Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

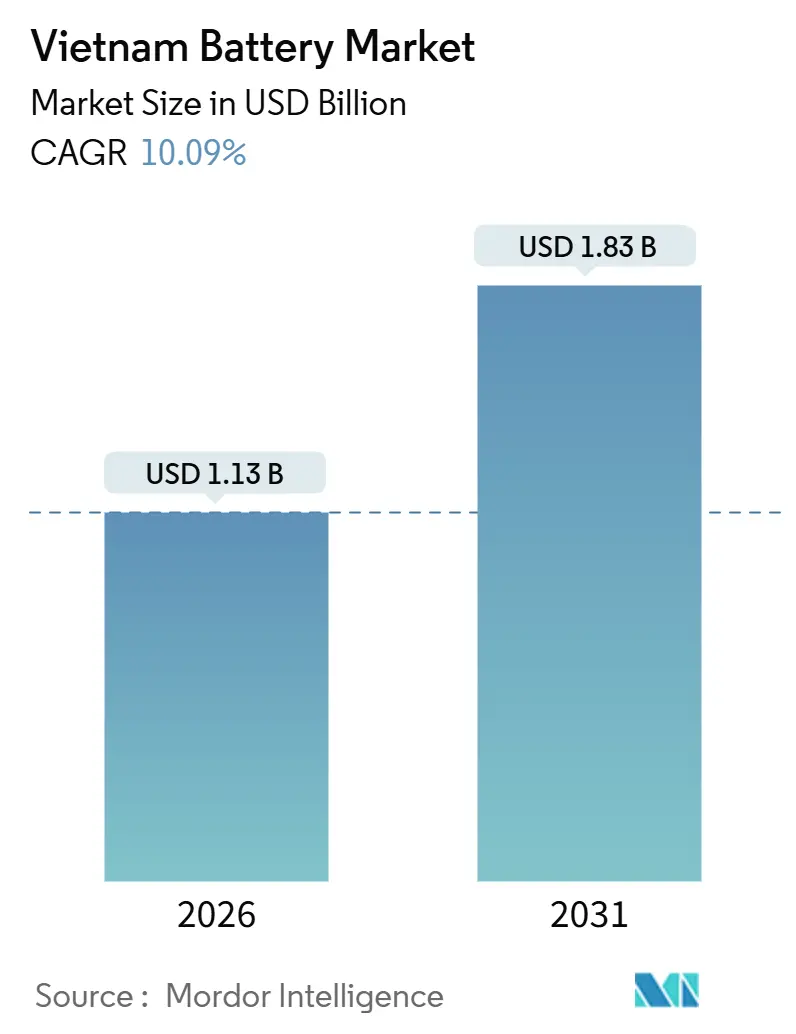

| Market Size (2026) | USD 1.13 Billion |

| Market Size (2031) | USD 1.83 Billion |

| Growth Rate (2026 - 2031) | 10.09% CAGR |

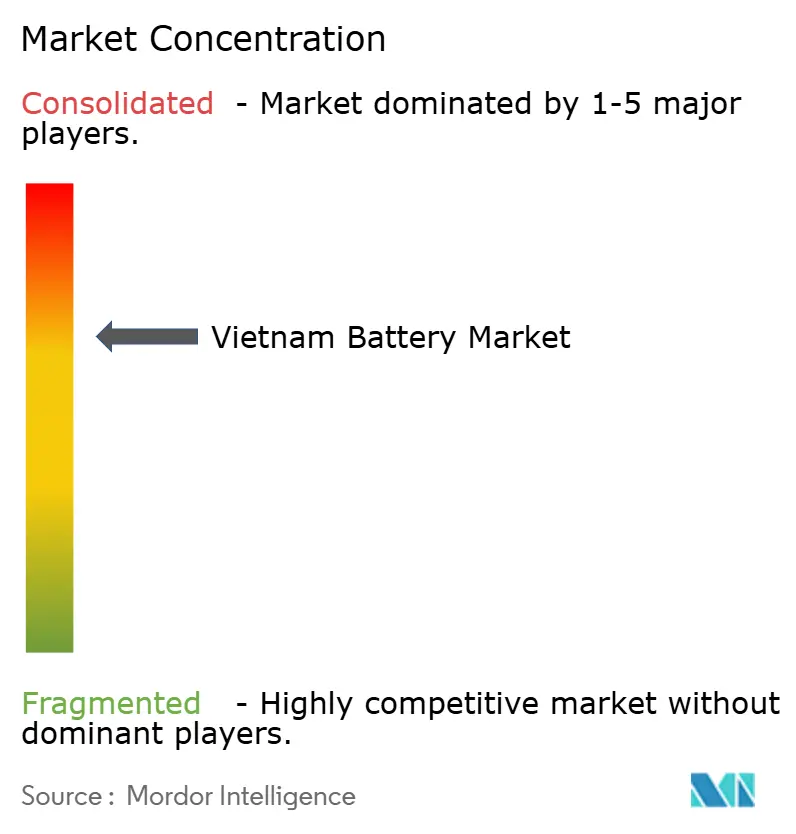

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Battery Market Analysis by Mordor Intelligence

The Vietnam Battery Market size is estimated at USD 1.13 billion in 2026, and is expected to reach USD 1.83 billion by 2031, at a CAGR of 10.09% during the forecast period (2026-2031).

Momentum stems from surging electric-vehicle (EV) adoption, domestic conglomerates’ vertical-integration playbooks, and the government’s ambition to anchor regional battery manufacturing. Automakers led by VinFast delivered nearly 97,400 EVs in 2024, more than doubling the prior year and signaling robust lithium-ion uptake.[1]Anonymous, “VinFast Delivers 97,399 EVs in 2024, Up 192% Year-on-Year,” Reuters, reuters.com Investment announcements from LG Energy Solution and Gotion High-Tech underscore rising foreign interest, while 5G network densification and data-center expansion diversify demand beyond mobility. Yet the Vietnam battery market must overcome 80-100% import dependence for key raw materials and clarify revenue models for energy-storage systems before growth can be fully unlocked.[2]Asian Development Bank, “Vietnam Lithium-Ion Battery Supply Chain Diversification,” adb.org

Key Report Takeaways

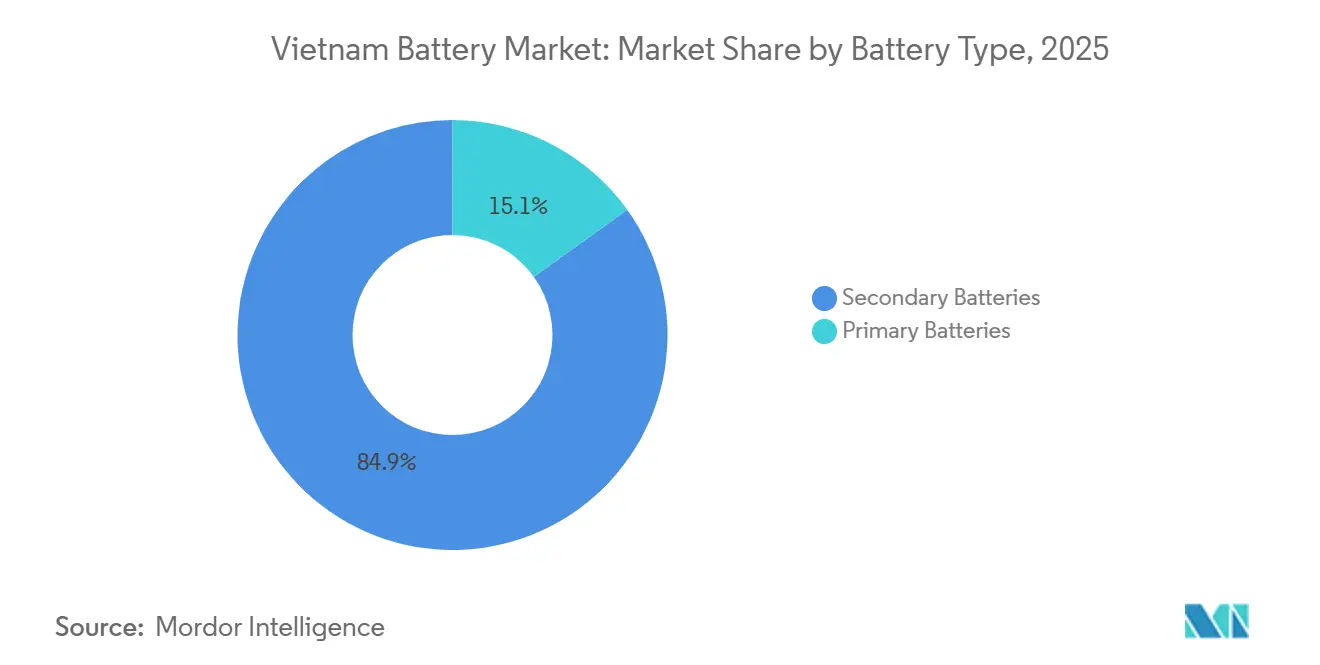

- By battery type, secondary rechargeable solutions held 84.9% of the Vietnam battery market share in 2025; primary cells trailed at 15.1% and are expanding at only 1.4% CAGR to 2031.

- By technology, solid-state platforms are forecast to post a 29.8% CAGR through 2031, while lithium-ion retained 55.2% of the Vietnam battery market share in 2025.

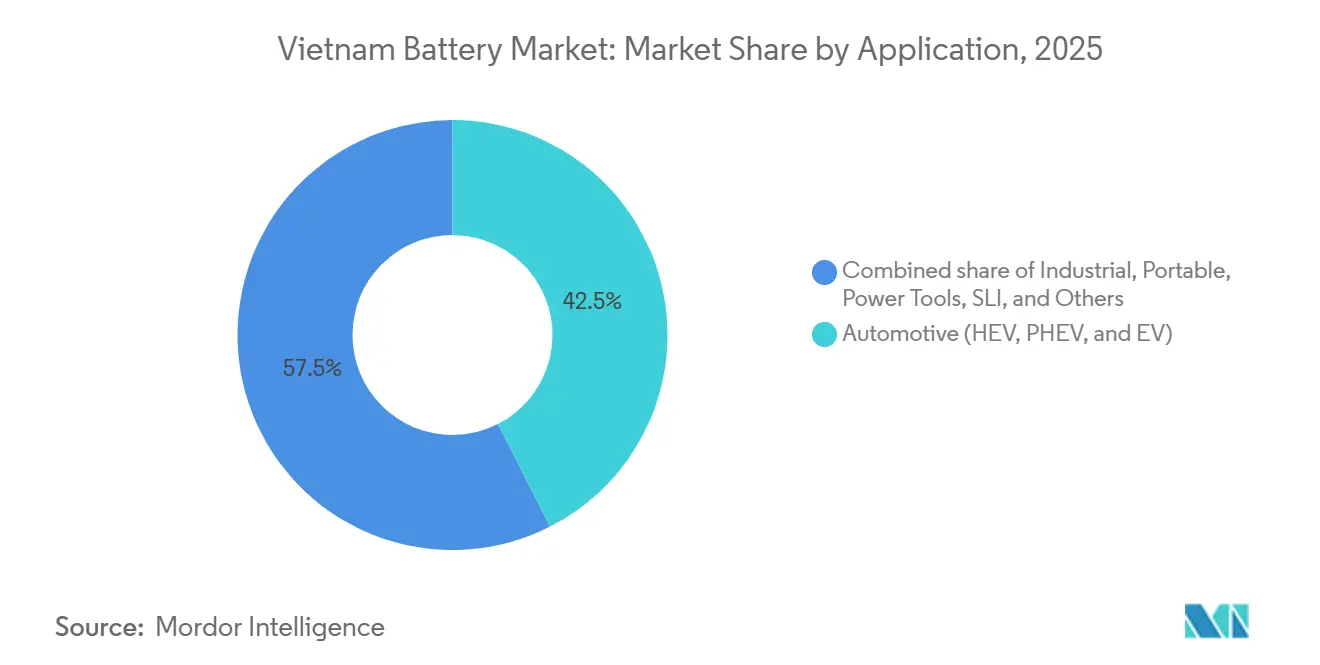

- By application, automotive captured 42.5% of the Vietnam battery market size in 2025 and is advancing at a 13.3% CAGR to 2031.

- VinES and its Gotion joint venture accounted for the single largest committed domestic EV-cell capacity at 5 GWh in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining lithium-ion cell prices | +2.1% | National, with stronger effect in price-sensitive e-motorcycle and industrial UPS segments | Medium term (2-4 years) |

| Surge in EV and e-bike adoption | +3.5% | National, concentrated in Hanoi and Ho Chi Minh City; spill-over to Da Nang and Can Tho | Short term (≤ 2 years) |

| Government incentives for local manufacturing | +1.8% | National, with priority zones in Ha Tinh, Hai Phong, and southern industrial corridors | Medium term (2-4 years) |

| Expansion of 5G and data-center back-up demand | +1.2% | Urban centers (Hanoi, Ho Chi Minh City) and coastal data-center hubs | Medium term (2-4 years) |

| VinFast/VinES vertical-integration investments | +2.3% | National, anchored by Ha Tinh cell plant and Hai Phong vehicle assembly | Short term (≤ 2 years) |

| Supply-chain diversification away from China | +1.6% | National, with cross-border logistics nodes in northern border provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Lithium-Ion Cell Prices

Pack costs for lithium-iron-phosphate systems slid under USD 100 per kWh in 2023, and global averages are poised to fall another 40% by 2030.[3]International Energy Agency, “Global EV Outlook 2024,” iea.org Material expenses dominate cell economics, so cheaper cathodes quickly translate into lower vehicle and storage prices. Vietnam’s e-motorcycle segment, already the world’s fourth largest, becomes price-competitive with 125 cc gasoline scooters once packs hit USD 80 per kWh, accelerating two-wheeler replacement. Industrial users see payback periods drop below three years when swapping valve-regulated lead-acid for lithium-ion, spurring uninterruptible-power-supply upgrades. Ho Chi Minh City’s plan to convert 400,000 motorcycles to electric propulsion starting in 2026 will test whether falling cell prices convert intent into mass adoption.

Surge in EV and E-Bike Adoption

Electric cars captured about 40% of new passenger-car sales in 2025, a level unrivaled in Southeast Asia and driven almost entirely by VinFast’s domestic ramp-up. Hanoi’s July 2026 ban on fossil-fuel motorcycles inside Ring Road 1 acts as a regulatory catalyst for two-wheeler electrification, while budget constraints postpone similar conversion in public bus fleets. Competition in e-motorcycles remains intense as Chinese brands such as Yadea battle local assemblers across battery-swap and plug-in architectures. Premium models deploy swappable lithium-ion packs, whereas ultra-low-cost options cling to lead-acid, bifurcating supply needs. Decision 876/QD-TTg further mandates 50% electrification of urban transport by 2030, solidifying long-term demand.[4]Government Office, “Decision 876/QD-TTg on Urban Transport Electrification,” chinhphu.vn

Government Incentives for Local Manufacturing

Hanoi’s battery strategy links preferential tax, land-lease, and import-duty relief to projects in selected economic zones, notably Ha Tinh and Hai Phong. These carrots helped attract the 5 GWh VinES-Gotion lithium-iron-phosphate plant and sealed LG Energy Solution’s memorandum with Kim Long Motor targeting 1 GWh in Hue by mid-2026. Manufacturing incentives also stipulate localization ratios that push suppliers to build module and pack lines inside Vietnam. Policy clarity on battery waste and recycling under Circular 02/2022/TT-BTNMT, though nascent, signals a full-life-cycle orientation that appeals to multinationals under ESG scrutiny. If fully executed, fiscal levers could shave capital costs enough to offset raw-material import premiums.

VinFast/VinES Vertical-Integration Investments

VinES’ Ha Tinh cell complex underpins VinFast’s plan to surpass 200,000 EVs annually by 2027. The USD 2 billion funding pipeline from Vingroup illustrates a high commitment but concentrates volume risk in a single automaker. Pilot battery-energy-storage deployments at the Vinpearl resort showcase ambition to diversify revenue streams, although the absence of an ancillary-services market hampers returns. VinFast’s ProLogium tie-up aims to commercialize sulfide solid-state cells with 800 Wh per liter energy density by 2029, offering a local first-mover edge if timelines hold. Successful vertical integration could carve a defensible domestic supply chain, yet export penetration in North America and Europe remains an execution overhang.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reliance on pumped-hydro over BESS | -1.4% | National, with strongest effect in northern hydropower-rich provinces | Medium term (2-4 years) |

| Limited domestic raw-material base | -1.9% | National, affecting all lithium-ion cell and cathode production | Long term (≥ 4 years) |

| Stricter hazardous-waste regulations | -0.8% | National, with heightened enforcement in urban and industrial zones | Short term (≤ 2 years) |

| Grid-connection bottlenecks for large ESS | -1.1% | National, concentrated in provinces with high renewable penetration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reliance on Pumped-Hydro Over BESS

Vietnam’s revised Power Development Plan VIII targets up to 16.3 GW of battery storage by 2030, yet historic preference for pumped-hydro keeps lithium-ion projects sidelined. Pumped-hydro’s longer discharge and multi-decade asset life appeal to planners, while lithium-ion’s sweet spot lies in short-duration frequency regulation. Electricity of Vietnam launched a 50 MW/50 MWh pilot in 2024 but has yet to publish standardized grid-connection codes for independent operators. Without a wholesale ancillary-services market, developers rely on time-of-use arbitrage alone, which seldom clears investment hurdles at USD 250–350 per kWh installed. Grid-scale deployment thus lags even as solar and wind curtailment rise in high-penetration provinces.

Limited Domestic Raw-Material Base

Vietnam boasts sizable nickel and graphite reserves yet lacks refinery throughput, resulting in near-total dependency on imported lithium compounds and cathode materials. Projected domestic demand of 46.9 GWh by 2030 will require roughly 9,400 t of lithium-carbonate equivalent and 23,500 t of cathode powders each year. Exposure to Chinese supply chains raises price and geopolitical risks. Extended producer responsibility rules under the Law on Environmental Protection 2020 and Circular 02/2022/TT-BTNMT mandate battery waste collection, yet hydrometallurgical recycling remains embryonic, limiting closed-loop material recovery. Absent upstream investments or offtake deals with Australian or Chilean miners, the Vietnam battery market stays a cell-assembly hub rather than a vertically integrated powerhouse.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Rechargeables Dominate Amid EV Surge

Secondary rechargeable batteries held 84.9% of the Vietnam battery market share in 2025 and are expanding at an 11.5% CAGR through 2031, outstripping overall growth. The surge reflects VinFast’s volume ramp, e-motorcycle proliferation, and 5G tower upgrades shifting from lead-acid to lithium-ion. Industrial power-backup buyers now value 3,000-cycle life and reduced maintenance, nudging valve-regulated lead-acid out of telecom cabinets. T&T Group’s planned 2 GWh storage-products facility, scaling to 10 GWh, illustrates rising confidence in rechargeable demand.

Primary cells maintained a 15.1% foothold in 2025, concentrated in remote sensors, medical devices, and low-drain consumer goods, where shelf life trumps cycle costs. Yet the transition to USB-C charging and energy-harvesting IoT nodes caps growth. Rechargeable momentum implies incremental demand of nearly 8 GWh by 2031, pressuring domestic producers to secure cathode supply even as automotive volumes dominate. The Vietnam battery market size for rechargeables could therefore eclipse USD 1.5 billion by 2031 if localization targets hold.

By Technology: Solid-State Disruption Looms Over Li-Ion

Lithium-ion retained 55.2% share in 2025, but solid-state chemistries are set to post a blistering 29.8% CAGR, the highest among all platforms. Lead-acid still served 28% of demand in starter-lighting-ignition and industrial motive niches due to low capex and robust recycling streams. Nickel-metal hydride, nickel-cadmium, sodium-sulfur, and flow batteries together comprised less than 7%, confined to specialized use cases.

Solid-state’s advance hinges on ProLogium’s and SK On’s pilot lines that promise 800 Wh per liter energy density by 2029. Eliminating flammable liquid electrolytes addresses thermal-runaway risk, a critical safety differentiator for buses and high-capacity storage. Vietnam’s first solid-state volumes will likely feed VinFast's premium EV models, creating an early local demand anchor. The Vietnam battery market size for solid-state could approach USD 400 million by 2031 if commercialization timelines hold.

By Application: Automotive Leads While Industrial Stabilizes

Automotive captured 42.5% of the Vietnam battery market size in 2025 and is forecast to expand at a 13.3% CAGR through 2031, adding about 5 GWh in incremental demand. Hanoi’s fossil-fuel motorcycle ban inside Ring Road 1 and Ho Chi Minh City’s 400,000-unit conversion plan intensify two-wheeler consumption, while VinFast targets export growth. Industrial stationary batteries accounted for 35% of demand but trail with an 8% CAGR because energy-storage revenues remain policy-constrained. Portable electronics held an 18% share, growing 6% annually as foldable devices and AR wearables lift per-unit capacity despite mature smartphone penetration.

Power tools and residual starter-lighting-ignition segments combine for 5%, showing minimal expansion. The Vietnam battery market share weighted to automotive exposes the ecosystem to cyclical passenger-car swings and to VinFast’s export execution risk, underscoring diversification needs into industrial and grid segments once regulatory clarity improves.

Geography Analysis

Northern provinces led by Hanoi, Hai Phong, and Ha Tinh account for nearly two-thirds of Vietnam's battery market demand, anchored by VinFast’s vehicle line and VinES’ upcoming cell complex. Proximity to China’s Guangxi border enables just-in-time cathode and BMS imports but poses geopolitical exposure. Southern zones around Ho Chi Minh City supply consumer electronics packs yet lack major EV-cell commitments, although Google Cloud’s 2024 data-center launch stimulated lithium-ion UPS upgrades.

Central Vietnam, notably Hue and Da Nang, emerges as a secondary hub following LG Energy Solution’s collaboration with Kim Long Motor. Infrastructure gaps, including shallow-draft ports and intermittent grid reliability, limit scale for now. Rural Mekong Delta provinces lag due to sparse charging networks, though electric fishing vessels and agricultural machinery present niche opportunities if battery costs fall another 30% by 2028. Within ASEAN, Vietnam competes with Thailand’s USD 1.4 billion battery project pipeline and Indonesia’s nickel-anchored gigafactories. Local rare-earth reserves lend a future comparative advantage for motor magnet supply, but the absence of lithium resources keeps the country dependent on imports.

Competitive Landscape

The Vietnam battery market hosts moderate fragmentation. Legacy lead-acid houses such as GS Battery Vietnam, PINACO, and Vision Group still dominate SLI and motive niches. In lithium-ion, Samsung SDI and Panasonic Energy operate consumer-electronics lines, while the VinES-Gotion joint venture commands the largest committed EV-cell capacity at 5 GWh. LG Energy Solution’s Hue pack project chases 80% localization to satisfy potential content rules tied to incentives.

Competitive dynamics bifurcate along technology. Multinationals invest in solid-state and high-nickel chemistries, seeking performance leadership. Domestic firms and Chinese entrants focus on cost-optimized lithium-iron-phosphate modules for e-motorcycles and distributed storage. White-space persists in grid-scale storage where no dominant supplier has emerged due to regulatory ambiguity. Early movers in flow or sodium-sulfur batteries could secure long-duration niches once ancillary-services pricing materializes.

Strategic moves in 2025 included LG Energy Solution’s MOU with Kim Long Motor, SK On’s pilot solid-state plant, and VinES’ pilot BESS deployment, all signaling a shift from import reliance toward local manufacturing depth. Market participants that accelerate R&D or secure upstream material supply will defend share as technology cycles compress.

Vietnam Battery Industry Leaders

Vision Group

PINACO

GS Battery Vietnam Co. Ltd

Leoch Battery Corporation

Heng Li (Vietnam) Battery Technology Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: SK On opened a solid-state pilot facility and pulled commercialization forward to 2029.

- August 2025: LG Energy Solution inked a cell-supply MOU with Kim Long Motor, targeting 1 GWh capacity and 80% localization by Q2 2026.

- July 2025: Hanoi issued a fossil-fuel motorcycle ban within Ring Road 1 effective Jul 2026.

- May 2025: Ho Chi Minh City has detailed plans to convert 400,000 motorcycles to electric drive from 2026.

- April 2025: T&T Group announced a 2 GWh storage-products joint venture, scaling to 10 GWh.

Vietnam Battery Market Report Scope

A battery is a device that converts chemical energy contained within its active materials directly into electric energy by means of an electrochemical oxidation-reduction (redox) reaction.

The Vietnamese battery market is segmented by battery type, technology and application. By battery type market is divided into primary batteries and secondary batteries. By technology, the market is segmented into lead-acid batteries, lithium-ion batteries, and other battery types. By application, the market is segmented into automotive, industrial, portable, power tools, and other applications. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Battery Type

| Primary Batteries |

| Secondary Batteries |

By Technology

| Lead-acid |

| Li-ion |

| Nickel-metal hydride |

| Nickel-cadmium |

| Sodium-sulfur |

| Solid-state |

| Flow Battery |

| Emerging chemistries |

By Application

| Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) |

| Portable (Consumer Electronics, etc.) |

| Power Tools |

| SLI |

| Other Applications |

| By Battery Type | Primary Batteries |

| Secondary Batteries | |

| By Technology | Lead-acid |

| Li-ion | |

| Nickel-metal hydride | |

| Nickel-cadmium | |

| Sodium-sulfur | |

| Solid-state | |

| Flow Battery | |

| Emerging chemistries | |

| By Application | Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) | |

| Portable (Consumer Electronics, etc.) | |

| Power Tools | |

| SLI | |

| Other Applications |

Key Questions Answered in the Report

How large is the Vietnam battery market in 2026?

The Vietnam battery market size stood at USD 1.13 billion in 2026.

Which battery technology is growing fastest in Vietnam?

Solid-state batteries are forecast to grow at nearly 30% annually to 2031, outpacing lithium-ion and lead-acid.

What share of Vietnam battery demand comes from automotive uses?

Automotive applications held 42.5% of market demand in 2025 and remain the largest single segment.

Why is raw-material supply a risk for Vietnamese battery makers?

Vietnam imports 80-100% of lithium and most cathode inputs, exposing producers to price volatility and geopolitical supply shocks.

What incentives exist for local battery manufacturing?

The government offers tax holidays, duty exemptions, and land-lease discounts in priority zones such as Ha Tinh and Hai Phong.

When will large-scale battery energy storage become viable?

Widespread deployment awaits clear ancillary-services pricing and standardized grid-connection rules, expected after 2027.

Page last updated on: