Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

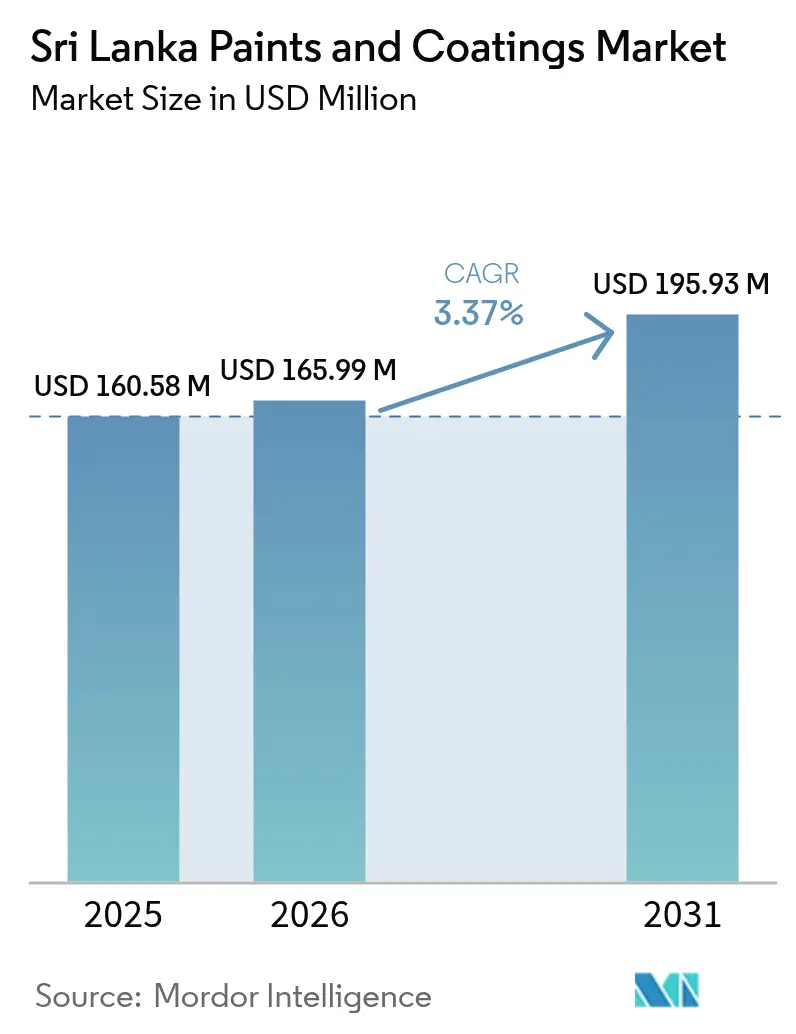

| Base Year Market Size (2025) | USD 160.58 Million |

| Market Size (2026) | USD 165.99 Million |

| Market Size (2031) | USD 195.93 Million |

| Growth Rate (2026 - 2031) | 3.37% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sri Lanka Paints And Coatings Market Analysis by Mordor Intelligence

Sri Lanka Paints and Coatings market size in 2026 is estimated at USD 165.99 million, growing from 2025 value of USD 160.58 million with 2031 projections showing USD 195.93 million, growing at 3.37% CAGR over 2026-2031. Tourism-led construction activity, steady industrial output gains, and a gradual return of consumer confidence after the 2022 balance-of-payments crisis underpin this growth trajectory. The construction sector’s revival is visible in hotel, resort, and mixed-use projects designed to meet rising visitor inflows, while public-sector infrastructure upgrades accelerate demand for protective and waterproof systems. Parallel regulatory tightening on volatile organic compounds steers local producers toward water-borne binders and recycled-content powders that satisfy sustainability mandates and hospitality air-quality guidelines. Currency stabilization, a stronger import-finance pipeline, and healthy remittance inflows have collectively eased raw-material procurement constraints and encouraged producers to restore pre-crisis capacity utilization.

Key Report Takeaways

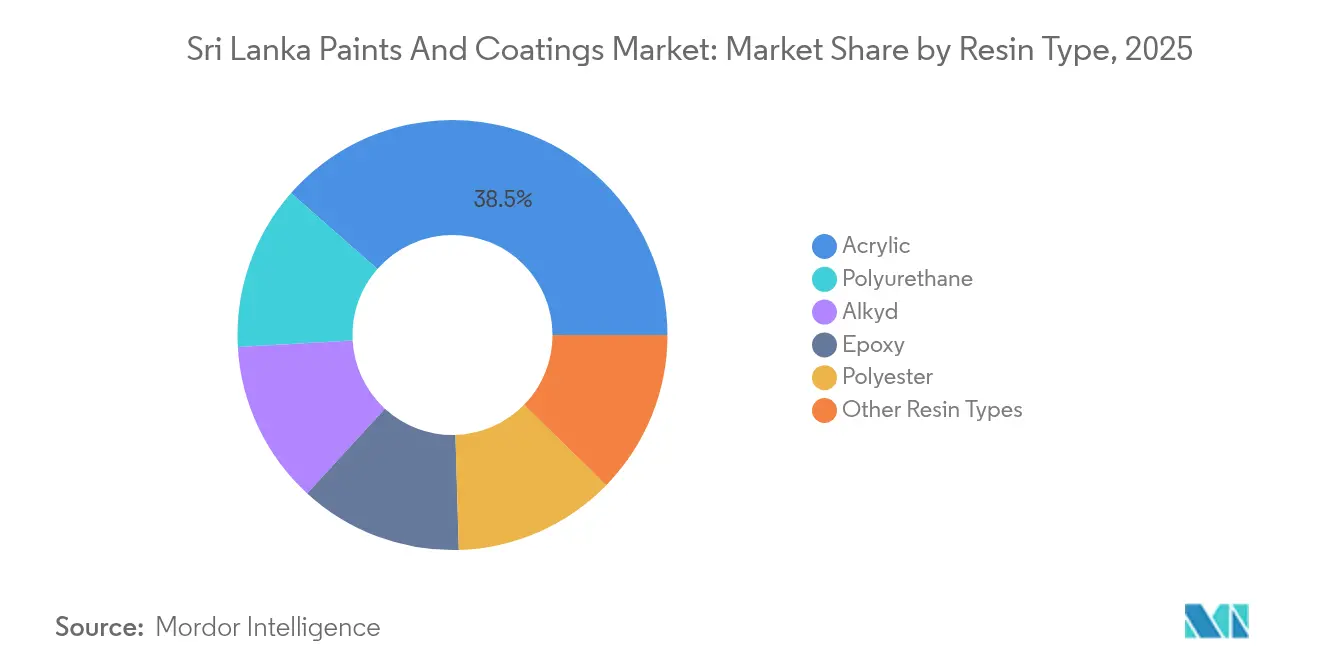

- By resin type, acrylic products accounted for 38.52% of the Sri Lanka Paints and Coatings market share in 2025; polyurethanes are projected to expand at a 3.52% CAGR through 2031.

- By technology, solvent-borne systems held 46.02% revenue share in 2025, whereas water-borne technologies are forecast to post a 3.48% CAGR over 2026-2031.

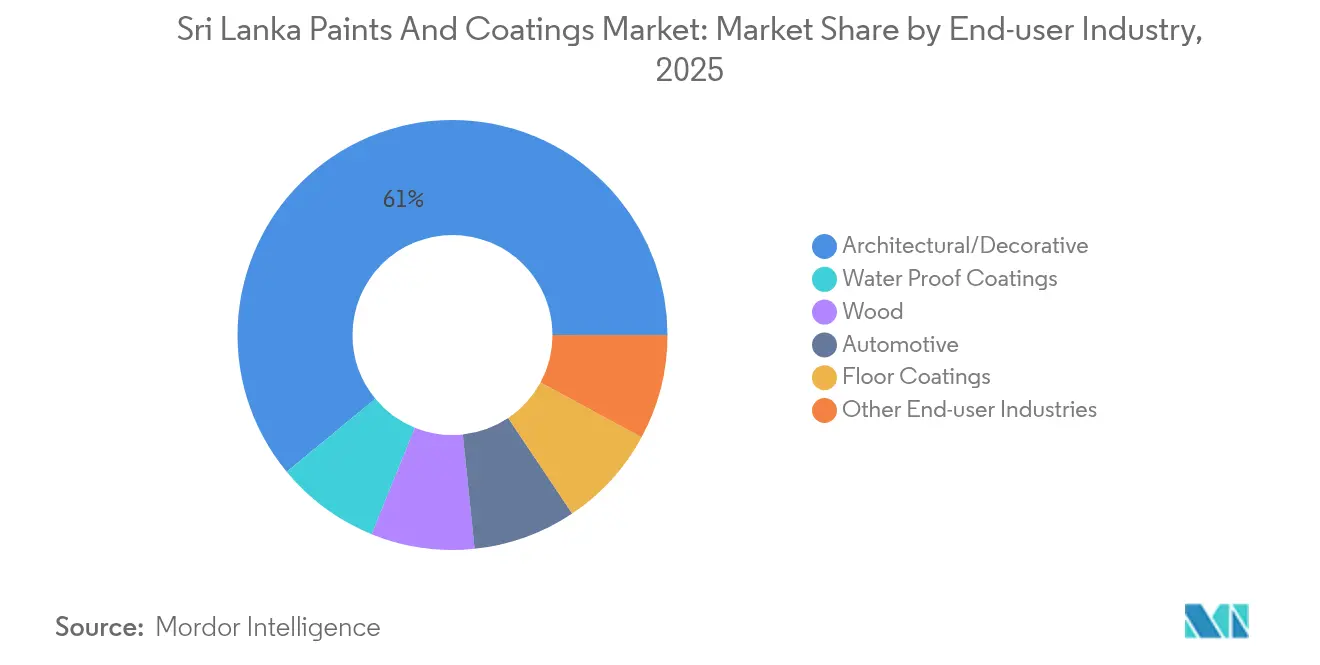

- By end-user, architectural and decorative formulations captured 60.98% revenue share in 2025; waterproof coatings are set to grow the fastest at a 3.58% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Sri Lanka Paints And Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-crisis Construction Rebound | +0.8% | National, with concentration in Western Province | Medium term (2-4 years) |

| Expansion of Automotive Refinish (used-car) Demand | +0.5% | National, with urban concentration | Short term (≤ 2 years) |

| Rising Preference for Polyurethane Performance Coatings | +0.4% | National, industrial zones focus | Long term (≥ 4 years) |

| Government-backed Home-improvement Loan Schemes | +0.6% | National, rural and suburban focus | Medium term (2-4 years) |

| Shift to Water-borne Decorative Paints Driven by VOC Limits | +0.3% | National, manufacturing compliance focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-crisis Construction Rebound

Building activity rebounded sharply after macro-stability returned, delivering a 5% GDP expansion in 2024 that unlocked stalled private investment[1]Reuters Staff, “Sri Lanka GDP Grows 5% Amid Post-Crisis Relief,” Reuters, reuters.com. Colombo’s USD 1 billion City of Dreams resort and the 687-room Cinnamon Life hotel illustrate large-floor-area projects that elevate premium exterior and interior demand. Protective coatings volumes rose with boat-building exports, which reached USD 13.37 million in April 2025 and required marine-grade anti-corrosion systems. Certification under Central Environmental Authority protocols steers new builds toward water-borne and low-VOC formulations. Industrial estate expansion in Western and Southern provinces boosts demand for floor coatings specified for chemical resistance, while hospitality developers insist on low-odor products to minimize downtime during phased renovations.

Expansion of Automotive Refinish Demand

Foreign-exchange normalization lifted used-car imports, and the existing 4.8 million-unit fleet drives steady refinishing throughput in urban workshops. Central bank reserves of USD 5.7 billion have relaxed import licensure, enabling distributors to stock advanced water-borne basecoats and high-solids primers that match global OEM shades[2]Bank for International Settlements, “Sri Lanka Reserve Update,” bis.org. Collision-repair operators increasingly promote nano-ceramic clearcoats that deliver self-cleaning properties aligned with consumer preferences for lower maintenance cycles. Demand also stems from aftermarket integration of sensors for advanced driver-assistance systems, which require optically clear protective topcoats. Local distributors now leverage tariff reductions under the proposed Indo-Sri Lanka and Sri Lanka-Thailand trade accords to import refinish consumables more cost-competitively.

Rising Preference for Polyurethane Performance Coatings

Manufacturing growth of 8.7% in 2025 fuels the uptake of two-component polyurethanes that offer abrasion resistance and extended durability on food-processing machinery. Petrochemical-resistant tank linings specified for upcoming refinery upgrades in Hambantota and Trincomalee further boost volumes. Polyurethane formulations’ shorter return-to-service intervals help offset skilled-labor shortages on project sites. Their compatibility with automated spray systems aligns with productivity gains sought by export-oriented apparel, pharmaceutical, and electronics plants. Board of Investment incentives that reward compliance with the International Organization for Standardization (ISO) 14001 environmental management frameworks reinforce migration to low-emissions polyurethane chemistries.

Government-backed Home-improvement Loan Schemes

Policy-rate reductions from 15.5% to 8% over 2024 enabled commercial banks to relaunch repair-and-renovation credit lines capped at LKR 3 million (USD 8,300) per household. Borrowers increasingly opt for low-odor emulsions and elastomeric waterproofing that qualify for green-finance rebates tied to energy conservation. Rural self-construction, encouraged by microfinance providers, favors affordable acrylic distempers supplied in recyclable pouches that reduce packaging material cost. Housing-deficit mitigation programs that target 189,000 units over 2025–2030 underpin demand for economy-grade exterior emulsion sold through hardware franchises in interior districts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency Volatility Inflating Imported Raw-material Costs | -0.7% | National, import-dependent manufacturers | Short term (≤ 2 years) |

| Softening of New Building Permits Amid Tighter Credit | -0.4% | Urban areas, commercial construction | Medium term (2-4 years) |

| Skilled Applicator Shortage Due to Outward Migration | -0.3% | National, construction and industrial sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Currency Volatility Inflating Imported Raw-material Costs

Sri Lanka imported USD 321.59 million of miscellaneous chemical intermediates and USD 255.21 million of organics in 2024, exposing formulators to exchange swings. Smaller paint makers lack hedging tools, forcing monthly price resets that erode channel confidence. Global epoxy shortages after European anti-dumping tariffs and United States probe findings have pushed Asia-origin bisphenol-A epoxy prices up by 18% since 2023. Working-capital requirements balloon when suppliers demand shorter credit tenors, compelling local firms to trim SKU breadth and defer R&D projects. End-users postpone noncritical repainting when retail tags spike, constraining immediate volume recovery.

Softening of New Building Permits Amid Tighter Credit

Although mortgage rates fell in 2024, loan-to-value ceilings tightened, lengthening developers’ presales cycles and delaying groundbreaks. Colombo’s construction cost index remains one of Asia’s highest, lifted by imported steel and cement surcharges. Commercial landlords struggle to secure anchor tenants under 5-year leases, making lenders cautious about exposure to speculative Grade-A office builds. Public-sector fiscal discipline under the International Monetary Fund (IMF) program restricts capital-works outlays, further tempering institutional demand. Consequently, premium architects defer specifying textured exterior finishes and Polyvinylidene fluoride (PVDF) topcoats with higher square-meter pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Dominance Across Applications

Acrylic formulations accounted for 38.52% of Sri Lanka Paints and Coatings market share in 2025 and are projected to deliver the fastest 3.55% CAGR through 2031. The Sri Lanka paints and coatings market size for acrylic offerings will grow in absolute value alongside residential repainting and hospitality refurbishments that favor low-odor, quick-dry emulsions. Demand also benefits from the resin’s broad compatibility with solvent-borne enamels and water-based lattices, allowing manufacturers to adjust product portfolios without re-engineering entire production lines. Domestic leader JAT Holdings recently installed a 7,200 tpa alkyd plant in Bangladesh to hedge against imported resin cost spikes, signaling the supply-security dividends of backward integration.

The versatility of acrylics extends to textured renders, elastomerics for parapet walls, and direct-to-metal primers that resist tropic humidity. Rural markets still buy budget alkyd gloss enamels for doors and grills, yet rising incomes and brand marketing are nudging consumers toward odor-controlled acrylic enamels. Polyurethane systems capture institutional buyers who need heavy-duty abrasion resistance in food-processing or pharma plants, while epoxy volumes rise where corrosion demands dictate higher cross-link density. Nevertheless, acrylics remain the default binder in the economy and mid-tier masonry segments because tooling and surface-preparation requirements are minimal, keeping contractor labor costs contained.

By Technology: Water-borne Transition Accelerates

Solvent-borne chemistry held 46.02% revenue share in 2025, but water-borne lines are outpacing at a 3.48% CAGR, reflecting the regulatory pull of Central Environmental Authority emissions caps. The Sri Lanka paints and coatings market size for water-borne systems is expected to surpass USD 73.4 million by 2031, buoyed by retail chains’ inventory pivots toward eco-labels that publicize VOC content. Consumer familiarity has improved through Do It Yourself (DIY) campaigns led by national hardware stores, mitigating the traditional perception that water-borne finishes underperform in sheen retention. Powder lines remain niche, reserved for architectural aluminum, domestic-appliance panels, and original equipment manufacturer (OEM) steel furniture, but application is widening following PPG’s launch of ultralow bake ranges that cure at 150°C and lower energy bills.

Solvent products still dominate automotive and industrial maintenance niches that require rapid rebuilds or very high gloss. However, global resin suppliers invest in next-generation water-reducible alkyds and self-cross-linking acrylics to achieve solvent-like flow. Equipment bottlenecks persist because contractors must invest in stainless-steel spray guns and humidity-controlled curing spaces to extract full performance gains. Technical service centers operated by multinationals such as AkzoNobel and Jotun, in alliance with local distributorships, provide the training and color-matching data needed to de-risk the shift at job sites.

By End-user Industry: Architectural Segment Leads Recovery

The architectural and decorative cluster represented 60.98% of 2025 revenues, reflecting robust urban refurbishment and greenfield hospitality builds driven by tourism arrivals that reached 85% of 2019 levels by August 2024. That share underscores how closely the Sri Lanka Paints and Coatings market tracks home-improvement loan origination and commercial lodging occupancy. Shops and multi-family dwelling owners adopt elastomeric waterproof layers for balconies and rooftop parapets given monsoon exposure. In the industrial realm, food-grade epoxy tanks and warehouse floor topcoats register steady orders as processing plants chase Hazard Analysis Critical Control Point (HACCP) certification for export markets.

Waterproof coatings post the fastest 3.58% CAGR because climate adaptation budgets prioritize flood-resistant design. Government civil works agencies mandate positive-side membranes on basements and substructures in coastal zone projects, pulling through large-volume orders. Automotive clearcoat demand is rising after import quotas eased, while the thriving teak-and-rubber furniture sector in Central Province pushes volume in UV-curable wood systems. Marine coatings volumes edge higher as boat-building yards near Galle and Trincomalee clock export contracts for fiberglass leisure craft destined for the Maldives, reinforcing niche demand for anti-fouling tributyltin-free formulations.

Geography Analysis

Western Province generates almost half of the national GDP and is the logistical fulcrum for the Sri Lanka Paints and Coatings market. Colombo’s port handles more than 70% of inbound resin and pigment cargos, giving nearby formulators a freight-cost advantage. The province’s 72.4% services employment share and 25.8% industry share underpin skyscraper refurbishments that specify high-build elastomeric claddings and marine-grade polyurethane for façade metalwork. Major transport-oriented developments such as the Port City SEZ are catalysts for specialized protective systems rated to ISO 12944 C5 coastal classifications. Western Province also houses the densest franchise retail depots, amplifying reach for premium brands that propagate color-consultancy services.

Central and Northern provinces provide steady demand from agro-processing, with Kandy’s 25.6% industrial workforce requiring corrosion-resistant linings on tea dryers and spice grinders. Lower disposable incomes in these districts tilt purchases toward mid-sheen economy emulsions packaged in 1 L and 4 L SKUs. Yet localized manufacturer clinics deliver skill-upgrading workshops that promote higher-margin products by demonstrating washability and mildew-resistance. Northern infrastructure restoration projects, including road resurfacing and public school repainting, channel recurring tender volumes to compliant suppliers carrying Central Environment Authority (CEA) discharge permits.

Eastern and Southern provinces exhibit nascent but fast growth across tourism and fisheries. Trincomalee’s deep-water port expansion attracts ship-repair operations that consume tank-coating cycles measured in thousands of square meters per voyage. Boutique resorts in Arugam Bay and Mirissa elevate demand for pastel-tone exterior emulsions formulated with UV absorbers that withstand sea-spray mist. Hardware cooperatives facilitate procurement for dispersed cottage-construction crews, but distance from resin import nodes adds 5%–8% landed-cost premiums that local stockists pass on through slimmer rebate structures.

Competitive Landscape

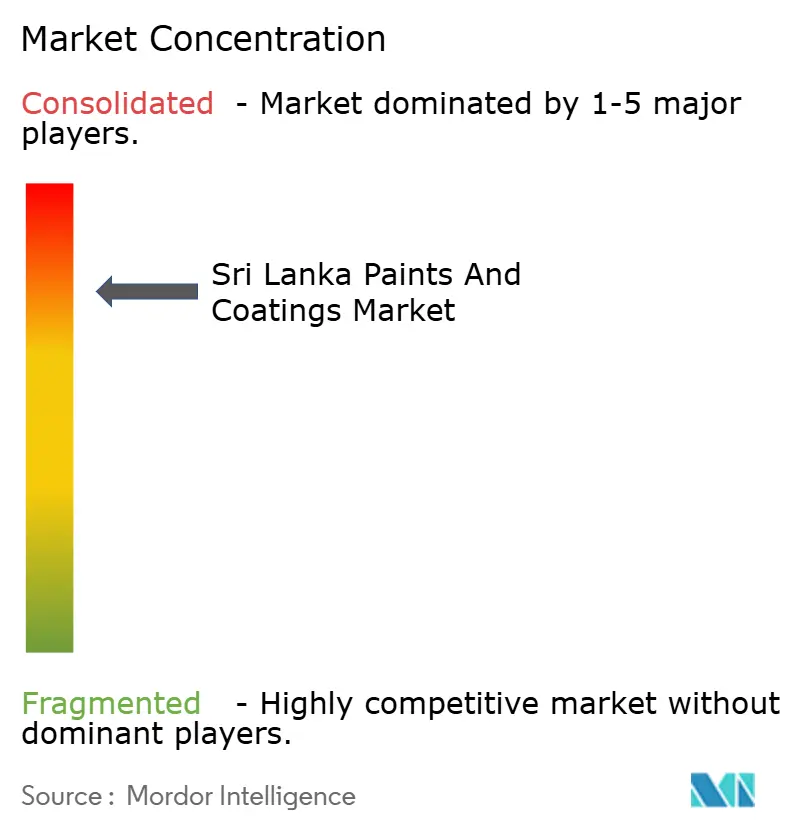

The Sri Lanka Paints and Coatings market is consolidated. Regional challengers compete through rapid-recoat exterior grades that promise 4-hour shower resistance. Kansai Nerolac’s August 2025 injection in fresh equity positions its subsidiary to scale a 6,000 tpa plant in Horana, enabling faster service to southern districts. Jotun’s powder-coating range leverages global marine certification to capture vessel new-builds and dry-dock overhauls. Meanwhile, Sherwin-Williams and PPG run Sri Lanka technical service teams through distributors who align product specs to multinational food-and-beverage client audits. Market entrants must secure Central Environmental Authority operating licenses and Sri Lanka Standards Institute marks, procedural hurdles that favor incumbents familiar with file-review cycles.

Sri Lanka Paints And Coatings Industry Leaders

Asian Paints

JAT Holdings PLC

Nippon Paint Lanka (Pvt) Ltd

Multilac Inc.

AkzoNobel Paints

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: In Sri Lanka, JAT Holdings PLC unveiled Hydro+, a cutting-edge waterproofing paint. Hydro+ harnesses the groundbreaking UV-cross-linking Acrylic-PUD Technology. Specifically designed for tropical climates, Hydro+ creates a robust protective barrier, shielding surfaces from severe environmental challenges.

- August 2025: Kansai Nerolac Paints, a paint manufacturer in India, unveiled its foray into the Sri Lankan market. The company greenlit a substantial investment of LKR 300 million (USD 1.04 million) in its Sri Lankan subsidiary, Kansai Paints Lanka (Private) Limited.

Sri Lanka Paints And Coatings Market Report Scope

The terms paint and coatings are used interchangeably. However, for the most part, paints are considered to be used primarily for aesthetics, while coatings are used principally to prevent substrate deterioration or corrosion protection.

The Sri Lanka Paints and Coatings Market Report is segmented by resin type (acrylic, alkyd, polyurethane, epoxy, polyester, and other resin types), technology (water-borne, solvent-borne, and other technologies), and end-user industry (architectural, automotive, wood, floor coating, waterproof coating, and other end-user applications). The report offers the market size and forecasts for the Sri Lankan Paints and Coatings Market in revenue (USD) for all the above segments.

By Resin Type

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Other Resin Types |

By Technology

| Water-borne Coatings |

| Solvent-borne Coatings |

| Other Technologies |

By End-user Industry

| Architectural/Decorative |

| Automotive |

| Wood |

| Floor Coatings |

| Water Proof Coatings |

| Other End-user Industries |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Other Resin Types | |

| By Technology | Water-borne Coatings |

| Solvent-borne Coatings | |

| Other Technologies | |

| By End-user Industry | Architectural/Decorative |

| Automotive | |

| Wood | |

| Floor Coatings | |

| Water Proof Coatings | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the current value of the Sri Lanka Paints and Coatings market?

It is valued at USD 165.99 million in 2026 and is forecast to grow to USD 195.93 million by 2031.

Which resin type leads sales in Sri Lanka?

Acrylic formulations capture 38.52% share and are also growing the fastest at a 3.55% CAGR.

Why are water-borne coatings gaining ground?

Central Environmental Authority VOC limits and hospitality air-quality standards are accelerating the switch from traditional solvent-borne chemistry.

How big is the architectural segment?

Architectural and decorative lines account for 60.98% of 2025 revenues, benefiting from tourism-linked construction and home-improvement loans.

What are the main challenges for suppliers?

Currency volatility that inflates imported raw-material costs and skilled-applicator shortages due to outward labor migration remain key constraints.

Which company holds the largest individual niche?

JAT Holdings commands 57% of wood-coating revenues through its Italian technology alliances and applicator training programs.

Page last updated on: