Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year Market Size (2025) | USD 0.11 Billion |

| Market Size (2026) | USD 0.13 Billion |

| Market Size (2031) | USD 0.21 Billion |

| Growth Rate (2026 - 2031) | 10.07% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Digital Signage Market Analysis by Mordor Intelligence

The Vietnam digital signage market was valued at USD 0.13 billion in 2026 and is projected to reach USD 0.21 billion by 2031, representing a 10.07% CAGR during the forecast period. The current Vietnam digital signage market size benefits from plummeting panel costs, a widening 5G footprint, and retail chains that are replacing static posters with networked screens more quickly than their regional peers. Samsung Display’s USD 1.8 billion OLED plant in Bac Ninh, LG Display’s additional USD 1 billion outlay for Haiphong, and BOE Technology’s CNY 2.02 billion Phase 2 complex in Ba Ria-Vung Tau are compressing logistics chains and eroding import premiums, thereby lowering the total cost of ownership for the Vietname digital signage market. Accelerated airport and stadium construction is driving demand for ultra-large LED walls, while cloud-based content-management platforms are nudging operators toward subscription models that favor service revenue. Regulatory tailwinds, such as government smart-city blueprints and the rising adoption of contactless solutions in healthcare, quick-service restaurants, and transit hubs, further strengthen the growth outlook for the Vietnam digital signage market.

Key Report Takeaways

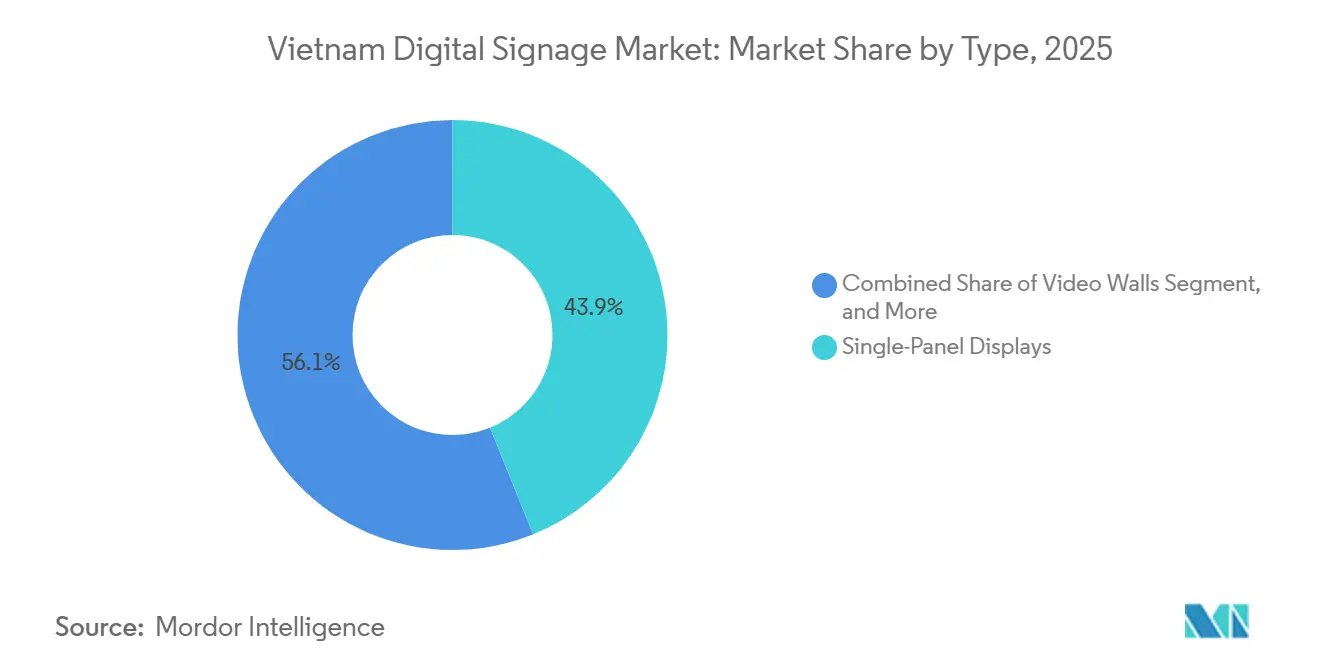

- By type, single-panel displays held 43.88% of the Vietnam digital signage market share in 2025, whereas projection and other alternative formats are forecast to grow at an 11.34% CAGR through 2031.

- By component, hardware led with 55.83% of the Vietnam digital signage market size in 2025, while services are advancing at 11.43% CAGR to 2031.

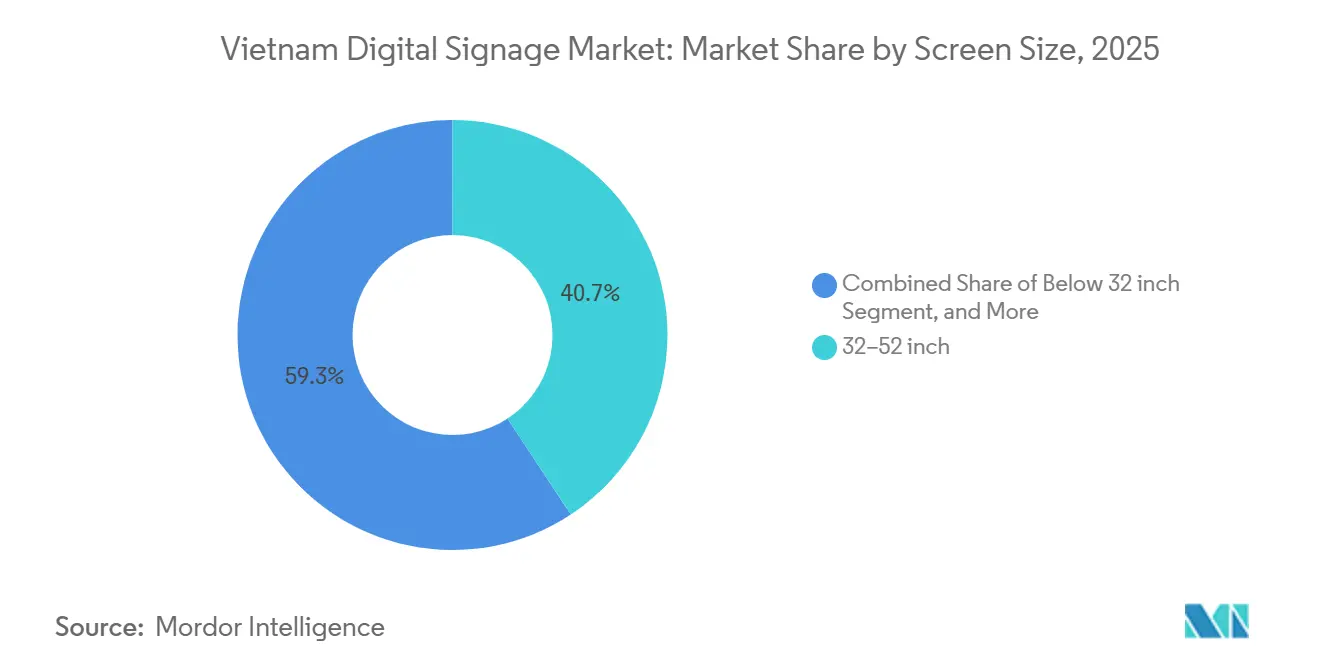

- By screen size, the 32-52 inch bracket captured 40.73% of the Vietnam digital signage market size in 2025; screens above 100 inches will post a 10.89% CAGR through 2031.

- By location, in-store and indoor deployments commanded 68.62% of the Vietnam digital signage market share in 2025 and are expanding at an 11.56% CAGR through 2031.

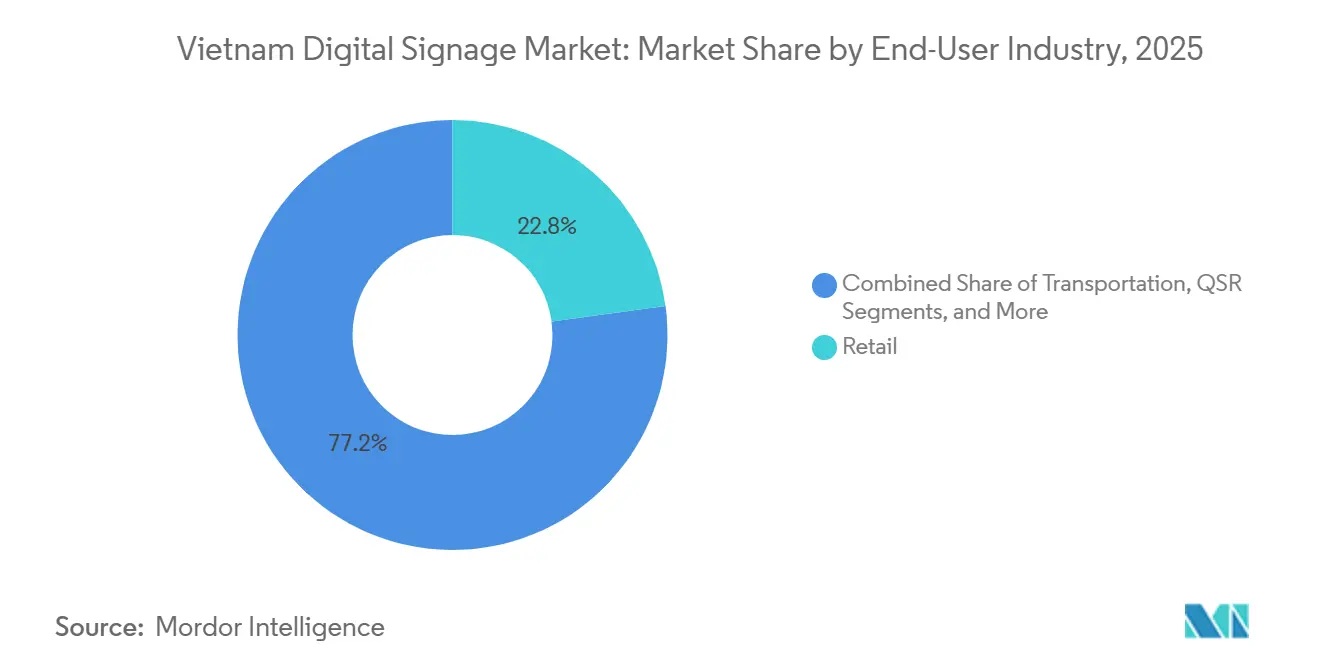

- By end-user industry, retail accounted for 22.84% of demand in 2025 of the Vietnam digital signage market, yet sports and entertainment is projected to register a 10.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Digital Signage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid decline in LED display costs | +2.1% | National, concentrated in Hanoi, Ho Chi Minh City, Da Nang industrial clusters | Short term (≤ 2 years) |

| Retail chain expansion and demand for dynamic advertising | +1.8% | National, with early gains in Hanoi, Ho Chi Minh City, Can Tho, Hai Phong | Medium term (2-4 years) |

| Government smart-city and smart-transport initiatives | +1.6% | National, pilot projects in Hanoi, Ho Chi Minh City, Da Nang | Medium term (2-4 years) |

| Adoption of contactless interactive signage post-COVID | +1.3% | National, accelerated in healthcare, retail, transportation hubs | Short term (≤ 2 years) |

| Roll-out of 5G and cloud CMS enabling real-time content updates | +1.5% | National, urban centers achieving 90% coverage by end-2025 | Medium term (2-4 years) |

| Localization of energy-efficient micro-LED production in Vietnam's industrial parks | +1.2% | National, Ba Ria-Vung Tau, Bac Ninh, Haiphong industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Decline in LED Display Costs

Samsung Display’s Bac Ninh OLED expansion and LG Display’s Haiphong investment have transformed Vietnam into a panel-manufacturing hub, reducing delivery lead times from eight weeks to less than four. BOE Technology’s Ba Ria-Vung Tau factory will produce 7 million displays and 40 million ePaper units annually from 2025, reducing landed costs by an estimated 20-25% for integrators serving the Vietnam digital signage market.[1]BOE Technology, “BOE Technology Breaks Ground on Phase 2 Vietnam Facility,” boe.com Local retailers can now acquire 55-inch commercial-grade screens at prices that were previously reserved for bulk imports, accelerating replacement cycles from 36-48 months to 18-24 months. Cost deflation is most pronounced in the 32-52 inch bracket that dominates quick-service restaurants and pharmacies. Pilot lines for micro-LEDs promise a 40% lower power draw and lifespans exceeding 100,000 hours, attributes that outdoor operators value in Vietnam’s humid climate.

Retail Chain Expansion and Demand for Dynamic Advertising

WinCommerce plans to grow from 4,300 stores in 2025 to 10,000 by 2030, cementing standardized digital signage at checkout queues and end-caps. The modern trade share of Vietnam’s USD 350 billion retail sector is expected to reach approximately 30% by 2030, leading to a steady shift from printed media to connected screens.[2]General Statistics Office of Vietnam, “Vietnam Retail Market Statistics 2025,” gso.gov.vn AEON Entertainment’s partnership with Beta Media to open cinemas nationwide will feature video walls, digital posters, and concession-area kiosks that monetize foot traffic. CGV Vietnam’s 2024 revenue surge, driven partly by on-screen advertising, underscores the incremental margin that networked displays deliver. The driver therefore amplifies content-refresh frequencies and elevates the Vietnam digital signage market as a tactical tool for brand consistency.

Government Smart-City and Smart-Transport Initiatives

Project 06 aims for 80% of public-service applications to shift online, spurring agencies to deploy AI kiosks across commune offices and police stations. Airports Corporation of Vietnam invested USD 430 million in Tan Son Nhat Terminal 3 and USD 200 million in Noi Bai Terminal 2 upgrades, each loaded with self-service kiosks and large-format LED boards. Real-time passenger information, biometric check-ins, and automated bag drops together demand durable, high-brightness screens that boost the Vietnam digital signage market. Chicilon Media’s network in 11 airports delivers 240 ten-second plays daily per layout, generating premium inventory for automotive and electronics advertisers. Smart-transport blueprints therefore translate infrastructure outlays into sustained display demand.

Adoption of Contactless Interactive Signage Post-COVID

Da Nang Hospital’s smart kiosks slash check-in time by two-thirds and reduce front-desk staffing by roughly 30%. A nationwide directive requires at least 1,001 similar units across medical facilities by end-2025, catalyzing orders for tamper-proof touchscreens and integrated payment terminals. Visa reported that contactless accounted for 75% of its Vietnam transactions in 2024, while QR-code volumes rose 159.6% in the first seven months of 2025, signaling consumer comfort with touch-free interfaces. LG Electronics supplies ISO 20022-compliant kiosks that lift average ticket sizes 10-15% through automated upsell prompts.[3]LG Display, “LG Display Invests Additional USD 1 Billion in Haiphong OLED Facility,” lgdisplay.com Behavioral shifts toward speed and hygiene propel interactive formats within the Vietnam digital signage market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital expenditure for large-format LED walls | -1.4% | National, acute in tier-2 and tier-3 cities | Medium term (2-4 years) |

| Cyber-security and data-privacy concerns in networked signage | -1.1% | National, heightened in healthcare, finance, government sectors | Short term (≤ 2 years) |

| Fragmented local content-creation ecosystem limiting ROI | -0.9% | National, most pronounced in tier-2 and tier-3 cities | Medium term (2-4 years) |

| Heritage-zone regulations capping outdoor display brightness | -0.6% | Hanoi Old Quarter, Hoi An Ancient Town, Ho Chi Minh City District 1 heritage areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure for Large-Format LED Walls

Screens above 100 inches cost USD 50,000-150,000 fully installed, an outlay that smaller venues struggle to amortize. The 60,000-seat PVF Stadium and Vingroup’s 135,000-seat Olympic complex illustrate how deep-pocketed sponsors absorb these costs, yet shopping centers in Can Tho or Vinh face double-digit financing rates and 30-40% down-payment requirements. Leasing models from BrightSign and Scala, priced on a per-screen subscription, are gaining favor but still depend on advertisers’ willingness to commit to multi-year contracts. Until alternative funding structures mature, capital intensity will temper rollout velocity in secondary cities, thereby moderating the Vietnam digital signage market growth trajectory.

Cyber-Security and Data-Privacy Concerns in Networked Signage

Decree 13/2023 mandates consent and breach reporting for biometric data collection, while the Cybersecurity Law 2018 requires local data storage for critical systems. Compliance lifts hosting expenses 15-20% compared with regional cloud hubs and discourages real-time audience measurement in sectors such as healthcare and finance. Draft AI regulations, expected in 2025, may further restrict demographic inference engines that underpin programmatic advertising yield. A single breach can trigger fines up to 5% of annual revenue, prompting risk-averse institutions to favor displays without integrated cameras. Consequently, security liabilities act as a drag on the Vietnam digital signage market until encryption and anonymization protocols become ubiquitous.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Single-Panel Displays Anchor Convenience Retail

Single-panel displays held 43.88% of the Vietnam digital signage market in 2025, underscoring their plug-and-play appeal for pharmacies, convenience stores, and branch banks. Video walls, although immersive, require structural reinforcement and precision calibration, limiting adoption to flagship stores and control rooms that collectively account for roughly one-fifth of demand. Projection and other alternative formats, including transparent OLED, ePaper, and holography, are set to expand at an 11.34% CAGR through 2031, driven by luxury retail and museum pilots where novelty attracts foot traffic.

Immersive venues provide further traction. The 60,000-seat PVF Stadium features perimeter LED ribbons that generate sponsorship revenue independently of ticket sales, while Absen’s 2,000-square-meter installation for Vietnam’s 80th National Day highlights its scale readiness. Such deployments widen awareness and accelerate experimentation, thereby broadening the addressable base for the Vietnam digital signage market.

By Component: Services Gain as Cloud CMS Lowers Barriers

Hardware contributed 55.83% to the Vietnam digital signage market size in 2025, yet the services segment, including installation, maintenance, creative, and managed operations, is forecast to grow 11.43% annually through 2031. Local panel output from Samsung, LG, and BOE shortens supply chains, but value shifts toward remote orchestration and uptime guarantees. Cloud CMS platforms, priced at USD 10-15 per screen monthly, eliminate licensing CAPEX, allowing small enterprises to launch pilots with minimal risk.

Analytics layers further monetize networks. HPT’s AI-enabled signage solution boosts ad fill rates up to 20% but must encrypt demographic logs to comply with Decree 13/2023. As 5G coverage approaches 90%, real-time firmware updates reduce truck rolls by 30-40%, further amplifying service demand. The outcome tilts revenue toward recurring contracts, reinforcing the Vietnam digital signage market’s shift from hardware dependency to service-centric economics.

By Screen Size: Ultra-Large Formats Ride Stadium Boom

Screens in the 32-52 inch range dominated with 40.73% share in 2025, equipping quick-service restaurants and cash-wrap zones where sightlines are short. Displays above 100 inches, while only a niche today, will post 10.89% CAGR to 2031, fueled by stadiums, convention centers, and cinema lobbies that prioritize spectacle. Luxmage’s COB-8K, an 80-square-meter wall at Eaton Park, underscores its readiness for ultra-high-resolution viewing distances under three meters.

Stadium investments amplify demand. PVF Stadium and Vingroup’s Olympic complex both specify 4K-plus side-line boards, driving orders for pixel pitches below P2.0 and brightness above 6,000 nits. As mega-venues standardize on these specifications, supply pricing will converge downward, gradually making jumbo formats accessible to large shopping malls and transportation terminals, thereby enlarging the Vietnam digital signage market.

By Location: In-Store Deployments Dominate as Retail Modernizes

In-store and indoor installations captured 68.62% of the Vietnam digital signage market in 2025 and are expected to expand at an 11.56% CAGR. WinCommerce’s nationwide rollout and AEON Mall’s expanding footprint rely on aisle-end screens and digital directories to centralize promotions and wayfinding. Airports likewise prioritize indoor touchpoints, Tan Son Nhat Terminal 3 alone added 42 kiosks and 27 gate screens in 2025.

Outdoor uptake, constrained to 31.38% share, faces brightness caps in Hanoi’s Old Quarter and Hoi An. Nonetheless, Chicilon Media’s airport network and LG’s IP56-rated signage illustrate technical pathways to compliance. Rollout of 5G enables streamed video on roadside billboards, yet permit complexity continues to skew deployments indoors, sustaining the Vietnam digital signage market’s retail-centric bias.

By End-User Industry: Sports and Entertainment Surge Ahead

Retail accounted for 22.84% of spending in 2025, driven by growth in modern trade and centralized merchandising. Yet sports and entertainment will outpace all sectors at a 10.94% CAGR, catalyzed by the PVF Stadium, Vingroup’s Olympic complex, AEON-Beta cinemas, and CGV’s screen upgrades. Transportation ranks next, with airports integrating biometric kiosks and large-format FIDS boards.

Healthcare and banking institutions are embracing interactive kiosks to reduce queue times, but stringent data-privacy rules are tempering near-term camera adoption. Corporate offices utilize lobby walls for branding and employee messaging, while educational institutions pilot e-paper timetables to reduce printing waste. Collectively, these trends diversify vertical exposure, reducing single-sector risk for the Vietnam digital signage market.

Geography Analysis

Hanoi, Ho Chi Minh City, and Da Nang collectively hosted roughly 70% of Vietnam digital signage market installations in 2025. Hanoi’s political stature attracts high-profile projects such as PVF Stadium and Vingroup’s Olympic complex, even as Decree 33/2022 restricts billboard luminosity in the Old Quarter. Noi Bai Terminal 2’s upgrade added 24 self-service bag drops and 24 kiosks, raising passenger capacity to 15 million annually.

Ho Chi Minh City, the commercial nucleus, underpins indoor retail signage demand. Tan Son Nhat Terminal 3’s self-check-in and AI bag-drop systems rely on high-brightness displays, while Chicilon Media’s network delivers premium ad slots to consumer-electronics brands.

Da Nang’s smart-city program showcases medical kiosks that authenticate chip-embedded IDs, serving as blueprints for nationwide rollouts. Tier-2 cities, including Can Tho, Hai Phong, and Vinh, represent 20-25% of current installations. Expansion there hinges on BOE’s local panel output and more flexible financing schemes. As 5G reaches 90% population coverage, remote management and real-time bidding become viable in provincial markets, widening the Vietnam digital signage market footprint beyond core metros.

Competitive Landscape

Global panel makers such as Samsung, LG, Sony, Sharp, and Panasonic jostle with Chinese LED majors Absen, Leyard, and Unilumin while Vietnamese integrators such as VDSignage, Net & Com, and ATT Systems provide turnkey bundles. Samsung and LG leverage local fabs to slash delivery lead times by half and win high-volume orders through aggressive pricing. Absen’s 2,000 square-meter Ba Dinh Square project showcased readiness for state ceremonies, nudging brand preference toward Chinese suppliers for large-format jobs.

System integrators compete on service-level agreements. NEC Vietnam guarantees 99.5% uptime, appealing to retail chains expanding beyond top-tier cities. VDSignage’s cloud CMS plus field-service model targets SMEs needing one-stop providers.

White-space persists in tier-2 locations where digital signage penetration trails national averages. Cloud CMS subscriptions allow operators to match fees with advertising cash flow, easing capex barriers. Emerging disruptors include transparent OLED vendors and ePaper specialists enabled by BOE’s 40 million-unit capacity ramp, which will broaden use cases in heritage zones with tight brightness caps. Overall, rivalry is intensifying, yet ample runway remains for differentiation via content-as-a-service models, micro-LED energy savings, and AI-driven analytics, supporting healthy margins within the Vietnam digital signage market.

Vietnam Digital Signage Industry Leaders

NEC Corporation

Intel Corporation

LG Electronics Inc.

ATT Systems (Vietnam) Pte. Ltd.

Samsung Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Sharp began shipping fully branded MultiSync ME Series large-format displays for corporate, retail, and transportation applications.

- December 2025: Hanoi approved Vingroup’s USD 38 billion Olympic Sports Complex featuring a 135,000-seat stadium equipped with ultra-large LED screens.

- December 2025: Airports Corporation of Vietnam opened Noi Bai Terminal 2 expansion, adding 24 bag-drop counters, 24 kiosks, and 30 gate displays.

- October 2025: Ministry of Public Security broke ground on the 60,000-seat PVF Stadium with FIFA-standard LED systems.

Vietnam Digital Signage Market Report Scope

The Vietnam Digital Signage Market Report is Segmented by Type (Single-Panel Displays, Video Walls, Totems/Digital Posters, Kiosks/Interactive Terminals, Outdoor LED/Billboard/Street Furniture, Projection/Others), Component (Hardware, Software, Services), Screen Size (Below 32 inch, 32-52 inch, 52-75 inch, Above 75 inch, Ultra-large Above 100 inch), Location (In-store/Indoor, Outdoor), and End-user Industry (Retail, Transportation, Hospitality, QSR, Corporate, Sports and Entertainment, Healthcare, Other End-user Industries). The Market Forecasts are Provided in Terms of Value (USD).

By Signage Type

| Single-Panel Displays |

| Video Walls |

| Totems / Digital Posters |

| Kiosks / Interactive Terminals |

| Outdoor LED / Billboard / Street Furniture (DOOH) |

| Other Signage Types (Projection, Etc.) |

By Component

| Hardware | Display Panels |

| Media Players and Controllers | |

| Mounts and Stands | |

| Other Hardwares | |

| Software | |

| Services |

By Screen Size

| Below 32 inch |

| 32–52 inch |

| 52–75 inch |

| Above 75 inch |

| Ultra-large Above 100" |

By Location

| In-store/Indoor |

| Outdoor |

By End-user Industry

| Retail |

| Transportation |

| Hospitalitiy |

| QSR |

| Corporate |

| Sports and Entertainment |

| Healthcare |

| Other End-user Industries |

| By Signage Type | Single-Panel Displays | |

| Video Walls | ||

| Totems / Digital Posters | ||

| Kiosks / Interactive Terminals | ||

| Outdoor LED / Billboard / Street Furniture (DOOH) | ||

| Other Signage Types (Projection, Etc.) | ||

| By Component | Hardware | Display Panels |

| Media Players and Controllers | ||

| Mounts and Stands | ||

| Other Hardwares | ||

| Software | ||

| Services | ||

| By Screen Size | Below 32 inch | |

| 32–52 inch | ||

| 52–75 inch | ||

| Above 75 inch | ||

| Ultra-large Above 100" | ||

| By Location | In-store/Indoor | |

| Outdoor | ||

| By End-user Industry | Retail | |

| Transportation | ||

| Hospitalitiy | ||

| QSR | ||

| Corporate | ||

| Sports and Entertainment | ||

| Healthcare | ||

| Other End-user Industries | ||

Key Questions Answered in the Report

What CAGR is projected for the Vietnam digital signage market through 2031?

The market is forecast to expand at a 10.07% CAGR, reaching USD 0.21 billion by 2031.

Which screen-size segment currently leads installations?

The 32–52 inch bracket held 40.73% share in 2025, favored by quick-service restaurants and convenience stores.

Which end-user vertical is expected to grow fastest?

Sports and entertainment applications are forecast to grow at 10.94% CAGR through 2031, driven by new stadium and cinema projects.

How will services revenue evolve relative to hardware?

Services, covering installation and cloud CMS, are projected to rise at 11.43% CAGR, outpacing hardware growth as operators prioritize uptime guarantees.

What role does 5G play in market expansion?

Nationwide 5G coverage approaching 90% by end-2025 enables real-time content updates and remote diagnostics, reducing maintenance costs and enhancing ROI.

Page last updated on: