Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

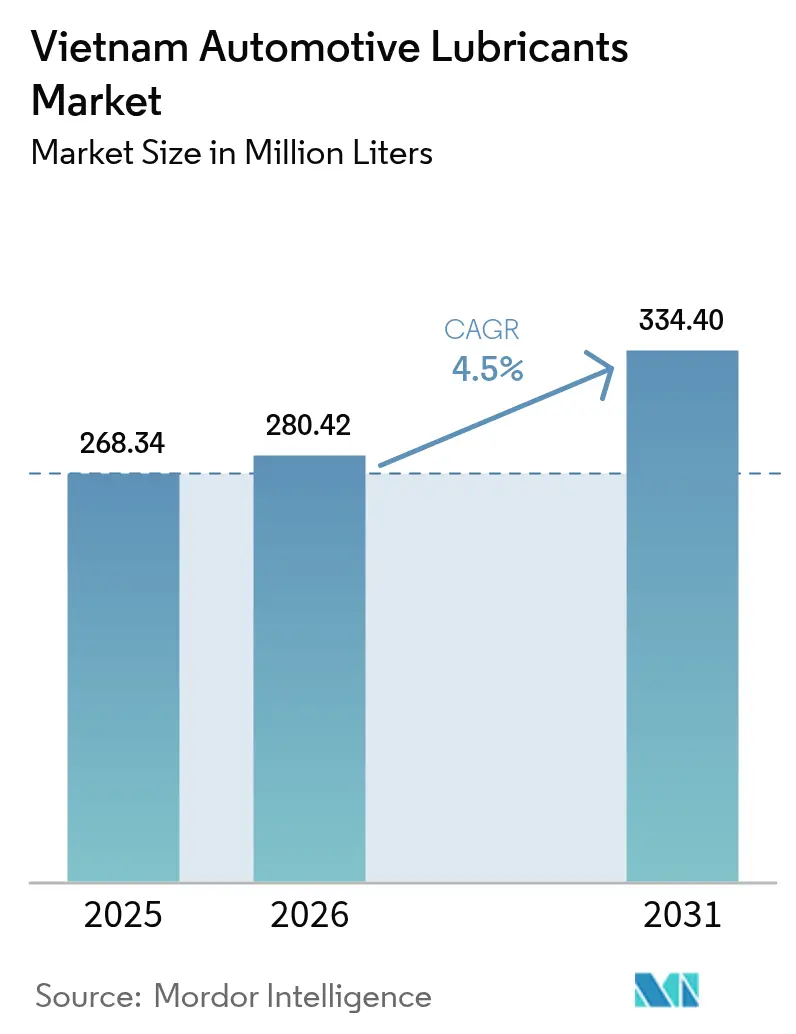

| Base Year Market Size (2025) | 268.34 Million liters |

| Market Volume (2026) | 280.42 Million liters |

| Market Volume (2031) | 334.40 Million liters |

| Growth Rate (2026 - 2031) | 4.50% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Automotive Lubricants Market Analysis by Mordor Intelligence

The Vietnam Automotive Lubricants Market size is expected to increase from 268.34 million liters in 2025 to 280.42 million liters in 2026 and reach 334.40 million liters by 2031, growing at a CAGR of 4.5% over 2026-2031. Robust demand stems from the country’s 70 million-unit motorbike fleet, the fastest-growing e-commerce delivery networks, and government-supported refinery upgrades that are enabling local blending of advanced API SP and ILSAC GF-6 oils. Multinational suppliers preserve brand equity through premium synthetics while state-owned fuel retailers leverage 8,100 service stations to bundle economy-grade oils with gasoline sales. Ride-hailing fleets, now managing more than 500,000 registered drivers, institutionalize 3,000 km oil-change cycles that add predictable volume even as electrification gains initial traction. Counterfeit products and environmental levies on used-oil disposal slightly temper volumes but simultaneously accelerate the migration toward higher-margin synthetics and closed-loop re-refining systems.

Key Report Takeaways

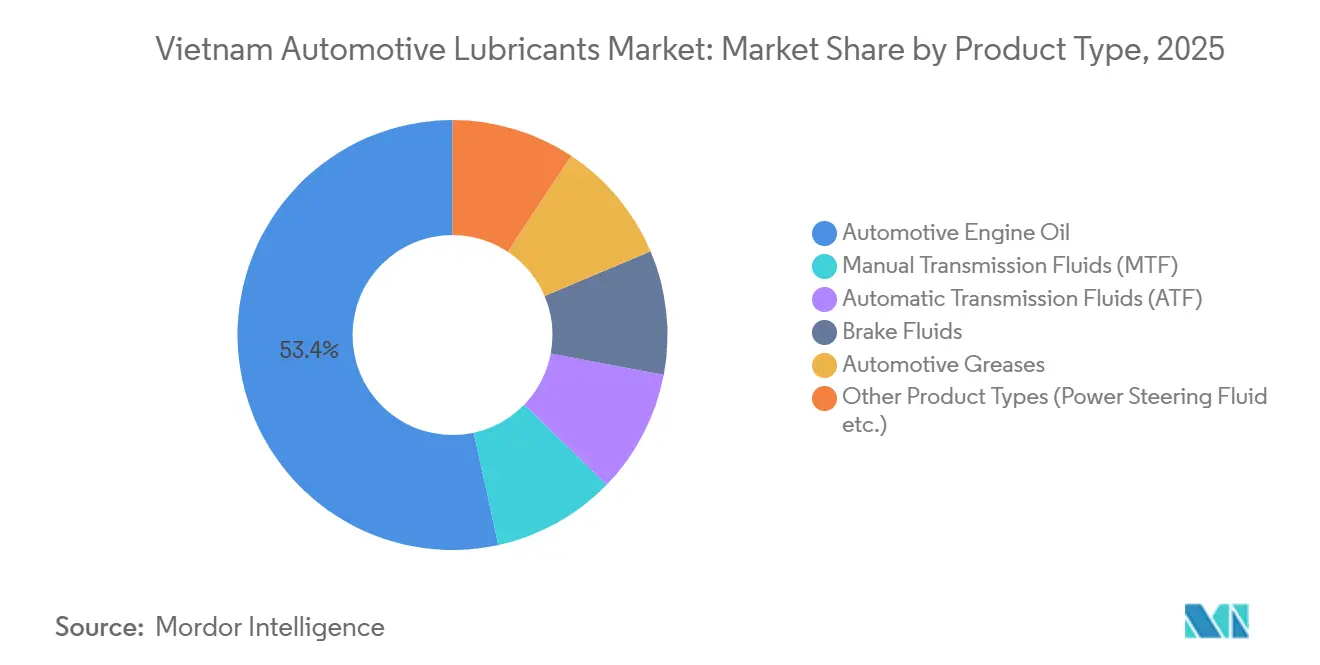

- By product type, Automotive Engine Oil led with a 53.42% share of the Vietnam automotive lubricants market in 2025. Automatic Transmission Fluids are forecast to expand at a 4.71% CAGR through 2031, the quickest among product categories.

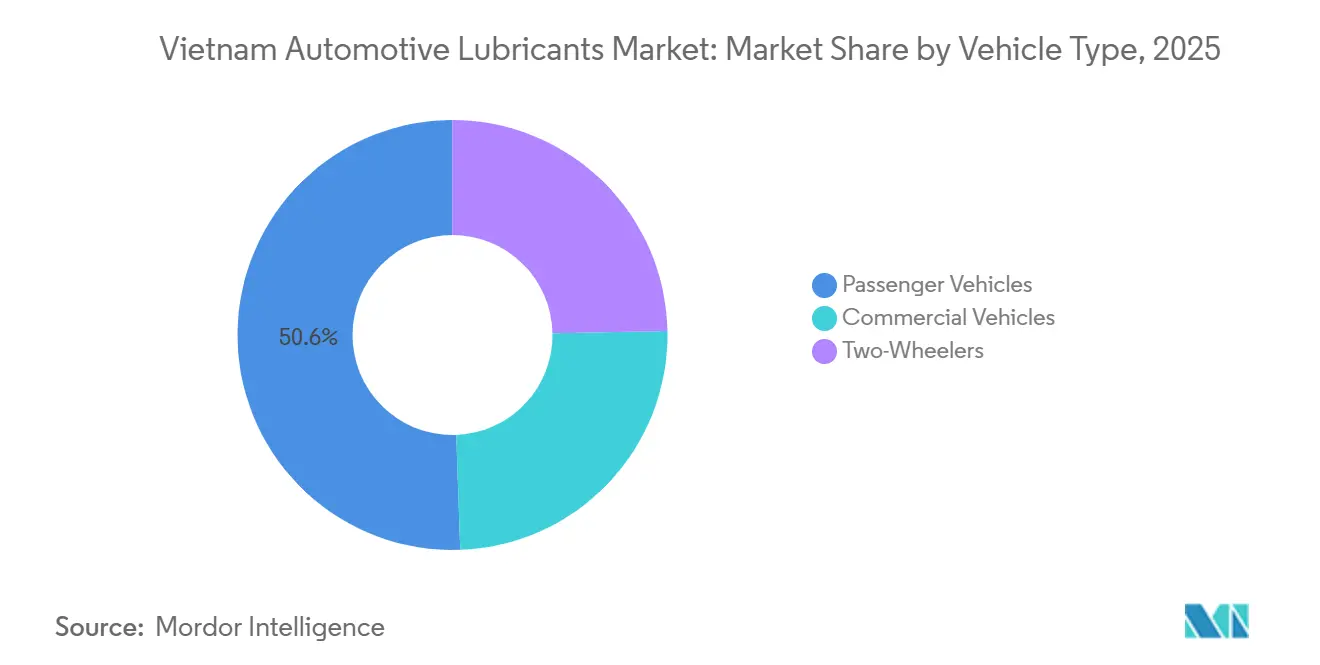

- By vehicle type, Passenger Vehicles accounted for 50.58% of the 2025 volume. Commercial Vehicles are advancing at a 4.92% CAGR over 2026-2031, the fastest among vehicle classes.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Two-wheeler dominance in urban mobility | +1.2% | Hanoi and Ho Chi Minh City | Medium term (2-4 years) |

| Surge in e-commerce logistics fleets | +1.0% | National, early gains in major urban hubs | Short term (≤ 2 years) |

| OEM extended-drain interval specifications | +0.8% | Spill-over to Vietnam assembly plants | Long term (≥ 4 years) |

| Rapid growth of ride-hailing motorbike fleets | +0.7% | Urban centers, expanding into tier-2 cities | Medium term (2-4 years) |

| Government incentives for local blending | +0.6% | Dung Quat and Nghi Son refinery catchments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Two-Wheeler Dominance in Urban Mobility

Vietnam’s registered motorbike parc surpassed 70 million units in 2025. Despite a slight contraction in new sales, each motorbike still undergoes three to four oil changes a year, forming a dependable demand base that insulates the Vietnam automotive lubricants market from swings in car sales[1]Vietnam Association of Motorcycle Manufacturers, “Motorcycle Industry Statistics 2025,” vamm.org.vn. Euro 5 emission rules, effective 2026, are steering riders toward low-SAPS API SN Plus and JASO MA2 oils, pushing premium synthetics deeper into mass retail. Electric scooter uptake, while expanding at triple-digit rates, has yet to materially dent lubricant volumes because bearings, brake hydraulics, and drivetrains continue to need greases and fluids, albeit in smaller quantities.

Surge in E-Commerce Logistics Fleets

Vietnam’s gross merchandise value rose from USD 22 billion in 2023 to an estimated USD 52 billion in 2025. Parcel networks responded by enlarging fleets 40-50%, subjecting engines to stop-start duty cycles that halve traditional drain intervals. Operators now favor semi-synthetic 10W-40 and 5W-30 oils that deliver thermal stability under 14-hour workdays. A 2024 decree requiring platforms to publish vehicle maintenance records is enforcing OEM-grade lubricant adoption and accelerating market formalization[2]Ministry of Industry and Trade, “Decree on Vehicle Standards for E-commerce Platforms,” moit.gov.vn.

OEM Extended-Drain Interval Specifications

Toyota, Honda, Hyundai, and VinFast have stretched factory-fill drains from 5,000 km to 10,000 km for gasoline engines and to 15,000 km for diesels by upgrading to API SP and ILSAC GF-6B formulation. Although this lowers per-vehicle liters, it lifts revenue because synthetic oils carry 50-80% premiums. The planned 171,000 bpd Dung Quat hydrocracker will supply Group II base stocks locally, shielding domestic blenders from freight volatility and exchange-rate risks while boosting the Vietnam automotive lubricants market’s self-reliance.

Rapid Growth of Ride-Hailing Motorbike Fleets

Ride-hailing revenue is projected to escalate from USD 880 million in 2024 to USD 2.16 billion by 2029. Platforms enforce 3,000 km or 30-day oil-change schedules for more than 500,000 active drivers, institutionalizing lubricant demand. Xanh SM’s deployment of 27,000 electric cars is creating niche demand for high-margin EV coolants and single-speed transmission fluids at two-to-three-times the margin of conventional oils. Proposed Ministry of Transport rules capping vehicle age promise quicker fleet turnover and additional lubricant throughput.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-sensitive consumers using low-grade oils | −0.5% | Rural and peri-urban districts | Short term (≤ 2 years) |

| Expanding counterfeit lubricant trade | −0.4% | Informal workshops and roadside stalls | Medium term (2-4 years) |

| Stricter levy on used-oil disposal | −0.3% | Industrial zones first, national roll-out later | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price-Sensitive Consumers Favoring Mineral Oils

Approximately 70% of vehicle owners prioritize upfront price, driving persistent demand for monograde 20W-50 and 15W-40 mineral oils that retail at 30-40% below synthetics. These oils deliver thinner gross margins and dilute premium-brand positioning in the Vietnam automotive lubricants market. Private-label brands imported from secondary refiners in China and India compound the erosion, often bypassing API licensing.

Growing Counterfeit Lubricant Trade

Counterfeits occupy up to 20% of informal volumes. In 2024, Ho Chi Minh City authorities seized 50,000 liters of fraudulent Shell, Castrol, and Mobil products during 1,200 inspections. Widespread QR-code authentication pilots and direct-to-consumer e-commerce storefronts have emerged as brand-protection countermeasures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Synthetic Blends Narrow the Gap with Conventional Oils

Automotive Engine Oil captured 53.42% of the Vietnam automotive lubricants market share in 2025 as internal-combustion engines remained the default powertrain across passenger, commercial, and two-wheeler segments. The Vietnam automotive lubricants market size for automatic transmission fluids is projected to climb at a 4.71% CAGR through 2031, propelled by the spread of CVTs in models such as the Honda City and Toyota Vios. Semi-synthetic 10W-40 grades anchor fleet demand by extending drains without breaching cost ceilings. Brake Fluids and Greases remain niche but critical for safety-compliance audits now common among e-commerce fleets.

A convergence toward lower-viscosity 5W-30 and 0W-20 grades is emerging as OEM factory fills embrace fuel-efficiency mandates. Aftermarket riders, however, retain a preference for 10W-40 or 15W-40 mineral oils, reinforcing a dual-channel inventory challenge for distributors. Ministry of Transport guidelines added in 2024 now oblige workshops to stock API SN Plus or higher, nudging even budget clients toward better-performing synthetics.

By Vehicle Type: Commercial Fleets Outpace Passenger Segment on Logistics Tailwinds

Passenger Vehicles accounted for 50.58% of lubricant volume in 2025, but commercial vehicles are forecast to record the quickest 4.92% CAGR during 2026-2031. This reflects intense utilization of light trucks and vans that support same-day deliveries, especially around Ho Chi Minh City’s industrial belt. Two-wheelers produce smaller sump volumes yet remain pivotal because they cycle through oil changes three to four times a year, adding resilient throughput to the Vietnam automotive lubricants market size.

Commercial-vehicle drain intervals shorten under twin-shift operations that accumulate 12-14 engine hours daily. Refrigerated vans compound consumption because auxiliary compressors raise lubricant temperatures by 10-15°C. A forthcoming low-SAPS diesel-oil mandate could lift per-liter prices 20-25% but is unlikely to curb volumes because fleet uptime requirements remain uncompromised.

Geography Analysis

Ho Chi Minh City and neighboring provinces generated close to half of Vietnam’s 2025 lubricant demand. Higher vehicle density, a thriving logistics ecosystem, and modern retail channels explain the concentration. Northern Vietnam, led by Hanoi and Hai Phong, contributed roughly one-third, supported by assembly plants that enforce OEM-approved oils from cradle to warranty. The central corridor around Da Nang is smaller but rising on the back of expressway buildouts that stimulate freight movements.

Regional product mixes diverge. Southern consumers, enjoying higher disposable incomes, assign about 40-45% of purchases to synthetics. By contrast, northern and central workshops rely on lower-priced mineral oils, limiting the synthetic share to 25-30%. Suppliers segment strategies accordingly: premium brands lean on authorized dealers in urban hubs, while economy lines penetrate rural communes through petrol-station bundling.

Future competitiveness will pivot on domestic blending near coastal hubs. Fuchs’s 20,000-ton Ba Ria-Vung Tau plant and PVOIL’s Binh Chieu facility already cut import lead times from six weeks to under ten days. The Dung Quat hydrocracker, slated for 2028, will provide Group II base oils that could trim finished-product prices 10-15% relative to imports. Provincial variance in used-oil collection remains a wild card. Ho Chi Minh City and Hanoi reach 60% workshop coverage, whereas many rural districts lag below 20%, creating unequal compliance costs that suppliers must navigate.

Competitive Landscape

The Vietnam automotive lubricants market is moderately consolidated. Castrol BP Petco’s 50,000-ton Nha Be plant underpins its market leadership yet is undergoing a strategic transition as BP divests 65% to Stonepeak for USD 10.1 billion, signaling a shift toward asset-light distribution that may unlock deeper e-commerce penetration. Petrolimex and PVOIL deploy bundled fuel-lubricant offerings across 8,100 service stations, capturing cost-sensitive motorists but sacrificing margin.

Mid-tier entrants capitalize on white-space niches. Fuchs localizes production for just-in-time deliveries to southern industrial clusters, slashing imported lead times. TotalEnergies promotes re-refined base oils that cut carbon footprints by 70% versus virgin Group II, aligning with corporate sustainability scores demanded by multinational fleet operators. Shell’s IoT-enabled bulk dispensers at fleet depots automate reorder points, trimming oil wastage by up to 20% and fortifying annual maintenance contracts.

Electric-vehicle fluids represent the next frontier. Thermal-management coolants and single-speed transmission oils, priced at double or triple conventional engine oils, remain underserved. With VinFast’s electric scooter deliveries growing over 500% in 2025 and ride-hailing platform Xanh SM scaling toward 50,000 EVs, early movers will enjoy outsized margins.

Vietnam Automotive Lubricants Industry Leaders

BP p.l.c.

Shell Plc

Petrolimex (PLX)

TotalEnergies

Idemitsu Kosan Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: TotalEnergies subsidiary Lubrilog launched the PFAS-free Plastogrease range for automotive actuators, anticipating regulator restrictions on per- and polyfluoroalkyl substances.

- June 2025: BP p.l.c. initiated a process to divest its Castrol lubricants arm, valued at up to USD 10 billion, as part of a wider USD 20 billion disposal program scheduled before 2027.

Vietnam Automotive Lubricants Market Report Scope

Automotive lubricants, made from base oils and additives, are specialized fluids and greases. They play a crucial role in minimizing friction, heat, and wear among moving engine and mechanical components. Beyond just reducing wear, these lubricants safeguard against corrosion, eliminate contaminants, and promote the smooth operation of vehicles.

The Vietnam automotive lubricants market is segmented by product type and vehicle type. By product type, the market is segmented into automotive engine oil (0W-XX, 5W-XX, 10W-XX, 15W-XX, monogrades, and other grades), manual transmission fluids (MTF), automatic transmission fluids (ATF), brake fluids, automotive greases, and other product types (power steering fluid, etc.). By vehicle type, the market is segmented into passenger vehicles, commercial vehicles, and two-wheelers. For each segment, the market sizing and forecasts have been done based on volume (liters).

By Product Type

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid, etc.) |

By Vehicle Type

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid, etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Key Questions Answered in the Report

How fast is lubricant consumption growing in Vietnam?

Volume is projected to rise from 280.42 million liters in 2026 to 334.40 million liters by 2031 at a 4.50% CAGR, supported by logistics fleet expansion and sustained motorbike use.

Which product category dominates sales?

Automotive Engine Oil leads with a 53.42% share in 2025, reflecting the prevalence of internal-combustion engines across vehicles.

What is the biggest growth opportunity for suppliers?

Automatic Transmission Fluids, expanding at 4.71% CAGR, and high-margin EV fluids tied to growing electric taxi and scooter fleets present standout prospects.

How does regional demand vary inside Vietnam?

Southern provinces around Ho Chi Minh City account for nearly half of the national volume and buy a higher share of synthetics, while northern and central regions remain more price-driven.

Which companies hold the largest shares?

Castrol BP Petco, Shell, Petrolimex, PVOIL, and TotalEnergies together command roughly 55-60% of the market.

What policies affect used-oil management?

A 2025 levy of VND 2,000 per liter on used-oil disposal is raising compliance costs and encouraging adoption of extended-drain synthetics and formal collection systems.

Page last updated on: