Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

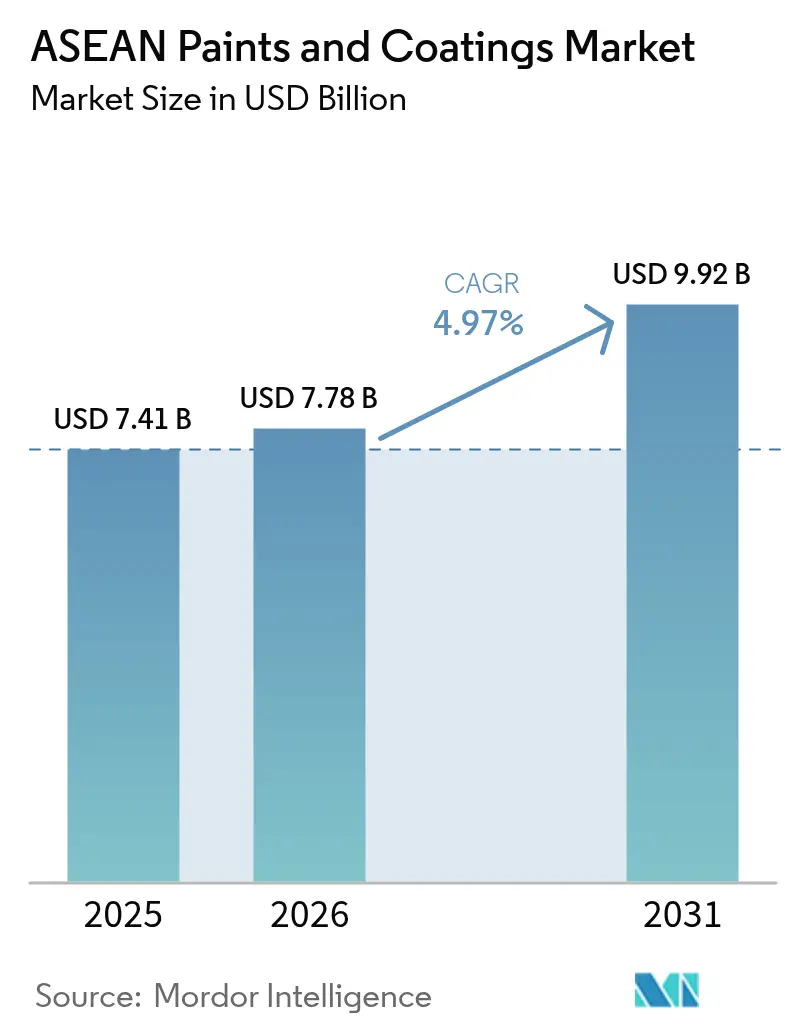

| Base Year Market Size (2025) | USD 7.41 Billion |

| Market Size (2026) | USD 7.78 Billion |

| Market Size (2031) | USD 9.92 Billion |

| Growth Rate (2026 - 2031) | 4.97% CAGR |

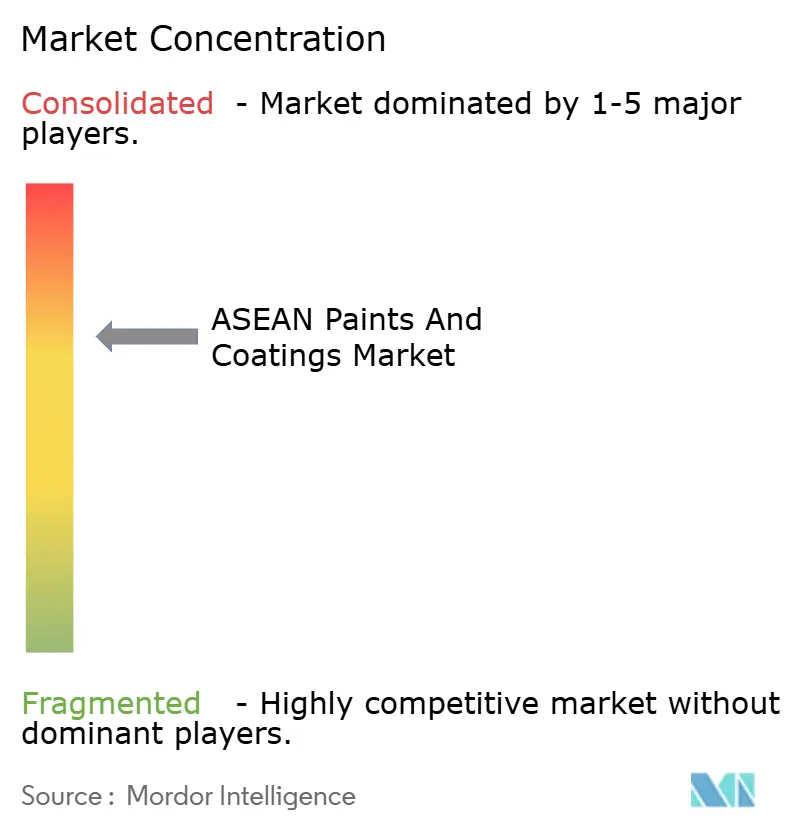

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Paints And Coatings Market Analysis by Mordor Intelligence

ASEAN Paints And Coatings Market size in 2026 is estimated at USD 7.78 billion, growing from 2025 value of USD 7.41 billion with 2031 projections showing USD 9.92 billion, growing at 4.97% CAGR over 2026-2031. Construction booms in Indonesia, Vietnam and Thailand, an ongoing wave of Chinese electric-vehicle investments, and government-backed infrastructure pipelines together underpin a multi-year uplift in architectural, protective and automotive volumes. Sustainability pressures are simultaneously nudging formulators toward water-borne, powder and radiation-cured chemistries that lower volatile-organic-compound (VOC) emissions without sacrificing performance. Competitive intensity is rising because domestic champions and multinational incumbents are racing to build plants closer to customers, localize resin supply and widen dealer footprints. Over the medium term, the ASEAN paints and coatings market will also capture incremental gains from accelerating free-trade agreements that shorten approval timelines for raw materials and finished goods.

Key Report Takeaways

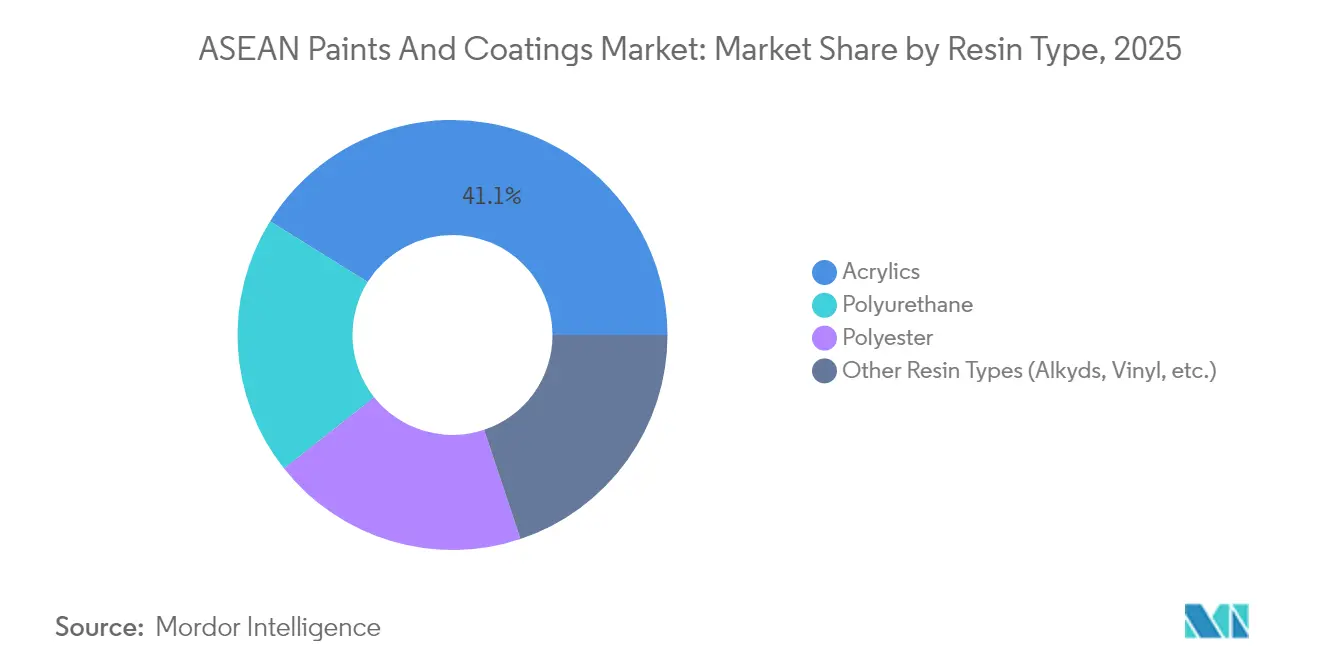

- By resin type, acrylics commanded 41.12% share of the ASEAN paints and coatings market size in 2025 and are set to grow at 6.83% CAGR between 2026-2031.

- By technology, solvent-borne systems led with 61.35% of ASEAN paints and coatings market share in 2025, while water-borne formulations are projected to expand at a 7.83% CAGR through 2031.

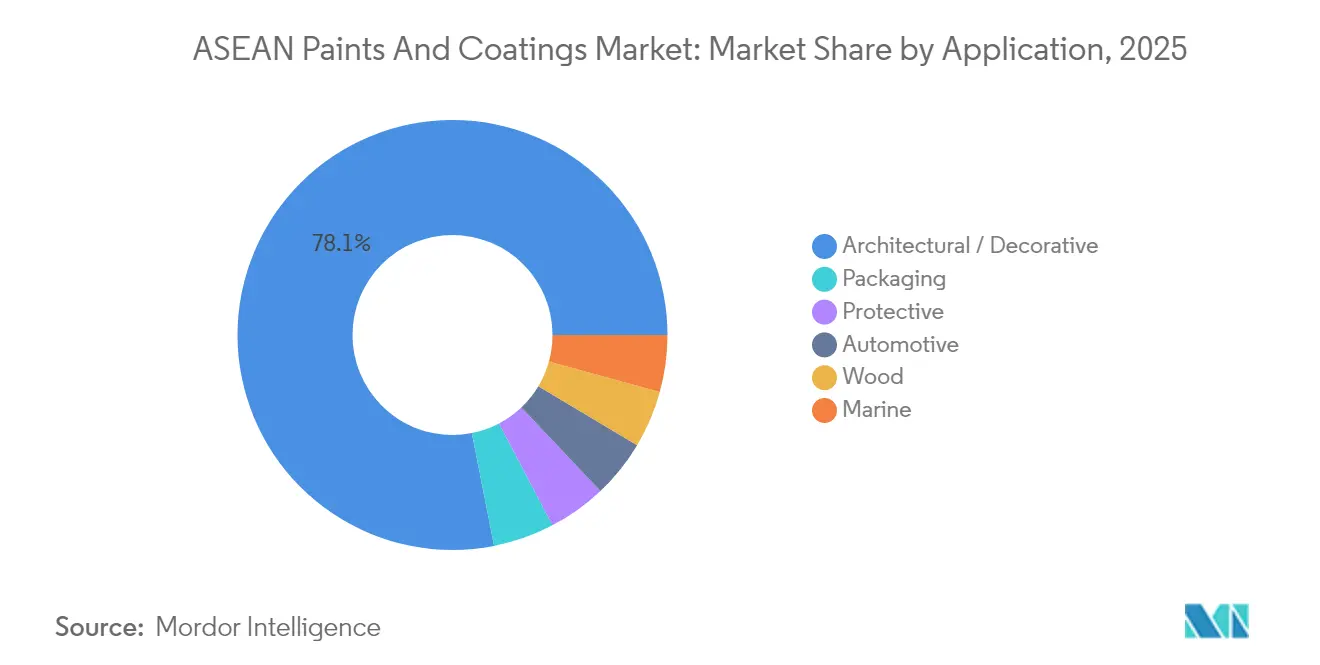

- By application, architectural coatings accounted for 78.10% of the ASEAN paints and coatings market size in 2025 and will advance at a 6.78% CAGR through 2031.

- By geography, Indonesia held 42.05% revenue share of the ASEAN paints and coatings market in 2025; Vietnam represents the fastest-growing country with a 6.66% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Paints And Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Urbanization and Infrastructure Development | +1.2% | Indonesia, Vietnam, Thailand core with spillover to Malaysia, Philippines | Medium term (2-4 years) |

| Expansion of the Automotive Sector | +0.8% | Thailand, Indonesia primary with Vietnam emerging | Long term (≥ 4 years) |

| Growing Foreign Investments in ASEAN Region | +0.6% | Global with concentration in Vietnam, Indonesia, Malaysia | Short term (≤ 2 years) |

| Expansion of Industrial Manufacturing Creating Demand | +0.4% | Indonesia, Thailand, Malaysia with Vietnam acceleration | Medium term (2-4 years) |

| Increasing Demand for Premium Aesthetics | +0.3% | Singapore, Malaysia urban centers with regional expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization and Infrastructure Development

Large-scale public-works programs are boosting the ASEAN paints and coatings market as governments deploy record budgets to roads, rail and affordable housing. Vietnam has earmarked USD 30 billion for multi-year transport corridors and energy assets expected to absorb high-build architectural and protective coatings[1]U.S. Department of Commerce, “Vietnam Country Commercial Guide 2025,” trade.gov . Thailand’s Eastern Economic Corridor continues to channel more than half of national construction outlays into megaprojects that require corrosion-resistant primers, traffic-marking paints and waterproof membranes. Indonesia’s Proyek Strategis Nasional portfolio likewise links maritime gateways and industrial estates, lifting demand for marine hull coatings and long-life epoxies that mitigate maintenance downtime. Parallel demographic shifts—urban migration and the rise of middle-income households—are enlarging the customer base for premium interior emulsions, textured finishes and moisture-barrier topcoats. The current project pipeline provides multi-cycle visibility, supporting stable procurement plans for resin suppliers through at least 2030.

Expansion of the Automotive Sector

The ASEAN paints and coatings market benefits from automakers’ shift toward regional electric-vehicle hubs. Chinese original-equipment manufacturers (OEMs) have allocated more than USD 1.4 billion to plants in Thailand and Indonesia that will assemble batteries, passenger cars and commercial vans. Thailand’s EV3.5 scheme alone targets annual output of up to 525,000 units by 2027, driving demand for cathodic-electrocoat primers, low-temperature powder topcoats and clearcoats that manage electromagnetic interference. Indonesia is charting a similar path, eyeing 2 million-unit capacity toward the mid-2030s. As production lines ramp, tier-one suppliers adopt UV-cured coatings that boost throughput while cutting energy bills, reinforcing the positive volume trajectory for automotive segments.

Growing Foreign Investments in ASEAN Region

Record foreign direct investment (FDI) of USD 230 billion in 2023 reaffirmed ASEAN’s status as the leading developing-region magnet for capital, and manufacturing projects dominate the pipeline[2]Association of Southeast Asian Nations, “Investment Report 2024,” asean.org. Multiple free-trade accords remove duties on resins and pigments, shortening lead times for new product launches across boundaries. Renewable-energy build-outs receive a disproportionate share of greenfield FDI, stimulating demand for weatherable polyurethanes on wind-turbine blades and high-temperature silicones on photovoltaic frames.

Expansion of Industrial Manufacturing Creating Demand

Specialty-chemical and petrochemical complexes under construction are another catalyst for the ASEAN paints and coatings market. SCG Chemicals invested USD 700 million to upgrade feedstock flexibility at its Long Son facility, enabling local supply of epoxies and acrylic monomers critical to high-performance coatings. Electronics assemblers in Malaysia and Thailand increasingly specify anti-corrosion fluoropolymers and heat-dissipation fillers in conformal coatings that protect circuit boards. Petrochemical tank farms and pipelines require high-build novolac epoxies and polyurea linings to withstand chemical immersion, and these assets typically mandate 20-year maintenance cycles that lock in recurring volumes. As ASEAN governments promote higher-value industrial clusters, the pull-through on performance coatings intensifies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Petro-Feedstock Prices | -0.7% | Global with acute impact on Indonesia, Thailand, Malaysia | Short term (≤ 2 years) |

| Chronic Skilled-Painter Shortage | -0.5% | Thailand, Malaysia, Singapore with spillover to urban Indonesia, Vietnam | Medium term (2-4 years) |

| Delayed Harmonisation of ASEAN Chemical Regulations | -0.4% | ASEAN-wide with concentrated impact on Philippines, Singapore, Vietnam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Petro-Feedstock Prices

Soft global demand and capacity surges in China have kept ethylene and propylene spreads under pressure, compressing margins for resin and solvent producers that supply the ASEAN paints and coatings market. Crude-linked monomers such as styrene, acrylates and glycols remain susceptible to geopolitical shocks, creating quarterly cost swings that smaller manufacturers struggle to absorb. European suppliers grappling with elevated gas prices have passed through mark-ups on imported additives, further squeezing formulators in Indonesia and Thailand. Steel and cement price volatility adds another layer of complexity because large architectural projects often bundle coating bids with structural materials. Although most market leaders hedge raw materials, sustained volatility reduces budget predictability for downstream construction contractors.

Chronic Skilled-Painter Shortage

Rapid building completions across megacities have outpaced the available pool of trained applicators, leading to labor shortages that delay handovers and, in turn, defer paint usage cycles. Contractors in Bangkok and Kuala Lumpur report daily wage inflation above consumer-price growth, forcing some developers to stagger phases or switch to lower-maintenance cladding materials. The skills gap also translates into quality problems—uneven film build, premature chalking and excessive wastage—that inflate total-cost-of-ownership for building owners. Multinationals now run on-site academies and digital-training platforms to raise workmanship standards, yet the pipeline will take years to normalize, capping the short-term upside for the ASEAN paints and coatings market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Versatility Sustains Leadership

Acrylic resins underpinned 41.12% of ASEAN paints and coatings market share in 2025, reflecting their compatibility with both water-borne and solvent-cut systems, excellent color retention and rapid-dry properties in tropical climates. They will grow the fastest, at 6.83% CAGR, as formulators exploit core-shell morphology and silicone-modified grades to raise dirt pick-up resistance. The ASEAN paints and coatings market size attributable to acrylic binders could approach USD 4.52 billion by 2031 on sustained residential repaint cycles. Polyurethanes hold a smaller but strategic niche in automotive topcoats and marine hull finishes where gloss retention and chemical resistance are paramount. Polyester resins remain workhorses for coil and roof coatings because of their cost-performance equilibrium, while alkyds cater to rural housing and anticorrosive primers where price outweighs lifespan.

Innovation pipelines are robust: researchers achieved 89.87% corrosion-inhibition efficiency in epoxy matrices modified with organic nanofillers, pushing epoxies into lighter gauge steel structures. Manufacturers are also tailoring acrylic emulsions with ambient-crosslinking aziridines that deliver polyurethane-like hardness without isocyanates. As petrochemical upstreams widen monomer supply, resin formulators gain pricing leverage that can be passed downstream, keeping acrylic platforms competitively priced against specialty polyurethanes.

By Technology: Environmental Momentum Propels Water-Borne Uptake

Solvent-borne chemistries retained a 61.35% share in 2025 and are deeply entrenched in marine, heavy-duty and wood-finishing lines where humidity tolerance and film-build speed remain decisive advantages. Nonetheless, the ASEAN paints and coatings market is witnessing a clear substitution trend as stricter VOC limits converge with buyers’ sustainability targets. Water-borne systems are accelerating at a 7.83% CAGR, buoyed by municipal procurement guidelines that now stipulate low-odor coatings for schools and clinics. The ASEAN paints and coatings market size for water-borne products is projected to add more than USD 890 million by 2031, helped by breakthroughs in self-crosslinking acrylics that deliver solvent-like hardness. Powder coatings have moved beyond appliances into aluminum extrusions for residential façades, supported by AkzoNobel’s USD 18 million Bac Ninh expansion that added five automatic lines calibrated for complex profiles.

The ASEAN paints and coatings market further benefits from emerging radiation-cured platforms whose instant cure speeds reduce factory footprints. Automotive battery enclosures now specify UV-cured primers that combine dielectric strength with thin-film uniformity. Meanwhile, niche players are commercializing bio-based diluents and reactive surfactants to improve water-borne corrosion resistance, narrowing the performance gap with conventional alkyds. Across the forecast horizon, a gradual re-balancing toward greener platforms is expected to trim solvent-borne’s share below 54%, though mission-critical industrial segments will ensure its residual dominance.

By Application: Architectural Paints Anchor Volume and Value Growth

The architectural segment dominated the ASEAN paints and coatings market with 78.10% share in 2025, a function of ongoing housing demand and public-sector capex across Indonesia, Vietnam and the Philippines. The segment is expected to clock a 6.78% CAGR up to 2031, supported by an estimated 35 million square meters of new floor area annually across the three largest economies. Protective-coating volumes will advance more slowly yet yield higher dollar margins as offshore platforms, refineries and LNG regasification units specify bespoke polyurethanes with 25-year design lives. Automotive coatings represent a smaller slice today, but the EV push coupled with Thailand’s export ambitions will scale this category rapidly.

Inside decorative paints, low-VOC and anti-bacterial interior finishes are gaining shelf space in urban retail outlets; Jotun’s flagship store roll-out in Manila demonstrates rising consumer pull for international brands. Wood-finishing systems leverage water-borne acrylic-alkyd hybrids for fast-dry furniture lines sold to e-commerce exporters. Marine anti-fouling paints are shifting to silicone-based foul-release films that lower vessel fuel burn. With multiple end-use vectors trending upward, the ASEAN paints and coatings market retains a balanced exposure to both high-volume mass markets and premium performance niches.

Geography Analysis

Indonesia anchors the ASEAN paints and coatings market with 42.05% share in 2025, leveraging real GDP growth of 5.05% in 2023 and a population exceeding 279 million. Domestic demand stood at 1.3 million tonnes against 1.6 million tonnes installed capacity, signifying room for throughput optimization and import substitution. Government megaprojects, from Jakarta’s MRT extensions to the Kalimantan new-capital build, underpin a recurring pipeline for protective primers and elastomeric roof coats. PT Nipsea forecasts decorative-segment turnover to rise 6% annually between 2024-2026, helped by expanded retail networks that bring economy, mid-tier and premium brands under one roof. Import tariffs on titanium dioxide and acrylic monomers were trimmed in 2024, marginally lowering finished-goods costs.

Vietnam is the growth frontrunner, set to grow the ASEAN paints and coatings market by 6.66% CAGR through 2031. Manufacturing rebounded to 8-9% output growth in 2024, and the government’s USD 30 billion infrastructure push includes metro lines in Hanoi and Ho Chi Minh City that necessitate graffiti-resistant topcoats. Long-Son petrochemicals started commercial supply of vinyl chloride monomer in late 2024, shortening lead times for local resin converters. Green-building guidelines now prevalent in major cities trigger mandatory use of low-VOC materials, pushing adoption of water-borne exterior emulsions. Free-trade agreements with the EU and UK remove duties on select pigments, allowing Vietnamese exporters to price competitively into high-spec furniture markets.

Thailand, Malaysia, the Philippines, Singapore and smaller ASEAN members make up the balance of market volume. Thailand’s 3-4% annual construction growth under the Eastern Economic Corridor ensures steady marine and industrial-maintenance demand, while its status as the 10th-largest global auto producer keeps automotive coating lines running near capacity. TOA Paint operates nine plants across the region and holds 48.7% domestic share, benefitting from early adoption of anti-fungal bathroom emulsions that suit tropical humidity. Malaysia’s Chemical Industry Roadmap 2030 endorses local sourcing of resins and pigments, aligning incentives for capacity additions. Singapore’s stringent chemical-control acts pressure formulators to eliminate long-chain perfluorocarbons, effectively accelerating technology migration that later diffuses into neighboring states. The Philippines enjoys a tourism-driven repaint cycle; Jotun’s decorative outlets target homeowners upgrading finishes after record remittance inflows.

Competitive Landscape

The ASEAN paints and coatings market exhibits moderate consolidation. Rising raw-material costs and tighter VOC regulations have compelled these leaders to invest in backward integration, automated tinting systems and omnichannel retail. Asian Paints’ Neo Bharat Latex allows the firm to penetrate price-sensitive rural communes without diluting premium urban marques.

Strategic deals have shaped the current hierarchy. Nippon Paint Holdings acquired specialty-formulator AOC in 2024, securing resin technologies for powder and UV lines, Asian Paints’ 24.3% stake in Egypt’s SCIB Chemicals hints at raw-material sourcing synergies, potentially feeding ASEAN alkyd lines. AkzoNobel’s Bac Ninh upgrade brings five new powder-coating lines and a water-borne cell, positioning it for eco-label bids across Vietnam’s electronics export clusters. TOA Paint leverages 700 dealers and 6,000 color-mixing machines to defend share against arriving Chinese and Korean challengers.

Technology leadership now determines sustainable competitive advantage. Multinationals deploy digital color-visualizer apps that shorten decision cycles for homeowners, while local brands focus on low-refill packaging sizes suited to micro-retail stores.

ASEAN Paints And Coatings Industry Leaders

Jotun

Akzo Nobel N.V.

TOA Paint (Thailand) Public Company Limited.

Nippon Paint Holdings Co., Ltd.

Avian Brands

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: PPG inaugurated a waterborne automotive coatings plant in Samut Prakan, Thailand. This new facility boosts PPG's capacity for producing waterborne basecoats and primers, addressing the growing demand for eco-friendly coatings from Southeast Asian automotive firms.

- March 2025: Asian Paints Ltd finalized the sale of its Indonesian operations, transferring ownership to the Singaporean arm of Australia's Omega Property Investments Pty Ltd, in a deal valued at SGD 6.8 million (approximately INR 44 crore).

ASEAN Paints And Coatings Market Report Scope

Paints and coatings are used not only for aesthetic applications but also to increase shelf life. They are used in various sectors, including construction and infrastructure, automotive, and other sectors. The market is segmented by technology, resin type, end-user industry, and geography. By technology, the market is segmented into solvent-borne coatings, water-borne coatings, and other technologies. By resin type, the market is segmented into acrylics, polyurethane, polyester, and other resin types. By end-user industry, the market is segmented into architectural/decorative, wood, protective, packaging, marine, and automotive. The report also covers the market size and forecasts for the ASEAN paints and coatings market across 6 countries in the ASEAN region. The report offers market size and forecast in revenue (in USD million) for all the above segments.

By Resin Type

| Acrylics |

| Polyurethane |

| Polyester |

| Other Resin Types (Alkyds, Vinyl, etc.) |

By Technology

| Solvent-borne Coatings |

| Water-borne Coatings |

| Other Technologies (Powder Coatings, Radiation Cured (UV, EB), etc.) |

By Application

| Architectural / Decorative |

| Protective |

| Wood |

| Automotive |

| Marine |

| Packaging |

By Geography

| Indonesia |

| Malaysia |

| Philippines |

| Singapore |

| Thailand |

| Vietnam |

| Rest of ASEAN Countries |

| By Resin Type | Acrylics |

| Polyurethane | |

| Polyester | |

| Other Resin Types (Alkyds, Vinyl, etc.) | |

| By Technology | Solvent-borne Coatings |

| Water-borne Coatings | |

| Other Technologies (Powder Coatings, Radiation Cured (UV, EB), etc.) | |

| By Application | Architectural / Decorative |

| Protective | |

| Wood | |

| Automotive | |

| Marine | |

| Packaging | |

| By Geography | Indonesia |

| Malaysia | |

| Philippines | |

| Singapore | |

| Thailand | |

| Vietnam | |

| Rest of ASEAN Countries |

Key Questions Answered in the Report

What is the current ASEAN Paints and Coatings Market size?

The market is valued at USD 7.78 billion in 2026 and is projected to reach USD 9.92 billion by 2031.

Which country leads regional demand?

Water-borne coatings are advancing at a 7.83% CAGR because of tightening VOC regulations and consumer preference for low-odor finishes.

Why are acrylic resins so dominant?

Acrylics combine weatherability, color retention and compatibility with low-VOC formulations, making them versatile across architectural, automotive and industrial lines.

Which country leads regional demand?

Indonesia accounts for major revenue share(42.05%), supported by large public-infrastructure budgets and a growing middle class.

Page last updated on: