Temperature Modulation Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

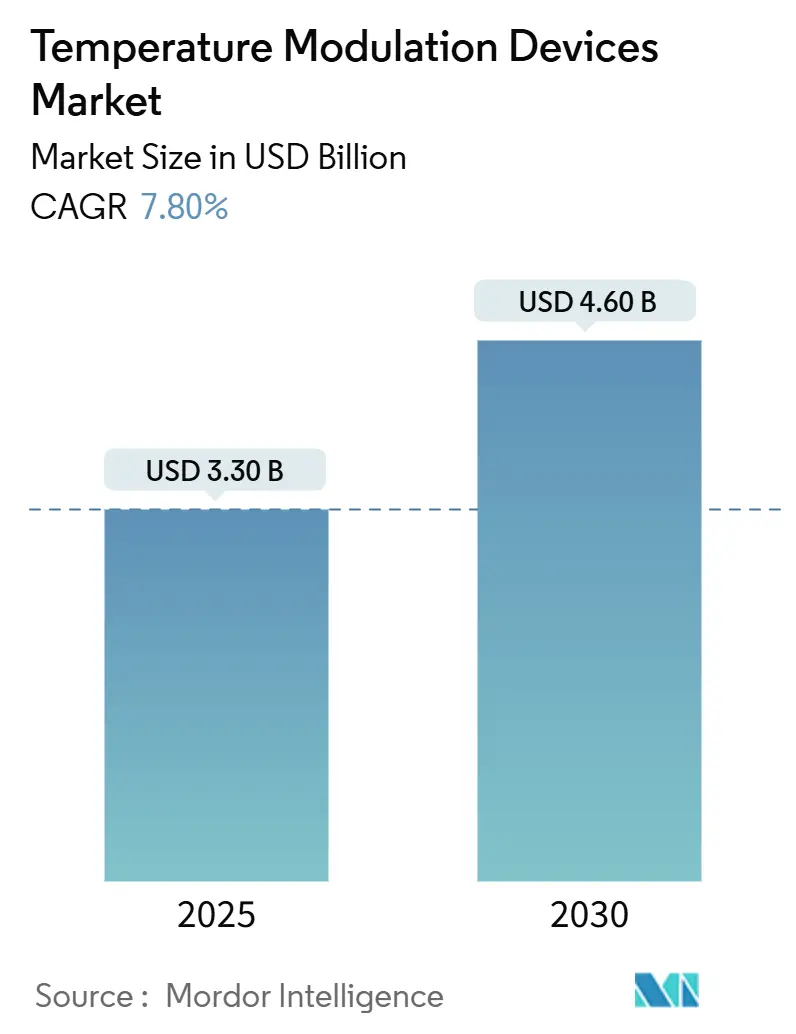

| Market Size (2025) | USD 3.30 Billion |

| Market Size (2030) | USD 4.60 Billion |

| Growth Rate (2025 - 2030) | 7.80% CAGR |

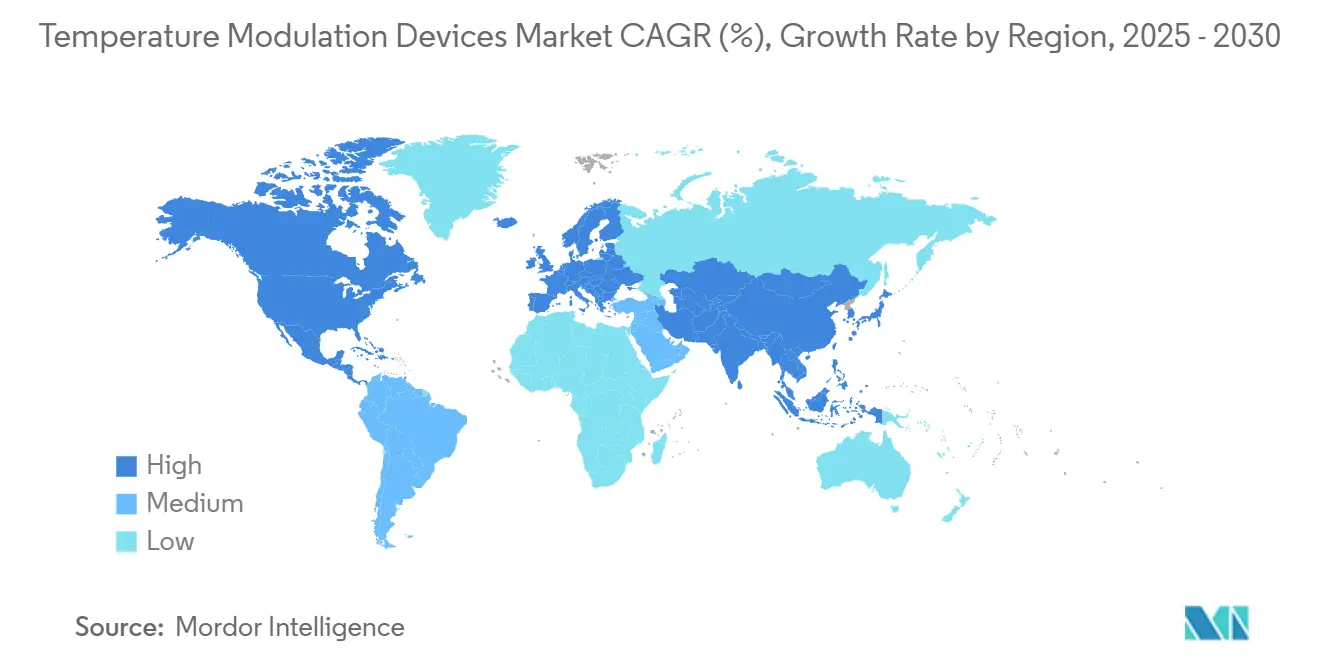

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Temperature Modulation Devices Market Analysis by Mordor Intelligence

The temperature modulation devices market size stood at USD 3.30 billion in 2025 and is forecast to reach USD 4.60 billion by 2030, translating into a 7.8% CAGR through the period. This expansion reflects the shift from basic warming tools toward closed-loop platforms that use real-time analytics to maintain normothermia during complex surgical, critical-care and emergency procedures. Rising surgical caseloads in aging high-income populations, rapid uptake of targeted temperature management after cardiac arrest and a steady flow of artificial intelligence upgrades all bolster demand for precision devices. Leading vendors are layering machine-learning algorithms onto established warming and cooling systems to cut nursing workload, while defense agencies are fast-tracking portable IV warmers that keep blood products viable in extreme settings. Collectively, these forces anchor a resilient growth trajectory for the temperature modulation devices market.

Key Report Takeaways

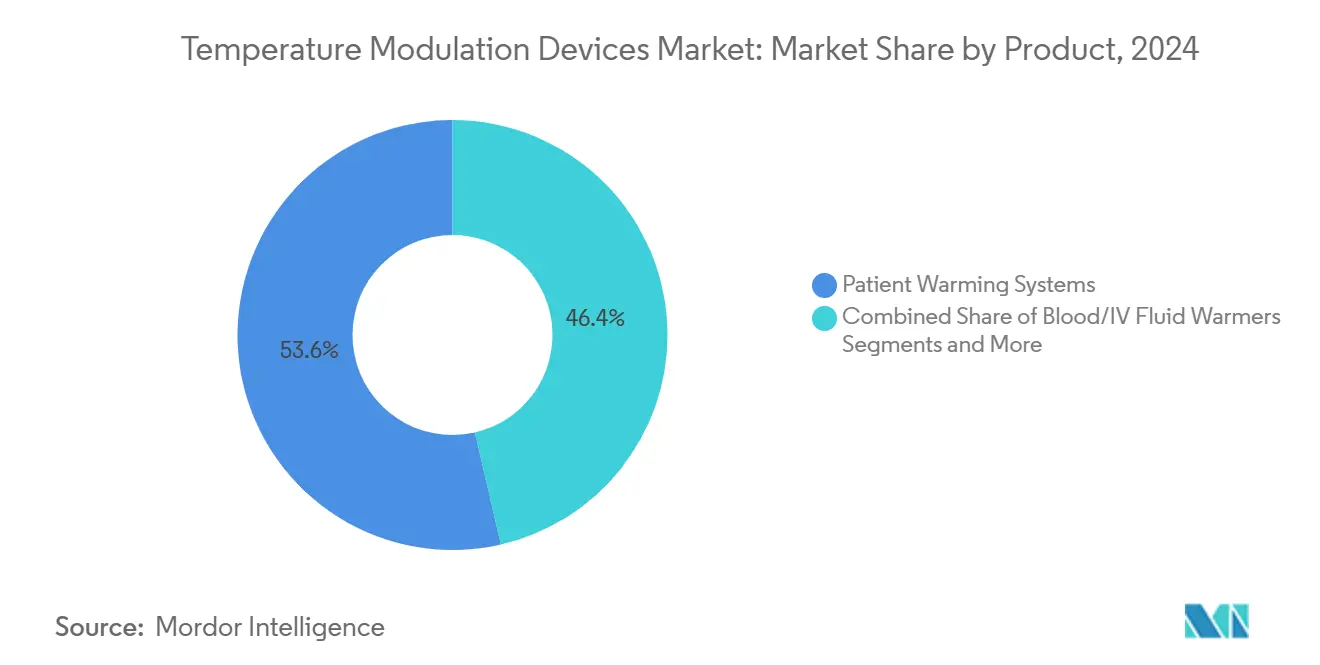

- By product, patient warming systems captured 53.6% of temperature modulation devices market share in 2024. Intravascular temperature-management systems are projected to post the fastest 12.1% CAGR through 2030.

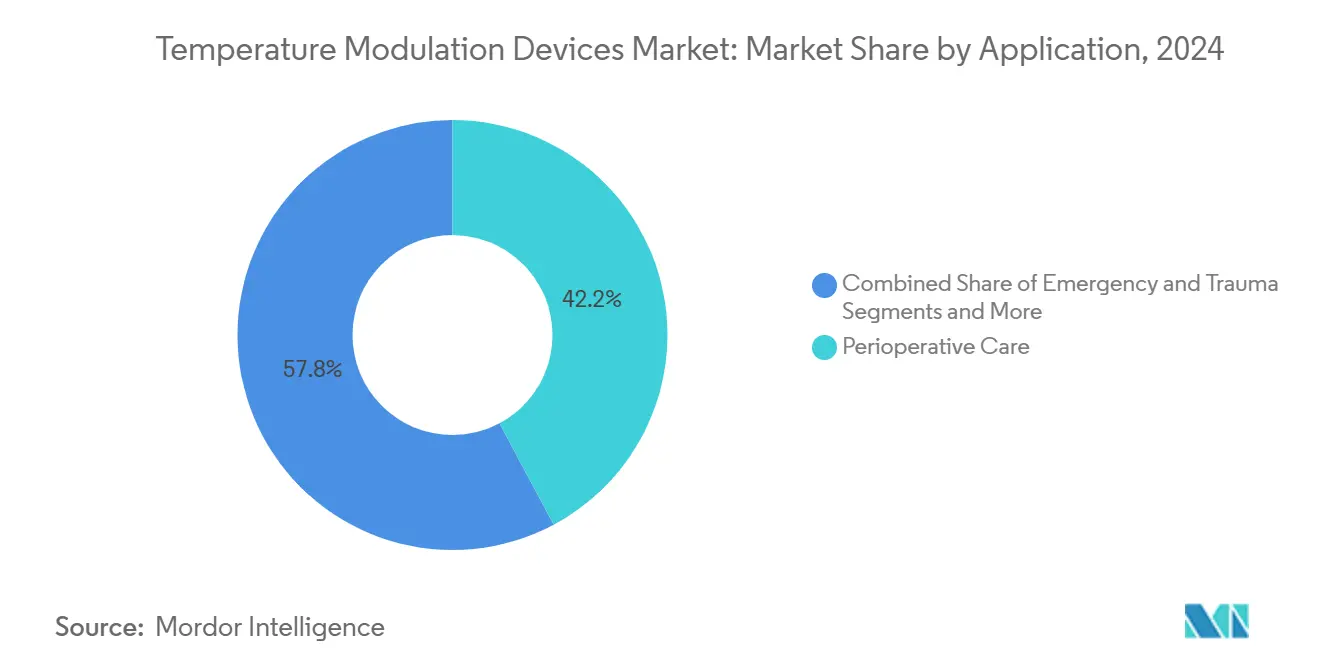

- By application, perioperative care held 42.2% of the temperature modulation devices market size in 2024. Emergency and trauma care is advancing at the highest 11.2% CAGR to 2030.

- By geography, North America led with a 40.6% temperature modulation devices market share in 2024; Asia Pacific is set to clock a 7.4% CAGR through 2030.

Global Temperature Modulation Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying surgical volumes in high-income countries | +1.80% | North America & Europe | Medium term (2-4 years) |

| Growing adoption of targeted temperature management post-cardiac arrest | +1.50% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Military demand for lightweight, battery-powered IV/blood warmers | +0.40% | North America, Europe, select APAC | Long term (≥ 4 years) |

| Rapid expansion of ambulatory surgery centers in APAC | +1.20% | Asia Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Esophageal heat-exchange devices gaining reimbursement in EU | +0.60% | Europe, expanding to North America | Medium term (2-4 years) |

| AI-driven closed-loop temperature-regulation platforms | +0.90% | Global, led by North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Surgical Volumes Drive Advanced Temperature Management Adoption

High-income health systems face surging orthopedic and cardiovascular caseloads that heighten hypothermia risk. Hospitals are therefore layering preoperative warming, intraoperative active warming, and postoperative temperature surveillance into one integrated workflow. These multimodal bundles have proven to cut infection rates, shorten recovery, and improve reimbursement metrics, driving continued investments in enterprise-level temperature platforms.[1]Yi Shang, “Strategies for Perioperative Hypothermia Management: Advances in Warming Techniques and Clinical Implications,” BMCSurg.biomedcentral.com

Military Applications Accelerate Portable Temperature Management Innovation

Defense agencies now specify sub-2-pound warmers capable of heating blood to 37 °C within minutes under battlefield conditions. Devices cleared for combat use are migrating into civilian trauma networks and air-ambulance fleets, where portability and battery life are critical. Prototype drone-deliverable refrigeration pods trialed in 2024 hint at future pre-hospital blood logistics that will lean heavily on rugged temperature-control modules.

Ambulatory Surgery Center Expansion Transforms APAC Temperature Management Landscape

Asia Pacific ambulatory surgery centers expect a 25% procedure jump this decade. Operators favor dual-mode systems that both warm and cool while fitting tight floor plans. Automated set-and-forget interfaces help offset nurse shortages and ensure guideline-compatible temperature profiles across ophthalmology, gastroenterology,y and day-orthopedic suites.[2]Sahely Mukerji, “Sg2 Annual Report Forecasts Growth in ASC Volume,” ASCfocus.org

AI-Driven Closed-Loop Systems Revolutionize Temperature Precision

Machine-learning algorithms are pushing precision from ±1 °C to ±0.2 °C by continuously recalibrating energy delivery in response to tissue feedback. Early deployments show energy savings and fewer manual interventions, signaling a step-change in perioperative safety benchmarks.[3]Sean Coeckelenbergh et al., “Closed-Loop Anesthesia Foundations and Applications,” Springer.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of intravascular cooling systems | -1.10% | Global, hitting emerging markets hardest | Short term (≤ 2 years) |

| Infection-control concerns around reusable blankets & hoses | -0.80% | Global, with scrutiny in North America & Europe | Medium term (2-4 years) |

| Litigation risk linked to forced-air warming in orthopedics | -0.60% | North America, expanding to Europe | Long term (≥ 4 years) |

| Limited skilled staff for neuro-protection protocols in LMICs | -0.70% | Sub-Saharan Africa & South Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Costs Constrain Intravascular Cooling System Adoption

Acquisition outlays often exceed USD 50,000 per console, deterring hospitals that cannot justify the premium over surface options priced at USD 5,000–15,000. Added training and consumable costs widen the gap, particularly in budget-tight public facilities, despite superior neurologic outcomes documented in peer-reviewed trials.

Infection-Control Concerns Challenge Reusable Temperature Management Components

Sterile-field breaches alleged in forced-air lawsuits have prompted some orthopedic centers to transition toward single-use or closed-loop alternatives. Reinforced cleaning protocols reduce risk but raise labor and compliance costs, nudging procurement toward disposable circuits where price points allow.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Intravascular Systems Challenge Traditional Warming Dominance

Patient warming systems retained 53.6% temperature modulation devices market share in 2024 on the back of universal perioperative protocols. The temperature modulation devices market size attributable to intravascular platforms is on track for a 12.1% CAGR to 2030, as neurologists and intensivists favor precise core cooling for post-cardiac-arrest care. Cooling blankets and conductive pads fill a well-established niche, yet hospitals looking for one-console versatility are trialing integrated dual-mode platforms that switch from warming to cooling with minimal disposables. FDA de novo clearance of the esophageal cooling device in 2024 unlocked a throat-based conduit that shields the esophagus during cardiac ablation and delivers rapid systemic cooling, pointing to a fertile innovation runway.

Greater algorithmic automation also differentiates next-generation consoles. Vendors integrate closed-loop controls that auto-adjust flow rates and alarm thresholds to the patient’s metabolic trajectory, shrinking clinician workload. Defense contracts for battery-optimized IV warmers add incremental unit demand and accelerate ruggedization R&D that later feeds civilian designs. As feature breadth expands, procurement teams compare platforms on disposables cost per case and interoperable data outputs more than on sticker price alone.

By Application: Emergency Care Accelerates While Perioperative Remains Dominant

Perioperative workflows commanded 42.2% of the temperature modulation devices market size in 2024 because every major surgical guideline now mandates active warming. Infection avoidance, shorter anesthesia emergence and reimbursement penalties for unplanned hypothermia reinforce perioperative leadership. Emergency & trauma segments, however, will deliver the fastest 11.2% CAGR as resuscitation bundles formalize normothermia targets after return of spontaneous circulation.

Growth in critical-care units remains steady as hospitals upgrade to networked consoles that feed data into electronic records for audit of neuro-protection protocols. Neonatal wards in low-resource countries continue to struggle with hypothermia: a 2024 Nigerian study recorded a 72.9% incidence among preterm admissions, underscoring an unmet need for low-cost incubators and wearable warmers. Telehealth pilots pairing wireless axillary patches with cloud dashboards hint at future home-based temperature surveillance for at-risk infants and post-operative patients alike.

Geography Analysis

North America accounted for 40.6% temperature modulation devices market share in 2024, supported by robust reimbursement and clear FDA pathways that de-risk innovation. Medicare pass-through codes covering advanced cooling catheters boost early adoption, while hospital consortia negotiate bulk disposables contracts that lower per-procedure costs. The region’s civilian ecosystems also benefit from dual-use technologies spun off U.S. military R&D, accelerating portable-device diffusion.

Europe follows with a mature yet evolving landscape shaped by the Medical Devices Regulation. Reimbursement approvals for esophageal heat-exchange systems in Germany and France underscore payer willingness to support evidence-backed niche devices. Vendors must now furnish stronger post-market surveillance datasets, prompting increased investments in cloud-connected consoles that auto-report utilization and outcome metrics to regulators.

Asia Pacific is the fastest-growing territory at 7.4% CAGR through 2030. Government spending to modernize surgical suites in China and India, alongside private investments in Japanese day-surgery chains, fuels rising unit volumes. Healthcare allocations across the region could top USD 138 billion by 2027, with critical care and surgical tech absorbing a sizable share. Local buyers favor compact dual-mode consoles that run on standard power feeds, creating opportunities for mid-priced entrants targeting secondary-city hospitals.

Competitive Landscape

The temperature modulation devices market shows moderate concentration. Medtronic, Stryker and Solventum hold sizeable installed bases across warming blankets, fluid warmers and cardiothoracic cooling lines. Haemonetics expanded into esophageal cooling by purchasing Attune Medical for USD 160 million in 2024, diversifying beyond its blood-management heritage. Getinge’s 2024 acquisition of Paragonix Technologies brought organ-preservation temperature solutions under its cardiovascular umbrella, illustrating a wider trend toward bolt-on buys that round out clinical-episode coverage.

Leading suppliers differentiate on precision, workflow integration and interoperable data streams rather than discounting. Closed-loop algorithms that cut manual intervention generate tangible nursing productivity gains, while built-in analytics satisfy growing regulator interest in real-world evidence. Start-ups focus on ultralight military or EMS devices, often partnering with drone-logistics firms to field-test temperature-controlled blood delivery. Incumbents respond by embedding battery management and rugged casings into next-gen hospital models, blurring traditional product boundaries.

Temperature Modulation Devices Industry Leaders

3M (Solventum)

Stryker

Medtronic

Gentherm Medical (CSZ)

ZOLL Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: BrainCool received an order from ZOLL for 10 demo BrainCool Systems valued at SEK 1.7 million (USD 160,000) to enhance post-cardiac-arrest cooling precision.

- November 2024: FDA approved the VARIPULSE Platform for paroxysmal atrial fibrillation, integrating temperature-control safeguards for ablation.

- August 2024: ZOLL Medical secured USD 37 million in funding to advance therapeutic temperature devices.

Global Temperature Modulation Devices Market Report Scope

| Patient Warming Systems |

| Patient Cooling Systems |

| Intravascular TTM Systems |

| Blood / IV Fluid Warmers |

| Integrated Dual-Mode Systems |

| Perioperative Care |

| Intensive / Critical Care |

| Emergency & Trauma |

| Neonatal & Pediatric Care |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Patient Warming Systems | |

| Patient Cooling Systems | ||

| Intravascular TTM Systems | ||

| Blood / IV Fluid Warmers | ||

| Integrated Dual-Mode Systems | ||

| By Application | Perioperative Care | |

| Intensive / Critical Care | ||

| Emergency & Trauma | ||

| Neonatal & Pediatric Care | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the temperature modulation devices market projected to grow?

It is forecast to rise from USD 3.30 billion in 2025 to USD 4.60 billion by 2030, reflecting a 7.8% CAGR.

Which product category currently leads spending?

Patient warming systems held 53.6% share in 2024 due to universal perioperative usage mandates.

Why are intravascular cooling systems gaining traction?

They offer tighter ±0.2 °C precision, cutting neurologic complications in post-cardiac-arrest care and are expected to post a 12.1% CAGR to 2030.

Which region adds the most new procedures?

Asia Pacific is expanding at a 7.4% CAGR as ambulatory surgery centers proliferate across China, Japan and India.

What is driving demand in emergency settings?

Broader adoption of targeted temperature management protocols after resuscitation fuels an 11.2% CAGR in emergency & trauma applications.

How concentrated is supplier power today?

The market is moderately concentrated with Medtronic, Stryker and Solventum heading global share, but acquisitions such as Haemonetics-Attune are tightening competition.

Page last updated on: