U.S. Electrotherapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

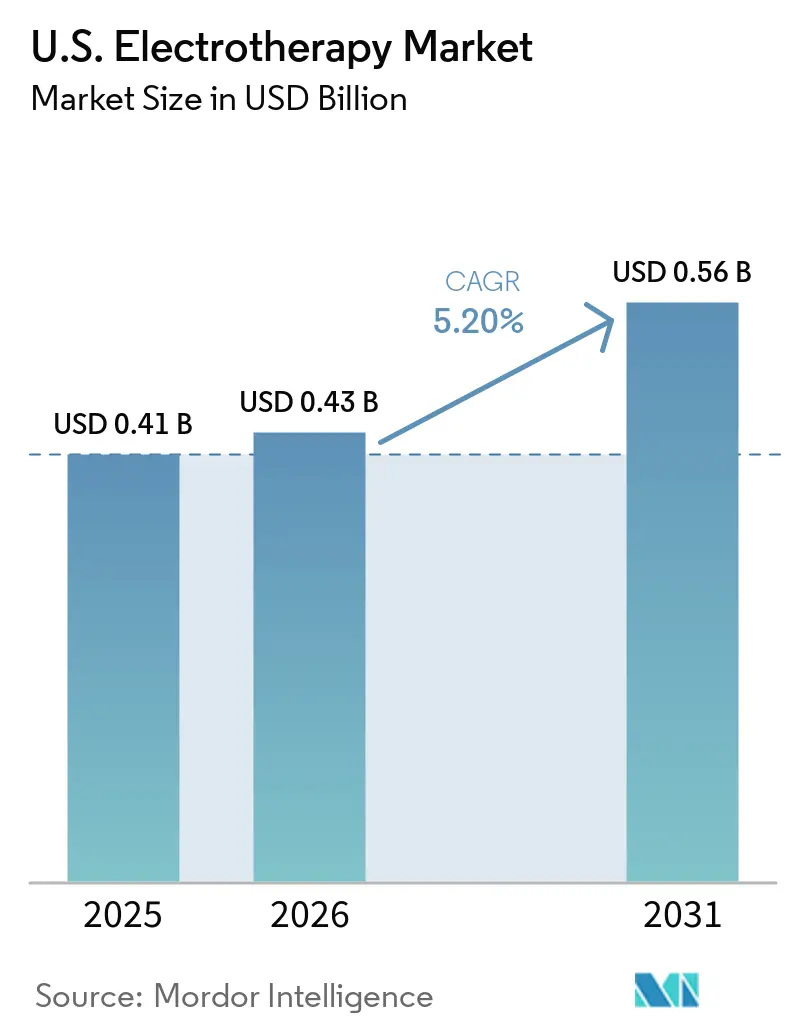

| Base Year Market Size (2025) | USD 0.41 Billion |

| Market Size (2026) | USD 0.43 Billion |

| Market Size (2031) | USD 0.56 Billion |

| Growth Rate (2026 - 2031) | 5.20% CAGR |

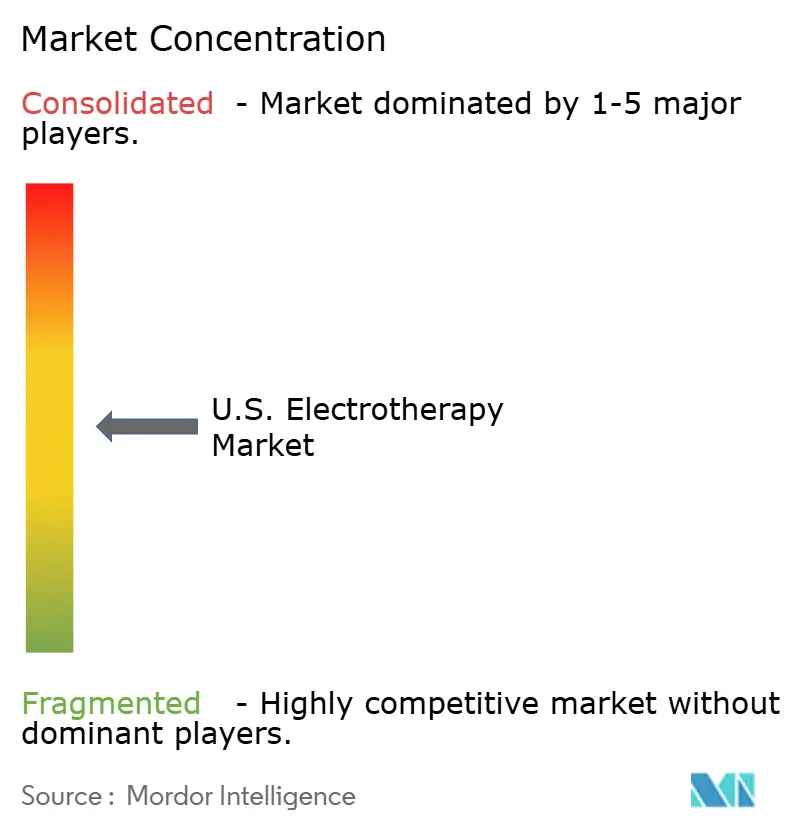

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Electrotherapy Market Analysis by Mordor Intelligence

The U.S. Electrotherapy Market size is expected to increase from USD 0.41 billion in 2025 to USD 0.43 billion in 2026 and reach USD 0.56 billion by 2031, growing at a CAGR of 5.20% over 2026-2031.

According to CDC data, 24.3% of adults in the United States, approximately 60 million people, experienced chronic pain, while 8.9% suffered from high-impact chronic pain that restricted daily activities. Older adults, particularly those aged 65 and above, reported a 36.0% prevalence rate, sustaining long-term demand for non-drug pain management solutions.[1]Centers for Disease Control and Prevention, “QuickStats: Percentage of Adults Aged ≥18 Years with Chronic Pain in the Past 3 Months, by Sex and Urbanization Level, United States, 2023,” MMWR, cdc.gov The United States electrotherapy market is gaining momentum due to increased policy and clinical support for non-opioid treatment pathways, particularly in specialized pain care and outpatient rehabilitation. Additionally, home-use clearances are expanding treatment access, transforming how the market is sold, monitored, and reimbursed.

Key Report Takeaways

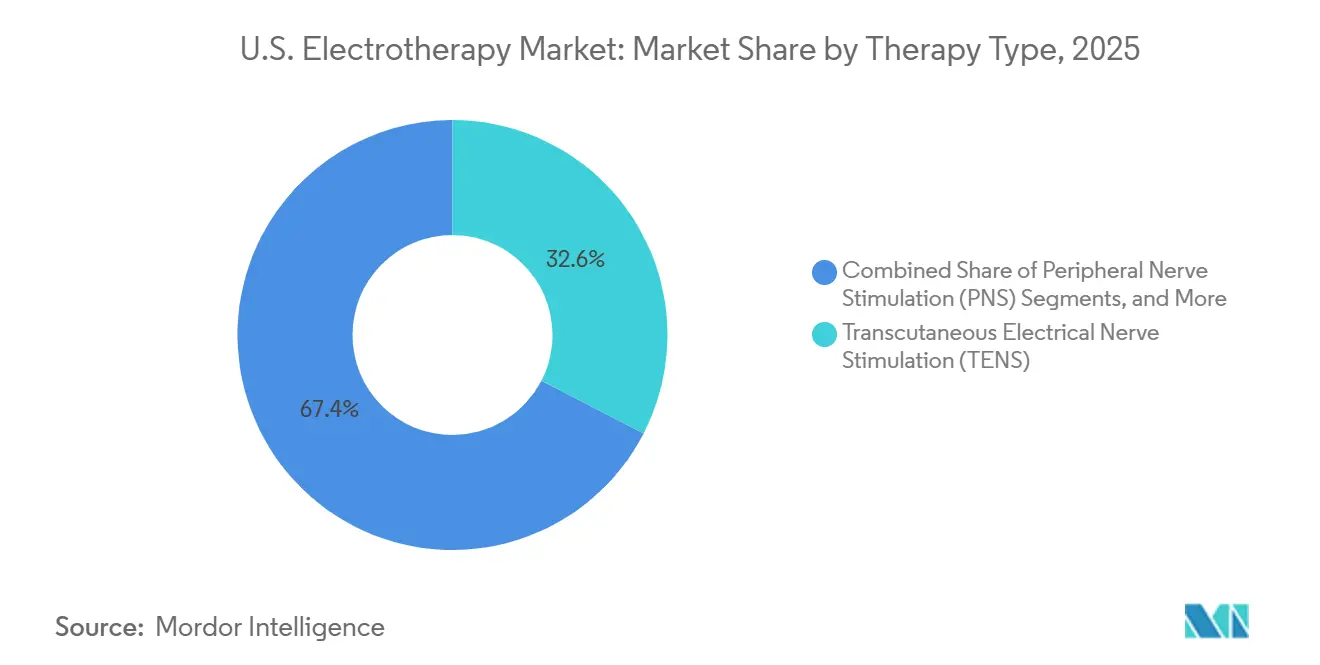

- By therapy type, TENS therapy devices led with 32.55% share in 2025, while neuromuscular electrical stimulation is projected to grow at a 6.80% CAGR through 2031.

- By application, pain management accounted for 42.88% share in 2025, while neuromuscular dysfunction and rehabilitation is forecasted to expand at a 6.35% CAGR through 2031.

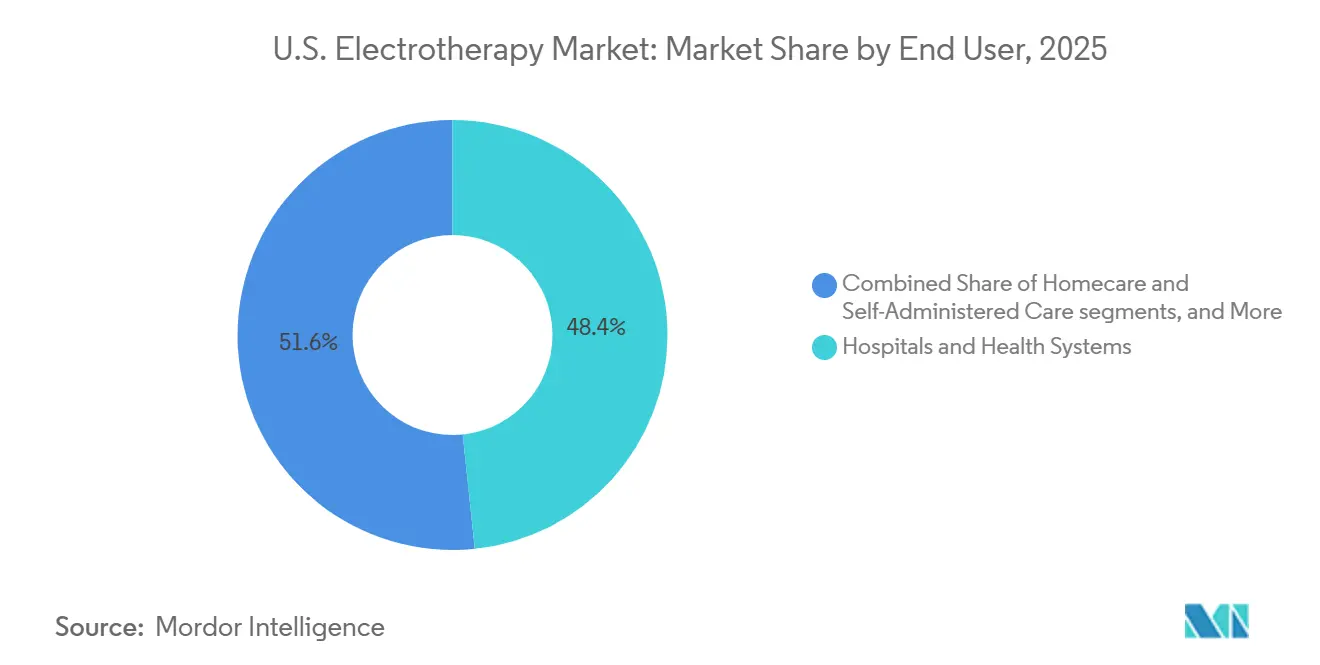

- By end user, hospitals and health systems held 48.35% share in 2025, while homecare and self-administered care is expected to grow at a 7.10% CAGR through 2031.

- By prescription type, prescription devices captured 79.25% share in 2025, while over-the-counter devices are projected to grow at a 6.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Electrotherapy Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Chronic pain burden and aging-related pain incidence | +1.2% | National, with higher intensity in the rural Midwest, Sun Belt, and Appalachian regions | Long term (≥ 4 years) |

| Opioid-sparing treatment preference across pain care pathways | +0.9% | National, with earlier traction in states with stricter prescribing mandates such as Ohio, Florida, and Massachusetts | Medium term (2-4 years) |

| Home-based rehabilitation and portable device adoption | +0.8% | National, with stronger pull in suburban and rural markets with limited clinic access | Medium term (2-4 years) |

| Higher outpatient musculoskeletal and post-surgical rehab volume | +0.6% | National, with key gains in high-ASC-density states such as Texas, Florida, and California | Short term (≤ 2 years) |

| Faster coverage visibility for breakthrough stimulation platforms | +0.5% | National, with earlier gains in New England and West Coast innovation hubs | Medium term (2-4 years) |

| Remote programming and adherence analytics improving home-use | +0.3% | National, concentrated in markets with more mature telehealth infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic Pain Burden and Aging-Related Pain Incidence

Chronic pain remains a significant driver for the United States electrotherapy market, with 24.3% of adults, approximately 60 million people, experiencing chronic pain in 2025. Among them, 8.9% faced high-impact chronic pain that disrupted daily activities. Older adults were most affected, with a 36.0% prevalence among those aged 65 and above, compared to 12.3% to 28.7% in younger groups.[2] Springer Nature, “Current Pain and Headache Reports Article on Peripheral Nerve Stimulation,” Current Pain and Headache Reports, springer.com Conditions like osteoarthritis and spinal degeneration highlight the role of electrotherapy in drug-sparing pain management. The market benefits from a stable demand base across outpatient rehabilitation, homecare, and chronic disease management settings.

Opioid-Sparing Treatment Preference Across Pain Care Pathways

The shift toward non-opioid pain treatments is strengthening the United States electrotherapy market across hospitals, outpatient facilities, and specialist channels. The NOPAIN Act supports Medicare payments for non-opioid treatments through 2027, enhancing the financial case for device-based pain management. The Alternatives to PAIN Act reduces prior authorization barriers under Medicare Part D, favoring non-drug therapies.[3]Centers for Medicare & Medicaid Services, “Transcutaneous Electrical Nerve Stimulators, LCD L33802,” Medicare Coverage Database, cms.gov Specialist endorsements for peripheral nerve stimulation in chronic back pain further drive adoption, with higher-value prescription systems gaining traction over consumer devices.

Home-Based Rehabilitation and Portable Device Adoption

Home-based treatments are expanding the United States electrotherapy market by increasing accessibility. ONWARD Medical received FDA clearance in 2025 for ARC-EX home use in incomplete spinal cord injury patients, with over 60 clinics adopting the system. ANEUVO's ExaStim, cleared in 2026, supports spinal cord injury care, including home use. Beurer expanded its TENS, EMS, and heat therapy portfolio in 2026, targeting drug-free pain relief outside clinical settings. These advancements bridge supervised rehabilitation and self-administered therapy, enhancing payer confidence with improved safety and regulatory standards.

Higher Outpatient Musculoskeletal and Post-Surgical Rehab Volume

The shift of musculoskeletal care to outpatient settings is driving demand for electrotherapy devices in the United States. Procedure migration to ambulatory and outpatient environments has increased the relevance of devices in discharge planning and recovery. Federal payment reforms tied to non-opioid treatments further support this trend. Devices like TENS, NMES, and interferential therapy are integral to post-operative rehabilitation, particularly after joint replacements and spinal procedures. A 2026 fibromyalgia study involving 384 patients across 28 clinics also validated TENS use in non-surgical populations, positioning rehabilitation providers as key influencers in patient adoption.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Reimbursement friction, prior authorization, and LCD limits | -0.8% | National, concentrated in Arizona, New Jersey, Ohio, Oklahoma, Texas, and Washington under the WISeR pilot | Short term (≤ 2 years) to Medium term (2-4 years) |

| Mixed clinical evidence across some indications and modalities | -0.7% | National, with disproportionate effect in academic medical centers and payer-heavy Northeast and Midwest markets | Long term (≥ 4 years) |

| Competition from physical therapy, drugs, injections, surgery, and other modalities | -0.5% | National | Medium term (2-4 years) |

| Crowded low-end device supply and compliance burden | -0.4% | National, strongest in OTC and direct-to-consumer segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Reimbursement Friction, Prior Authorization, and LCD Limits

Reimbursement complexities remain a key short-term challenge for the United States electrotherapy market. The WISeR Model, effective January 1, 2026, in states like Arizona, New Jersey, and Texas, introduces AI-assisted prior authorization for electrical nerve stimulators, increasing operational burdens and extending sales cycles. Stricter compliance requirements, such as the CMS LCD L33802 for TENS implemented in January 2024, have already added to suppliers' challenges. Larger manufacturers manage these changes more effectively due to scale and resources, while smaller suppliers face significant administrative hurdles. Texas, a critical Medicare-heavy market, amplifies the revenue impact of these added reviews.

Mixed Clinical Evidence Across Some Indications and Modalities

Uneven clinical evidence across surface electrotherapy modalities limits market growth in specific indications. Conventional TENS shows inconsistent results for chronic low back pain and knee osteoarthritis, while microcurrent and interferential therapies face similar challenges due to limited high-level evidence and payer scrutiny. A March 2026 fibromyalgia study demonstrated the value of larger pragmatic trials in generating real-world support. Implantable neuromodulation benefits from stronger evidence and specialist guidelines, creating a market divide where premium implantables maintain value through evidence, while surface devices compete on price, access, and convenience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: TENS Leads Volume as NMES Reshapes the Growth Profile

In 2025, TENS therapy devices held a 32.55% share of the therapy type mix, leading the United States electrotherapy market. Their dominance was driven by broad availability across prescription and over-the-counter channels, enhancing access through clinics, pharmacies, retail outlets, and direct purchases. The FDA's 510(k) pathway remained active, with clearances like the OTC 4-Channel Rechargeable TENS Unit and Zynex Medical's TensWave expanding the prescription TENS portfolio. Interferential and microcurrent therapies retained their roles in physiotherapy, while PENS and bone growth stimulation remained specialized.

Neuromuscular electrical stimulation (NMES) is projected to grow at a 6.80% CAGR through 2031, making it the fastest-growing therapy type. Its adoption is increasing in stroke rehabilitation, spinal cord injury recovery, and post-surgical muscle re-education, supported by home-use clearances. High-value implantables like spinal cord stimulation and sacral neuromodulation continue to dominate revenue, while surface devices drive higher unit sales.

By Application: Pain Management Dominates, Neuromuscular Rehabilitation Accelerates

Pain management accounted for 42.88% of the application mix in 2025, leading the United States electrotherapy market. This reflects the concentration of prescription TENS, peripheral nerve stimulation, and spinal cord stimulation in outpatient pain clinics and spine practices. Bone healing and spinal fusion support maintained stable demand, driven by clinical necessity in high-risk cases, while wound care and dermatological applications remained limited due to reimbursement challenges.

The market for neuromuscular dysfunction and rehabilitation is forecast to grow at a 6.35% CAGR through 2031, driven by rising incidences of stroke, spinal cord injuries, and traumatic brain injuries. Boston Scientific's acquisition of Axonics strengthened its position in pelvic dysfunction therapy, adding a high-growth segment to the application mix. Pain management remains the anchor, while rehabilitation and pelvic neuromodulation are gaining traction.

By End User: Hospital Primacy Persists While Homecare Redefines the Margin Profile

Hospitals and health systems captured 48.35% of end-user revenue in 2025, maintaining their lead in the United States electrotherapy market. Their dominance is tied to implantable neuromodulation procedures requiring surgical infrastructure and post-implant monitoring. Pain management and spine clinics remain key for non-implantable devices, while ambulatory surgery centers are gaining relevance as orthopedic and spine procedures shift from inpatient care.

The homecare segment is expected to grow at a 7.10% CAGR through 2031, making it the fastest-growing end-user category. Clearances for clinical-grade neurostimulation devices have expanded home use, reducing reliance on in-clinic visits. Zynex's restructuring and improved reimbursement access highlight the potential of direct-to-home models, positioning homecare as a significant commercial channel.

By Prescription Type: Prescription Segment Retains Value Share as OTC Grows in Volume

In 2025, prescription devices accounted for 79.25% of revenue, underscoring their dominance in the United States electrotherapy market. High-value products like spinal cord stimulation and sacral neuromodulation remain firmly within this channel, supported by stringent coverage criteria and clinical oversight. Hybrid direct-to-home models are emerging around the prescription base, ensuring its continued revenue leadership.

Over-the-counter devices are projected to grow at a 6.90% CAGR through 2031, driven by easier consumer access, increased awareness of drug-free pain relief, and digital discovery of home-use options. While OTC devices are expanding in volume, their value growth is limited by lower selling prices and intense competition. The prescription channel is expected to retain its dominant revenue share as OTC devices expand their market presence.

Geography Analysis

The United States electrotherapy market benefits from high healthcare spending, established reimbursement channels for durable medical equipment, and an FDA framework supporting implantable and surface stimulation technologies. Demand varies due to differences in chronic pain prevalence by urbanization and gender. In large metropolitan areas, 22.2% of women and 18.8% of men reported chronic pain in the past three months, while rural and micropolitan areas showed higher rates.

The Sun Belt is the leading commercial region for the United States electrotherapy market, driven by large older populations and extensive networks of pain clinics, hospitals, and ambulatory surgery centers in states like Texas, Florida, Arizona, and California. Texas and Arizona's participation in the WISeR pilot from January 2026 adds compliance requirements for suppliers with significant Medicare exposure.

The Midwest and Mid-Atlantic regions exhibit unique demand patterns, with the Veterans Health Administration's extensive network of over 170 medical centers providing centralized procurement for prescription electrotherapy devices. Strong physical therapy utilization in parts of the Midwest drives recurring demand for clinical-grade TENS and NMES systems in rehabilitation.

Competitive Landscape

The United States electrotherapy market has a moderately concentrated. Medtronic, Boston Scientific, and Abbott lead the premium implantable segment by leveraging scale, specialized sales networks, strong physician relationships, and robust clinical evidence. Medtronic enhanced its position with FDA approval for the Inceptiv closed-loop spinal cord stimulator in April 2024, featuring full-body 3T MRI access, strengthening its premium differentiation in spinal cord stimulation. Boston Scientific expanded its pelvic health portfolio with the USD 3.7 billion acquisition of Axonics in November 2024, solidifying its position in sacral neuromodulation. Abbott maintained its competitive edge through outcomes-focused strategies, supported by five-year real-world data for BurstDR therapy presented at NANS 2026.

The surface-stimulation segment is highly competitive, with companies like DJO, LLC, Mettler Electronics, OMRON Healthcare, NeuroMetrix, and Zynex Medical operating across rehabilitation, prescription, and consumer channels. Price pressures are most significant in lower-end and over-the-counter devices, where limited product differentiation and high compliance costs impact profitability. Zynex's restructuring in early 2026 highlighted the challenges of reimbursement friction in direct-to-home models but also demonstrated recovery potential with improved payer access. Nalu Medical's Aetna coverage win in July 2025 for peripheral nerve stimulation showcased how smaller innovators can secure market access through strategic payer contracting and clinical support.

U.S. Electrotherapy Industry Leaders

Abbott Laboratories

Boston Scientific Corporation

Medtronic plc

Enovis Corporation

DJO, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ANEUVO received FDA 510(k) clearance for its ExaStim Stimulation System, a portable, non-invasive platform for spinal cord injury rehabilitation, enabling its U.S. commercial launch.

- March 2026: Beurer expanded U.S. access to its TENS, EMS, and heat-combination therapy devices, targeting the growing OTC and home-use pain relief market.

- February 2026: Zynex Medical resolved its federal investigation and announced a restructuring plan following its December 2025 Chapter 11 filing.

- January 2026: Abbott reported a 75% reduction in pain-related healthcare visits with its BurstDR SCS therapy and received FDA approval for prone MRI scans with its DRG neurostimulation system.

U.S. Electrotherapy Market Report Scope

As per the scope of the report, electrotherapy is a medical and physiotherapy treatment that uses low-voltage electrical currents and electromagnetic energy to stimulate nerves and muscles. It is primarily used to relieve acute and chronic pain, reduce inflammation, heal tissues, prevent muscle atrophy, and improve blood circulation.

The U.S. electrotherapy market is segmented by therapy type, application, end-user, and prescription type. By therapy type, the market includes transcutaneous electrical nerve stimulation (TENS), interferential therapy (IFt), neuromuscular electrical stimulation (NMES) / functional electrical stimulation (FES), microcurrent therapy, percutaneous electrical nerve stimulation (PENS), spinal cord stimulation (SCS), peripheral nerve stimulation (PNS), sacral neuromodulation (SNM), and bone growth stimulation. By application, the market is categorized into pain management, neuromuscular dysfunction and rehabilitation, bone healing and spinal fusion adjunct therapy, urinary and fecal incontinence / pelvic floor dysfunction, and other indications. By end-user, the market is segmented into hospitals and health systems, pain management and spine clinics, physical therapy and rehabilitation centers, ambulatory surgery centers and outpatient orthopedic clinics, homecare and self-administered care, and others. By prescription type, the market is segmented into prescription devices, over-the-counter devices, and hybrid physician-enabled direct-to-home devices. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Transcutaneous Electrical Nerve Stimulation (TENS) |

| Interferential Therapy (IFT) |

| Neuromuscular Electrical Stimulation (NMES) / Functional Electrical Stimulation (FES) |

| Microcurrent Therapy |

| Percutaneous Electrical Nerve Stimulation (PENS) |

| Spinal Cord Stimulation (SCS) |

| Peripheral Nerve Stimulation (PNS) |

| Sacral Neuromodulation (SNM) |

| Bone Growth Stimulation |

| Pain Management |

| Neuromuscular Dysfunction and Rehabilitation |

| Bone Healing and Spinal Fusion Adjunct Therapy |

| Urinary and Fecal Incontinence / Pelvic Floor Dysfunction |

| Other Indications |

| Hospitals and Health Systems |

| Pain Management and Spine Clinics |

| Physical Therapy and Rehabilitation Centers |

| Ambulatory Surgery Centers and Outpatient Orthopedic Clinics |

| Homecare and Self-Administered Care |

| Others |

| Prescription Devices |

| Over-the-Counter Devices |

| Hybrid Physician-Enabled Direct-to-Home Devices |

| By Therapy Type | Transcutaneous Electrical Nerve Stimulation (TENS) |

| Interferential Therapy (IFT) | |

| Neuromuscular Electrical Stimulation (NMES) / Functional Electrical Stimulation (FES) | |

| Microcurrent Therapy | |

| Percutaneous Electrical Nerve Stimulation (PENS) | |

| Spinal Cord Stimulation (SCS) | |

| Peripheral Nerve Stimulation (PNS) | |

| Sacral Neuromodulation (SNM) | |

| Bone Growth Stimulation | |

| By Application | Pain Management |

| Neuromuscular Dysfunction and Rehabilitation | |

| Bone Healing and Spinal Fusion Adjunct Therapy | |

| Urinary and Fecal Incontinence / Pelvic Floor Dysfunction | |

| Other Indications | |

| By End User | Hospitals and Health Systems |

| Pain Management and Spine Clinics | |

| Physical Therapy and Rehabilitation Centers | |

| Ambulatory Surgery Centers and Outpatient Orthopedic Clinics | |

| Homecare and Self-Administered Care | |

| Others | |

| By Prescription Type | Prescription Devices |

| Over-the-Counter Devices | |

| Hybrid Physician-Enabled Direct-to-Home Devices |

Key Questions Answered in the Report

What is the size of the US electrotherapy market in 2026 and 2031?

The US electrotherapy market size is USD 0.43 billion in 2026 and is projected to reach USD 0.56 billion by 2031, growing at a 5.20% CAGR.

Which therapy type leads revenue in the US electrotherapy space?

TENS therapy devices held the largest therapy-type share at 32.55% in 2025 because they are well established in both prescription and OTC channels.

Which therapy type is growing the fastest through 2031?

Neuromuscular electrical stimulation is the fastest-growing therapy modality, with a projected 6.80% CAGR through 2031, supported by rehabilitation demand and home-use expansion.

Why is pain management the largest application area?

Pain management held 42.88% share in 2025 because it captures the largest concentration of prescription TENS and implantable stimulation use in outpatient pain and spine settings.

Which end-user setting is expanding the fastest in the United States?

Homecare and self-administered care is expected to grow at a 7.10% CAGR through 2031 as FDA-cleared home-use systems make treatment easier outside clinics.

Why do prescription devices still dominate value despite OTC growth?

Prescription devices accounted for 79.25% of revenue in 2025 because the highest-priced products, including SCS, SNM, and PNS systems, are physician-directed and reimbursement-linked.

Page last updated on: