UV-Curable Adhesives Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

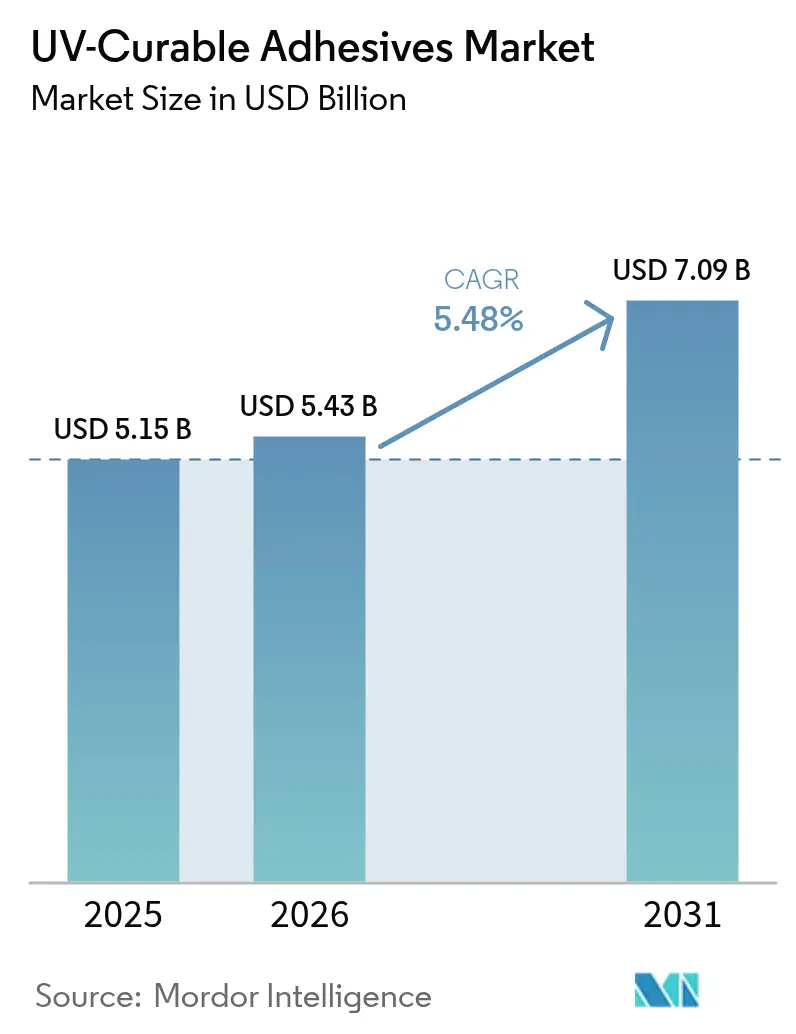

| Market Size (2026) | USD 5.43 Billion |

| Market Size (2031) | USD 7.09 Billion |

| Growth Rate (2026 - 2031) | 5.48% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UV-Curable Adhesives Market Analysis by Mordor Intelligence

The UV-Curable Adhesives Market size is expected to grow from USD 5.15 billion in 2025 to USD 5.43 billion in 2026 and is forecast to reach USD 7.09 billion by 2031 at 5.48% CAGR over 2026-2031. Expanding regulatory pressure for solvent-free chemistries, rapid miniaturization in consumer electronics, and the medical sector’s pivot toward biocompatible instant-cure bonding solutions jointly sustain demand. Automotive lightweighting programs are substituting mechanical fasteners with UV-curable structural adhesives to cut assembly time, and packaging converters are installing in-line digital presses that rely on adhesives curing in under 200 milliseconds to support just-in-time workflows. Hybrid formulations combining UV and moisture cure are gaining attention because they bond shadow-tolerant assemblies without secondary ovens. Supply-chain resilience remains a focus after photoinitiator price spikes in 2025, prompting leading producers to expand captive capacity and diversify raw-material sourcing.

Key Report Takeaways

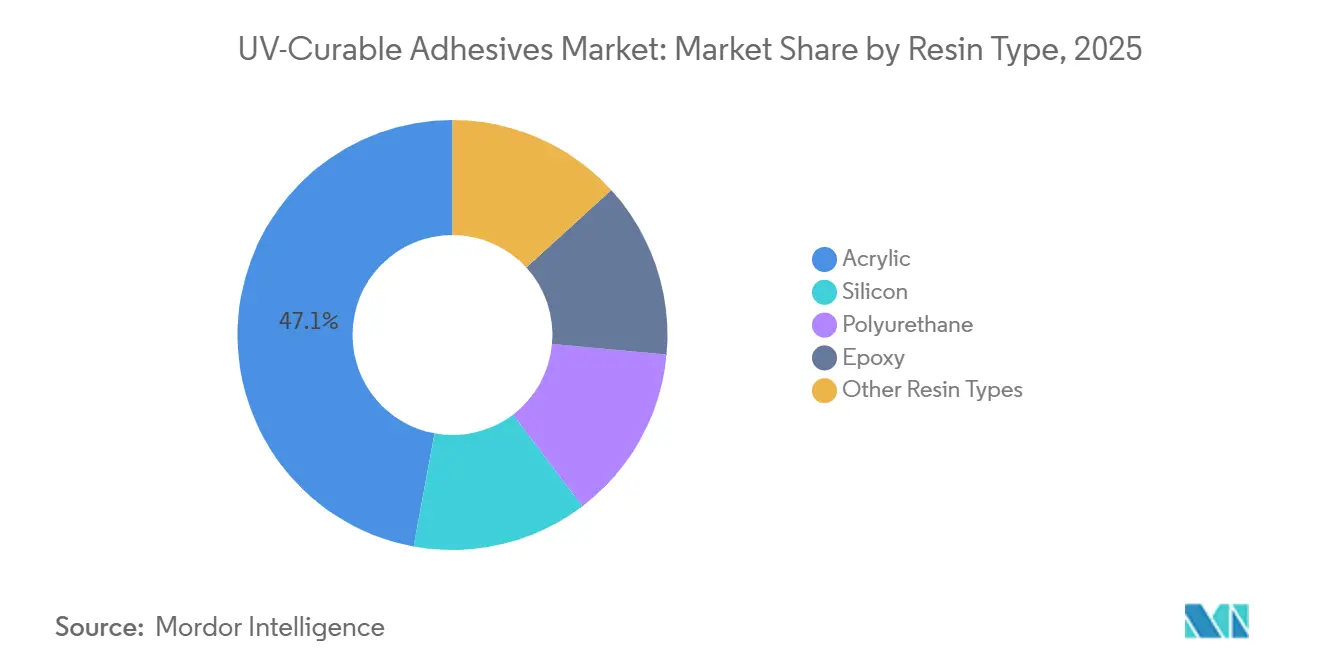

- By resin type, acrylic led with 47.12% of the UV-curable adhesives market share in 2025, while epoxy is projected to advance at a 5.61% CAGR through 2031.

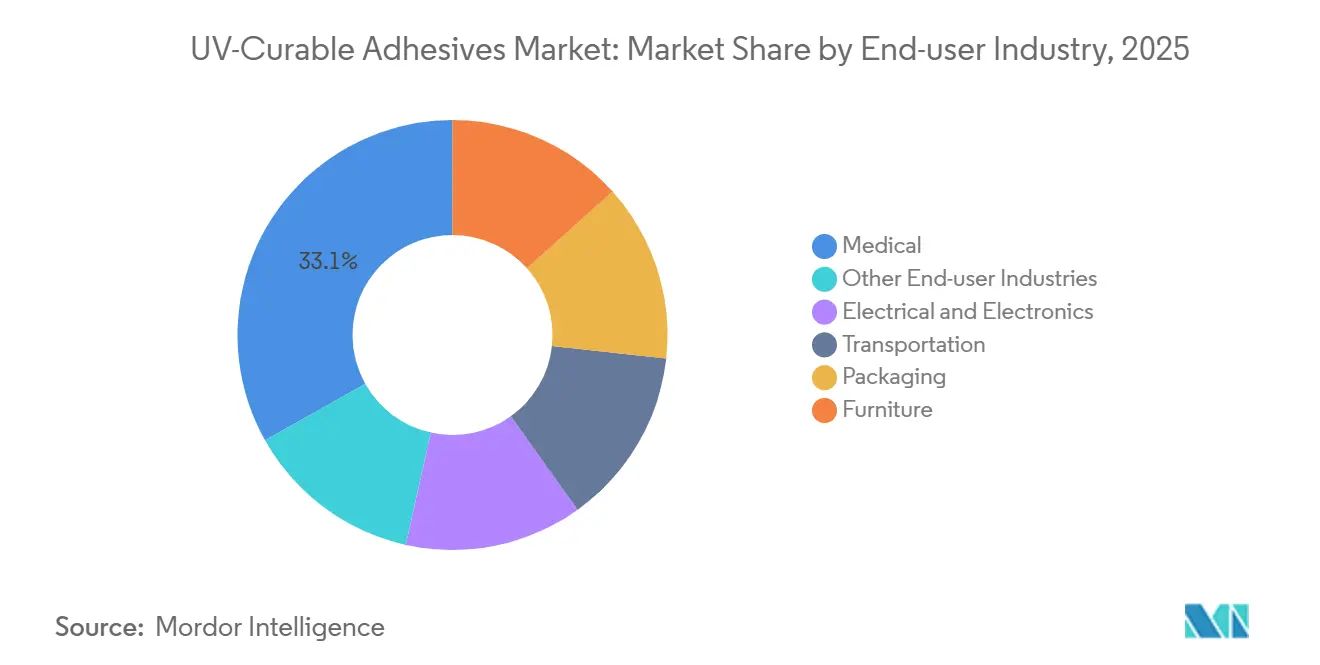

- By end-user industry, medical held 33.14% of the UV-curable adhesives market share in 2025 and is expected to grow at a 6.68% CAGR to 2031.

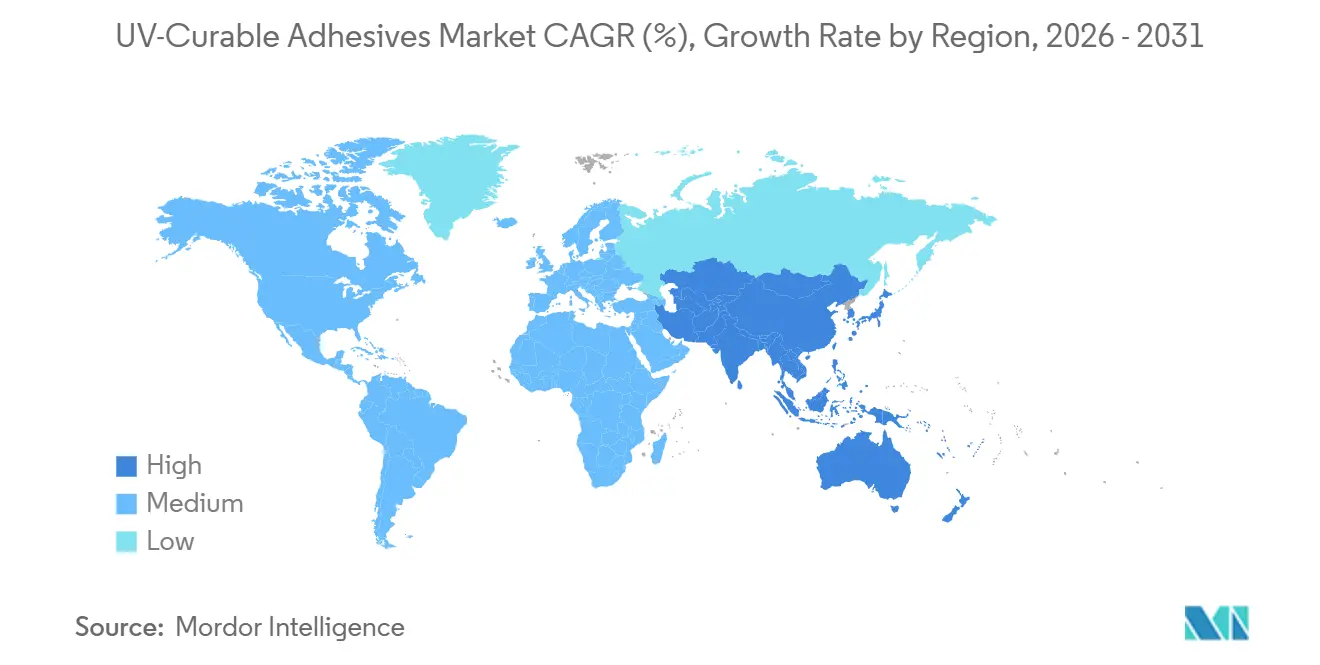

- By geography, North America accounted for 42.88% of the UV-curable adhesives market share in 2025, whereas Asia-Pacific is forecast to post a 5.69% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global UV-Curable Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| UV-curable adhesives adoption in automotive and aerospace | +1.2% | Global, with concentration in Germany, United States, Japan | Medium term (2-4 years) |

| Stricter VOC/REACH regulations favor solvent-free chemistries | +1.5% | North America and Europe, spillover to APAC export hubs | Short term (≤ 2 years) |

| Miniaturization in consumer electronics | +0.9% | APAC core (China, South Korea, Vietnam), secondary in North America | Medium term (2-4 years) |

| Rapid uptake in wearable medical devices | +1.3% | North America and Europe, early adoption in urban India and China | Long term (≥ 4 years) |

| In-line digital packaging print lines demanding instant bonding | +0.6% | Global, with early gains in Germany, United States, India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

UV-Curable Adhesives Adoption in Automotive and Aerospace

Original-equipment manufacturers are swapping two-part epoxies for UV-curable adhesives when bonding ADAS camera modules, panoramic-roof glass, and electric-vehicle battery-pack components, lowering fixture time from 30 minutes to under 60 seconds. DELO’s LED-curable resin for stator potting, introduced May 2025, boosted line throughput by 30% while withstanding 150°C continuous operation. The IEC 62899-1 guideline, published in 2024, standardized validation protocols, reducing qualification effort for Tier-1 suppliers by six months.

Stricter VOC/REACH Regulations Favor Solvent-Free Chemistries

The European Chemicals Agency added three glycol ethers to the REACH Candidate List in March 2025, accelerating the shift to UV-curable acrylic adhesives containing zero VOCs. California’s South Coast Air Quality Management District cut VOC limits for industrial adhesives to 50 g/L effective January 2026, compelling converters to retool production lines[1]“Rule 1168 – Adhesives and Sealants,” South Coast AQMD, aqmd.gov . China’s GB 38507-2024 lowered plant-level VOC emissions to 80 mg/m³, stimulating UV technology investment in Guangdong. The U.S. EPA’s October 2025 draft revision of hazardous-air-pollutant standards is projected to displace 15% of solvent-based adhesive volume by 2029.

Miniaturization in Consumer Electronics

Smartphone assemblers now cure UV-acrylic adhesives in under 5 seconds to bond 0.3 mm glass covers, raising automated throughput to 120 units per hour. Apple employed a UV-silicone grade for Series 9 Watch biometric-sensor bonding, ensuring electrical stability over 10,000 flex cycles. Hydrophobic UV epoxies that pass IPX7 testing, such as Master Bond UV15-7HP, prevent sweat ingress in true-wireless earbuds. Semiconductor packaging houses are piloting die-attach UV epoxies with sub-10 µm bond lines to manage heat in advanced packages.

Rapid Uptake in Wearable Medical Devices

The U.S. FDA cleared 47 wearable devices in 2025, all relying on UV-curable biocompatible adhesives meeting ISO 10993-5 and -10 standards. Abbott’s FreeStyle Libre 3 glucose monitor uses a UV-acrylic bond line stable for 14 days of continuous wear. Europe’s Pharmacopoeia 11.0 capped residual monomer content at 0.1%, intensifying demand for ultra-low-extractable UV grades. H.B. Fuller’s purchase of Medifill in December 2024 positioned the company to target 20% share of the wearable-patch segment by 2027. ISO 20417 simplifies documentation, trimming four months from Class II device approvals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of UV-LED curing systems | -0.8% | Global, acute in price-sensitive APAC and South America | Short term (≤ 2 years) |

| Availability of alternative 2-part epoxies and cyanoacrylates | -0.5% | Global, particularly in industrial maintenance and repair | Medium term (2-4 years) |

| Supply volatility of key photoinitiators | -0.4% | Global, with bottlenecks in China and India monomer plants | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of UV-LED Curing Systems

Industrial UV-LED conveyors cost USD 50,000 to USD 300,000, deterring small converters. A 2024 Adhesive & Sealant Council survey showed 38% of North American packagers citing capital cost as their chief barrier. Indian label printers absorb 28% customs duty plus 18% GST on imported systems, inflating price by 52%[2]“Import Tariff Schedule,” Ministry of Commerce & Industry, commerce.gov.in . Subscription models from Phoseon trimmed upfront cost by 60% for 40 European early adopters. Lawrence Berkeley National Laboratory documented 70% electricity savings relative to mercury-arc technology, offsetting USD 15,000-25,000 annual operating expenses.

Availability of Alternative 2-Part Epoxies and Cyanoacrylates

Two-part epoxies still dominate structural repairs where gap-filling and shear strength exceed 25 MPa, especially in aerospace composite work. Cyanoacrylates cure instantly without light, making them preferable for opaque substrates; Henkel’s Loctite 401 alone generated USD 180 million revenue in 2024. Medical syringe assemblers prefer cyanoacrylates for stainless-steel cannula bonding. Hybrid solutions blur categories: 3M Scotch-Weld EC-3524, introduced in September 2024, enables optional UV acceleration, giving manufacturers process flexibility. UV-curable grades remain 30-50% more expensive per kilogram than commodity epoxies, impeding uptake in furniture and footwear assembly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Leads, Epoxy Accelerates

Acrylic accounted for 47.12% of UV-curable adhesives market share in 2025 and delivered the cost-to-performance blend favored for pressure-sensitive labels and medical assemblies. Epoxy is forecast to post a 5.61% CAGR through 2031, powered by automotive and aerospace needs for tensile strengths above 25 MPa and glass-transition temperatures over 120 °C. The UV-curable adhesives market size for epoxy products is projected to expand steadily alongside rising electric-vehicle battery-pack adoption. Silicone UV grades serve high-temperature electronics and LED packaging as demonstrated by Dow Corning OE-6630 qualifying for engine-compartment sensors. Polyurethane UV adhesives attract flexible-circuit and textile users because elongation surpasses 300%, absorbing substrate movement without delamination.

Acrylic supply chains benefit from commodity monomer pricing near USD 2.20 /kg, whereas cycloaliphatic epoxy resins exceed USD 6.50 /kg, supporting acrylic cost leadership. Hybrid UV-plus-moisture epoxies such as SikaFlex-525 UV reach 80% of ultimate strength after 10 seconds of irradiation, finishing cure in shaded areas through moisture crosslinking. Polyurethane formulations face higher raw material costs after the EU restricted aromatic di-isocyanates in consumer products in 2024. Silicone UV adhesives command a triple price premium but remain indispensable where 200 °C thermal endurance is non-negotiable.

By End-user Industry: Medical Devices Outpace All Segments

Medical held 33.14% of the UV-curable adhesives market share in 2025 and is advancing at a 6.68% CAGR to 2031, spurred by continuous glucose monitors, cardiac patches, and minimally invasive surgical tools. Electrical and electronics manufacturers, such as those involved in smartphone, tablet, and wearable assembly lines, require instant-cure, low-outgassing adhesives for bonding applications. Transportation demand grows from electric-vehicle battery packs and head-up displays, while packaging converters pivot to UV-curable laminations that eliminate solvent-recovery infrastructure.

Stringent ISO 10993 biocompatibility testing drives elevated specification requirements in the medical sector; adhesives must show leachable monomers below 0.1% and pass cytotoxicity and sensitization assays. Electronics producers specify defogging-resistant UV grades for camera modules, such as Dymax 9014-F, which recorded total mass loss under 0.5% during ASTM E 595 testing. Furniture plants explore UV-cure edge-banding to lower cycle time from 45 seconds to under 5 seconds while dropping VOC emissions to meet SCAQMD standards. Packaging adoption accelerates as European Regulation 10/2011 constrains overall migration to 10 mg/dm², a threshold readily achieved by low-migration UV acrylics.

Geography Analysis

North America led the UV-curable adhesives market in 2025 with 42.88% revenue owing to dense medical-device clusters in Massachusetts, California, and Minnesota, where 60% of FDA-cleared wearables are designed. Automotive OEMs such as General Motors and Ford integrated UV-curable bonding on ADAS cameras and panoramic roofs, trimming assembly time by 40%. California’s 50 g/L VOC limit, effective 2026, further accelerates migration from solvent-based grades. Health Canada’s March 2024 endorsement of ISO 10993 strengthened demand for biocompatible UV-curable bonds in insulin pumps and diagnostic cartridges.

Asia-Pacific is projected to grow at a 5.69% CAGR over 2026-2031, propelled by vast smartphone and display manufacturing in China’s Yangtze River Delta, South Korea’s semiconductor hubs, and Vietnam’s assembly corridors. China’s GB 38507-2024 VOC cap is moving converters toward UV systems, while India’s two-wheeler OEMs adopt UV adhesives to satisfy Bharat Stage VI rules on manufacturing emissions. Japan’s Olympus and Terumo cut endoscope and catheter assembly time by 30% after switching to UV bonding in 2024. South Korean panel manufacturers utilized UV-curable adhesives in response to the increasing demand for foldable OLEDs.

Europe’s demand is led by Germany, France, and the United Kingdom. Germany’s EV battery-pack lines now specify UV-curable adhesives to save 35% energy on cure cycle. France’s pharma sector adopted UV bonds in prefilled syringes and transdermal patches to meet European Pharmacopoeia residual-monomer limits. The U.K. enforces EU migration rules post-Brexit, prompting flexible-pack converters to replace solvent-borne laminating adhesives with UV grades. South America and Middle-East and Africa remain early-stage markets constrained by UV-LED equipment costs, although Brazil’s automakers and the UAE’s medical-device free zones are piloting niche uses.

Competitive Landscape

The UV-curable adhesives market exhibits consolidation. The top five suppliers, Henkel, 3M, H.B. Fuller, Dymax, and Arkema, held 60-70% combined revenue in 2025. Competitive levers revolve around cure speed, depth, and substrate versatility. Henkel filed a 2024 patent for photoinitiator-free thiol-ene UV acrylics that could disrupt food-contact adhesives by eliminating migration risk. Arkema will add 30% photoinitiator capacity at Nansha by 2026 to secure inputs for its Sartomer resins and raise margin by roughly 200 basis points. Dymax, DELO, and Master Bond specialize in high-value niches such as ADAS camera modules and moisture-resistant wearables, commanding double-digit price premiums.

Technology convergence is evident as 3M’s hybrid two-part epoxy can optionally receive UV acceleration, offering single-line flexibility for opaque and transparent sections. Panacol’s Vitralit UC 6694, certified to ISO 10993-5 in August 2024, targets implantable devices, while DELO focuses on EV stator potting requiring 1 W/m·K thermal conductivity alongside 30% faster throughput. Sustainability is an emerging differentiator: start-ups are piloting lignin-based photoinitiators to cut petrochemical reliance, though commercial scale remains years away.

Regulatory compliance forms a pricing moat. Suppliers holding ISO 10993 certification and FDA Drug Master Files can price 25-40% above commodity levels because customer revalidation is costly. As UV-LED lamp penetration climbs and VOC limits tighten globally, competitive intensity is expected to rise, especially among mid-tier Asian formulators competing on application engineering rather than cost.

UV-Curable Adhesives Industry Leaders

3M

Dymax

H.B. Fuller Company

Henkel AG & Co. KGaA

Arkema

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Permabond Engineering Adhesives Ltd launched Permabond UV6357. This UV-curable adhesive was specifically engineered to withstand extreme cold and maintain durable, flexible bonds in refrigeration environments subject to significant thermal cycling.

- June 2025: Toyochem Co., Ltd., a subsidiary of artience Co., Ltd., introduced the TOYOMELT P-201 series, a solvent-free, UV-curable hot melt adhesive designed for high-performance automotive and electronic applications. This adhesive provided heat resistance exceeding 100°C, bridging the gap between traditional hot melts and specialty adhesives, while maintaining flexibility on materials such as metal, glass, and plastics (PE/PP).

Global UV-Curable Adhesives Market Report Scope

UV-curable adhesives can be cured without heating upon exposure to UV light or other radiation sources and then bonded to the required substrate. These adhesives offer beneficial properties such as superior thermal stability, optical clarity, and resistance to moisture, solvents, and chemicals.

The UV-curable adhesives market is segmented by resin type, end-user industry, and geography. By resin type, the market is segmented into acrylic, silicon, polyurethane, epoxy, and other resin types. By end-user industry, the market is segmented into medical, electrical and electronics, transportation, packaging, furniture, and other end-user industries. The report also covers the market sizes and forecasts for the UV-curable adhesives in 27 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Acrylic |

| Silicon |

| Polyurethane |

| Epoxy |

| Other Resin Types |

| Medical |

| Electrical and Electronics |

| Transportation |

| Packaging |

| Furniture |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Malaysia | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Turkey | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| Nigeria | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Resin Type | Acrylic | |

| Silicon | ||

| Polyurethane | ||

| Epoxy | ||

| Other Resin Types | ||

| By End-user Industry | Medical | |

| Electrical and Electronics | ||

| Transportation | ||

| Packaging | ||

| Furniture | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Malaysia | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Turkey | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the UV-curable adhesives market?

The UV-curable adhesives market stands at USD 5.43 billion in 2026 and is expected to reach USD 7.09 billion by 2031, registering a 5.48% CAGR from 2026 to 2031.

Which resin type dominates global demand in 2025?

Acrylic led with 47.12% demand in 2025 because it combines optical clarity and versatile adhesion.

Why is medical the fastest-growing end-user industry through 2031?

Rising FDA approvals for wearable sensors and stricter ISO 10993 limits on residual monomers are pushing medical adoption at a 6.68% CAGR through 2031.

What geographical region shows the strongest growth through 2031?

Asia-Pacific is forecast to expand at a 5.69% CAGR through 2031, propelled by electronics and automotive manufacturing in China, South Korea, and India.

Page last updated on: