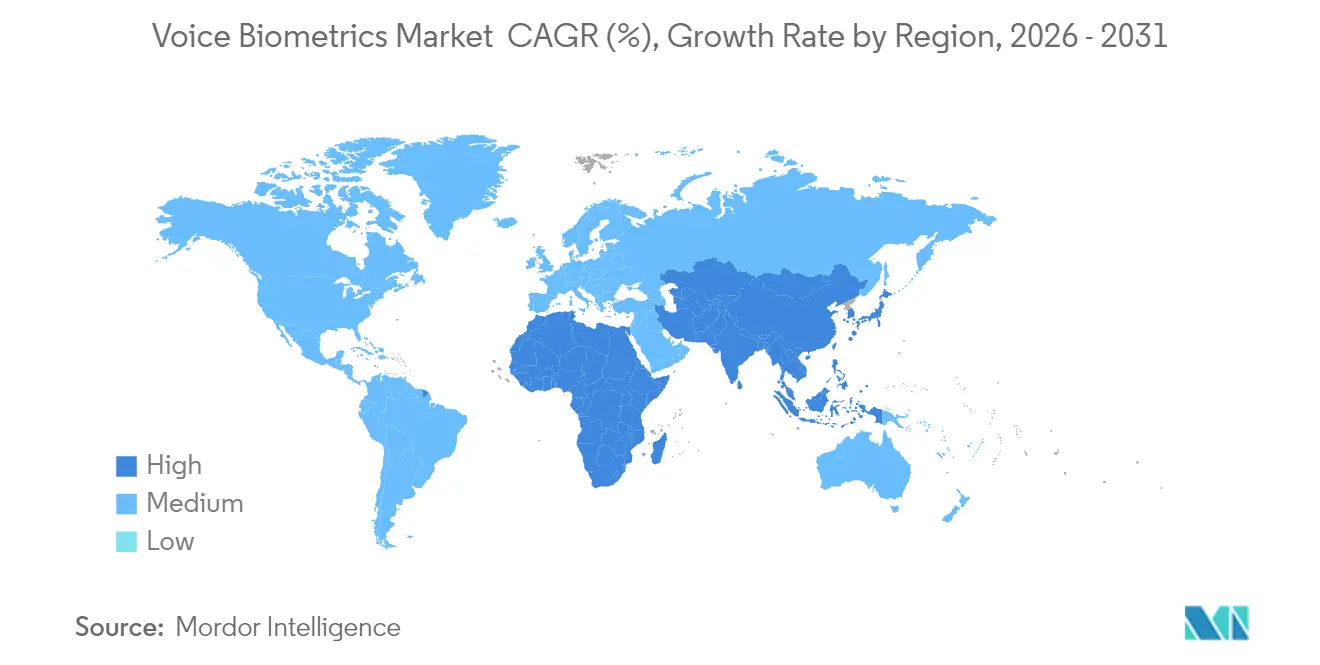

| Fastest Growing Market | Asia |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Voice Biometrics Market Analysis by Mordor Intelligence

The voice biometrics market size is expected to grow from USD 2.63 billion in 2025 to USD 3.06 billion in 2026 and is forecast to reach USD 6.54 billion by 2031 at 16.41% CAGR over 2026-2031. Demand is rising because cyber-criminals now weaponize artificial intelligence, social engineering, and synthetic speech, rendering passwords unreliable. Financial institutions, telecom operators, and government agencies respond by replacing knowledge-based questions with real-time voice verification. Wider 5G coverage, edge AI chips in smartphones, and lower cloud inference costs also sustain adoption. Regulatory authorities classify voiceprints as sensitive personal data, so organizations must combine privacy-by-design practices with anti-spoofing analytics. Vendor consolidation is underway as platform players integrate biometrics into zero-trust toolkits, while specialist firms supply deepfake detection modules and multilingual models tuned for low-resource dialects.

Key Report Takeaways

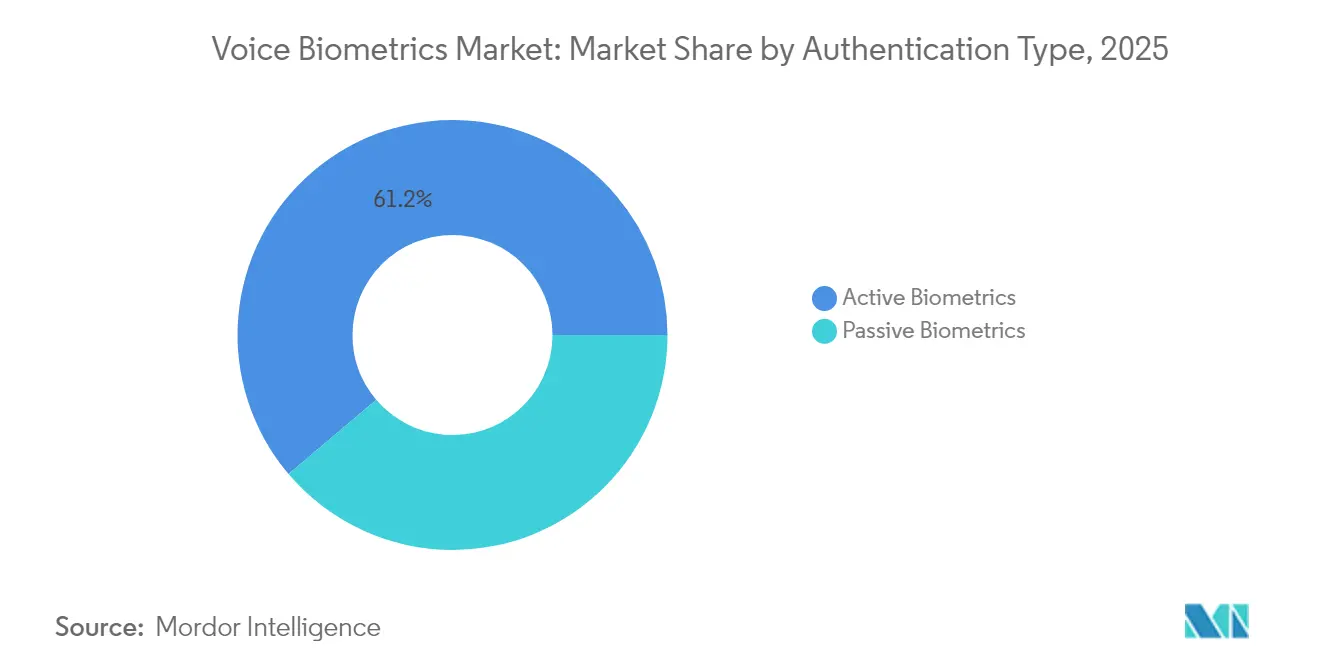

- By authentication type, active solutions held 61.20% of the voice biometrics market share in 2025; passive solutions are projected to expand at an 18.36% CAGR to 2031.

- By component, software captured 69.10% revenue share in 2025, whereas services are on track to grow at 18.02% CAGR through 2031.

- By deployment model, cloud accounted for 67.10% share of the voice biometrics market size in 2025 and is forecast to climb at an 17.74% CAGR between 2026-2031.

- By enterprise size, large organizations led with 57.20% share in 2025; small and medium businesses are expected to post 18.89% CAGR to 2031.

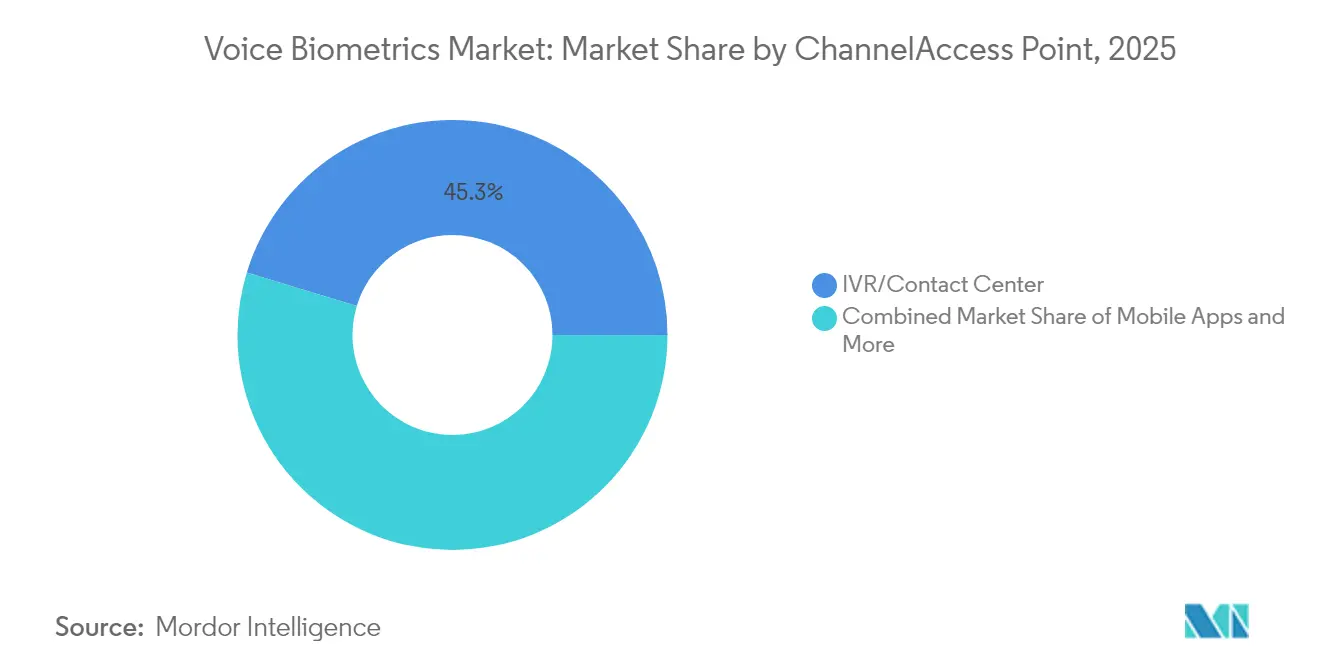

- By channel, IVR and contact centers led with 45.30% share of the voice biometrics market size in 2025, while mobile apps should record a 19.62% CAGR to 2031.

- By end-use industry, BFSI commanded 31.40% of the voice biometrics market share in 2025, and healthcare is projected to progress at 19.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Voice Biometrics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Transition to password-less authentication in mobile banking | +3.2% | North America, Europe, APAC spillover | Medium term (2-4 years) |

| Regulatory pressure for strong customer authentication | +2.8% | EU, India, United States | Short term (≤ 2 years) |

| Deepfake-driven contact-center upgrades | +4.1% | North America, Europe | Short term (≤ 2 years) |

| Fintech-led payment growth in emerging Asia | +2.5% | India, China, ASEAN-5 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Transition to password-less authentication in mobile banking

Banks and e-wallet providers substitute static passwords with voiceprints to decrease abandonment during log-in and to stop account-takeover fraud. 81% of contact-center leaders already deploy or plan voice verification, and flagship institutions such as Bank of Ireland invested USD 36 million to embed voice checks into interactive voice response menus.[1]Biometric Update, "Bank of Ireland to introduce voice biometrics to authentication for phone interactions", biometricupdate.com The method suits small screens where typing is slow and error-prone, while continuous authentication during a call trims handle time and removes one-time codes.

Regulatory pressure for strong customer authentication

Rules such as PSD2, the Reserve Bank of India’s guidelines, and US instant-payment rails oblige financial firms to prove user identity with at least two independent factors. Voice biometrics adds an inherent layer that satisfies compliance without extra hardware for customers. The EU Artificial Intelligence Act labels voice verification a high-risk category, obliging providers to document model governance, bias testing, and incident response, accelerating procurement of certified platforms.[2]European Parliament, "Regulation (EU) 2024/1689 of the European Parliament and of the Council of 13 June 2024 Laying Down Harmonised Rules on Artificial Intelligence", eur-lex.europa.eu

Deepfake-driven contact-center upgrades

Synthetic speech now imitates senior executives with near-perfect prosody, enabling large-scale fraud. A USD 25 million heist in 2024 revealed gaps in caller validation, leading enterprises to augment existing speaker recognition with real-time deepfake scoring and voice-liveness checks.[3]Reality Defender, "Contact Center Security - Reality Defender", realitydefender.comSpecialist engines compare spectral cues and emotional variance to flag cloned audio, and managed-service outsourcers integrate these APIs to reopen customer lines with lower friction.

Fintech-led payment growth in emerging Asia

Super-apps and payment banks scale across India and Southeast Asia, enrolling first-time digital users who may not possess high-quality identity documents. Voice verification, agnostic to literacy and compatible with local dialects, simplifies KYC and supports inclusive onboarding. Government incentive schemes for open banking and real-time payments further encourage providers to embed voice authentication into mobile flows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bias in multilingual and dialect-rich models | −1.8% | India, EU, Africa | Medium term (2-4 years) |

| Data-residency rules limiting cloud deployment | −2.2% | EU, Middle East, Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Bias in multilingual and dialect-rich models

Academic benchmarks show higher word-error rates for under-represented accents, genders, and age groups, triggering fairness debates. Disparities erode trust, slow public roll-outs, and may breach equality directives. Vendors now widen training corpora, run periodic bias audits, and issue transparent model cards to reassure regulators and civil-society observers.

Data-residency rules limiting cloud deployment

The GDPR and similar statutes classify voiceprints as sensitive data, forcing providers to process and store records within specific jurisdictions. Cloud hyperscalers respond by opening sovereign zones and offering customer-managed encryption keys, yet enterprises sometimes default to on-premise nodes, increasing capital expenditure and lengthening procurement cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Authentication Type: Passive adoption accelerates frictionless security

Passive verification analyzed less than 40% of the voice biometrics market in 2025, yet is forecast to grow faster than the headline rate, moving at 18.36% CAGR. Its appeal lies in authenticating callers during natural conversation, eliminating scripted phrases, and shaving up to 45 seconds from average handle-time. The Credit Union of Colorado confirmed time savings after replacing keypad questions. Active methods retain 61.20% leadership because mandated phrases deliver robust audit trails critical for high-value transfers and government clearances. Hybrid stacks are emerging that trigger active fallback only when risk scores exceed tolerance.

Passive solutions benefit from advances in real-time signal processing and speaker diarization running on edge devices. Continuous monitoring throughout a session also helps detect account sharing and coercion. Meanwhile, active engines innovate with shorter passphrases and promptless verification on supported handsets. The two branches together reinforce the voice biometrics market as enterprises mix assurance and usability.

By Component: Services revenue expands as integration complexity rises

Software still provided 69.10% of spending in 2025 thanks to core speech-feature extraction libraries and model-management consoles. Yet professional and managed services are projected to advance 18.02% CAGR, reflecting the need to fine-tune engines for dozens of languages, connect to legacy IVR platforms, and run red-team tests against deepfake attacks. Telecom-business-process outsourcers partner with niche algorithm suppliers to offer turnkey packages that bundle hosting, tuning, and continuous fraud monitoring.

Consultants also steer clients through evolving privacy law, draft data-protection-impact assessments, and design consent flows. Managed-service contracts include rapid-response teams for breach events and quarterly bias reporting. As these engagements mature, outcome-based pricing linked to fraud-loss reduction gains traction, embedding service revenue deeper into the voice biometrics market.

By Deployment Model: Cloud retains the scale advantage

Cloud nodes process 67.10% of traffic today and will maintain dominance with an 17.74% CAGR, supported by elastic compute for deep-learning inference and pay-per-use economics for seasonal contact-center peaks. Continuous model updates detect novel spoof vectors sooner than appliance refresh cycles. Nonetheless, critical sectors deploy hybrid topologies that route low-risk transactions through regional clouds while storing enrolment templates on-premise behind hardware-security-modules.

EU data-sovereignty directives and Middle East financial regulators push vendors to certify local hosting and offer zero-knowledge architectures. Government agencies occasionally opt for fully isolated installations, as illustrated by the US Department of Veterans Affairs biometric-access pilot where sensitive enrolment data never leaves federal premises. These blended approaches further diversify the voice biometrics market.

By Enterprise Size: SMBs close the capability gap

Large organizations held 57.20% share in 2025 because they could fund bespoke integrations and extensive user-acceptance tests. Yet SMB adoption is accelerating at 18.89% CAGR as vendors launch subscription bundles with usage-based pricing and low-code APIs. Voice biometrics as a service reduces procurement friction, and pre-configured risk policies suit regional banks, medical clinics, and e-commerce merchants.

At the upper end, multinational corporations integrate speaker recognition into zero-trust access gateways, cutting password-reset tickets and insider-threat exposure. Thirty percent of enterprises that replaced passwords with multimodal biometrics report measurable declines in credential-stuffing incidents. This dual-segment momentum reinforces sustained expansion for the voice biometrics market.

By Channel/Access Point: Mobile apps outpace legacy IVR

Interactive-voice-response and agent-handled calls still account for 45.30% of deployments because fraudsters target telephone banking. Yet mobile applications are climbing at 19.62% CAGR on the back of digital-first consumer behavior. Amazon Pay India pilots voice checkout flows that work across regional languages and noisy environments. Developers embed voice verification into mobile SDKs alongside device-binding and behavioral-biometric signals to create layered defences.

Smart-home assistants represent an exploratory domain. Studies show background speech can trigger false accepts, prompting research into directional microphones and context-aware models. Kiosks in hospitals and government offices use speaker recognition to streamline check-in while satisfying accessibility standards. These diverse access points amplify surface area yet also expand total addressable revenue within the voice biometrics market.

By End-use Industry: Healthcare demand gathers pace

BFSI remains the anchor vertical with 31.40% revenue because account-takeover losses directly threaten capital ratios. Regulators encourage biometric controls, and many banks market voice prints as customer-friendly. Healthcare, however, is forecast to post a 19.05% CAGR, propelled by telemedicine, e-prescription access, and clinician single-sign-on to electronic medical records. The MATCH IT Act prioritizes correct patient identification, making frictionless voice checks attractive during virtual consultations.

Government, law enforcement, and border management employ voice biometrics for inmate monitoring and remote probation check-ins. Retailers explore voice-activated payments to quicken checkout and personalize offers. Each domain contributes unique requirements, yet combined they broaden use-case diversity, underpinning resilient growth across the voice biometrics market.

Geography Analysis

North America holds the largest portion of the voice biometrics market owing to early adoption by banks, card networks, and healthcare providers. Federal rules classify voiceprints as sensitive identifiers, so vendors deploy FedRAMP-authorized clouds and encryption to satisfy agency audits. Contact-center modernization funded under corporate cyber-resilience budgets further boosts demand. Venture capital also backs speech-security startups, keeping innovation local.

Asia Pacific is the swiftest-growing region. India’s unified-payments interface and rapid smartphone uptake create fertile ground for inclusive, language-agnostic authentication. China scales speaker recognition across super-app ecosystems, while ASEAN telcos embed voice liveness to curb SIM-swap fraud. Regional data-localization laws encourage joint ventures that host models inside national borders, stimulating domestic capacity.

Europe combines advanced infrastructure with the world’s strictest privacy framework. The Artificial Intelligence Act designates speaker recognition as high-risk, so enterprises procure certified toolkits with explainable inference and detailed audit logs. Investment announcements such as Bank of Ireland’s EUR 34 million (USD 36 million) program show that budget still flows where compliance and customer convenience intersect.

Latin America and Africa trail in absolute spend but present sizable upside. Telecom operators in Brazil and South Africa deploy voice-enabled IVR to cut agent workload and verify prepaid subscribers. Independent tower roll-outs have improved 4G coverage, enabling cloud inference. Local accent diversity and low-resource languages are challenges that vendors address through transfer learning and regional datasets, thereby extending reach of the voice biometrics market.

Competitive Landscape

Industry structure is moderately concentrated. Microsoft’s 2022 purchase of Nuance embedded voice prints into the Azure trust portfolio, giving the platform economy a strong foothold. Specialist vendors such as Pindrop, Veridas, and Reality Defender differentiate with spoof-resistant spectral analysis, multilingual engines, and streaming deepfake detection. These firms target compliance-driven sectors seeking certified accuracy rather than generalist speech services.

Strategic moves emphasize ecosystem partnerships. HGS paired with ValidSoft to offer managed contact-center security, aligning product, delivery, and outcome metrics. Auraya upgraded its EVA engine with deepfake heuristics, signalling continuous innovation to protect installed bases. Y Combinator funds early-stage ventures that package voice AI into developer-friendly APIs, accelerating diffusion into long-tail applications.

White-space remains in verticalized solutions for healthcare, public safety, and retail. Vendors capable of supplying full stacks—enrolment, storage, analysis, and privacy controls—are positioned to capture share as clients rationalize point tools. Patent filings on liveness cross-checks and speech-content correlation imply sustained defensive investment, consolidating intellectual property around core algorithms and reinforcing entry barriers across the voice biometrics market.

Voice Biometrics Industry Leaders

-

Nuance Communications Inc.

-

NICE Ltd

-

Verint Systems Inc.

-

Pindrop Security Inc.

-

LexisNexis Risk Solutions Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: HGS partnered with ValidSoft to deploy a managed contact-center solution that combines voice authentication with synthetic speech analytics, aiming to cut fraud losses and shorten call times.

- May 2025: Bank of Ireland allocated EUR 34 million (USD 36 million) to add voice verification to phone and CRM channels, seeking faster queries and lower impersonation risk.

- May 2025: US Department of Veterans Affairs initiated a biometric access pilot using face and iris recognition, with expansion paths toward voice enrolment for multi-facility staff access.

- January 2025: Auraya Systems enhanced EVA with advanced deepfake detection to strengthen real-time spoof mitigation capabilities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the voice biometrics market as all software, SDKs, and managed services that capture and match a speaker's distinctive acoustic and behavioral patterns to authenticate or identify a person across digital and telephony channels. Valuation is expressed in USD and reflects end-user spending on new deployments plus recurring licenses and maintenance.

We exclude pure speech-to-text engines, voice assistants that do not perform identity verification, and hardware-only microphone arrays.

Segmentation Overview

-

By Authentication Type

- Active Biometrics

- Passive Biometrics

-

By Component

- Software/SDK

- Services (Integration, Consulting, Managed)

-

By Deployment Model

- Cloud

- On-premise

-

By Enterprise Size

- Small and Medium Enterprises

- Large Enterprises

-

By Channel/Access Point

- IVR/Contact Center

- Mobile Apps

- Web and Kiosk

- Smart Devices/IoT

-

By Application

- Fraud Detection and Prevention

- Customer Authentication and IDandV

- Payments and Transaction Security

- Workforce Management/Logical Access

-

By End-use Industry

- Banking, Financial Services and Insurance

- Government and Law Enforcement

- Telecom and IT

- Healthcare

- Retail, E-commerce and CPG

- Transport and Logistics

- Others (Education, Hospitality)

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

-

APAC

- China

- India

- Japan

- South Korea

- ASEAN-5

- Australia

- New Zealand

- Rest of APAC

-

Middle East

- GCC

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Nigeria

- Rest of Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed information-security leads at North American and Asia-Pacific banks, telecom product managers, and identity-platform engineers to stress-test adoption rates, typical license fees, anti-spoofing upgrade costs, and regional compliance triggers, which closed gaps seen in secondary findings.

Desk Research

We began with national cyber-crime statistics from the US Federal Trade Commission, the UK National Fraud Intelligence Bureau, and INTERPOL, supplemented by regulatory texts like Europe's PSD2 strong-customer-authentication rule. White papers from the FIDO Alliance, ETSI, and the Biometrics Institute, patent analytics sourced through Questel, and annual reports of major banks and telecom operators supplied baseline volumes, pricing clues, and technology road maps. Additional context came from business media feeds in Dow Jones Factiva and call-center traffic data released by the US FCC. This list is illustrative, not exhaustive.

Market-Sizing & Forecasting

We apply a top-down addressable-account model that converts reported contact-center call minutes, digital banking user counts, and smartphone shipments into potential authentication events, then multiplies these by verified penetration rates and average price per verification. Supplier roll-ups and sample price-times-volume checks act as a pragmatic bottom-up counterpoint that adjusts totals where under-reported. Key forecast drivers, such as e-commerce transaction growth, fraud incidence trends, regulatory deadlines, and the shift to cloud delivery, feed a multivariate regression projecting demand through 2030. When source data are missing, regional analogues and expert consensus guide careful interpolation.

Data Validation & Update Cycle

Our outputs move through anomaly flags, senior-analyst peer review, and a final cross-check against independent metrics such as patent filings and venture funding. Our model refreshes annually, and interim updates occur when material events, for example, a deepfake fraud surge, alter base assumptions.

Why Mordor's Voice Biometrics Baseline Commands Confidence

We acknowledge that published estimates often diverge, and we preview the scope limits, currency bases, and refresh cadences that usually create such gaps.

We observe that other studies may bundle speech analytics revenue, apply aggressive price erosion, or freeze assumptions for several years, while Mordor recalibrates inputs after each regulatory or technology inflection.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.63 B (2025) | Mordor Intelligence | - |

| USD 2.30 B (2024) | Global Consultancy A | Bundles voice recognition hardware and speech-to-text services |

| USD 2.39 B (2025) | Industry Research Firm B | Uses static license price and limited primary validation |

| USD 2.27 B (2024) | Regional Consultancy C | Relies on a single top-down model and excludes cloud subscription renewals |

These comparisons show that Mordor's balanced scope selection, dual-path validation, and timely refresh deliver a dependable baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is driving the rapid expansion of the voice biometrics market?

Rapid growth stems from deepfake fraud escalation, password fatigue, and new regulations that mandate multi-factor authentication, pushing enterprises toward voiceprints for secure yet user-friendly identity checks.

How large is the voice biometrics market size today and where is it heading?

The voice biometrics market size stands at USD 3.06 billion in 2026 and is projected to reach USD 6.54 billion by 2031, reflecting a 16.41% CAGR.

Which region is expected to grow fastest in voice authentication adoption?

Asia Pacific shows the highest trajectory as fintech apps, digital identity schemes, and inclusive banking initiatives accelerate demand across India, China, and ASEAN economies.

Why are passive voice biometrics solutions gaining momentum over active methods?

Passive engines verify speakers during natural conversation, cutting call-handling time and improving user experience, while advances in real-time spectral analysis close historical accuracy gaps.

How do data-residency laws influence deployment choices?

Strict sovereignty requirements push some organizations toward hybrid or on-premise setups, even though cloud remains dominant for scalability; vendors now offer regional hosting and customer-controlled keys to comply.

Which industries beyond banking show strong uptake potential for voice authentication?

Healthcare is moving quickly to secure telehealth and electronic records, while retail and public sector services explore voice-enabled payments and secure citizen verification respectively.

Page last updated on: