Proton Therapy Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.56 Billion |

| Market Size (2031) | USD 2.20 Billion |

| Growth Rate (2026 - 2031) | 7.15% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Proton Therapy Systems Market Analysis by Mordor Intelligence

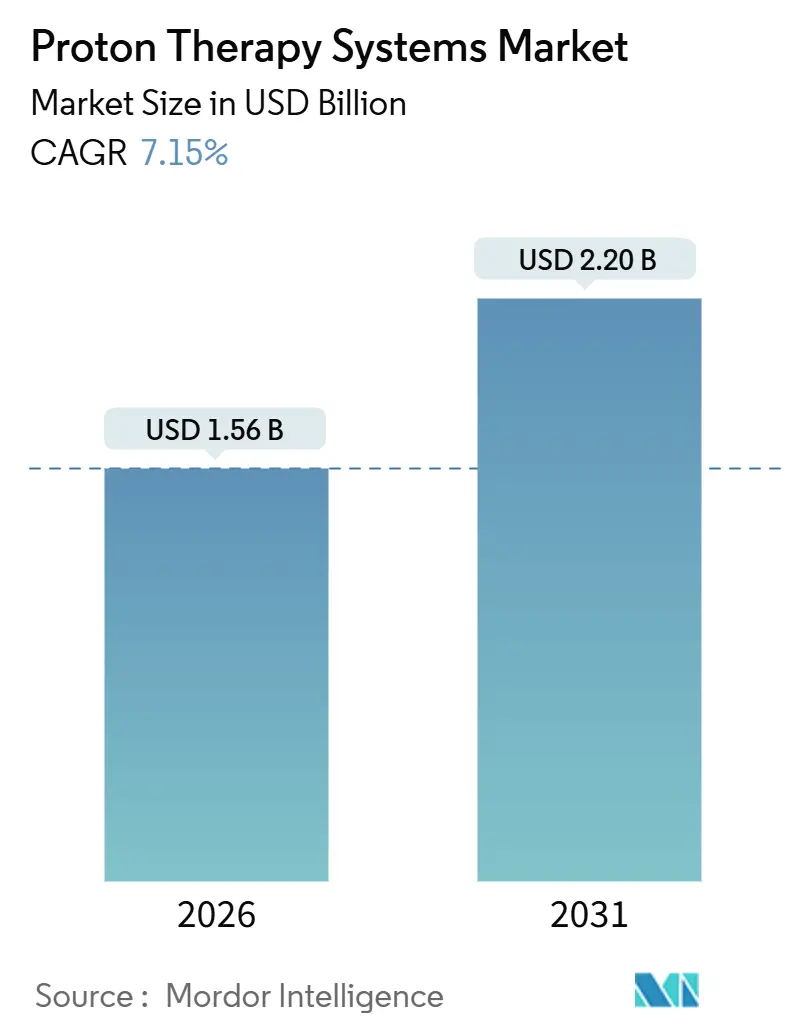

The proton therapy systems market size is estimated at USD 1.56 billion in 2026 and is projected to reach USD 2.20 billion by 2031, advancing at a 7.15% CAGR during the forecast period. Capital-efficient single-room installations, reimbursement expansions for pediatric and central nervous system (CNS) cancers, and the shift to pencil-beam scanning with AI-driven adaptive planning are accelerating commercial adoption. Leading cancer centers routinely exceed 100 daily treatments, signaling throughput gains that improve payback periods. Asia-Pacific is emerging as the fastest-growing region, supported by public insurance coverage in Japan and large infrastructure programs in China and India. Compact superconducting synchrocyclotrons are compressing operating costs by up to USD 1 million per gantry annually, widening the addressable base of regional hospitals. At the same time, early FLASH and ultra-high-dose-rate (UHDR) trials hint at a premium-priced niche should long-term toxicity benefits be confirmed.

Key Report Takeaways

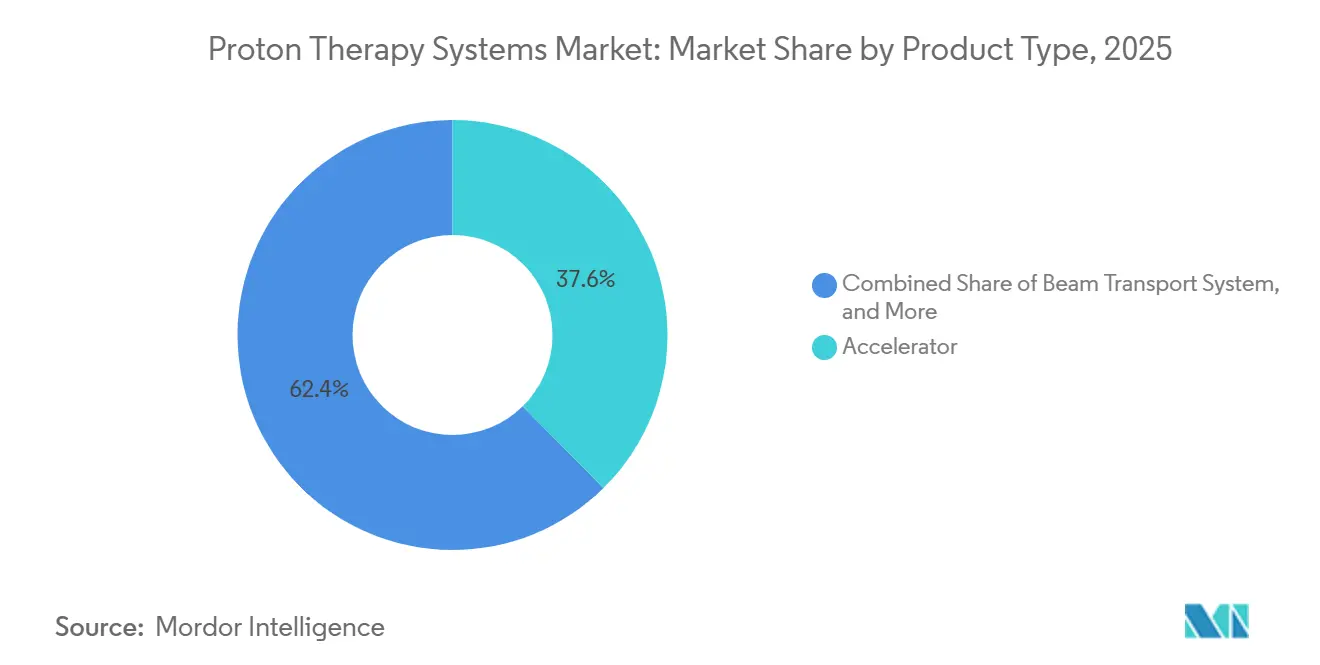

- By product type, accelerators led with 37.55% revenue share in 2025; patient-positioning systems are forecast to expand at a 9.25% CAGR through 2031.

- By system configuration, multi-room installations held 54.53% of the proton therapy systems market share in 2025, while single-room platforms are projected to grow at an 11.85% CAGR to 2031.

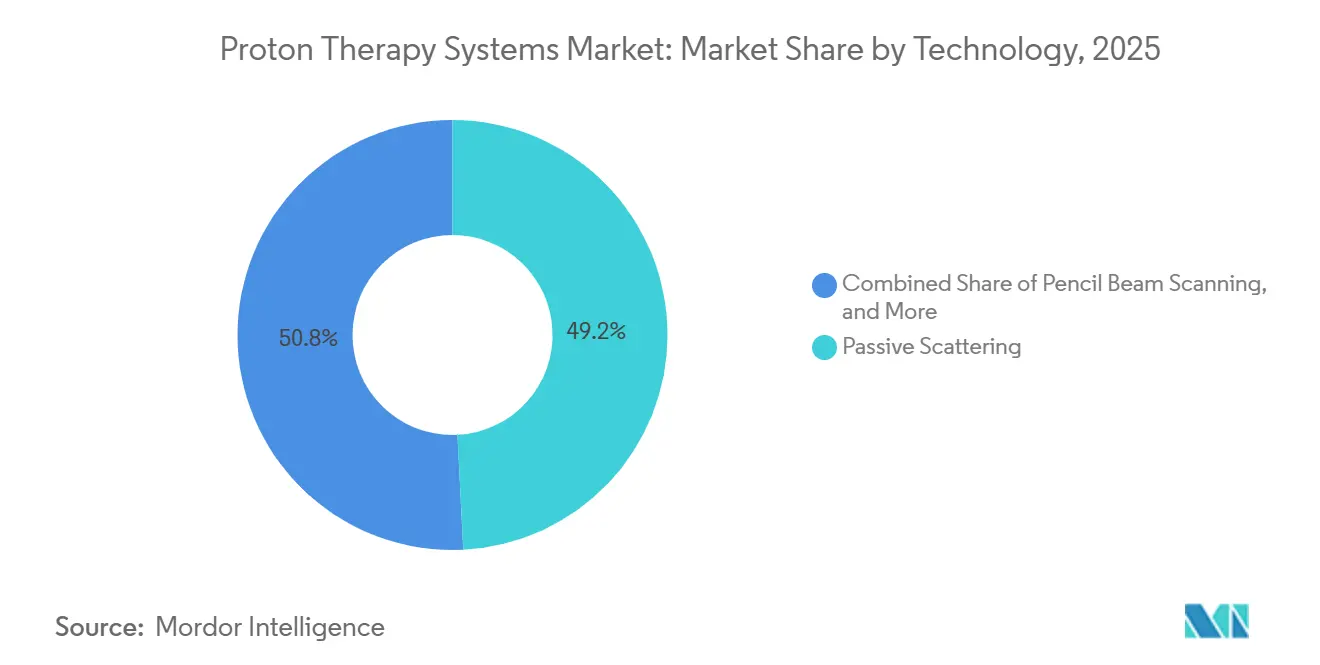

- By technology, passive scattering retained a 49.23% share in 2025; pencil-beam scanning is advancing at a 10.55% CAGR through 2031.

- By application, CNS cancers accounted for 30.03% of the proton therapy market in 2025, and breast cancer is growing at a 12.11% CAGR through 2031.

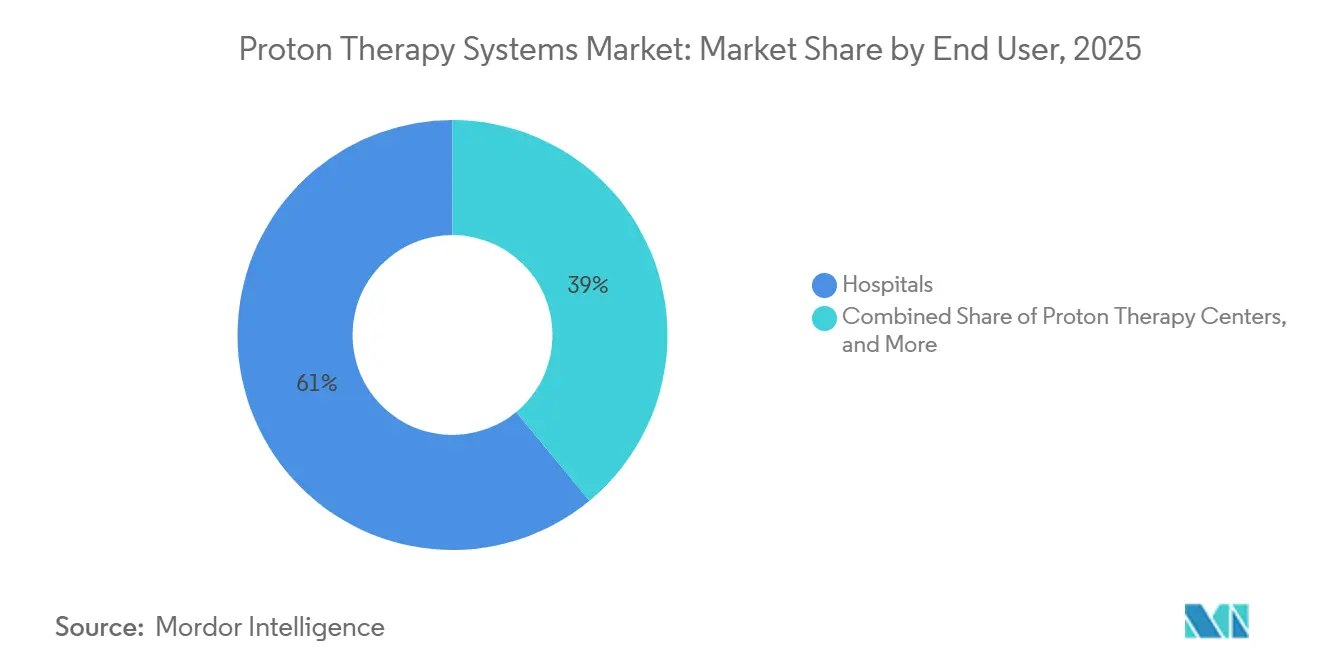

- By end user, hospitals accounted for 61.03% demand in 2025; research institutes will post a 10.11% CAGR to 2031.

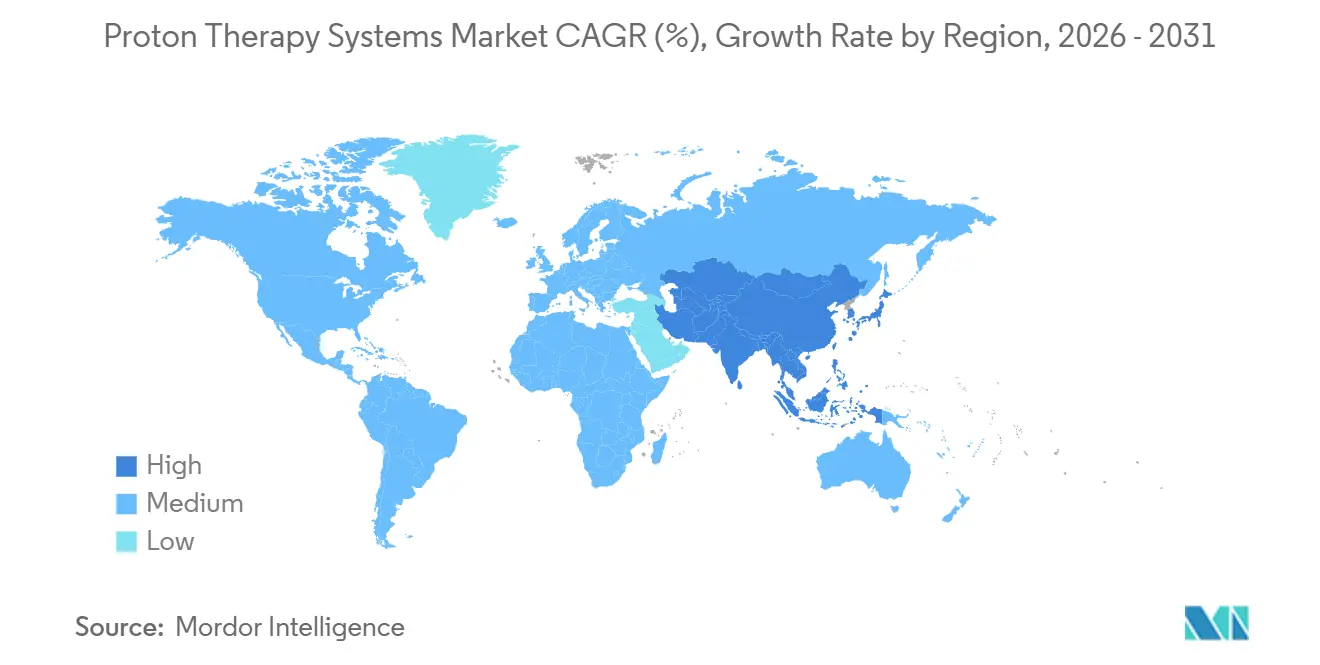

- By geography, North America led with 46.13% revenue share in 2025; Asia-Pacific is forecast to record the fastest 9.81% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Proton Therapy Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of Compact Single-Room Systems Lowers CAPEX | +1.8% | North America, Europe, Australia | Short term (≤ 2 years) |

| Expanding Reimbursement for Pediatric & CNS Cancers | +1.2% | North America, Europe, Japan | Medium term (2–4 years) |

| Shift To Pencil-Beam Scanning & AI Adaptive Planning Boosts Throughput | +1.0% | North America, Europe | Medium term (2–4 years) |

| Government-Funded Oncology Infrastructure Programs | +1.5% | China, India, UAE, Saudi Arabia | Long term (≥ 4 years) |

| Superconducting Synchrocyclotrons Cutting Operating Costs | +0.8% | North America, Japan | Medium term (2–4 years) |

| Early FLASH/UHDR Trials Opening Premium Niches | +0.5% | United States, Switzerland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adoption of Compact Single-Room Systems Lowers CAPEX

Compact single-room platforms are trimming construction costs by 30% to 40%, enabling community hospitals to commission proton centers for USD 33 million to USD 60 million rather than nine-figure budgets[1]BayCare Health System, “BayCare Opens Proton Therapy Center in Tampa,” baycare.org. FDA clearance of the Mevion S250-FIT in September 2025 demonstrated the feasibility of vault retrofit, cutting build times to under 18 months. Stanford Medicine targeted summer 2025 commissioning after a 14-month build, half the time of a typical multi-room project. Regional networks such as Froedtert Health opened Wisconsin’s first center in August 2025, capturing patients who previously traveled out of state. Similar strategies are unfolding in secondary Australian and Canadian markets, suggesting durable cost-driven diffusion.

Expanding Reimbursement for Pediatric & CNS Cancers

Medicare Local Coverage Determinations L35075 and L33937 cover 27 ICD-10 codes, including medulloblastoma, chordoma, and ocular melanoma, guaranteeing baseline volumes for U.S. providers[2]Centers for Medicare & Medicaid Services, “Local Coverage Determination Proton Beam Therapy L35075,” cms.gov . The U.K. National Health Service funds pediatric and skull-base indications at two national centers. However, adult breast, prostate, and lung cancers remain excluded, leading to cross-border referrals to Germany and Switzerland. Japan’s June 2024 insurance expansion reimburses USD 26,000–33,000 per course, lifting annual patient throughput above 3,600 cases. India’s Ayushman Bharat scheme similarly finances pediatric access at ACTREC in Mumbai, broadening the Asian demand base. Ongoing RADCOMP data for breast cancer and COMPPARE findings for prostate cancer are poised to widen payer criteria after 2027.

Shift to Pencil-Beam Scanning & AI Adaptive Planning Boosts Throughput

Pencil-beam scanning (PBS) magnetically steers micro-spotted beams, enabling intensity-modulated proton therapy that doubles daily capacity versus passive scattering at leading U.S. sites, IBA. AI-powered adaptive planning in RayStation cuts replanning time for head-and-neck cases from 4 hours to 90 minutes, freeing physicist bandwidth and elevating patient slots by 20%. The University of Florida Health Proton Therapy Institute is embedding these workflows in a USD 50 million expansion to target 150 treatments a day. Such efficiencies are crucial where reimbursement is bundled per course rather than per fraction.

Government-Funded Oncology Infrastructure Programs

China earmarked RMB 50 billion in its 14th Five-Year Plan for the rollout of proton centers in Guangdong, Shandong, and Jiangsu, supporting provincial Healthy China 2030 targets. India allotted USD 1.2 billion in 2024 to add centers in New Delhi, Bengaluru, and Chennai, aiming to curb outbound medical tourism. The UAE’s Dubai Health Authority ordered a ProteusONE for delivery in 2029, inaugurating Gulf Cooperation Council capacity. Saudi Arabia’s Vision 2030 seeks to treat 1,700 annual cases through multilateral support from the International Atomic Energy Agency’s Rays of Hope program. These public initiatives de-risk supplier backlogs that topped EUR 500 million at IBA in Q3 2025.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Multi-Room Installation Cost | -1.5% | Emerging markets in South America, Southeast Asia | Medium term (2–4 years) |

| Shortage Of Certified Proton-Therapy Physicists & Engineers | -0.8% | North America, Europe | Short term (≤ 2 years) |

| Sparse Cost-Effectiveness Data Outside Pediatrics/CNS | -0.6% | North America, Western Europe | Medium term (2–4 years) |

| Supply-Chain Dependence on <10 Accelerator Vendors | -0.4% | Global bottlenecks, especially Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Multi-Room Installation Cost

Two-gantry builds often exceed USD 224 million, matching those of three linear-accelerator centers and requiring 1,200–1,500 annual patients to break even[3]Penn Medicine, “Penn Medicine Breaks Ground on Roberts Center for Proton Therapy,” pennmedicine.org. Mayo Clinic’s USD 100 million add-on will treat 900 patients a year but requires a decade-long payback under current Medicare rates. Australia’s delay in the Adelaide Bragg Centre underscores how supply-chain inflation can quickly jeopardize capital budgets.

Shortage of Certified Proton-Therapy Physicists & Engineers

CAMPEP accredits fewer than 50 proton-specific physicists annually in North America, while 15–20 new centers are slated through 2031[4]European Society for Radiotherapy and Oncology, “ESTRO Workforce Requirements for Proton Therapy,” estro.org . Stanford postponed S250-FIT commissioning to summer 2025 for workforce recruitment. European capacity needs 200 additional physicists by 2030; training remains concentrated in the U.K., Germany, and Switzerland, creating regional mismatches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Accelerators Anchor Revenue, Positioning Systems Surge

Accelerators accounted for 37.55% of 2025 revenue, underscoring their USD 30–60 million price tag. Patient-positioning systems are projected to post a 9.25% CAGR, driven by robotic couches with six-degree motion correction, which are essential for adaptive therapy. Superconducting designs are replacing legacy isochronous cyclotrons, cutting operating costs and space. Elekta’s surface-guided systems and Siemens imaging add-ons are gaining favor as hypofractionation raises geometric accuracy demands. This momentum positions the segment to outpace overall growth in the proton therapy systems market.

The proton therapy systems market size for accelerators is projected to reach USD 820 million by 2031, while advanced positioning platforms could exceed USD 320 million, reflecting double-digit expansion in secondary installations. Vendors offering bundled service contracts and training programs stand to capture the incremental spending wave.

By System Configuration: Single-Room Platforms Disrupt Multi-Room Dominance

Multi-room facilities retained a 54.53% share in 2025, but single-room units will expand at a 11.85% CAGR as community hospitals seek faster returns. The proton therapy systems market share for single-room builds could surpass 45% by 2031 if present order books convert. Mevion’s S250-FIT requires just 2,500 square feet and leverages existing vaults, trimming capex by USD 40 million–60 million.

Single-room platforms typically treat 15–25 patients daily, yet higher throughput from AI-adaptive planning closes revenue gaps with multi-room peers. Gantry-less solutions from P-Cure further shrink footprints by 40%, indicating future architectural shifts that align with urban land constraints.

By Technology: Pencil-Beam Scanning Overtakes Passive Scattering

Passive scattering still accounted for 49.23% of installed capacity in 2025, but pencil-beam scanning is surging at 10.55% CAGR as it supports intensity-modulated protocols. Centers adopting PBS report 2-minute beam times per fraction, doubling room turnover. FLASH, while nascent, could layer an additional premium revenue stream if toxicity benefits materialize post-2028. Hypofractionated proton treatments at 5×10 Gy for pancreatic or liver tumors are gaining traction, demanding PBS spot-scanning accuracy and robust motion management. Legacy passive systems are being retired, evidenced by Loma Linda’s 2024 swap-out for an IBA PBS platform.

By Application: CNS Cancers Lead, Breast Indications Accelerate

CNS tumors led demand with a 30.03% share in 2025, buoyed by consistent reimbursement and strong clinical evidence. Breast is the fastest-growing indication, with a 12.11% CAGR, backed by RADCOMP data showing a 60% lower mean heart dose. Pending payer decisions post-2027 could elevate breast volumes to rival CNS cases by 2031.

Prostate uptake should improve after COMPPARE demonstrated 30% lower gastrointestinal toxicity than photon therapy. Pediatric protocols continue to expand under the imperatives of survivorship, keeping lifetime secondary malignancy risk reduction at the forefront of clinical decision-making.

By End User: Hospitals Dominate, Research Institutes Expand

Hospitals accounted for 61.03% of 2025 revenue, as integrated cancer centers bundle surgery, systemic therapy, and imaging around in-house proton therapy capacity. Research institutes are projected to log a 10.11% CAGR due to FLASH and AI-planning trials that require dedicated beam time and specialized dosimetry. Provision Healthcare’s multi-state rollout illustrates how standalone centers can reach 800-plus annual patients with focused referral networks.

Military, Veterans Affairs, and global referral hubs occupy a small but rising slice as defense agencies evaluate proton’s neuro-protective benefits for service-related injuries. These diversified end users will support aftermarket service revenue as installed bases mature.

Geography Analysis

North America retained a 46.13% share in 2025, supported by stable Medicare LCDs and a wave of single-room installations in community settings. New builds in Florida, Wisconsin, and California shorten travel distances for insured patients, while Penn Medicine’s two-gantry FLASH-ready center will reinforce regional dominance from 2027.

Asia-Pacific is the fastest-growing region, with a 9.81% CAGR, driven by Japan’s insurance expansion, China’s RMB 50 billion build-out, and incoming capacity in India and Thailand. Hitachi, Sumitomo, and B dot Medical are capturing local orders, confirming a pivot toward domestic suppliers. Australia’s delay in the Adelaide Bragg Centre underscores the region’s supply-chain sensitivities.

Europe shows mixed momentum. The U.K.’s restricted adult coverage caps growth, yet Germany, Switzerland, and Italy benefit from case-by-case insurer approvals. Switzerland’s Paul Scherrer Institute anchors European FLASH research leadership and attracts cross-border referrals. The Middle East is at an early stage, with Dubai’s 2029 launch setting a beachhead for GCC precision oncology initiatives.

South America remains nascent; Brazil’s USD 120 million São Paulo proposal stalled amid funding gaps, compelling patients to travel abroad. Multilateral finance from IDB and private partnerships will dictate the timeline for regional entry.

Competitive Landscape

Fewer than 10 vendors supply accelerators, conferring moderate oligopoly power. Ion Beam Applications (IBA), Hitachi Ltd., Mevion Medical Systems, Sumitomo Heavy Industries Ltd., and Siemens Healthineers (Varian Medical Systems, Inc.) dominate installed base metrics, though Varian’s recent strategic focus tilts toward photon devices under Siemens ownership. IBA booked EUR 500 million in backlog for Asia-Pacific and Middle East projects in Q3 2025, reflecting turnkey contracting strength. Hitachi leverages domestic ties to win sequential orders at Tokyo Metropolitan Hospital and the University of Tsukuba. Mevion’s S250-FIT now anchors the compact segment at U.S. community centers.

Disruptors such as P-Cure pursue gantry-less technology, cutting facility footprints by 40% and attracting pediatric applications. RaySearch Laboratories owns the AI software layer, with 1,000-plus RayStation deployments, and continues to integrate adaptive proton modules. Supply-chain lead times of 24–36 months remain a vulnerability; any vendor production slip can delay hospital revenue starts and dent ROI models.

Proton Therapy Systems Industry Leaders

-

Hitachi Ltd.

-

Ion Beam Applications (IBA)

-

Mevion Medical Systems

-

Sumitomo Heavy Industries Ltd.

-

Siemens Healthineers (Varian Medical Systems, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Atlantic Health Morristown Medical Center broke ground on a Mevion S250-FIT installation in New Jersey, targeting first treatment in 2027.

- September 2025: Leo Cancer Care and Sumitomo Heavy Industries entered a strategic collaboration to introduce a new Proton Therapy configuration. This collaboration highlights their commitment to advancing the accessibility of proton therapy worldwide.

Global Proton Therapy Systems Market Report Scope

As per the report's scope, proton therapy systems are advanced radiation therapy platforms used in cancer treatment that deliver high-energy proton beams to target tumors precisely. Unlike conventional photon-based radiotherapy, proton therapy allows radiation to stop at a specific depth, minimizing damage to surrounding healthy tissues. These systems are especially beneficial for treating pediatric cancers and tumors located near critical organs.

The proton therapy systems market segmentation includes product type, system configuration, technology, application, end user, and geography. By product type, the market is segmented into accelerators, beam transport systems, beam delivery systems, nozzle & image viewers, and patient positioning systems. By system configuration, the market is segmented into single-room / compact systems, multi-room systems, gantry-based systems, and fixed-beam systems. By technology, the market is segmented into passive scattering, pencil beam scanning, intensity-modulated proton therapy (IMPT), and flash proton therapy. By application, the market is segmented into central nervous system cancer, head & neck cancer, prostate cancer, breast cancer, pediatric cancers, gastrointestinal cancers, lung cancer, and others. By end user, the market is segmented into hospitals, proton therapy centers, research institutes, and others. By geography, the global market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Accelerator |

| Beam Transport System |

| Beam Delivery System |

| Nozzle & Image Viewers |

| Patient Positioning System |

| Single-room / Compact Systems |

| Multi-room Systems |

| Gantry-based Systems |

| Fixed-beam Systems |

| Passive Scattering |

| Pencil Beam Scanning |

| Intensity-Modulated Proton Therapy (IMPT) |

| FLASH Proton Therapy |

| Central Nervous System Cancer |

| Head & Neck Cancer |

| Prostate Cancer |

| Breast Cancer |

| Pediatric Cancers |

| Gastrointestinal Cancers |

| Lung Cancer |

| Others |

| Hospitals |

| Proton Therapy Centers |

| Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Accelerator | |

| Beam Transport System | ||

| Beam Delivery System | ||

| Nozzle & Image Viewers | ||

| Patient Positioning System | ||

| By System Configuration | Single-room / Compact Systems | |

| Multi-room Systems | ||

| Gantry-based Systems | ||

| Fixed-beam Systems | ||

| By Technology | Passive Scattering | |

| Pencil Beam Scanning | ||

| Intensity-Modulated Proton Therapy (IMPT) | ||

| FLASH Proton Therapy | ||

| By Application | Central Nervous System Cancer | |

| Head & Neck Cancer | ||

| Prostate Cancer | ||

| Breast Cancer | ||

| Pediatric Cancers | ||

| Gastrointestinal Cancers | ||

| Lung Cancer | ||

| Others | ||

| By End User | Hospitals | |

| Proton Therapy Centers | ||

| Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the proton therapy systems market?

The proton therapy systems market size reached USD 1.56 billion in 2026.

How fast is global demand for proton therapy equipment growing?

Market value is forecast to rise to USD 2.20 billion by 2031, reflecting a 7.15% CAGR.

Which configuration type is gaining ground most rapidly?

Single-room platforms are projected to grow at an 11.85% CAGR as hospitals favor lower capital outlays.

Why is Asia-Pacific the fastest-growing region?

Public-insurance coverage in Japan and large state infrastructure programs in China and India drive a 9.81% regional CAGR.

What clinical trend most boosts daily patient throughput?

Adoption of pencil-beam scanning combined with AI-driven adaptive planning doubles fraction capacity at high-volume centers.

Page last updated on: