Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

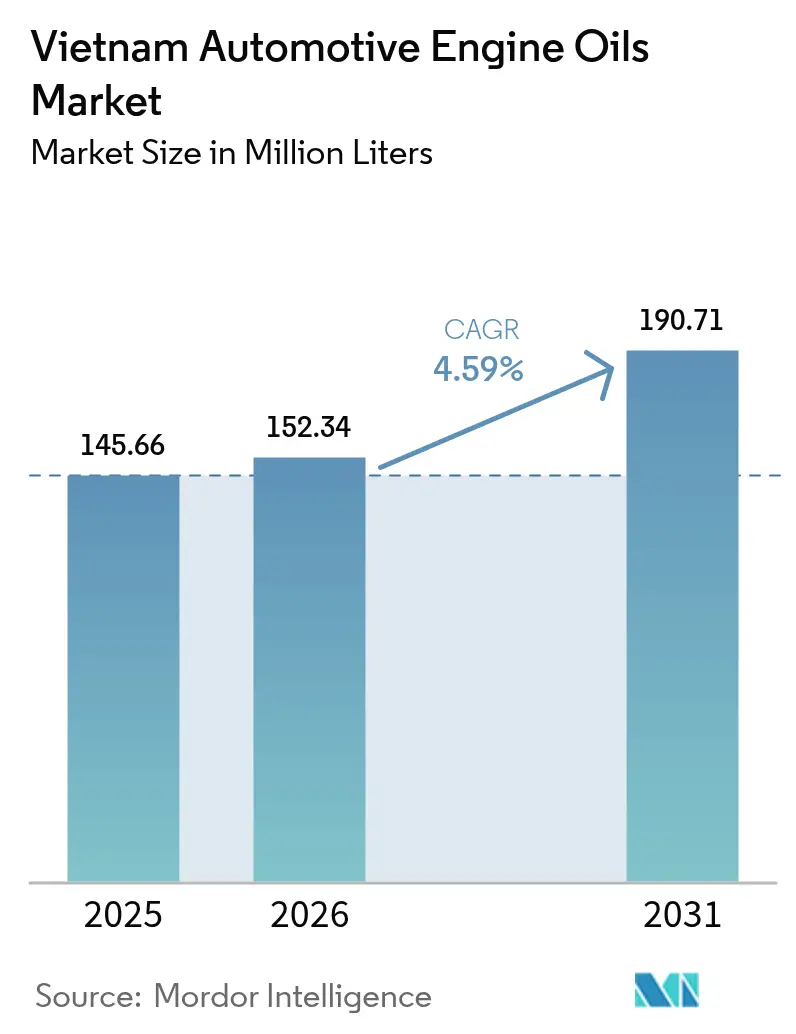

| Base Year Market Size (2025) | 145.66 Million Liters |

| Market Volume (2026) | 152.34 Million Liters |

| Market Volume (2031) | 190.71 Million Liters |

| Growth Rate (2026 - 2031) | 4.59% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Automotive Engine Oils Market Analysis by Mordor Intelligence

The Vietnam Automotive Engine Oils Market size is expected to grow from 145.66 million liters in 2025 to 152.34 million liters in 2026 and is forecast to reach 190.71 million liters by 2031 at 4.59% CAGR over 2026-2031. Sustained lubricant consumption stems from the country’s 73 million-strong motorcycle fleet, faster oil-change cycles compared with passenger cars, and incremental demand from localized engine production. Premiumisation trends are unfolding as consumers shift to low-viscosity synthetics, while government incentives for domestic blending encourage cost-competitive local supply. Multinational and state-owned players focus on technology ties and digital sales to protect share, and counterfeit mitigation and e-commerce authentication tools gain prominence as online volumes rise. At the same time, the looming electric-vehicle (EV) pivot and higher environmental levies compel blenders to optimize formulations and margins.

Key Report Takeaways

- By product type, passenger car motor oil led the Vietnam automotive engine oils market with a 61.45% share in 2025, whereas motorcycle engine oil is projected to grow at a 4.78% CAGR through 2031.

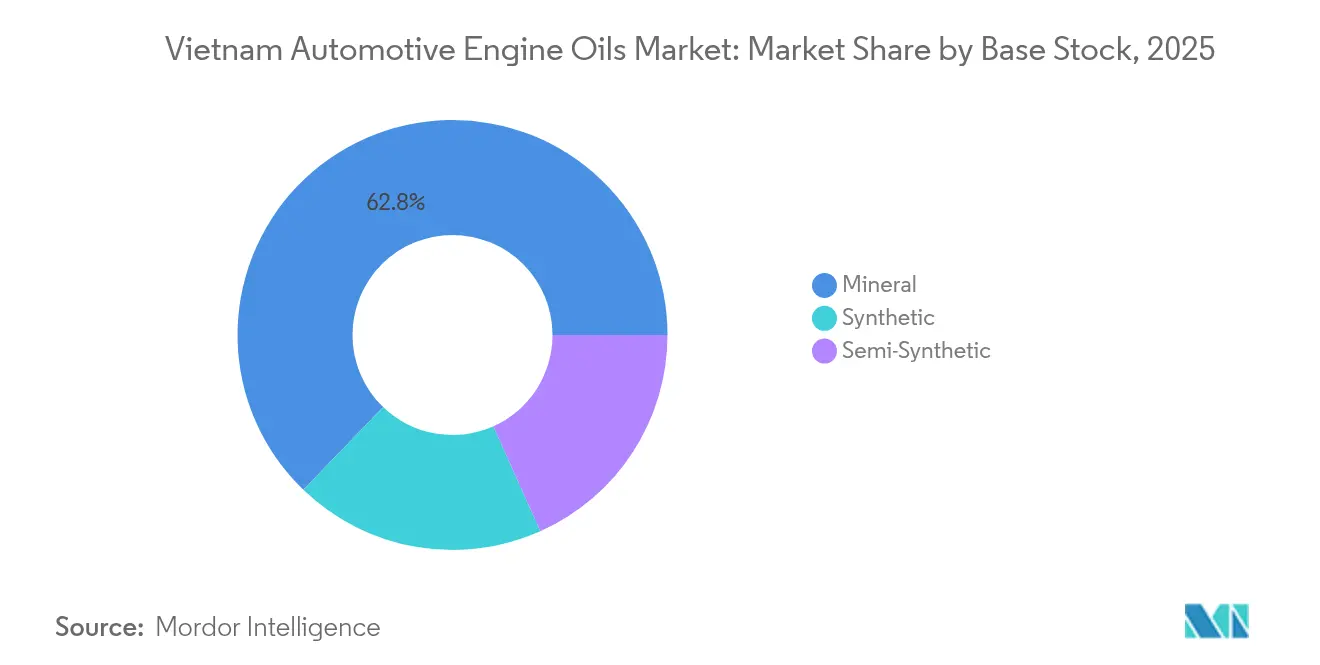

- By base stock, mineral grades accounted for 62.80% of the Vietnam automotive engine oils market size in 2025, while synthetic oils are advancing at a 4.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging motorcycle parc and maintenance frequency | +1.80% | Ho Chi Minh City, Hanoi, Mekong Delta | Long term (≥ 4 years) |

| Government incentives for domestic oil blending capacity | +0.90% | Ba Ria-Vung Tau, Nghe An | Medium term (2-4 years) |

| Shift toward low-viscosity synthetic grades | +0.70% | Urban corridors, spreading to rural areas | Medium term (2-4 years) |

| E-commerce expansion in lubricant retailing | +0.50% | Nationwide, led by major metropolitan areas | Short term (≤ 2 years) |

| OEM factory-fill localisation partnerships | +0.40% | Thua Thien Hue, Ba Ria-Vung Tau, Dong Nai | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Motorcycle Parc and Maintenance Frequency

More than 73 million gasoline two-wheelers require oil changes every 3,000–5,000 kilometers, compared with 10,000–15,000 kilometers for cars, so lubricant throughput remains high even as new bike sales soften. Honda’s share across motorcycle sales drives standardized servicing, helping branded oils secure repeat volumes. The motorcycle segment generated a significant percent of national lubricant demand in 2024, underscoring its weight in overall consumption. Rural ownership continues to rise thanks to upgraded roads and higher disposable incomes, expanding the replacement cycle. Ageing bikes in peripheral provinces further elevate change frequency, offsetting modest electrification in core cities.

Government Incentives for Domestic Oil Blending Capacity

Authorities encourage local blending to curb import reliance, exemplified by Fuchs’ EUR 9 million (USD 10.2 million) plant in Ba Ria-Vung Tau and the USD 1.2 billion Dung Quat refinery upgrade to 7.5 million tons per year. Fiscal perks, streamlined licensing, and land-use support cut operating costs for blenders, letting them target mainstream price points with made-in-Vietnam labels. Partnerships such as ongoing Aramco-Petrolimex talks hint at deeper downstream collaboration that could seed ASEAN export potential. Domestic capacity also helps cushion distributors against freight volatility and foreign-exchange swings, a structural upside for independent retailers.

Shift Toward Low-Viscosity Synthetic Grades for Fuel Economy

Euro 5 emissions, fuel-economy rules, and PVOIL’s premium fuel rollout nudge motorists toward 5W- and 10W-grade synthetics, prized for thermal stability and extended drains. Commercial fleet operators embrace synthetics to trim downtime, while consumer education through OEM workshops accelerates acceptance. Semi-synthetics offer a transitional bridge for cost-sensitive riders, especially in the motorcycle channel. Malaysia’s experience, where synthetics cross 40% share, serves as a regional signpost and bolsters supplier confidence. Innovative hybrids such as PTT’s EVOTEC blend address internal-combustion and electric-assisted units, future-proofing portfolios.

E-Commerce Expansion in Lubricant Retailing

Shopee, Lazada, and PVOIL Easy collectively grow lubricant traffic in Vietnam’s online sphere, helping blenders reach riders outside tier-one cities. PVOIL Easy boosted B2B volumes 20% year-over-year in 2024, while its 4U app logged 35,000 registrations, showing openness to digital re-ordering[1]PVOIL, “Retail Expansion and Digital Transformation,” pvoil.com.vn . The 2023 Consumer Rights Law holds platforms liable for fakes, prompting QR-based authentication such as Yamaha’s scheme. Verified e-stores cut channel layers, preserve margins, and generate user data that underpin tailored promotions. Yet vigilance is critical as Ho Chi Minh City authorities seized more than 220,000 counterfeit bottles in 2024, highlighting persistent gray-market threats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing EV penetration in urban centres | -0.80% | Ho Chi Minh City, Hanoi | Long term (≥ 4 years) |

| Counterfeit / grey-market engine oils | -0.60% | Nationwide, online and informal channels | Short term (≤ 2 years) |

| Crude-price volatility squeezing blender margins | -0.40% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing EV Penetration in Urban Centres

Government targets of 350,000 EVs by 2030 and PVOIL’s rollout of 369 charging points begin to erode combustion-engine lubricant volumes, especially among taxi and ride-hail fleets[2]PVOIL, “EV Charging Network Update,” pvoil.com.vn . Two million electric motorcycles already circulate, advancing 30–35% annually, although from a low base. E-fluids for gearboxes and thermal management partially offset the lost engine oil, but lack a comparable volume density. Outside Hanoi and Ho Chi Minh City, limited charging and rural duty cycles preserve internal-combustion dominance until infrastructure matures. Hence, the headwind remains gradual, yet strategic investors already price this shift into long-range capacity plans.

Counterfeit / Grey-Market Engine Oils

Fake oil operations dilute brand equity and risk engine damage, as a 2024 bust in Ho Chi Minh City uncovered 220,000 counterfeit packs mixing unidentified base stocks with premium labels. Platforms now face statutory liability, but enforcement gaps persist, especially in informal workshops. Blenders spend more on tamper-evident packaging and consumer education, pushing up operating costs. Price-sensitive riders sometimes trade authenticity for savings, giving counterfeiters recurring demand. Repeated seizures and QR verification are gradually curbing the issue, yet near-term growth suffers a measurable drag.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PCMO Dominance Masks MCO Growth Momentum

Passenger Car Motor Oil retained a 61.45% slice of the Vietnam automotive engine oils market share in 2025 as the passenger-vehicle fleet rose to 510,000 units. Motorcycle Engine Oil, however, posts the quickest clip at 4.78% CAGR to 2031, propelled by 73 million active bikes requiring changes every 3,000–5,000 kilometres. Heavy-Duty Motor Oil services freight trucks on arterial corridors linking Ho Chi Minh City and Hanoi to export ports, reinforcing steady baseline volume.

The Vietnam automotive engine oils market benefits from 1.6% growth in motorcycle imports to 464,194 units through February 2025, while passenger car imports grew to 172,240 units in 2024. Honda’s dominance simplifies compatibility for suppliers, whereas car OEM fragmentation widens product portfolios. High-performance lines such as Motul 300V Road Racing and Yamaha’s anti-counterfeit Yamalube enhance segment segmentation and capture price premium.

By Base Stock: Mineral Oils Lead While Synthetics Accelerate

Mineral grades secured 62.80% of the Vietnam automotive engine oils market in 2025 because of accessible pricing and entrenched supply networks. Yet synthetics will likely outpace at a 4.82% CAGR to 2031 as Euro 5 standards and fuel-saving awareness spread. Semi-synthetics bridge affordability and performance, appealing to urban commuters upgrading from mineral oils.

Vietnam automotive engine oils market size for synthetic blends is predicted to reach double-digit share by 2030 as OEM manuals specify 5W-30 or 10W-40 fluids for new vehicle warranties. Malaysia’s 40% synthetic penetration indicates regional viability, and PTT’s EVOTEC hybrid-ready formula demonstrates that advanced additives can future-proof lubricant relevance. Bio-based oils remain niche, yet policy momentum around sustainability suggests a slow but incremental foothold in commercial fleets.

Geography Analysis

Ho Chi Minh City and Hanoi concentrate the majority of lubricant consumption because they house the densest vehicle registrations and fleet bases. The Vietnam automotive engine oils market size in these hubs grows steadily on the back of service-centric incomes and strict maintenance regimes. Ho Chi Minh City’s higher disposable incomes pivot demand toward premium synthetics, and workshop chains cluster to capture wallet share. Hanoi’s government fleets and industrial logistics require predictable, OEM-approved fluids, benefiting brands with compliance certifications.

The Mekong Delta fuels substantial motorcycle oil turnover; humid climate and agricultural roadways cause more frequent oil degradation. Provincial workshops lean on mineral formulations, though wider e-commerce access is slowly introducing semi-synthetics. Manufacturing corridors spanning Ba Ria-Vung Tau, Dong Nai, and Binh Duong draw industrial and factory-fill volumes as blending plants come onstream, cutting lead times for OEM contracts.

Central Vietnam is emerging through the Yuchai engine complex in Thua Thien Hue, which will anchor localised supply chains and specialty grade demand. Cross-border trade sees Petrolimex subsidiaries funnel product into Laos and Cambodia, leveraging improved highways. Coastal provinces add marine engine oil demand for the country’s fishing armada, while mountainous northern routes challenge distributors, reinforcing the value of Petrolimex’s provincial depots and PVOIL’s 838-station reach.

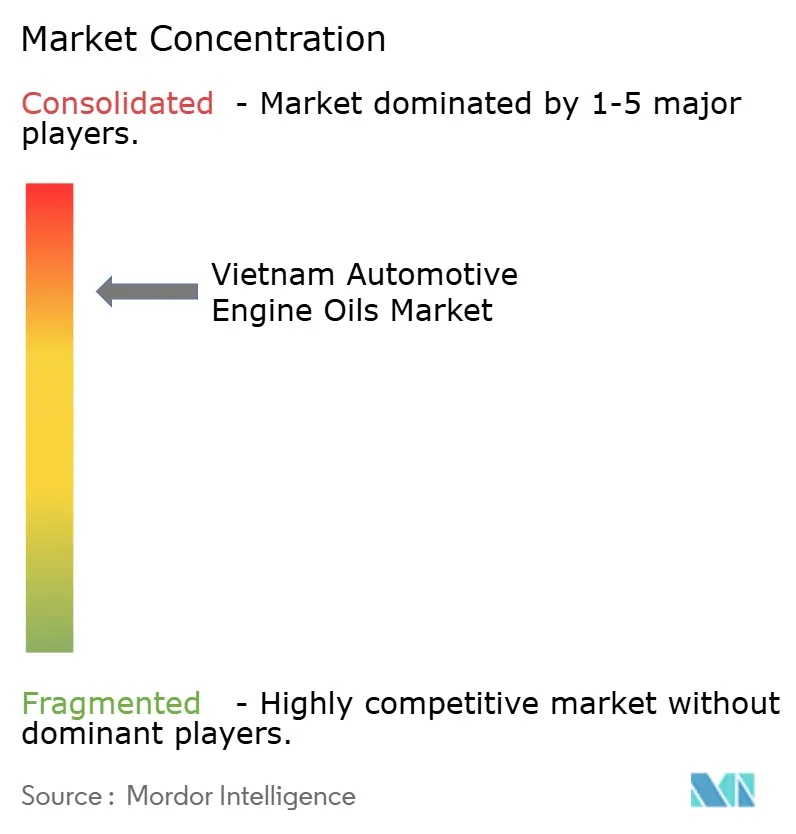

Competitive Landscape

The Vietnam automotive engine oils market exhibits highly consolidated concentration. Castrol BP Petco, Petrolimex, and PVOIL control a sizeable share through entrenched retail footprints and OEM alliances. Castrol’s joint-venture lineage ensures brand familiarity, though 2024 revenue tapered amid margin pressure. Petrolimex integrates upstream refining and downstream retail, enabling price agility, whereas PVOIL combines 838 stations with a digital B2B platform that saw 150,000 m³ transactions in 2024.

Strategic differentiation centers on anti-counterfeit measures and hybrid-compatible blends. Yamaha’s QR-embedded Yamalube and PTT’s green-innovation roadmap illustrate defensive and offensive tactics. Domestic players leverage tax incentives and proximity to engage OEMs in factory-fill deals, while multinationals supply advanced additive packages. Compliance with QCVN 04/77/86/109:2024 boosts the relevance of firms with global R&D backing, elevating the barrier to entry for new brands without certifications.

Future rivalry may intensify in the synthetic tier as price gaps narrow and EV drivelines demand ancillary fluids. Partnerships with charging-station operators and data-rich digital storefronts will likely determine share gains, and counterfeiting clampdowns could reallocate revenue toward legitimate channels. Overall, brand equity, distribution agility, and technical accreditation remain decisive levers in sustaining leadership.

Vietnam Automotive Engine Oils Industry Leaders

Petrolimex (PLX)

Shell Plc

Exxon Mobil Corporation

Motul Vietnam (Vilube)

BP p.l.c.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: TotalEnergies partnered with Cao Gia Quy Environment Company to recycle waste engine oil in Vietnam. This initiative ensures compliance with Vietnam's EPR regulations, requiring lubricant companies to recycle 15% of their engine oil or contribute to the Vietnam Environment Protection Fund.

- November 2024: Champion Lubricants, a brand of Belgium's Wolf Oil Corporation, entered the Vietnamese market through an exclusive distribution agreement with Vietsea Company. The brand offers lubricants for motorcycles, passenger cars, commercial vehicles, and maintenance solutions.

Vietnam Automotive Engine Oils Market Report Scope

By Product Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

Key Questions Answered in the Report

What is the current volume outlook for Vietnam’s automotive engine oils?

Consumption stands at 152.34 million liters in 2026 and is projected to reach 190.71 million liters by 2031.

Which lubricant segment is expanding fastest?

Motorcycle Engine Oil is growing at a 4.78% CAGR to 2031 due to frequent change intervals and a 73 million-unit bike fleet.

How dominant are mineral oils versus synthetics in Vietnam?

Mineral grades held 62.80% share in 2025, but synthetics are forecast to post a 4.82% CAGR as fuel-economy norms tighten.

What key factor drives lubricant demand in rural areas?

High motorcycle ownership combined with challenging road conditions triggers more frequent oil changes, anchoring rural demand.

How does EV adoption affect lubricant sales?

EVs reduce traditional engine-oil volumes, but the impact remains modest until after 2030 due to infrastructure and rural mobility patterns.

Page last updated on: