United States Mortgage/Loan Brokers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

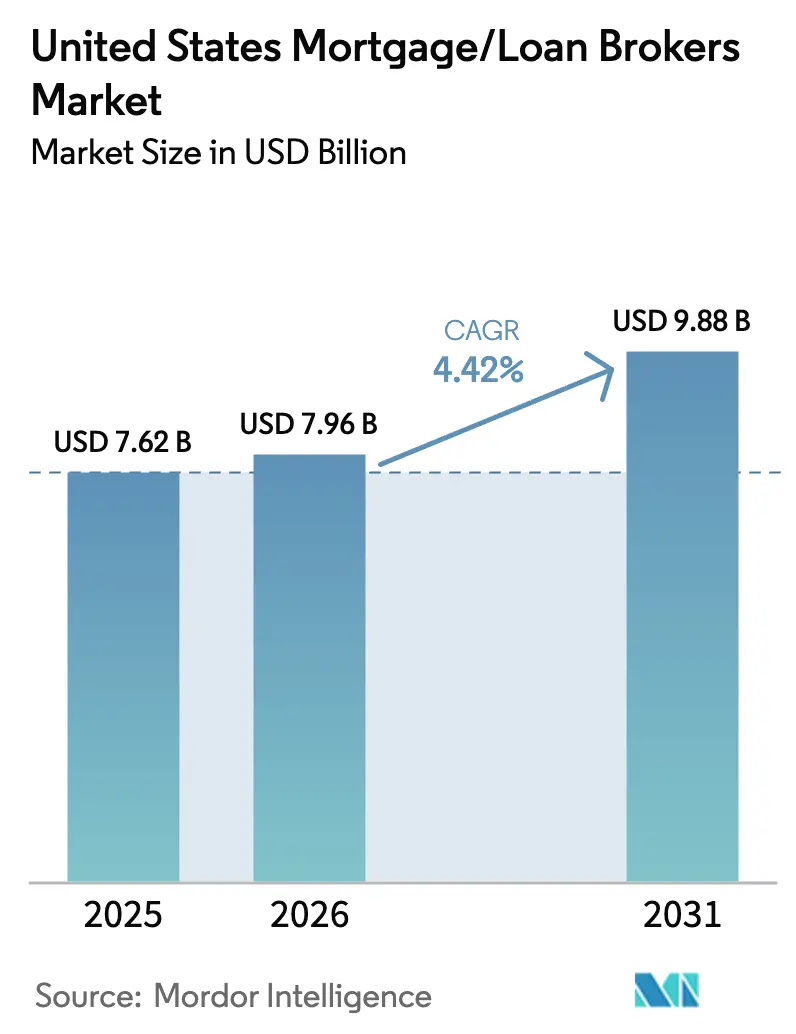

| Base Year Market Size (2025) | USD 7.62 Billion |

| Market Size (2026) | USD 7.96 Billion |

| Market Size (2031) | USD 9.88 Billion |

| Growth Rate (2026 - 2031) | 4.42% CAGR |

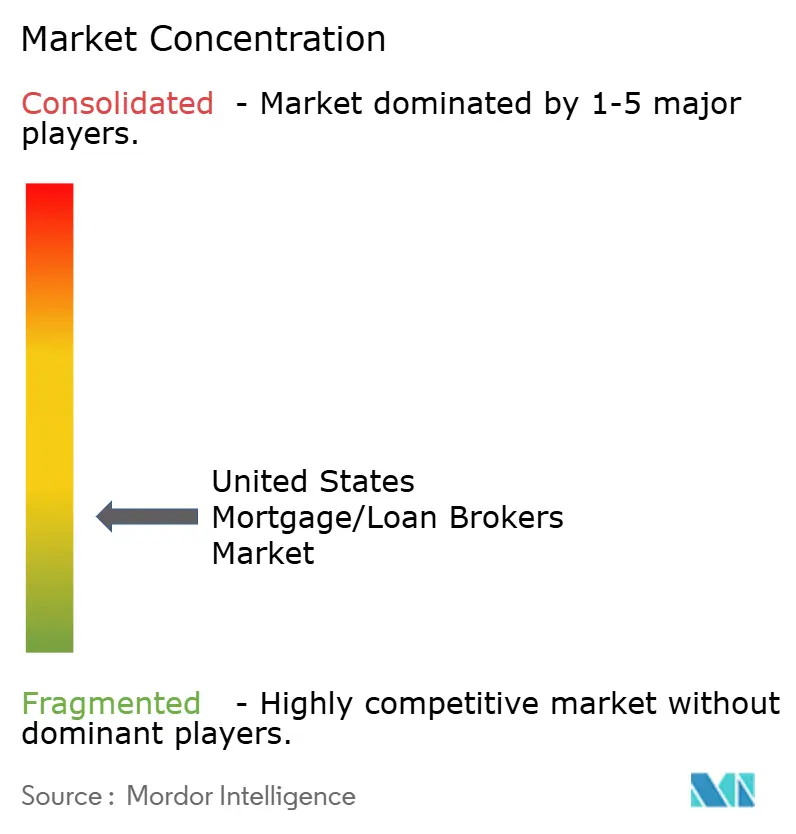

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Mortgage/Loan Brokers Market Analysis by Mordor Intelligence

The United States mortgage/loan brokers market size is expected to grow from USD 7.62 billion in 2025 to USD 7.96 billion in 2026 and is forecast to reach USD 9.88 billion by 2031 at 4.42% CAGR over 2026-2031. This growth trajectory reflects brokers’ ability to remain relevant despite rising compliance costs and rapid digitization, enabling them to bridge borrowers and a fragmented lender landscape. Technology adoption is no longer optional, as 79% of mortgage professionals identify eClosing capabilities as a critical differentiator, while 72% believe artificial intelligence (AI) will reshape lending workflows. Demographic momentum also underpins demand: millennials are now the largest group of homebuyers and, at a median age of 38, often require specialized guidance on down-payment assistance and alternative income documentation[1]Jessica Lautz, “2024 Home Buyers and Sellers Generational Trends Report,” National Association of Realtors, nar.realtor. Wholesale lenders have deepened ties with brokers, illustrated by United Wholesale Mortgage’s technology-heavy, broker-first model, which accelerates approvals and improves pricing. Interest-rate volatility that pushed 30-year fixed rates toward 7% in 2024 has re-weighted business toward purchase loans, but it also created openings for niche products such as renovation and construction-to-permanent mortgages.

Key Report Takeaways

- By loan type, conventional conforming mortgages led with 64.12% of the United States mortgage/loan brokers market share in 2025, whereas non-qualified products are projected to grow at a 4.75% CAGR through 2031.

- By borrower profile, repeat and second-home buyers accounted for 44.05% share of the United States mortgage/loan brokers market size in 2025; real-estate investors represent the fastest-growing group at 5.53% CAGR.

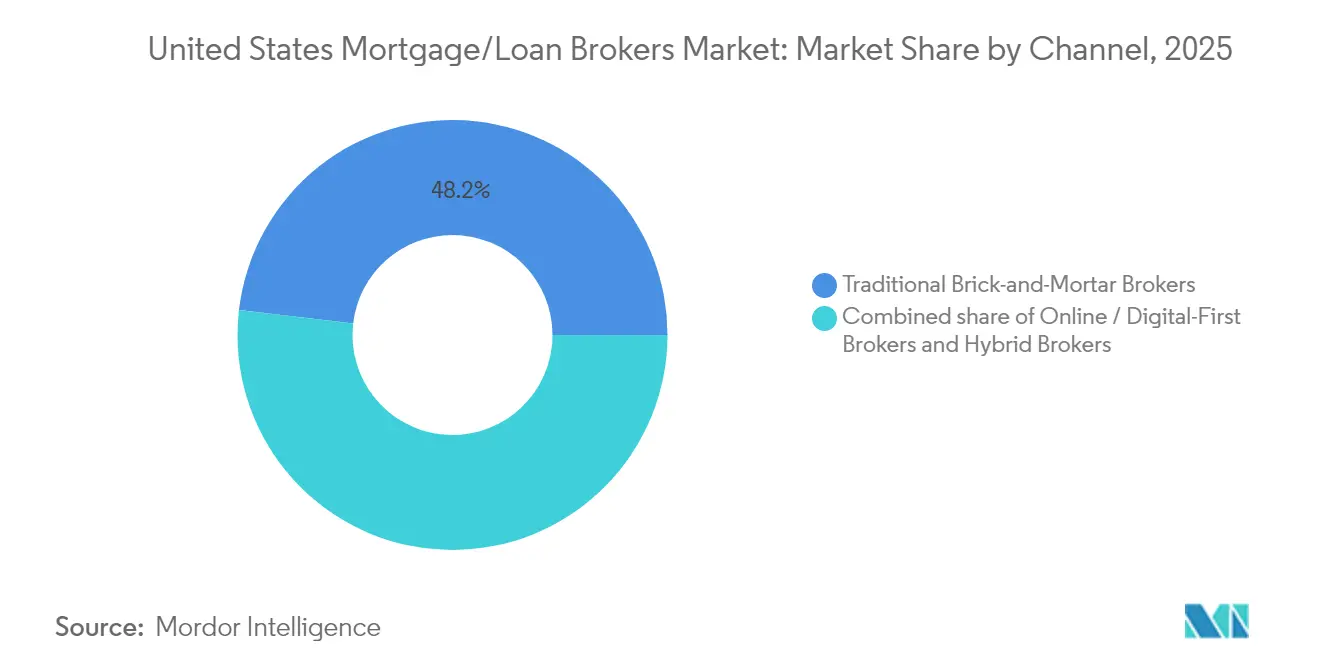

- By distribution channel, brick-and-mortar brokers held 48.15% revenue share in 2025, while online and digital-first brokers are expected to expand at a 4.90% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Mortgage/Loan Brokers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demographic tailwind of millennial home-buyers | +0.8% | National, with concentration in metropolitan areas | Medium term (2-4 years) |

| Persistent low-to-moderate mortgage rates | +0.6% | National | Short term (≤ 2 years) |

| Expansion of wholesale lender programs for brokers | +0.7% | National, with stronger impact in competitive markets | Medium term (2-4 years) |

| Digitisation lowering application friction | +0.5% | National, with faster adoption in tech-forward regions | Long term (≥ 4 years) |

| AI-driven pre-qualification tools raising broker conversion | +0.4% | National, with early gains in major metropolitan areas | Medium term (2-4 years) |

| Growing demand for green-home mortgage products | +0.3% | West Coast, Northeast, and environmentally conscioUnited States markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demographic tailwind of millennial buyers

Millennials are reaching prime purchase age and already form the largest cohort of homebuyers, yet affordability challenges have lifted the median first-time-buyer age to 38. These borrowers gravitate toward brokers for help with down-payment grants, non-traditional income verification, and nuanced lender comparisons. Their preference for digital processes dovetails with broker investments in mobile apps and eClosing portals, shortening approval cycles and reducing fallout. Because many millennials buy in high-cost metros, demand for jumbo and non-conforming loans rises, allowing brokers to command premium fees. Persistent student-debt burdens and variable gig-economy income further heighten reliance on broker guidance.

Expansion of wholesale-lender programs for brokers

Nonbank lenders captured 83.2% of agency originations by late 2024 and rely on brokers as cost-effective distribution partners[2]Laurie Goodman, “Housing Finance at a Glance, Oct 2024 Chartbook,” Urban Institute, urban.org. United Wholesale Mortgage’s AI-enabled broker tools illustrate how deeper technology integration can cut time-to-close and sharpen pricing. Larger menus, marketing subsidies, and compliance resources from wholesale lenders make it easier for small and midsize brokers to compete with direct-lending fintechs. Heightened competition among wholesalers has improved broker compensation and service-level agreements. These enhancements reinforce the perceived value of brokers in complex loan scenarios.

AI-driven pre-qualification tools raising broker conversion

A 2024 survey showed 72% of mortgage executives consider AI transformative for underwriting and lead conversion. AI engines instantly parse credit, employment, and income data to determine eligibility, enabling brokers to deliver same-day conditional approvals. Machine-learning models flag documentation gaps early, allowing borrowers to resolve issues before lock expiration. Self-employed applicants benefit because algorithms evaluate cash-flow consistency rather than traditional W-2s. As subscription prices drop, even boutique brokers can deploy predictive analytics, closing the technology gap with nationwide players.

Growing demand for green-home mortgage products

Government-sponsored enterprises now buy loans under programs such as HomeStyle Energy, which funds energy-efficiency upgrades at concessional rates[3]Fannie Mae, “HomeStyle Energy Overview,” fanniemae.com. State and municipal incentives amplify savings, motivating eco-conscious buyers in California, Massachusetts, and Washington to seek specialized financing. Brokers versed in green certifications and rebate stacks can monetize advisory roles while enhancing borrower affordability through lower utility bills. Millennials and Gen Z consumers express strong preferences for sustainable housing finance, aligning demographic and environmental tailwinds. Rising energy-efficiency premiums in home values further cement this niche.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened CFPB & state regulatory scrutiny | -0.9% | National, with varying state-level intensity | Short term (≤ 2 years) |

| Interest-rate volatility suppressing refinance volume | -1.2% | National | Short term (≤ 2 years) |

| Fintech direct-lending models bypassing brokers | -0.6% | National, with stronger impact in tech-savvy demographics | Medium term (2-4 years) |

| Rising cyber-security & data-compliance costs | -0.4% | National, with higher impact on smaller brokers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Interest-rate volatility is suppressing refinance volume.

Thirty-year fixed rates hovered near 7% throughout 2024, erasing most conventional refinance incentives. Brokers that once relied on serial refis now chase purchase business, which typically requires deeper borrower counseling and higher acquisition costs. Rate locks became pricier, and indecisive borrowers often delay closings, shrinking pipelines. With existing-home sales down and new-construction starts unpredictable, competition for purchase leads intensifies among brokers and fintechs alike. Firms must pivot to niche products such as renovation, DSCR, or reverse mortgages to stabilize revenue.

Heightened CFPB & state regulatory scrutiny

The Consumer Financial Protection Bureau has broadened examinations of nonbank mortgage companies, levying multimillion-dollar penalties for pricing discrimination and disclosure lapses[4]Consumer Financial Protection Bureau, “CFPB Supervisory Highlights – 2024,” consumerfinance.gov. Many states added licensing tiers and cybersecurity mandates, forcing brokers to expand compliance staff or outsource costly legal reviews. FHA also shortened incident-reporting windows for cyberbreaches, raising technology overhead. Smaller independents struggle to absorb these expenses, accelerating consolidation toward capital-rich networks. Documentation creep lengthens processing times, eroding profitability for volume-based brokers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Loan Type: Conforming anchors volume while specialty loans outpace

Conventional conforming mortgages represented 64.12% of the United States mortgage/loan brokers market share in 2025, supported by standardized underwriting and liquidity from the secondary market. The United States mortgage/loan brokers market size for conforming products is projected to reach USD 6.34 billion by 2031, mirroring steady demand for mainstream financing. Jumbo and non-conforming loans thrive in metros where median prices surpass federal limits, allowing brokers to capture higher fees on complex files. FHA, VA, and USDA loans remain essential for underserved or rural borrowers, expanding broker reach into niche geographies. Rate shifts have bolstered renovation and construction-to-permanent loans, enabling owners to upgrade existing homes rather than move.

Specialty products—non-qualified mortgages, reverse, renovation, and construction-to-permanent loans—are growing at a 4.75% CAGR, the fastest among all loan types. Flexible underwriting appeals to self-employed borrowers and investors who cannot meet agency guidelines yet exhibit strong cash flow. Reverse mortgages gain traction as baby boomers monetize equity without monthly payments, a trend brokers exploit through senior-focused advisory practices. Renovation financing satisfies demand amid tight housing supply, merging purchase and rehab funds into a single closing. Because these loans carry wider spreads, brokers can offset shrinking refi volume and enhance profitability.

By Borrower Type: Investor appetite widens broker scope

Repeat and second-home buyers controlled 44.05% of the United States mortgage/loan brokers market share in 2025, reflecting equity-rich owners upgrading or adding vacation properties. Investors, however, exhibit a robust 5.53% CAGR through 2031, buoyed by cash-flow-based DSCR products that evaluate rental income over personal debt-to-income ratios. The United States mortgage/loan brokers market size for investor lending is forecast to cross USD 1.73 billion by 2031. Brokers adept at analyzing rent rolls and cap rates can differentiate themselves in this segment. First-time-buyer activity remains constrained by down-payment hurdles and high prices, yet targeted assistance programs present advisory opportunities.

Investor momentum fuels the development of portfolio loans and fix-and-flip credit lines, forcing brokers to master valuation techniques and exit strategies. Seniors increasingly consider reverse mortgages to supplement retirement, demanding specialized counseling and compliance safeguards. Refinancing borrowers have largely vanished given current rates, compelling brokers to re-tool lead-generation strategies from database recapture to purchase-centric prospecting. Each borrower archetype carries unique disclosure and licensing requirements, underscoring the need for segment-specific expertise. Successful brokers segment marketing by lifecycle stage to optimize conversion.

By Channel: Digital acceleration re-shapes service models

Brick-and-mortar brokers still generated 48.15% of 2025 volume, underpinned by local referral networks and face-to-face interactions that resonate in complex transactions. Yet the fastest-growing route is digital-first, projected at 4.90% CAGR as tech-savvy borrowers favor online self-service portals. The United States mortgage/loan brokers market size tied to digital channels could exceed USD 4.46 billion by 2031. Hybrid models that blend physical presence with end-to-end digital workflows are emerging as best practice, offering convenience without sacrificing human touch. High-volume digital brokers leverage AI chatbots and automated verifications to cut cycle times to under 15 days.

Regulatory parity across channels keeps compliance burdens similar, but digital operators shoulder extra cybersecurity and e-signature duties. Cost advantages from leaner footprints let pure-play online brokers price aggressively, pressuring traditional shops to modernize. Conversely, complex jumbo or construction loans often revert to relationship-heavy models, preserving relevance for community-based brokers. The channel shift also broadens geographic reach, enabling digital brokers licensed in multiple states to capture demand spikes irrespective of physical location. Investment in omnichannel capabilities will likely define future winners.

Geography Analysis

Regional dynamics remain pivotal for the United States mortgage/loan brokers market, with high-cost metros on the coasts producing elevated average loan balances that boost commission revenue. California, New York, and Washington, D.C. require jumbo expertise and non-conforming solutions, translating into larger per-file earnings for brokers familiar with complex underwriting. Environmental ordinances in California also drive demand for green mortgage products, reinforcing brokers that specialize in energy-efficient lending. Regulatory overlays add another dimension; California’s additional licensing and disclosure rules heighten entry barriers for out-of-state firms, indirectly concentrating share among compliant incumbents.

The Southeast, led by Texas and Florida, benefits from inbound migration and relatively affordable housing, generating brisk purchase activity. Population inflows sustain demand for FHA and VA loans, while robust rental markets attract investors seeking DSCR financing. These states feature business-friendly regulations and lower closing costs, allowing brokers to operate with thinner margins yet higher volume. Rural regions across the Midwest and Great Plains lean on USDA programs, rewarding brokers versed in government-backed lending and property eligibility mapping. Though transaction counts are lower, brokers build durable relationships through personalized service.

Interest-rate sensitivity varies by region; Sunbelt markets witness stronger purchase resilience, whereas high-tax Northeastern states saw sharper volume contractions when rates climbed. Tech-sector exposure on the West Coast introduces cyclical demand swings tied to employment volatility. Local zoning and appraisal norms further complicate underwriting, emphasizing the need for geographic mastery. Brokerages expanding via remote-licensing strategies must still invest in regional compliance and appraiser networks to maintain service quality. Ultimately, regional heterogeneity underscores why national brands pair centralized technology with localized expertise.

Competitive Landscape

The United States mortgage/loan brokers market is moderately fragmented but moving toward consolidation as compliance and technology costs climb. Rocket Companies set a transformative precedent by acquiring Redfin for USD 1.75 billion and proposing a USD 9.4 billion takeover of Mr. Cooper, creating an end-to-end real-estate-to-servicing ecosystem. Such vertical integration pressures stand-alone brokers to partner with prop-tech platforms or risk disintermediation. Three strategic archetypes dominate: tech-centric brokers deploying AI and e-close stacks, regional specialists serving high-value metros, and integrated real-estate brands bundling search, agency, and loan origination.

United Wholesale Mortgage exemplifies a broker-aligned wholesaler, rolling out the ChatUWM AI platform that automates borrower Q&A and document intake. Guaranteed Rate reinforced its sales force by onboarding veteran loan officers from rivals, a talent-acquisition play responding to contracting origination volumes. Fintech challengers such as Better.com advance embedded-finance APIs that let builders or real-estate portals offer point-of-sale mortgages, sidestepping traditional brokers. In response, networks like AIME (Association of Independent Mortgage Experts) provide compliance and technology toolkits at scale, helping independents retain autonomy.

Size now confers regulatory insulation; larger brokerages spread fixed compliance costs over higher volume and invest in cyber-defense. Smaller shops combat scale disadvantages by niching into reverse mortgages, non-QM lending, or multicultural markets. Pricing competition remains intense, yet service differentiation—human guidance on complex files—still commands loyalty. Market share is fluid as lenders recalibrate pricing and repurchase risk, underscoring brokers’ role as borrower advocates shopping multiple outlets. The next consolidation wave may hinge on AI adoption rates and capital access.

United States Mortgage/Loan Brokers Industry Leaders

CrossCountry Mortgage, LLC

Fairway Independent Mortgage Corporation

Guaranteed Rate, Inc.

Guild Mortgage Company

Caliber Home Loans, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Rocket Companies announced a USD 1.75 billion acquisition of Redfin, integrating property search, brokerage, and mortgage origination under one umbrella.

- March 2025: Rocket Companies proposed a USD 9.4 billion acquisition of Mr. Cooper Group, aiming to build the nation’s largest servicing portfolio exceeding USD 1 trillion.

- December 2024: Guaranteed Rate completed a talent-acquisition sweep, hiring high-performing loan officers from competing firms to defend share amid lower volumes.

- May 2024: United Wholesale Mortgage launched ChatUWM, an AI-powered chatbot that streamlines broker communications and accelerates application processing.

United States Mortgage/Loan Brokers Market Report Scope

A mortgage broker is a middleman who helps people or businesses with the mortgage loan application process. In essence, they build connections between mortgage lenders and borrowers without investing any of their own money. The report provides a comprehensive background analysis of the US Mortage/Loan Brokers market, covering the current market trends, restraints, technological updates, and detailed information on various segments and the industry's competitive landscape. Additionally, the COVID-19 impact has been incorporated and considered during the study.

The United States Mortgage/Loans Broker Market Is Segmented By Component (Products And Services) And By Enterprise Size (Large, Small, And Medium-Sized). By Application (Home Loans, Commercial And Industrial Loans, Vehicle Loans, Loans To Governments, And Others), And By End-User (Businesses And Individuals). The Report Offers Market Size And Forecasts For The Us Mortgage/Loans Market In Value (USD) For All The Above Segments.

| Conventional Conforming |

| Non-Conforming / Jumbo |

| FHA-Insured |

| VA-Guaranteed |

| USDA / Rural Housing |

| Others (Non-QM, Reverse Mortgag,Renovation, Construction-to-Perm) |

| First-time Home Buyers |

| Repeat & Second Home Buyers |

| Real-Estate Investors |

| Others (Refinance Borrowers,Seniors / Reverse Borrowers) |

| Online / Digital-First Brokers |

| Traditional Brick-and-Mortar Brokers |

| Hybrid Brokers |

| By Loan Type (Value) | Conventional Conforming |

| Non-Conforming / Jumbo | |

| FHA-Insured | |

| VA-Guaranteed | |

| USDA / Rural Housing | |

| Others (Non-QM, Reverse Mortgag,Renovation, Construction-to-Perm) | |

| By Borrower Type (Value) | First-time Home Buyers |

| Repeat & Second Home Buyers | |

| Real-Estate Investors | |

| Others (Refinance Borrowers,Seniors / Reverse Borrowers) | |

| By Channel (Value) | Online / Digital-First Brokers |

| Traditional Brick-and-Mortar Brokers | |

| Hybrid Brokers |

Key Questions Answered in the Report

What is the projected size of the United States mortgage/loan brokers market in 2031?

It is forecast to reach USD 9.88 billion by 2031, reflecting a 4.42% CAGR from 2026.

Which loan category is expanding fastest?

Non-qualified mortgages, including reverse, renovation, and construction-to-permanent loans, are growing at a 4.75% CAGR.

Why are investors an attractive segment for brokers?

Investor demand is driven by DSCR loans that qualify based on rental income, propelling a 5.53% CAGR through 2031.

How are digital-first brokers affecting competition?

They cut cycle times with AI and eClose tools, growing at a 4.90% CAGR and pressuring traditional shops to modernize.

What regulatory trend is most challenging for brokers?

Heightened CFPB and state scrutiny increases compliance costs, disadvantaging smaller independents and accelerating consolidation.

Page last updated on: