Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

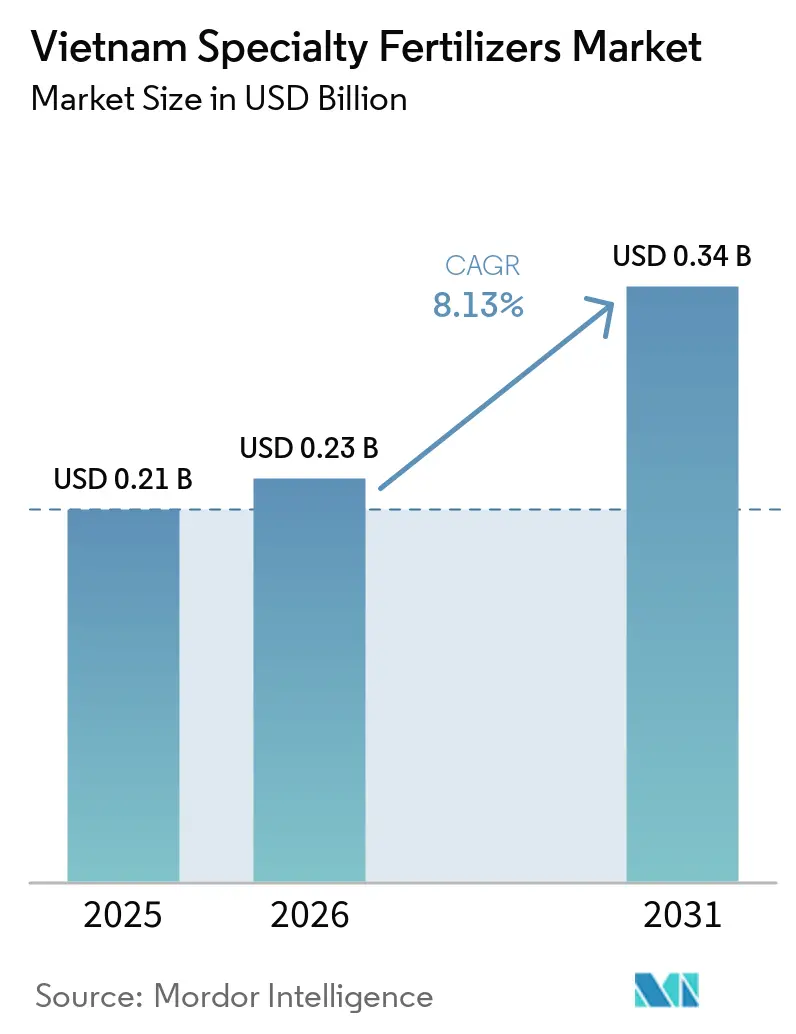

| Base Year Market Size (2025) | USD 0.21 Billion |

| Market Size (2026) | USD 0.23 Billion |

| Market Size (2031) | USD 0.34 Billion |

| Growth Rate (2026 - 2031) | 8.13% CAGR |

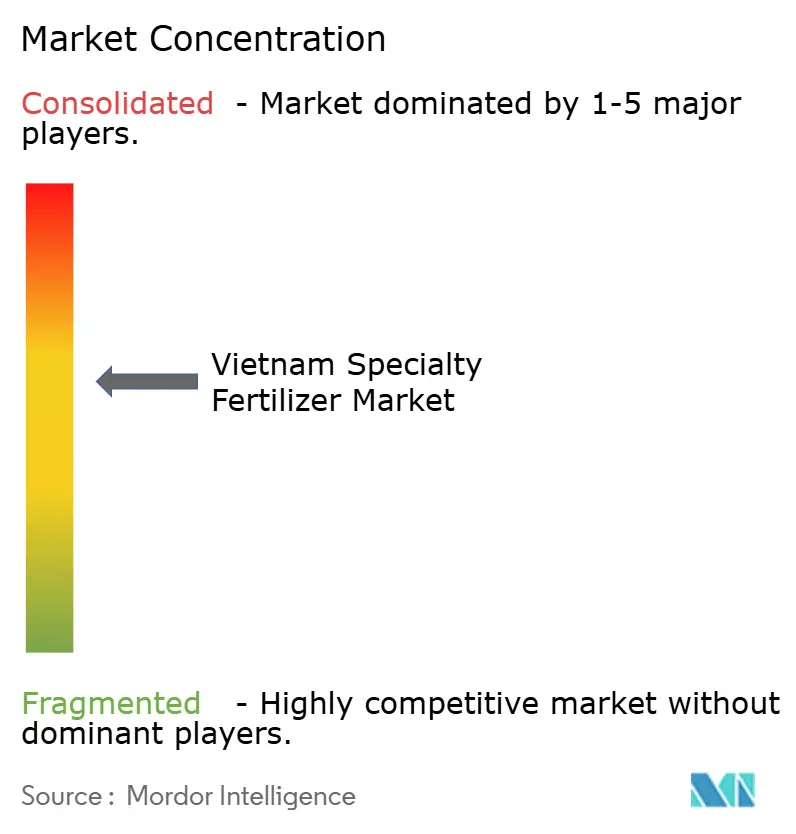

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Specialty Fertilizers Market Analysis by Mordor Intelligence

The Vietnam specialty fertilizers market size was valued at USD 0.21 billion in 2025 and estimated to grow from USD 0.23 billion in 2026 to reach USD 0.34 billion by 2031, at a CAGR of 8.13% during the forecast period (2026-2031). The measured pace reflects a broader shift from commodity inputs to precision nutrient management, driven by Vietnam’s status as the world’s second-largest coffee producer and the largest pepper exporter.[1]Source: Vietnam Ministry of Agriculture and Rural Development, “Agricultural Statistics 2025,” mard.gov.vn Liquid products dominate today’s volumes, but controlled-release lines are gaining traction as domestic urea makers add polymer-coating equipment. A July 2025 cut in the value-added tax on fertilizers from 10% to 5% has already narrowed the cost gap between imports and local brands, raising margins for companies that invest in water-soluble and coated offerings. Farmers are also under mounting pressure to curb nutrient losses, meet export quality rules, and adapt to labor shortages, all of which steer spending toward high-efficiency products that can be applied through fertigation, drones, or a single pass of coated granules.

Key Report Takeaways

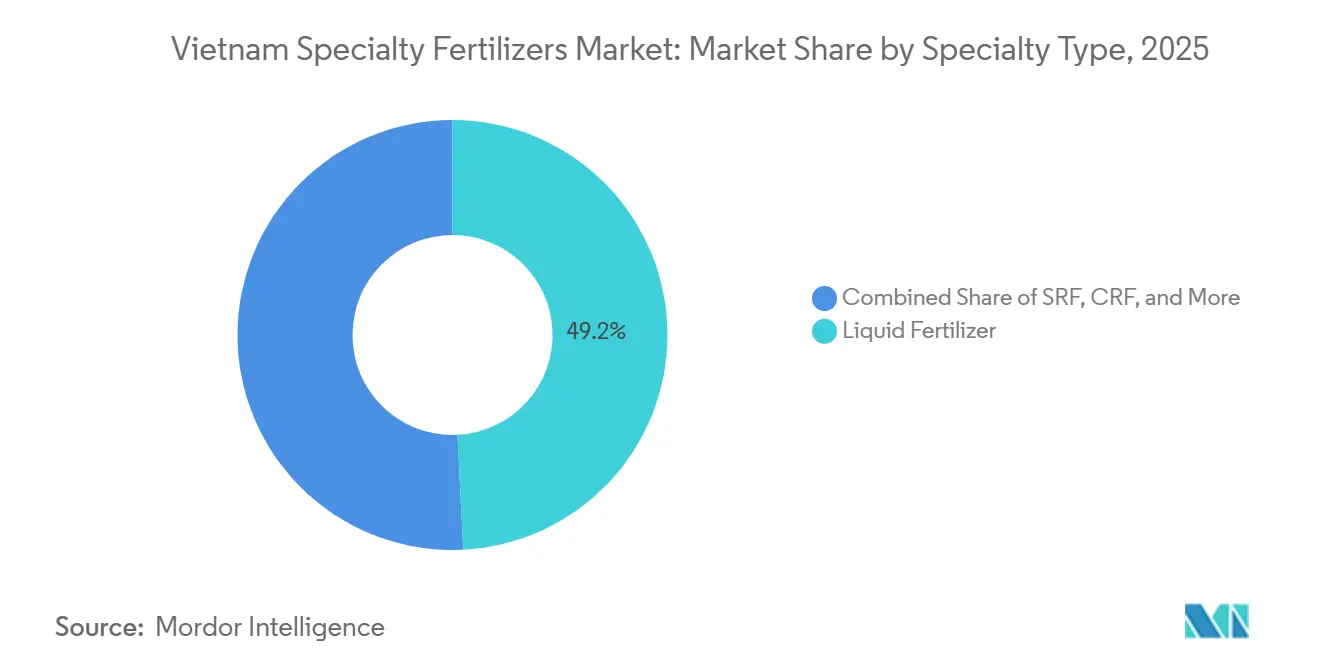

- By specialty type, liquid fertilizers held 49.2% of the Vietnam specialty fertilizers market share in 2025, while controlled-release fertilizers are projected to expand at a 4.3% CAGR through 2026 to 2031.

- By application mode, fertigation accounted for 47.3% of the Vietnam specialty fertilizers market size in 2025, and soil application is the fastest-growing mode at 4.0% CAGR from 2026 to 2031.

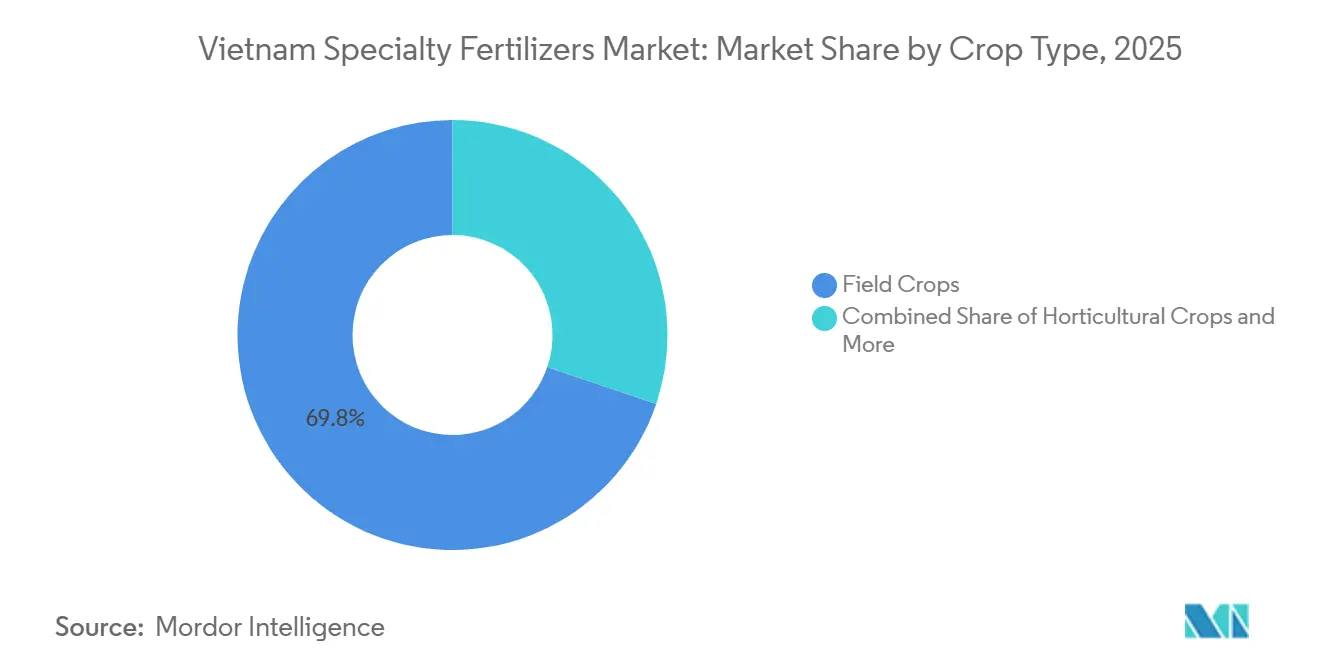

- By crop type, field crops dominated the Vietnam specialty fertilizers market with a 69.8% share in 2025, whereas turf and ornamental applications will post the highest 5.3% CAGR through 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Specialty Fertilizers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision-farming adoption boosts demand for efficient inputs | +0.8% | National, with early gains in Mekong Delta, Central Highlands, Red River Delta | Medium term (2-4 years) |

| Government VAT change (5%) improves domestic producer margins | +0.6% | National | Short term (≤ 2 years) |

| High-value crop export expansion (fruit, coffee, pepper) | +0.7% | Central Highlands, Southeast, Mekong Delta | Long term (≥ 4 years) |

| Rapid growth of greenhouse vegetable acreage | +0.5% | National, concentrated in Lam Dong, Da Lat, peri-urban zones | Medium term (2-4 years) |

| Surplus urea capacity enables coated-urea value-added lines | +0.3% | National, production hubs in Ca Mau, Ninh Binh | Medium term (2-4 years) |

| Dutch manure-granulate imports accelerate organic blends | +0.2% | National, strongest in organic-certified zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Precision-Farming Adoption Boosts Demand for Efficient Inputs

Drone application covered 50,000 hectares of rice in 2024, reducing nutrient costs by up to 25% through variable-rate dosing that relies on digital soil maps. Specialty liquids dissolve evenly and avoid the hopper clogging that restricts drones to low-dust materials. Yara International partnered with PepsiCo on 1,200 hectares of contract potato farms, raising yields 15% and cutting nitrogen runoff 30% in 2024. The government plans to shift 1 million hectares of rice to alternate wetting and drying irrigation by 2030, a system that requires slow-release nitrogen to match water schedules.[2]Source: Vietnam National University of Agriculture, “Drone Fertilizer Application Trials,” vnua.edu.vn Soil-mapping programs already cover 2.5 million hectares, equipping agribusinesses with deficiency data that validate premium blends. Adoption will scale in phases because most farms remain below one hectare and depend on cooperative models for capital-intensive technology.

Government VAT Cut Improves Domestic Producer Margins

From July 2025, a 5% VAT replaced the prior 10% rate, shrinking the landed-cost advantage of imports by roughly five percentage points and freeing up local firms to pursue specialty investments. National fertilizer capacity stands near 8 million metric tons compared with demand above 11 million metric tons, so imports will still flow, yet domestic manufacturers now enjoy higher pricing headroom. PetroVietnam Ca Mau earmarked 15% of 2025 capital expenditure for polymer-coated NPK, leveraging its 800,000 metric tons urea base to climb the value chain. Management expects specialty output to rise 10-15% by 2027. The near-term timeline reflects immediate tax savings, while engineering and commissioning of new lines require up to two years.

High-Value Crop Export Expansion in Coffee and Pepper

Coffee exports reached USD 5.4 billion in 2024 as robusta prices crossed USD 4,000 per metric ton, prompting farmers to chase quality premiums with smarter nutrient regimes. Pepper and cashew combined added another USD 5.7 billion, so even small yield gains unlock sizable revenue bumps. Lam Dong secured geographical-indication status for coffee in 2024, obliging growers to adopt fertigation and organic inputs to keep certification. ICL Group introduced Polysulphate through Duc Giang Chemicals, giving farmers a slow-release potassium and sulfur option that trims leaching by up to 40%. Because coffee trees produce over many seasons, adoption proceeds over multi-year replacement cycles, hence the long-term outlook.

Rapid Growth of Greenhouse Vegetable Acreage

Protected cultivation expanded at a 13% CAGR from 2024 into early 2025, with Lam Dong alone hosting more than 3,500 hectares of high-tech greenhouses. Operators double or triple open-field yields by pairing climate control with fertigation that delivers water-soluble NPK at 150–200 parts per million. Hydroponic systems now supply 60% of premium salad greens to urban supermarkets, using 40% less water and sidestepping soil disease. Rising organic mandates intersect with greenhouse growth because closed environments simplify compliance. The medium-term horizon stems from the capital intensity of greenhouse construction and the payback period growers require before expanding plots.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile natural-gas feedstock costs | -0.5% | National, concentrated in ammonia-dependent producers | Short term (≤ 2 years) |

| Farmer price-sensitivity toward premium inputs | -0.4% | National, most acute in smallholder rice zones | Medium term (2-4 years) |

| Proliferation of counterfeit and sub-standard products | -0.3% | National, concentrated in rural distribution channels | Short term (≤ 2 years) |

| Limited cold-chain for microbial and liquid specialties | -0.2% | National, gaps in rural and upland areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Natural-Gas Feedstock Costs

Ammonia prices fell from over USD 700 per metric ton in 2022 to USD 300–400 per metric ton in 2024, underscoring the sensitivity of urea margins to global gas swings. PetroVietnam Ca Mau relies on offshore gas fields whose output has slipped 3–5% each year since 2020, forcing supplemental imports. When feedstock costs spike, producers hesitate to fund specialty upgrades that could turn uneconomic if pricing cannot be passed along to cost-conscious farmers. Imports priced near USD 314 per metric ton from China set a ceiling that domestic suppliers must watch. The short-term timeline highlights immediate pressure during price shocks, although hedging and product-mix shifts can soften the blow.

Farmer Price Sensitivity Toward Premium Inputs

Authorities recorded more than 450 counterfeit-fertilizer cases in May 2025 alone, with nutrient content falling below 70% of label claims.[3]Source: Vietnam Chamber of Commerce and Industry, “Draft Decree on Counterfeit Goods,” vcci.com.vnSub-standard water-soluble products clog fertigation systems and erode trust in legitimate brands. A draft decree now proposes penalties up to VND 400 million (USD 15,750) for offenders, yet enforcement gaps persist in remote districts. Yara and ICL add holographic labels and QR codes, but these raise costs by 2–3%. The restraint acts quickly because counterfeit volumes surge during planting seasons, though stronger policing could dilute the effect over time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Specialty Type: Liquid Fertilizer Dominance Masks Controlled-Release Momentum

Liquid fertilizers accounted for 49.2% of the Vietnam specialty fertilizers market share in 2025, anchored by greenhouse vegetables, where fertigation delivers nutrients at 150–200 parts per million. Hydroponic growers in Da Lat supply a large share of premium salad greens and report considerable water savings, cementing liquids as the default feed. Limited cold chain infrastructure narrows distribution outside urban zones. Binh Dien’s upcoming launch of water-soluble granules offers an alternative that can be stored at ambient temperatures and targets coffee and pepper farms.

Controlled-release fertilizers are anticipated to grow at a CAGR of 4.3% from 2026 to 2031. PetroVietnam Ca Mau’s surplus urea enables polymer-coated lines that extend nitrogen release, aligning with coffee and dragon-fruit cycles. Biochar-polyurethane coatings reduce leaching and meet rising organic content rules. Water-soluble products trail liquids in market share but are gaining traction across coffee and pepper farms, where drip systems significantly cut labor. Slow-release sulfur-coated granules grow more slowly because heavy rainfall can trigger uneven nutrient pulses.

By Application Mode: Fertigation Leads, Soil Application Accelerates

Fertigation accounted for 47.3% of the Vietnam specialty fertilizers market size in 2025, with high-tech greenhouses in Lam Dong achieving yield increases of up to 3 times compared with open fields. Yara–PepsiCo potato cultivation pilots demonstrated significant yield improvements and reduced runoff, adding momentum. Drone spraying of dissolved nutrients was implemented across a large area of rice fields, appealing to cooperatives aiming to reduce labor requirements.

Soil application is projected to be the fastest-growing mode, with a CAGR of 4.0% during 2026 to 2031, as coated granules fit mechanized rice seeding, reducing field visits from three to one per season. Alternate wetting and drying irrigation on 1 million hectares of rice will further favor the use of slow-release nitrogen. Foliar feeding remains niche, used on pepper and dragon fruit during flowering stages. Haifa trials showed sugarcane yields jumping by 16 tonnes per hectare, but uptake is confined to plantations able to justify the extra labor.

By Crop Type: Field Crops Anchor Demand, Turf and Ornamental Surge

Field crops led the Vietnam specialty fertilizers market with a 69.8% share in 2025, accounting for 4 million hectares of Mekong rice and 2.5 million metric tons of fertilizer annually. Specialty penetration is low, yet absolute tonnage potential is sizable as precision pilots scale. Coffee contributes USD 5.4 billion in export earnings and drives steady uptake of potassium-sulfur blends that lift bean size and moisture consistency.

Turf and ornamental applications are anticipated to achieve the highest CAGR of 5.3% from 2026 to 2031. Vietnam’s numerous golf courses and a wave of urban landscaping in Hanoi and Ho Chi Minh City allocate a significant portion of project budgets to grass maintenance. Developers prefer controlled-release formulations that minimize burns and reduce mowing frequency. Horticultural crops, including vegetables, fruits, and spices, represent a substantial segment, driven by growth in protected cultivation and export contracts to markets such as Singapore and Japan.

Geography Analysis

The Central Highlands dominate high-value specialty use, hosting extensive areas of coffee and pepper cultivation that justify premium nutrients. Lam Dong’s network of greenhouses achieves significantly higher yields compared to open plots, lifting regional demand for liquids and water-solubles. Soil acidity in this zone also favors slow-release potassium-sulfur products.

The Mekong Delta accounts for the largest fertilizer tonnage due to its vast rice cultivation, yet specialty usage lags because smallholders focus on upfront cost. Precision pilots using drones and alternate irrigation on select areas hint at future uptake. Government programs plan to convert a significant portion of land to water-saving methods by 2030, which will require coated nitrogen to match intermittent flooding cycles.

The Red River Delta records the fastest turf and ornamental growth as golf and real-estate projects add green areas around Hanoi. Developers rely on granular slow-release products to ease maintenance workloads. Southeast Vietnam, close to Cat Lai port, acts as the main gateway for imported liquids and microbial products. Northern uplands remain underserved due to cold-chain gaps and fragmented plots, though coffee planting is slowly expanding into higher elevations for climate resilience.

Competitive Landscape

Market concentration is moderate, with the top five suppliers holding a 67% share of the Vietnam specialty fertilizers market in 2024. Yara International and ICL Group leverage global research pipelines to introduce proprietary formulas, such as ICL’s 2024 purchase of Compass Minerals’ plant-nutrition assets, which widened its micronutrient range. Domestic players PetroVietnam Ca Mau and Binh Dien invest in polymer-coating and water-soluble lines that repurpose existing urea and NPK capacity, sidestepping greenfield ammonia spends.

Technology-bundled services differentiate leaders. Yara’s digital agronomy platform underpins potato contracts with PepsiCo, ensuring traceable low-carbon supply while securing input loyalty. Chinese entrants such as Kingenta Ecological Engineering compete on price, undercutting European labels by up to 20% yet offering acceptable quality, forcing incumbents to stress brand assurance.

Regulatory tightening on counterfeit goods will likely reinforce branded share as penalties climb to VND 400 million (USD 15,750) for offenders. Firms with holographic and QR traceability gain an edge in rural channels. Capacity additions center on coated urea and liquid NPK, aided by surplus domestic urea and the VAT reduction that improves margins for local upgrades.

Vietnam Specialty Fertilizers Industry Leaders

Grupa Azoty S.A. (Compo Expert)

ICL Group Ltd

Yara International ASA

Baconco (Hebang Biotechnology Co. Ltd.)

Duc Giang Chemicals Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Newsun Crop Science and Minh Long Agro have introduced CropBoost-AP in Vietnam, a biostimulant aimed at improving crop productivity and resilience. The product promotes sustainable agriculture by enhancing plant growth, stress tolerance, and yield efficiency. This launch bolsters Vietnam's specialty fertilizers market, with a specific focus on the biostimulant segment.

- September 2025: The IRRI–Vietnam–USDA project introduced fertilizers designed to improve rice productivity and promote sustainability in Vietnam. These formulations increase nutrient efficiency and minimize environmental impact, supporting contemporary farming practices. The initiative contributes to the growth of Vietnam’s specialty fertilizers market, aligning with the country's sustainable agriculture objectives.

- July 2025: PVFCCo has introduced a new fertilizer in Vietnam composed entirely of potassium sulphate, aimed at high-value crops. This specialty fertilizer enhances crop quality by providing potassium without chloride, improving stress tolerance and increasing yields. This development bolsters Vietnam's specialty fertilizers market, particularly in the water-soluble and soil-applied categories.

Vietnam Specialty Fertilizers Market Report Scope

CRF, Liquid Fertilizer, SRF, Water Soluble are covered as segments by Speciality Type. Fertigation, Foliar, Soil are covered as segments by Application Mode. Field Crops, Horticultural Crops, Turf & Ornamental are covered as segments by Crop Type.Speciality Type

| CRF | Polymer Coated |

| Polymer-Sulfur Coated | |

| Others | |

| Liquid Fertilizer | |

| SRF | |

| Water Soluble |

Application Mode

| Fertigation |

| Foliar |

| Soil |

Crop Type

| Field Crops |

| Horticultural Crops |

| Turf and Ornamental |

| Speciality Type | CRF | Polymer Coated |

| Polymer-Sulfur Coated | ||

| Others | ||

| Liquid Fertilizer | ||

| SRF | ||

| Water Soluble | ||

| Application Mode | Fertigation | |

| Foliar | ||

| Soil | ||

| Crop Type | Field Crops | |

| Horticultural Crops | ||

| Turf and Ornamental |

Market Definition

- MARKET ESTIMATION LEVEL - Market Estimations for various types of fertilizers has been done at the product-level and not at the nutrient-level.

- NUTRIENT TYPES COVERED - Primary Nutrients: N, P and K, Secondary Macronutrients: Ca, Mg and S, Micronutients: Zn, Mn, Cu, Fe, Mo, B, and Others

- AVERAGE NUTRIENT APPLICATION RATE - This refers to the average volume of nutrient consumed per hectare of farmland in each country.

- CROP TYPES COVERED - Field Crops: Cereals, Pulses, Oilseeds, and Fiber Crops Horticulture: Fruits, Vegetables, Plantation Crops and Spices, Turf Grass and Ornamentals

| Keyword | Definition |

|---|---|

| Fertilizer | Chemical substance applied to crops to ensure nutritional requirements, available in various forms such as granules, powders, liquid, water soluble, etc. |

| Specialty Fertilizer | Used for enhanced efficiency and nutrient availability applied through soil, foliar, and fertigation. Includes CRF, SRF, liquid fertilizer, and water soluble fertilizers. |

| Controlled-Release Fertilizers (CRF) | Coated with materials such as polymer, polymer-sulfur, and other materials such as resins to ensure nutrient availability to the crop for its entire life cycle. |

| Slow-Release Fertilizers (SRF) | Coated with materials such as sulfur, neem, etc., to ensure nutrient availability to the crop for a longer period. |

| Foliar Fertilizers | Consist of both liquid and water soluble fertilizers applied through foliar application. |

| Water-Soluble Fertilizers | Available in various forms including liquid, powder, etc., used in foliar and fertigation mode of fertilizer application. |

| Fertigation | Fertilizers applied through different irrigation systems such as drip irrigation, micro irrigation, sprinkler irrigation, etc. |

| Anhydrous Ammonia | Used as fertilizer, directly injected into the soil, available in gaseous liquid form. |

| Single Super Phosphate (SSP) | Phosphorus fertilizer containing only phosphorus which has lesser than or equal to 35%. |

| Triple Super Phosphate (TSP) | Phosphorus fertilizer containing only phosphorus greater than 35%. |

| Enhanced Efficiency Fertilizers | Fertilizers coated or treated with additional layers of various ingredients to make it more efficient compared to other fertilizers. |

| Conventional Fertilizer | Fertilizers applied to crops through traditional methods including broadcasting, row placement, ploughing soil placement, etc. |

| Chelated Micronutrients | Micronutrient fertilizers coated with chelating agents such as EDTA, EDDHA, DTPA, HEDTA, etc. |

| Liquid Fertilizers | Available in liquid form, majorly used for application of fertilizers to crops through foliar and fertigation. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms